Home / Labor Law / Payment and Benefits / Bonuses

Back

Published: 04/08/2016

Reading time: 6 min

0

3117

Bonuses are one of the best ways to stimulate workers , which has a positive effect on the effective functioning of the entire enterprise as a whole.

The bonus system is developed for each enterprise separately, taking into account the goals and objectives set for its employees. Employers take into account several factors at once, such as efficiency and achievement of goals, labor indicators, and the conditions under which bonus funds are issued.

There are often cases when employees remain dissatisfied with the amount of accrued bonus funds and even write complaints to the labor inspectorate. To avoid such troubles, the employer needs to foresee possible conflict situations in advance and draw up bonus regulations adjusted for controversial issues.

The possibility of rewarding for effective and conscientious work is laid down in Article 22 of the Labor Code.

The procedure for paying cash bonuses must be clearly stated in the employment contract, taking into account the opinions and wishes of the entire team (in accordance with Article 144 of the Labor Code).

The following types of bonus incentives are distinguished.

- Systematic Based on the results of the work performed

- For length of service

What types of awards are there?

There are two main groups of rewards.

Labor bonus . A one-time bonus may be given for introducing new technology or performing one-time work that is not part of daily duties.

Often, the employer introduces rewards for exceeding the production or sales plan. The bonus is an agreed percentage of the salary; it is paid not once, but monthly.

Social bonus . This type of bonus is not related to work achievements. The remuneration is paid one-time for any reason. For example, February 23, March 8, New Year, birthday and so on.

Types of bonuses for employees

According to the Labor Code, the payment of bonuses is one of the aspects of the remuneration system.

It is developed in accordance with the needs and specifics of the activities of a particular organization. The law does not establish specific criteria and amounts of incentives for employees. How to reward employees is an internal decision of the company management. Monthly bonuses are usually set at a certain percentage of the salary. It is also possible to pay monthly incentives in a fixed amount. It is issued simultaneously with the transfer of the salary (tariff) part.

It is permissible to pay one-time incentives based on the performance of the organization or the employee personally. A collective agreement sometimes establishes social benefits related to significant events in the life of an employee and not directly related to the performance of job duties.

Where to find out about awards

A bonus is not a salary, and the employer is not obliged to pay it monthly. When hiring an employee, he is introduced to the Labor Regulations and other local acts, including the provisions on bonuses or the collective agreement, which spells out the procedure for bonuses (Article 68 of the Labor Code of the Russian Federation).

The provision must describe all one-time and monthly bonuses that the employee may qualify for. And most importantly, the employee must understand what needs to be done to receive the bonus.

What documents to prepare

The main document defining the grounds for assigning bonus payments is the provision on bonus payments to employees. It states:

- grounds and criteria for bonuses;

- calculation and amount of payment;

- documentary support for bonuses;

- list of employees;

- grounds for deprivation of bonuses;

- sources of financing.

For example, when calculating 13 salaries, the regulations indicate the wording of the grounds for bonuses to employees, for example, the following:

- have worked at the enterprise for more than a year;

- all employees - calculated in proportion to time worked;

- all employees receive 100% of their salary.

It is advisable to develop accrual criteria taking into account the opinion of the team.

One of the conditions is a memo from the employee’s immediate supervisor offering a bonus. The general basis for bonuses is an order from the head of the organization. The document contains a link to the regulations, additional documents (if any), a list of employees receiving bonuses, and the amount of bonuses.

Is it necessary to draw up a bonus clause or a collective agreement?

Nobody bothers you to pay a bonus without a collective agreement or Regulations. But the employer is at risk. Art. 252 of the Tax Code of the Russian Federation establishes that all expenses, including bonuses, must be documented, in which case they can be accepted to reduce the income tax base.

When checking, a Federal Tax Service employee may not agree to include the bonus as an expense if he does not see it either in the labor agreement, in the collective agreement, or in the Regulations on Bonuses.

Therefore, write down the bonus procedure and amount of remuneration in one of three documents.

- Employment contract - if you fix the bonus in this document, you will be obliged to pay it, otherwise the employee has the right to go to court. The size and order of bonuses can be changed only by mutual agreement.

- A collective agreement is a multilateral agreement and is even more difficult to change.

- The bonus clause is signed by the employer, so it is easy to make changes to it.

Keep records of exports and imports in the Kontur.Accounting web service. Simple accounting, payroll and reporting in one service

Bonuses paid from profits: problems of accounting and taxation

Author: L. V. Karpovich

Each of us is pleased to receive a bonus, say, for a birthday, for the New Year, or at the end of a quarter. Some organizations stipulate the payment of such bonuses in documents regulating wages, while others issue them spontaneously.

In both cases, the accountant has to solve many problems associated with accounting for such bonuses. Is it always legal to pay bonuses from profits, and what taxes should be calculated on these amounts?

In this article, based on the reasoned points of view of representatives of the Ministry of Finance and the Arbitration Court, we want to give answers to the questions posed.

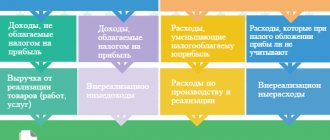

Production and non-production bonuses

Bonuses can be of a production or non-production nature. Production bonuses are an incentive element of remuneration and are paid to employees for achieving specific work results. They must be specified in labor and collective agreements, as well as in the regulations on bonuses in the organization.