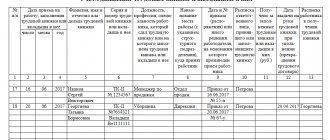

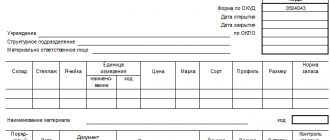

Under the designation M-17 lies a primary accounting document called the “Material Accounting Card”. It is used to control the movement of inventory items stored in the warehouse of enterprises and organizations. The preparation of this document is the responsibility of storekeepers and other warehouse workers, who issue it both upon receipt and upon shipment of goods and materials. It must be filled out directly on the day of the transaction for the movement of inventory and inventory.

- Form and sample

- Free download

- Online viewing

- Expert tested

FILES

Basic rules for issuing an M-17 card

Today there is no single, obligatory sample of a material accounting card, so enterprises and organizations have the opportunity, at their discretion, to develop a document template and use it in their activities (sometimes they do this by ordering a printing house to print their own forms or printing them on a regular printer). But most often, warehouse workers, in the old fashioned way, fill out the previously generally accepted form M-17, which reflects all the necessary information about the supplier, consumer and inventory items.

For each type of product or material, its own accounting card is filled out, which is then necessarily numbered in accordance with the numbering of the warehouse card file. All necessary receipts, consumables and invoices are attached to the card.

The document can be written by hand or filled out on a computer. Moreover, regardless of how the data will be entered into it, it must contain the “living” signature of the storekeeper, as a materially responsible person who is responsible for the safety of the property entrusted to him. It is not necessary to put a stamp on the document, since it relates to the internal document flow of the organization.

Inaccuracies and blots in the materials accounting card should not be allowed, but if some mistake does occur, it is better to fill out a new form, or, as a last resort, carefully cross out the incorrect information and write the correct information above, confirming the correction with the signature of the responsible employee. In the same way, it is unacceptable to draw up a document in pencil - this can only be done with a ballpoint pen.

After the end of the reporting period (usually one month), the completed materials accounting card is first transferred to the enterprise’s accounting department, and then, like other primary documents, to the enterprise’s archive, where it must be stored for at least five years.

Receipt of materials

In accordance with paragraph 2 of section. 2 guidelines for accounting of inventories, approved by Order of the Ministry of Finance dated December 28, 2001 No. 119n, the concept of “materials” includes a wide range of enterprise inventories with a useful life of less than a year. Materials include:

- raw materials necessary for the production of semi-finished or finished products;

- auxiliary materials that are not included in the finished product, but are used to ensure the operability of the equipment, as well as any technological needs;

- fuels and lubricants;

- spare parts;

- container;

- purchased semi-finished products;

- waste production;

- others.

In an organization that has warehouses, the manager’s order approves a list of materially responsible persons (MRPs) responsible for the safety and maintenance of warehouse records of materials for each warehouse.

Inventory and materials received from suppliers have a set of shipping documentation, represented by an invoice (form TORG-12, M-15 or another accepted by the supplier), an invoice, a waybill, and a specification. Of these, the invoice serves as the basis for capitalization. In the absence of shipping documents, materials can also be capitalized.

Read about the rules for such posting in the article “How to post goods without accompanying documents.”

Upon acceptance, materials must be checked for compliance of the actual quantity, quality and assortment with the data stated in the supplier’s accompanying documents.

If no discrepancies were identified during the verification process, the MOL issues a receipt order in Form M-4. It is allowed to put a stamp on the supplier's documents instead of receipt orders. The stamp must reflect all M-4 details.

If, after the inspection, discrepancies are still identified, it is necessary to issue a statement of discrepancies in the TORG-2 form.

For the form and sample of filling out this form, see the material “Unified form TORG-2 - form and sample” .

Another way of receiving materials is their purchase by accountable persons at retail outlets. In this case, the primary source is invoices or sales receipts attached to the expense report.

ConsultantPlus draws your attention to the fact that starting from 2021, materials must be taken into account strictly in accordance with the new Federal Accounting Standards 5/2019 “Inventories”. The new rules were explained in detail by legal experts. To see the recommendations, get trial access to K+ for free and go to the ready-made solution.

How to fill out the M-17 card correctly

This form is filled out on the basis of primary receipt documents for each item number of the material on the day of the transaction. All primary documents on the receipt and consumption of materials are attached to card M-17. Accounting for receipts, expenses and balances of materials in the warehouse is carried out by the warehouse manager or storekeeper.

The storekeeper fills in the details of the storage location of the material in the warehouse - rack, cell.

The column “Inventory norm” indicates the amount of material that is necessary for uninterrupted production. This quantity of material must always be present in the warehouse.

The “Shelf life” column is filled in for materials for which it is important to take this period into account, for example, for putties, varnishes, etc. For other materials, a dash is placed in this field.

When materials are received or consumed, the following is filled in the main table of the card:

— record date is the date of the receipt or expense transaction;

- document number and serial number - the number of the document on the basis of which the material was posted or issued is indicated, and the serial number of this document in the card is also indicated;

- from whom it was received or to whom it was issued - this column indicates the names of the organizations or departments from whom the materials were received or to whom the materials were issued;

— accounting unit of production (work, services) – indicates the name of the product for the production of which materials are supplied, as well as its accounting unit (piece, kilogram, etc.);

— receipt—indicates the quantity of materials received at the warehouse;

— consumption – indicates the amount of materials released from the warehouse;

- balance - this column indicates the balance of material after each operation - receipt or expense;

- signature, date - in this column, opposite each operation, the storekeeper puts his signature and indicates the date of signing.

Parish Operations

Warehouse receipt orders are papers that help register the receipt of goods and materials. This is not primary documentation; it is drawn up using an invoice or a surplus act. No one has the right to write out this document without reason.

It states:

- name of the consignee company;

- the name of the counterparty from whom the supplies were received;

- number is a required condition;

- Date of preparation;

- name of premises;

- code of the accounting account on which the values will be recorded.

Not all organizations decide to use an expense order; it does not apply to strict reporting documents.

Purpose of the document

Materials, goods and raw materials are an integral part of the activities of any business entity. Some companies have very little inventory, just a few pieces of household equipment. In large enterprises, the number of types of material reserves can reach several thousand. But regardless of the volume of reserves, management must ensure the safety and intended use of valuables. Otherwise, theft and damage to property cannot be avoided.

To reflect operations on the movement of materials, special accounting forms are provided. This is a card for warehouse accounting of goods and other material assets. The form allows you to track the movement of a specific item from the moment of delivery to actual use.

The materials warehouse card records not only information about the receipt, movement and disposal of assets. The form details information about the qualitative characteristics of goods and materials, cost and quantitative expression.

Which form to work with

There is no single form of warehouse card for materials accounting. With the introduction of the Law “On Accounting” No. 402-FZ, companies are not required to use unified standards. The forms approved by Goskomstat and the Ministry of Finance remain only recommendations.

Organizations have the right to develop their own forms and documents that will meet the individual specifics of their activities. For example, in healthcare institutions it is necessary to supplement the warehouse record card with information about the category and class of medical drugs and requirements for their storage.

In practice, most companies continue to operate using established forms. That is, they use the unified form M-17 - a warehouse inventory card. They are convenient, universal, and reveal all the necessary information without unnecessary and unnecessary detail. The current form is approved by Resolution of the State Statistics Committee of Russia No. 71a. You can download the M-17 materials warehouse card.

What assets of the institution can be taken into account in the MC accounting card

The card can be used both to account for the institution’s own assets and for assets taken into account off the balance sheet:

- OS (fixed assets);

- inventory items in the custody of the institution;

- various materials, including as customer-supplied raw materials;

- assets that were leased;

- assets in storage or for free use;

- fixed assets and inventories in transit;

- materials used in the manufacture of experimental devices;

- awards, cups, prizes and other transferable signs of merit;

- parts and spare parts that were installed on vehicles to replace those that had failed.

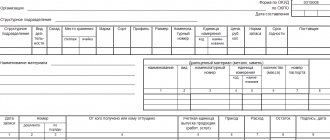

Card of quantitative and total accounting of material assets according to form 0504041

The quantitative and total accounting card, approved by order of the Ministry of Finance of the Russian Federation dated March 30, 2015 No. 52n, is used in government agencies to provide analytical accounting of the following assets:

- fixed assets;

- materials used in the manufacture of experimental devices;

- spare parts and components installed on vehicles to replace those that have failed;

- transferable badges of merit (awards, prizes, cups);

- inventory items in safekeeping;

- OS, MPZ on the way;

- materials;

- materials as customer-supplied raw materials;

- leased assets;

- assets for free use and storage.

Thus, f. 0504041 is used both for own assets and for those that are taken into account off the balance sheet.

This document is filled out by an accountant. First of all, you need to carry forward the balance to the beginning of the year. Then, during the period, data on the movement of the asset is entered into the card based on primary documents, and at the end of the period the balance is displayed. Receipts are indicated in the “Debit” column, disposals - in the “Credit” column. Information is filled in in rubles and in units of measurement. Information about the useful life of the asset and the expected write-off date is also provided.

A separate card is drawn up for each name. In addition, a separate card must also be filled out for each financially responsible person, even if the names of the assets under their control are identical. Also, for certain types of material assets, the following analytics are provided, listed in the table, that is, separate cards are compiled for each characteristic.

| Types of material assets | Characteristics |

| Valuables for rent | Lessor's inventory number |

| Non-financial assets in transit | Provider |

| Inventory in safekeeping | Owner |

| Provided raw materials and supplies | Customer, type, grade of materials and their location |

Basic list of types of warehouse documents

To understand what exactly is used in the work of an organization, let’s look at why they are created and how they are used to design all internal procedures.

Varieties

| View | Name | Base |

| Reception | Invoice from suppliers | Based on this, acceptance occurs. |

| Purchase Invoice | Needed to take into account incoming products. | |

| TTN No. 1-T | It is issued to confirm the movement of inventory items. The first section reflects the transported items, the second – logistics and calculations of the activities carried out. | |

| M-4 | It reflects the materials and goods actually received during the day. It is not written on its own, only if there is a reason. | |

| M-7 | Formed if the receipt was not in the required volume or with incorrectly drawn up reasons after drawing up a report of all the shortcomings. | |

| TORG-1 | They write it out when the item has been rechecked and no defects or damage have been found. This is confirmation that everything is now considered accounted for. | |

| TORG-2 | The consignee creates it if he wants to reflect discrepancies and inconsistencies at the time of acceptance. | |

| Storage The main list of warehouse documents necessarily contains documentation that allows you to monitor the condition of the product and how it moves within the company | TORG-11 | It is designed for each name and contains a lot of information. Required to fill out inventories during the audit. |

| M-17 | With their help, you can easily track the location in the warehouse. A separate card is filled out for the size range, models - each raw material, element of the assortment. | |

| TORG-13 | Created if it is necessary to transfer between enterprise branches at different addresses. In 2 copies, one for the sending party, the second for the receiving party. | |

| Disposal The circle of warehouse documentation ends upon release from the storage location | M-15 | It is issued when things are moved from one organization to another or at the time of sale. A mandatory item is the cost of the shipped property. |

| TORG-12 | Formed for direct release of materials and sales, as well as similar operations. | |

| TORG-16 | Reflects the write-off of low-quality, damaged and unused items. |

Features of filling out the M-17 card

Document M-17 is unified, so it can be found on any other accounting resource.

Information on the card is entered only on the basis of incoming and outgoing documents. When filling out Form M-17 for the first time or for a new product, difficulties may arise.

- If the cost of goods in lots differs, you can either enter a separate M-17 for each price, or change the table and add a column indicating the cost of the product.

- If materials are received in one unit of measurement and released in another (for example, tons and kilograms), then it is allowed to indicate both attributes in one cell.

- If you want to change the unit of measurement altogether, a transfer act is drawn up, on the basis of which changes are made to the card.

- If it is necessary to issue products using several identical invoices, it is allowed to make one entry listing the numbers of all documents.

- If a product does not have an expiration date, a dash is placed in the column. The same applies to the details grade, profile and others.

- In the “Signature” column, it is placed by the storekeeper, and not by the third party who accepted or shipped the goods.

- Corrections to the card are not allowed. If there are errors, the line is completely crossed out and a new line is filled in below. Opposite the damaged entry, the storekeeper and the supplier/recipient of the goods put their signatures.

It is convenient to maintain warehouse cards for goods in electronic form. In this case, you can easily edit their graphs using software methods. In addition, if necessary, you can print the document on paper. Therefore, it is advisable to install programs in the warehouse for accounting for goods, which significantly speed up work processes.

They provide ample opportunities for automation of trade and commodity operations. In such programs, M-17 materials warehouse cards are generated automatically based on the input primary documents, that is, they are not specially filled out.

Intra-warehouse movement of goods and materials

Some accountants or merchandisers may ask, “What is movement?” In the course of business activities, an enterprise needs to move materials between warehouses or structural divisions. The primary document in this case is the demand invoice (form M-11). It is issued by the MOL of the sending party in 2 copies: the 1st remains with the transferring party and serves as the basis for writing off materials from the register, the 2nd is transferred to the MOL of the receiving party and is the basis for accepting the goods and materials for registration.

For information on filling out a demand invoice, read the material “Procedure for filling out form M-11 demand invoice.”

What information is reflected

Thus, regardless of the sample (unified or proprietary), it should reflect the following information:

- name of the warehouse and its owner (i.e. LLC, individual entrepreneur, etc.);

- exact parameters describing the placement of products in the warehouse;

- Full name of the employee financially responsible for the receipt and release of materials, his signature;

- key characteristics by which it can be accurately identified among many other products and materials (article number, grade, brand, etc.);

- persons who released and accepted the goods;

- information about the document on the basis of which the entries in the accounting card were recorded (name, number and date of preparation of the document).

Disposal of materials

The write-off of materials from the warehouse must be accompanied by one of the documents: a limit card (Form M-8), an invoice for the release of materials to the third party (Form M-15), a demand invoice (Form M-11) or a consignment note (Form TORG- 12).

- Limit-receipt card is a document intended for the release of one item of materials to another warehouse of the enterprise or to a third party. For example, baking bread requires flour. Form M-8 reflects the daily write-off of flour from the storage warehouse to production. This document is maintained for a month in 2 copies: one each for the releasing and receiving parties. The card contains data on the quantity of materials issued, which are endorsed by the signatures of the person who issued and accepted the MOL. At the end of the period, the cards are handed over to the accounting department.

- The demand invoice is issued once for each release of goods and materials in 2 copies: one for each of the parties.

- An invoice for the release of materials to a third party is issued as a result of the disposal of materials to a third-party legal entity (when selling or, for example, transferring materials as customer-supplied raw materials) or to a geographically remote division of the company. The document is issued in 2 copies. If the release was made to a third-party organization, a power of attorney from the recipient of the goods and materials must be attached to Form M-15.

The form M-15 can be found in the material “Unified form M-15 - form and sample” .

- When selling materials to a third party, an invoice is issued in the TORG-12 form in 2 copies: the 1st remains with the seller’s company, the 2nd is transferred to the buyer. If inventory items are transported by road, it is also necessary to draw up a TTN (Form 1-T).

For information about the documents drawn up during transportation, read the article “Confirmation of transportation expenses - with what documents.”

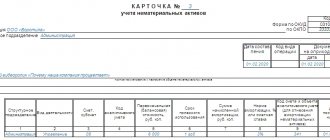

Card for recording material assets (form 0504043)

Form 0504043 has been approved and is used for accounting in places where assets are stored (as a rule, in warehouses); it must be filled out by the financially responsible employee himself based on warehouse accounting data. The accounting form is used in government institutions where there is a small number of MCs.

Important!

A quantitative and total accounting card is generated separately for each material value. In this case, a separate sheet of such a card is created for each name of the MC.

A card in form 0504043 is generated to reflect information about the following material assets of the institution:

- library items;

- various materials;

- various types of dishes;

- soft equipment;

- finished products.

Consignment note

This is a document from the storekeeper at the warehouse, which proves that goods and materials were transferred using road or other transport. This is significant documentary evidence - the basis for writing off or recording for storage. If something was imported from abroad, it is allowed to be accepted on the basis of reports submitted by the sender of the goods. A certified real TTN is not always able to take into account features and sudden changes. Some industrial establishments create their own documentation forms. If the state likes it, it is accepted and they begin to use it.

Printed in 4 copies. You keep one for yourself, the rest are given to the carrier. Based on this document, the assortment is delivered to the warehouse, and the cargo carrier delivers its copies to management for signing. Form T-1 - it contains a lot of details of both parties - names, BIC, TIN, legal and actual addresses, many other questions. But it is worth noting that not everything must be filled out.

How to fill out a card according to form 0504041

Important!

Even if the names of assets managed by different financially responsible persons are identical, a separate accounting card must be issued for each employee.

Important!

A separate accounting card is created for each name of material assets.

To correctly fill out a wealth registration card, you must adhere to the following rules:

- The “Debit” column is intended for listing receipts.

- The “Credit” column must indicate disposals.

- Information is entered in rubles and in units of measurement.

- The date of write-off (predicted) and information about the permissible operating time are required.

- Separate cards are compiled for each characteristic. For certain types of MC, the following analytics are taken into account:

| № | Types of MC | Characteristics |

| 1 | Provided raw materials and supplies | Customer, type, grade of materials, location |

| 2 | Inventory assets in safekeeping | Owner |

| 3 | Non-financial assets in transit | Provider |

| 4 | Material assets rented | Lessor's inventory number |

Instructions for filling

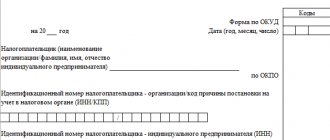

The card consists of a header of three tabular parts:

- The header contains information about the organization:

- full official name (for example, Limited Liability Company “Vintage”), but the abbreviation LLC is also allowed;

- OKPO activity code;

- date – it must exactly correspond to the fact (i.e. exactly on the day of the corresponding incoming or outgoing transactions).

- Information about the warehouse as a structural division of the company, as well as about the inventory items themselves:

- official name (in accordance with the accepted nomenclature system);

- name of the structural unit (usually “Warehouse”);

- parameters of material value - brand, grade, dimensions, product number, expiration dates and others; If there is no description for this parameter, a dash is entered.

NOTE. For precious materials, as well as products made from them, a separate table is filled out, in which, along with the usual parameters, the data of the accompanying passport is indicated.

- Finally, the main part of the form is devoted to the transactions that were carried out on that day (receipt or expense). The final table contains information:

- about the recipient or the person who released it;

- about the amount of expense or income;

- about the balance as a result of each incoming or outgoing transaction.

Sample document 2021

It is possible to develop a template of your own type, in accordance with the peculiarities of inventory accounting in a particular company. Accounting is always carried out according to the distinctive features of values:

- unique name;

- unique code or article - a combination of numbers and/or letters in accordance with the nomenclature system of the enterprise;

- brand;

- dimensions;

- variety and others.

The template developed within the company must contain all the sections that are given in the unified template.

Accounting for M-17 cards in the warehouse

A closed warehouse registration card, filled out in accordance with the requirements, must be kept at the enterprise for 5 years. Inspection authorities may require documents for this period. At the same time, the primary paper documents that were the basis for the operations must still be present in the archive.

- The cards are accounted for by the accounting department in a single journal, which must be laced, numbered and registered.

- Each M-17 card is assigned a unique number, after which it is signed by the chief accountant. Only then is the document transferred to the storekeeper.

- In the new year, card numbers may begin again, unless otherwise provided by orders of the enterprise.

- Entries in M-17 are made exclusively on the day of movement of goods.

- Every month, the storekeeper prepares a free-form report for each card, summing up the total turnover and displaying the balances.

- At the end of the year, the cards sum up the results, they are closed and the archive is transferred. The remainder is transferred to the new M-17 form. The old cards are accompanied by primary documents that were the basis for the records.

- M-17 can be used for several years. The deadlines for generating results for cards are independently approved by the management of the enterprise.

- Cards are not specifically maintained in the automated warehouse accounting program. They are generated upon request in the form of an analytical report.

- The accounting department must conduct full or random checks of the correctness of filling out cards on a monthly basis.

- You are permitted to print and file additional sheets for Form M-17.

- It is advisable that the storekeeper have a sample of filling out for each warehouse record card.

- Cards can be maintained in a warehouse by simple operators, but only with the permission of the financially responsible person.

With a small assortment and insignificant warehouse turnover, enterprises can keep records not in M-17, but in special journals. Their graphs are determined by the company independently.

The results are compiled monthly or quarterly in journals. The rules for designing and maintaining these reporting forms remain the same as for the warehouse accounting card.

It is more difficult to register it correctly and learn how to fill it out. But the best option is still to use computer programs to account for goods. They minimize errors when filling out warehouse documents and reduce the time spent by staff on routine operations.

Storage

An organization can create a warehouse designed to store materials from third-party organizations and receive a certain remuneration for storage services. This activity is regulated by Art. 909 of the Civil Code of the Russian Federation.

In this case, a public agreement is concluded between the counterparties. That is, anyone has the right to deposit their inventory items. Acceptance of materials based on quality, quantity and assortment is carried out by the storage warehouse's MOL. The depositor has the opportunity to inspect or check, as well as pick up his valuables at any time in the presence of the MOL.

The entire storage procedure is documented with primary documents. Let's look at the main ones.

Acceptance of goods and materials for storage is accompanied by an act of acceptance and transfer of goods and materials (form MX-1), which is issued in 2 copies: one for each party. The MOL records the receipt of inventory items for storage in a special journal (form MX-2).

Upon expiration of the storage period, as well as if the depositor wishes in writing, the storage warehouse returns the materials. This procedure is accompanied by a certificate of return of goods (form MX-3).

All data on the quantity and movement of inventory items are recorded by the MOL in special journals (MX-4, -5, -6, -7, -8).

Forms for forms MX-1 and MX-3 and the procedure for filling them out can be found in the materials:

- ,

- “Unified form No. MX-3 - form and sample”.

Requirements for state employees

State and municipal institutions are required to keep records according to special rules. The requirements for the organization of accounting are established not only by Law No. 402-FZ, but also by Instruction No. 157n. In addition to exceptional accounting rules, public sector institutions operate using unified primary documents. The forms are approved by a separate Order of the Ministry of Finance No. 52n.

But the filling principle is practically no different from the unified M-17 form. The form for state employees has OKUD 0504043. It is filled out separately for each type of inventory in storage. That is, for each asset received at the warehouse, you will have to create a separate document. Maintaining warehouse records cards in a budgetary institution is suitable for a small amount of material reserves.

Document flow diagram

Receipt of goods from the supplier to the warehouse:

- Inventory.

- Write-off of defects/damage.

- Formation of internal/external reporting.

- Return to supplier.

- Return from buyer.

- Sale.

- Entering a document into the system.

- Reception and recount.

If a company is aimed at constant development and is not going to stop at a couple of dozen items, then it needs to install software on the equipment and regularly update it for the most efficient operation.

With the help of correct and high-quality accounting, you can reduce the number of personnel errors and failures due to inattention. Number of impressions: 71699

Structure of the material warehouse card form

The document states:

- name of the organization that owns the warehouse;

- the name of the structural unit in which records of objects are kept, the type of its activity;

- number of the warehouse, rack and cell where the material is stored;

- information about the object being taken into account (its brand, grade, profile, size, item number);

- code and name of the unit of measurement for the volume of material;

- material cost;

- service life of the material;

- information about the material supplier;

- specific name of the material;

- additional information about the material if it is classified as precious;

- date, number of making an entry on the card;

- information about the entities that transmitted the material or received it;

- accounting unit for the delivery of goods (works, services);

- amount of receipt or expense for material, balance.

Each entry in the card is certified by the signature of the MOL. His signature is required to confirm that the document has been completed.

How are cards maintained?

Accounting and storage of documents is carried out according to the following rules:

- All records of the movement of valuables are carried out only on the day of actual transactions.

- A warehouse employee records current balances every day.

- Every month, a warehouse employee submits a final report, which indicates current balances, as well as all incoming and all outgoing transactions. The form of this report is arbitrary; it is developed within the enterprise.

- At the end of the calendar year, an annual (final) report is drawn up, all current balances are transferred to the date January 1. All completed forms are filed and archived.

- The principle is that each number (according to the internal nomenclature of the enterprise) must correspond to 1 card.

- All cards are subject to mandatory accounting - accounting employees create a special register where they record documents as they are received.

- Before handing over a document to a warehouse employee, it must be marked with a unique number (in chronological order), as well as a visa for the chief accountant or his replacement employee.

- Cards are maintained every year starting on January 1. Numbering is carried out by year, i.e. Every new year new numbers are put on.

- The warehouse employee must indicate in the document comprehensive information about the place where the goods or other material value is stored. Typically, each enterprise has its own designation system, which is a combination of letters and numbers. The row number, side (even/odd), rack number and mark of a specific place on the shelf are displayed.

- Each type of goods movement is registered separately - i.e. separate arrival and leave.

- If several identical movements are made, it is permissible to record them in the form of a single record, but it is important that all these movements occur within 1 business day.

- Finally, blots, unreadable text, tears, etc. are not allowed in the document. However, if a correct, legible correction is made, it must be signed by the chief accountant or his designee. The corrected entry must be clear and located next to the one in which the error or inaccuracy was made.

NOTE. In the case of small enterprises, when there is no need to create a separate system for recording the movement of materials, it is permissible to use ordinary warehouse books, as well as prepare monthly reports in any form and send them to the accounting department.

Internal movement invoice

It differs mainly in that it is issued only for movements within the enterprise - to the workshop, to the warehouse. The first thing to do is to enter the date. Looking at it, the one who sent the cargo will write it off, and the one who accepted it will credit it. Without this value, the sheet becomes invalid. The number of the future document must be created. For this, not only numbers, but also letters can be used. Then enter the shipper and the acquiring party.

Next, there is a table, it will indicate the list of things to be moved, each with a separate number. All the details are indicated:

- volumes;

- what is it measured in?

- at what cost?

The last line presents the total data - the sum of all columns. Signed by both parties.

Registration of a warehouse registration card

It is fundamentally important that the preparation of warehouse documentation is assigned to the responsibility of a specific employee. The person responsible can be appointed by a separate management order. Include in your job descriptions statements about responsibility for the correct execution and safety of warehouse forms.

If necessary, prepare special instructions or a memo for maintaining documentation in the warehouse.

Fill out the materials warehouse card taking into account the following recommendations:

- You can work using a self-developed template or warehouse accounting card. Fix the choice of form in the company's accounting policy.

- Warehouse inventory cards can be issued by hand or using a computer. Printed papers must be certified by the signatures of responsible persons and management.

- Maintaining documentation in electronic form is allowed. For example, using specialized accounting or accounting programs. Electronic registers require certification with a digital signature.

- It is not necessary to put the organization's stamp on the card. The form does not provide this information during registration.

- The use of corrective putties, tapes and other means is not permitted. The erroneous entry is crossed out and corrections are made nearby. The correction is certified by the signature of the responsible employee. The date and full name are placed next to it. and position.

- The form is opened for one calendar year. At the end of the period, a new document must be created.

Submit documentation from previous years to the institution's archives. The storage period for cards is 5 years from the end of the reporting period. Or five calendar years from the date of the audit.

Results

In order to record the movement of materials in warehouses, the unified form M-17, approved by the State Statistics Committee, can be used. It is filled out by the financially responsible employee and certified by him.

Sources

- https://assistentus.ru/forma/m-17-kartochka-ucheta-materialov/

- https://Class365.ru/blanki-dokumentov/forma-m-17-kartochka-ucheta-materialov/

- https://gosuchetnik.ru/shablony-i-formy/instruktsiya-zapolnyaem-kartochku-skladskogo-ucheta

- https://online-buhuchet.ru/forma-kartochki-ucheta-materialnyh-cennostej/

- https://nalog-nalog.ru/buhgalterskij_uchet/dokumenty_buhgalterskogo_ucheta/zapolnyaem_kartochki_ucheta_materialnyh_cennostej_obrazec/

- https://www.ekam.ru/blogs/pos/kartochka-skladskogo-ucheta-materialov-m-17

- https://2ann.ru/kak-zapolnit-kartochku-ucheta-materialov-po-forme-m-17/

- https://nalog-nalog.ru/buhgalterskij_uchet/dokumenty_buhgalterskogo_ucheta/kartochka_skladskogo_ucheta_materialov_blank_i_obrazec/