Registration of a taxpayer’s personal account (brief educational program)

To submit 3-NDFL via the Internet, the taxpayer must create an account on tax.ru (https://lkfl2.nalog.ru/lkfl/login). This can be done in 3 ways:

- Contact the tax office with your passport and request the creation of a profile from the operator. He will immediately issue the applicant a password, which must be changed within a month. Your login will be your TIN number.

- If you are the happy owner of a qualified electronic signature, click on the appropriate link.

- The most attractive way to log in is to log in through State Services, if you have a verified account. You will need to enter your credentials from the State Services and you will be taken to your account.

What to do with overpayment of taxes for individual entrepreneurs and legal entities

The taxpayer can dispose of the overpaid amount, provided that it was actually overpaid. At the same time, there are no tax arrears, penalties or fines to the INFS. Otherwise, the fact that the amount is displayed in the personal account must be ignored - it will disappear as soon as tax officials process the reports or when the due date for payment of fees arrives, according to the Tax Code of the Russian Federation.

According to Art. 78 of the Tax Code of the Russian Federation, taxpayers may:

- offset against payment of taxes, fees, arrears for the current or future period;

- return and receive to your bank account.

The taxpayer or employees of the Federal Tax Service can dispose of the surplus within three years (Clause 7, Article 78 of the Tax Code of the Russian Federation). If the deadlines are violated, the money is considered unclaimed and cannot be received.

Having decided to use finance, the payer does not have to return/credit the entire amount. It can also be divided into parts, sending one to pay off accruals for future periods, returning the other, and covering the arrears/fine/penalties with the third.

For transactions carried out by the Federal Treasury and the tax authority, commissions or interest are not charged to the payer.

Crediting funds

It is legal to offset the surplus to pay off other fees. Each individual case has its own nuances - the Federal Tax Service employees carry out the offset independently or upon application from the taxpayer.

Let's consider all possible options, based on Art. 78 Tax Code of the Russian Federation:

- Offset against the closing of future fees for similar or other charges is carried out upon the written application of the payer. If there are debts to the Federal Tax Service, first of all, funds are sent to repay them; the balance can be offset at your discretion.

- Transfers to repay underpayments, open debt on penalties and fines are made by tax authority specialists unilaterally. Any surplus generated over the past three years will be taken into account.

The application must be submitted to the Federal Tax Service located at the place of registration of a commercial organization or individual. It must indicate the details of the tax to which funds need to be transferred, including the type of tax and its type, BCC.

If it is necessary to offset an incorrectly paid fee to another address, the application should indicate the details of the first payment - date, amount, BCC, as well as the details to which the transfer must be made.

The tax authority sends information about the transfer of funds to the payer in writing within 5 business days from the date of actual offset. The message is transmitted only to the head of the commercial organization or his authorized representative, an individual - an individual entrepreneur.

Refunds in excess of amounts paid

Overpayment of tax, confirmed by the Federal Tax Service at the place of residence or registration, can be returned to the account. To do this, the payer must submit a corresponding application to the regulatory authority in writing (in person or by registered mail), through a personal account and via telecommunications using UKEP. Money is transferred within 30 calendar days.

If there is an underpayment of any type of tax, a refund is made after payment of the debt. The balance can be returned to the account of an individual or organization, depending on the legal form of the commercial enterprise.

How to send a 3-NDFL declaration for tax deduction in your personal account

The interface of the new account has been transformed and has become intuitive: filing a declaration is elementary. For greater understanding, it makes sense to break the entire algorithm into blocks, acting sequentially.

First, we create an electronic signature (read about how to do this here). In short, click on your full name in your personal account and get to the section with information about yourself. Scroll through the tabs to the “receive electronic signature” sub-item. The most rational and least labor-intensive option would be to choose “store the digital signature in the Federal Tax Service database.” Then we come up with a password and wait for the generation to complete. After this, we will begin sending the declaration.

We select life situations in the top line. We are interested in filing 3-NDFL, so we go to the point of the same name and move on.

At the next step, the taxpayer has a choice - fill it out online or send a ready-made declaration. Deklaracia3ndfl.ru is dedicated to the preparation of 3-NDFL in the program, that’s why our “download” button, but in the future we will also consider filling it out online.

Here we indicate the year for which 3-NDFL is sent. Please note that if you are applying for a tax deduction for several years at once, you need to create a new application each time. You need to send a file in xml format, which is made in the program (To save it from the software, after filling it out, click “XML file” and place it in a convenient place. It is from there that you will need to upload it to the taxpayer’s personal account).

Now you need to attach documents to the 3-NDFL declaration to receive a deduction (look for the list on the website). To do this, press the “attach” button. Papers, contracts and checks need to be scanned, but not everyone has a scanner at home, but a mobile phone with a good camera is more common. Therefore, you can send high-quality photographs with a total volume of no more than 20 MB.

The last step is to enter your email password and click confirm and send.

Deadlines for consideration and status of declaration verification

The verification process can be viewed in the messages section. After filing 3-NDFL through the taxpayer’s personal account, you will receive a notification that the application has been registered. You will then receive a letter in which you can track the status.

I would like to immediately note that in each specific case the time after sending may vary. However, there is a certain limit beyond which the tax office cannot consider the declaration.

According to the NKRF, namely Article 88, the maximum inspection period is 3 months. It doesn’t matter if it was submitted through a personal account, or if it was handed over to an inspector.

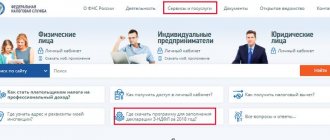

When a message is received about the successful result of the desk audit, the amount of overpayment to the budget will appear. The only thing left to do is submit an application for a deduction. To do this, from the main page, go to “life situations” and select the “dispose of overpayment” item. Next, fill in the bank details for a tax refund and submit the application. The period during which the money will arrive is 1 month.

I hope this instruction helped you send the completed 3-NDFL declaration through your personal account and you will receive the 13% due to you from the state without wasting effort, precious time and queuing.

What does “overpayment” mean in the taxpayer’s personal account?

An overpayment displayed in the personal account of an individual entrepreneur or individual taxpayer does not always mean an overpaid amount that is subject to refund . In some cases, this is a fee that has been paid but not yet transferred to the budget. Therefore, you first need to determine where it came from.

Strictly speaking, the term “overpayment” does not appear in the Tax Code of the Russian Federation, which raises questions about the amounts in the LC column of the same name. Based on the operating principle of the interactive service (personal account), these amounts can be understood as a positive balance. This formulation is not official, but most accurately reflects the meaning.

According to a publication on the official website of the Federal Tax Service of the Russian Federation, before submitting a document on the return of finances, it is necessary to obtain confirmation of the surplus from the tax authority. You can contact the Federal Tax Service in person or through feedback in your personal online account. The presence of a positive amount in the “overpayment” column is not an official notification.

Clause 3. Art. 78 of the Tax Code of the Russian Federation states that the tax authority informs the payer about the formation of excess amounts within 10 days from the moment such a fact is discovered. As a rule, the notification arrives by regular mail or letter via other communication channels, with an electronic digital signature.

New application forms from 03/31/2017

New application forms for offset and refund of overpaid taxes and contributions were approved by Order of the Federal Tax Service of Russia dated February 14, 2017 N ММВ-7-8/ [email protected] Their main difference from the previous ones is that now the new forms allow you to submit applications not only for offset and a refund of overpaid taxes, but also of contributions to social funds, which from 2021 are administered by the Federal Tax Service.

and statements valid from March 31, 2017:

- Application for refund of overpaid tax

- Application for offset of overpaid tax

What to do if your declaration is refused

Refusal to accept tax reporting will result in a violation of the deadlines for its submission. And this, in turn, is the basis for bringing an organization/individual entrepreneur to tax liability under Art. 119 of the Tax Code of the Russian Federation.

The penalty under this rule is 5% of the amount of tax not paid on the basis of the submitted declaration. Moreover, this fine is imposed for each full or partial month of delay in submitting the declaration. Ultimately, the fine may amount to 30% of the amount of tax not paid according to the declaration.

Therefore, if the Federal Tax Service Inspectorate refuses to accept the declaration on a legal basis, the payer must, as soon as possible, correct the errors/shortcomings made during submission and send the corrected version of the reporting to the Federal Tax Service Inspectorate. It’s better not to delay fixing errors. The longer the delay, the higher the fine.

If the acceptance of the reporting was refused unreasonably, the refusal can be appealed to a higher tax authority. In a complaint against the actions of the Federal Tax Service, you need to indicate in detail the essence of the complaint, and also pay attention to clause 19 and clause 142 of the Administrative Regulations for the provision of public services for accepting tax returns, approved. by order of the Federal Tax Service dated July 8, 2019 No. ММВ-7-19/343, which contains an exhaustive list of grounds for non-acceptance of declarations.

In addition, the actions of tax officials can be appealed in court. Judicial practice on this issue is formed in favor of payers. At the same time, the courts agree that the tax authorities do not have the right to refuse to accept a tax return submitted in the prescribed form (see, for example, Resolution of the Arbitration Court of the West Siberian District dated July 25, 2018 No. A67-9224/2017).

How to manage overpayment of taxes for individuals

Individuals can also use overpaid funds in two ways:

- Offset against other or similar taxes for the current or future period. For example, if there is a tax surplus on a vehicle, it can be transferred to pay off fees for a second vehicle. Property tax and land tax are calculated in a similar way.

- Return all or part of the surplus to your bank account.

Where to start is to clarify whether the overpayment is an actual surplus with the tax authority. If necessary, reconcile the calculations; it is carried out at the initiative of the Federal Tax Service or the payer himself.

It is more convenient to form an application in your personal online account. So it will already be pre-filled. All that remains is to enter the details of the recipient account to which the funds need to be transferred, or indicate the address for the repayment of which budget accrual the funds need to be transferred to.

To use funds, you must submit a refund/credit application. This can be done in different ways:

- Send by mail. It is better to send it with a description of the attachment - this way the payer will have documentary evidence of the contents of the letter, and the date of submission of the application will be the date of sending. The inventory form and shipping receipt must be kept until the money is received.

- In person, by contacting the Federal Tax Service office at your place of registration. In this case, you need to prepare two copies - the tax officer will stamp one with the date of receipt and signature. This is important documentary evidence of the transfer of the application.

- For example, telecommunication channels can be used to send tax reports. To sign, you need a valid UKEP, as well as installation of the latest CryptoPro plugins and related software.

- Through the taxpayer's account, having previously checked the digital signature.

Depending on the reason for the excess, additional documents may be required. For example, a copy of an erroneous payment receipt, documents for receiving benefits.

How to manage funds in your personal account

Users of their personal account can make a refund remotely by following the instructions:

- Log in to the system and log into your account.

- Go to the “Life Situations” section.

- Then in “Dispose of overpayment”, see whether the overpayment amount is indicated, click “Dispose”.

- In a new tab, enter the details of the recipient account - BIC of the bank, its full name, account number. Click on the “Confirm” button.

- Check the information provided - name of the tax authority, code, OKTMO, amount to be refunded, details.

- Enter the EDS password and send the document to the Federal Tax Service.

If the overpayment is confirmed by the Federal Tax Service, the payer has the right to use it at its own discretion. Offsetting funds is convenient when the amount of excess funds is insignificant or the next payment of the budget contribution is due. If the surplus is large, it is optimal to return it to your account.