Answer from Natalya *VAT cannot arise from the claim amount, and the amount goes entirely externally. income. You can recover VAT only from the cost of goods that you will not use in activities subject to VAT. But you can sell these torn bags a few kilograms at a time to your employees or anyone else, you can draw up an estimate for office repairs and write them off, which means this operation is subject to VAT, which means no one needs to restore anything. Reply from 2 replies Hello! Here are more topics with the necessary answers: Revenue limit for calculating advance payments with or without VAT? How to calculate: the whole Kt 90.1 or minus Dt 90.3? sold the goods to the supplier with VAT, and returned the goods with or without VAT? tags: Return of goods Suppliers I am opening my own online store and opening an individual entrepreneur, but I don’t know whether to open an individual entrepreneur with VAT or without VAT?? My suppliers work with VAT.

Delivery of goods with discrepancies in quantity and quality

Attention

The carrier lost 2 pieces - 20,000 rubles (including VAT 3,600 rubles). The buyer submitted a claim in the amount of 20,000 rubles (VAT 3,600) to the cargo carrier.

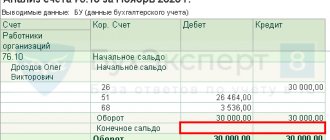

The carrier says that it accepts the claim minus VAT. Is the carrier right???? entries 41 -60, 19-60 - for the amount of accepted goods including VAT, 76/2 - 60 - claim for the amount of missing goods including VAT, 76 -76/2 claim accepted by the cargo carrier. those. The amount of the claim includes VAT, this does not mean that you are charging the carrier VAT, you are only paying off your losses, since you must pay the supplier for the goods, the ownership of which has transferred to you, as I understand it, from the moment the goods are shipped by the supplier, including VAT.

Recognition of the right to return prepayment

The counterparty has the right to claim the return of the advance (part of the advance) under the contract if the obligations under it were not fulfilled (Article 453 of the Civil Code of the Russian Federation). For example, if the organization did not deliver the goods to the buyer within the period specified in the contract, he has the right to demand a refund of the amount paid for the delivery (Article 463 of the Civil Code of the Russian Federation).

On the day when the counterparty’s claim is recognized (that is, the obligations under the contract are canceled or changed), reflect the debt to the partner:

Debit 62 (76) Credit 76-2 – the debt to the counterparty is reflected in the amount of the advance to be returned (based on the agreement of the parties).

For organizations that apply the general taxation regime, such an operation will affect the calculation of taxes as follows.

When calculating income tax using the accrual method, the amount of the advance (both received and returned) is not taken into account in the tax base (subclause 1, clause 1, article 251 and clause 49, article 270 of the Tax Code of the Russian Federation).

When calculating income tax using the cash method, the received advance increases the organization’s income, and the returned advance increases expenses (clauses 2 and 3 of Article 273 of the Tax Code of the Russian Federation).

After the contract is terminated and the advance payment is returned, the amount of VAT accrued and paid on it can be deducted (clause 5 of Article 171 of the Tax Code of the Russian Federation). In this case, register the invoice issued for the previously received advance in the purchase book and make the following entry in accounting:

Debit 68 subaccount “Calculations for VAT” Credit 76 subaccount “Calculations for VAT from advances received” – accepted for deduction of VAT previously paid on the returned advance.

An example of how to reflect the return of an unearned advance in accounting and taxation. The organization applies a general taxation system

On September 20 (Q3), Torgovaya LLC received 100 percent prepayment from Alpha LLC under the agreement dated September 1. The contract provides for the supply of a consignment of goods to Alfa in the amount of 590,000 rubles. (including VAT - 90,000 rubles) in October (IV quarter).

The amount of VAT calculated from the prepayment (90,000 rubles) is reflected in the declaration for the third quarter (September) and paid to the budget on October 17.

To account for settlements with the buyer, the accountant opened subaccounts: – to account 62 – subaccount “Settlements for advances received”; – to account 76 – subaccount “Calculations for VAT on advances received.”

Postings were made in the Hermes accounting.

September 20:

Debit 51 Credit 62 subaccount “Settlements on advances received” – 590,000 rubles. – the advance received from the buyer under the purchase and sale agreement is reflected;

Debit 76 subaccount “Calculations for VAT on advances received” Credit 68 subaccount “Calculations for VAT” - 90,000 rubles. – VAT is charged on the advance received.

17 October:

Debit 68 subaccount “Calculations for VAT” Credit 51 – 90,000 rubles. – VAT calculated from the advance payment was paid to the budget.

By the deadline established in the contract, Hermes did not have time to purchase the required quantity of products and did not deliver. On November 20, Alpha submitted a claim to Hermes for violation of the deadline for fulfilling the contract with a request to terminate it.

On November 21, the contract between Hermes and Alpha was terminated. On the same day, Hermes returned to Alpha the advance received in the amount of 590,000 rubles. (including VAT – 90,000 rubles).

Entries were made in the accounts.

November 21:

Debit 62 subaccount “Settlements on advances received” Credit 76-2 – 590,000 rubles. – the debt to the buyer is reflected in the amount of the advance, subject to return due to termination of the contract based on the received claim;

Debit 76-2 Credit 51 – 590,000 rub. – the debt to the buyer is repaid.

Hermes calculates income tax on a monthly basis and uses the accrual method. When calculating income tax for January–November, the accountant did not include the amount of the returned advance as an expense.

The amount of VAT paid to the budget from the returned advance was deducted by Hermes (based on the results of the fourth quarter):

Debit 68 subaccount “Calculations for VAT” Credit 76 subaccount “Calculations for VAT from advances received” – 90,000 rubles. – VAT previously paid on the returned advance is accepted for deduction.

For information on how to take into account the amounts of returned advances to simplified organizations, see On what income you need to pay a single tax when simplified.

When calculating UTII, the returned advance does not affect the calculation of the tax amount (Article 346.29 of the Tax Code of the Russian Federation).

Is the amount of compensation for damage subject to VAT?

InfoTechnical support 8-800-333-14-84 Free call within the Russian Federation ICQ: 609-394-313 E-mail: support Sales department Request a call

- Rates

- Integration with 1C

- For partners

- For the media

- Projects

- About company

- Video guide

- Blog

- Payment Methods

- Licenses and certificates

Privacy and Security

- Rules for using the service

- Rules for using information from the site

- Privacy Policy

Copying and further distribution of any texts from the freshdoc.ru website without the permission of the authors or the site administration, as well as borrowing fragments of texts will be considered a violation of copyright. Remember the responsibility provided for in Article 146, paragraph 3 of the Criminal Code of the Russian Federation.

Deducting VAT on a claim - is it possible?

Claim to supplier with or without VAT? Article 475 of the Civil Code of the Russian Federation states that in the event of detection of significant violations of product quality requirements that cannot be eliminated or their elimination entails disproportionate costs, as well as in other cases, the buyer has the right:

- demand a refund for paid goods;

- require replacement of a defective product.

When requesting a refund of the cost of a product, the question arises: does the buyer need to file a claim with or without VAT? In other words, should the claim requirement include the VAT amount? There are two options to consider:

- 1. If the amount paid included VAT, then the claim must include VAT.

The buyer has the right to demand a refund of the full price he paid for the defective product, including VAT; - 2.

Accounting and taxation according to the “constant-variable” scheme

It will be exactly the same as in the case when the supplier organizes the delivery of goods to customers at his own expense, taking into account transport costs in the final price of the goods. What happens to VAT in this case?

- The supplier issues the buyer a single invoice without any mention of transport services, that is, with the price of the goods, which already takes into account variable transport costs.

- VAT in the invoice is also allocated as a total amount calculated on the basis of the generalized cost of the goods sold.

- If there is an invoice, the entire amount of VAT can be fully refunded by the buyer.

- The supplier, in turn, also receives an invoice and a certificate of delivery services - but from the carrier, on their basis, takes into account the amount of transport costs in account 44 and deducts VAT on these services.

As you can see, the scheme is very simple and convenient. Now let’s move on to consider the issue of calculating VAT on some other types of reimbursable expenses.

Claim with or without VAT

If the amount paid did not include VAT, then the requirement does not include VAT. But it is worth considering that the situation is different for a non-resident. In the case of a non-resident supplier, VAT is not included in the amount paid.

The VAT that is paid at customs when importing goods of inadequate quality should be compensated as losses (Article 15 of the Civil Code of the Russian Federation). Sometimes an agreement with a non-resident may stipulate that the terms of delivery are not regulated by the laws of the Russian Federation, then the actions will be different - in accordance with foreign legislation.

The VAT claim was submitted by the buyer to the simplified tax system. The buyer may not be a payer of value added tax if working on a simplified basis.

Payment of a claim with or without VAT

Defect upon acceptance2. 94/68.2 Recovering VAT3. 60/76.2 We file a claim with the supplier4. The supplier satisfied the claim: 76.2/94 Reply from 2 replies Hello! Here is a selection of topics with answers to your question: VAT on reimbursement of the cost of goods under a claim. Accounts payable from buyers are reflected on line 1230 with or without VAT? What is the best way to work on a simplified basis with or without VAT? tags: VAT agreement with VAT or without VAT? Is depreciation calculated from the full cost with or without VAT? Tell me, in the general system, revenue in account 90.1 is displayed with or without VAT? What is the best way to work on a simplified basis with or without VAT?

Accounting and legal services

According to Art. 146 of the Tax Code of the Russian Federation, the object of VAT taxation is the sale of goods, works, and services. In addition, based on paragraphs. 2 p. 1 art. 162 of the Tax Code of the Russian Federation, the tax base for VAT increases, in particular, by amounts associated with payment for goods sold (work, services).

The amount of the claim paid by the contractor for failure to comply with safety regulations is not related to the sale of goods (performance of work, provision of services), therefore VAT is not charged on it. In accounting, this operation is reflected by the following entries: Dt 91.02 Kt 76.02 - the claim is recognized Dt 76.02 Kt 51 - the amount of the claim is paid In tax accounting, the amount of the claim transferred to the counterparty is included in non-operating expenses in accordance with paragraphs. 13 clause 1 art. 265 Tax Code of the Russian Federation.

- demand a refund for paid goods;

- require replacement of a defective product.

When requesting a refund of the cost of a product, the question arises: does the buyer need to file a claim with or without VAT? In other words, should the claim requirement include the VAT amount? There are two options to consider:

- 1. If the amount paid included VAT, then the claim must include VAT. The buyer has the right to demand a refund of the full price he paid for the defective product, including VAT;

- 2.

Recognition of the right to return goods

The buyer can return the purchased goods (products) on the following grounds:

- provided for by law (for example, clause 1 of article 466, clause 1 of article 468, clause 2 of article 475 and clause 2 of article 480 of the Civil Code of the Russian Federation);

- specified in the contract (clause 4 of article 421 of the Civil Code of the Russian Federation).

In accounting and taxation, a claim demanding the return of goods (products) is considered recognized after the return has been made (Article 1 of the Law of December 6, 2011 No. 402-FZ and Chapters 25, 26.2 and 26.3 of the Tax Code of the Russian Federation). The procedure for recording the operation to return a product (product) depends on whether the ownership of it has been transferred to the buyer or not.

For more information about accounting and taxation of this operation, see:

- How can a supplier record returns of goods from customers?

- How can a supplier record losses from external defects when returning them?

If the buyer demands that the returned goods (products) be replaced, then in accounting and taxation the satisfaction of such a claim should be reflected in two operations: the return of some goods (products) and the sale of others.

Claims are not subject to VAT

If the cargo is lost during transportation, is the forwarder obliged, along with the cost of the lost goods, to reimburse the client for the amount of VAT included in this cost?

As a general rule, the forwarder is liable to the client in the form of compensation for actual damage for loss, shortage or damage (spoilage) of the accepted cargo (Article 7 of the Federal Law of June 30, 2003 N 87-FZ “On Freight Forwarding Activities”). The Law specifies that for the loss or shortage of cargo accepted by the forwarder for transportation with declared value, damage is compensated in the amount of the declared value or part thereof, proportional to the missing part of the cargo.

Procedure for filing claims

The reason for violation of the terms of the contract may be:

- The supplier violated the delivery deadlines;

- Violation of payment terms;

- The delivered product does not meet the specified characteristics;

- The delivered goods do not correspond to the quantity;

- Not delivery of goods;

- Works and services not completed.

In the letter of complaint, the buyer must indicate which terms of the contract were violated and provide evidence of the supplier’s guilt. The letter of claim must be accompanied by original documents that confirm the claims made against the supplier:

The deadline for consideration of claims can be set:

- Legislation (clause 5 of Article 12 No. 87-FZ of June 30, 2003);

- Agreement;

- Internal regulations of the organization.

Payment for a claim with or without VAT

If the cargo was accepted for transportation without declaring its value, the actual (documented) value of the cargo or its missing part is subject to compensation.

The general principle on which the above rule is based is formulated in Art. 15 of the Civil Code of the Russian Federation: a person whose rights have been violated may demand full compensation for the losses caused to him, unless the law or contract provides for compensation for losses in a smaller amount. Losses are understood as expenses that a person whose right has been violated has made or will have to make to restore the violated right, loss or damage to his property (real damage), as well as lost income that this person would have received under normal conditions of civil circulation if his right was not violated (lost profits).

At the same time, as a general rule, both incomplete compensation for losses incurred and enrichment of the victim at the expense of the tortfeasor are excluded. In particular, expenses not incurred or incurred by the victim as a result of the offense, but compensated to him in full from other sources, cannot be included in damages. Otherwise, grounds would be created for the victim to repeatedly receive the same amounts of compensation and, accordingly, for them to derive property benefits, which is contrary to the goals of the institution of compensation for harm.

In this case, the burden of proving the existence of losses and their composition rests with the victim seeking protection of his rights. Consequently, it is he who must prove that the VAT amounts presented to him were not and cannot be taken for deduction, that is, they represent his uncompensated losses (damages). The fact that tax deductions are provided for by the norms of tax, and not civil legislation, does not prevent their recognition as a special mechanism for compensating the expenses of a business entity.

A person entitled to a deduction must be aware of its existence, must comply with all legal requirements to obtain it and cannot transfer the risk of non-receipt of the corresponding amounts to his counterparty, which in fact is for the latter an additional public law sanction for violating a private law obligation. Such conclusions were made in the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated July 23, 2013 N 2852/13.

In this regard, one of the circumstances that must be clarified is the following: does the freight forwarder's client have the right to deduct VAT included in the cost of the lost cargo? Naturally, there is no such right if the client applies the simplified tax system or does not claim VAT deductions for other reasons due to the peculiarities of his status as a taxpayer. If the freight forwarder’s client is the buyer of the goods, then he cannot deduct the VAT presented by the supplier until the goods are accepted for accounting. Accordingly, if the cargo is lost during transportation, was not taken into account, a tax deduction was not claimed, the forwarder is obliged to pay compensation including tax (Resolution of the AS UO dated 02/06/2015 N F09-9909/14 in case N A60-5124/2014).

But if the supplier hires a freight forwarder to deliver his goods to customers, then it is he (the supplier) who must prove the impossibility of applying VAT deduction. In the absence of such evidence, the amount of recoverable damages will be reduced by the amount of tax (Resolution of the Federal Antimonopoly Service ZSO dated January 20, 2014 N F04-8664/2013 in case N A45-30162/2012, Ninth Arbitration Court of Appeal dated November 10, 2014 N 09AP-40309/2014 on case No. A40-41346/14). However, here it is more correct to say that the supplier is not obliged to charge VAT, since the sale did not take place (the goods were not delivered to the buyer, ownership was not transferred), and disposal for reasons beyond the will of the taxpayer is not recognized as an operation taken into account when forming object of taxation (clause 10 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated May 30, 2014 N 33). As part of the declared (actual) value of the cargo, the forwarder compensates for actual damage (cost) and lost profits (surcharge). At the same time, the supplier does not have the obligation to restore the “input” VAT accepted for deduction when purchasing (manufacturing) goods earlier, since the loss of goods is not a VAT-free operation (Decision of the Supreme Arbitration Court of the Russian Federation dated May 19, 2011 N 3943/11).

In the event of loss of cargo accepted for transportation, the forwarder is obliged to compensate the client for losses. It is in the interests of the culprit to consider all options for legally reducing the amount of compensation. One of them is the exclusion of the amount of VAT from the amount of losses, if, of course, according to the documents for the cargo, the tax is included in its cost. As follows from examples of judicial practice, it is the victim who must prove that the amount of VAT constitutes his loss (cannot be deducted or accrued). Such a number will not work if the client uses the simplified tax system or for other reasons does not calculate VAT, and also if he acts as a buyer of transported cargo - he has no right to deduct the “input” tax, since he did not take the lost goods into account.

If you do not find the information you need on this page, try using the site search:

P.S

As a general rule, the documents required to recognize compensation for damage caused as non-operating expenses are:

- a bilateral act signed by the parties to the agreement, or another document confirming the fact of violation of contractual obligations and allowing to determine the amount of the recognized debt (letter of the Ministry of Finance of Russia dated December 23, 2004 N 03-03-01-04/1/189);

- decision to recognize the damage caused;

- a copy of the letter sent to the counterparty acknowledging the claim and indicating the amount of damage caused;

- payment documents (payment order, cash settlement).

When compensating for damage, the Court must compensate for damage including VAT

Judicial practice shows that when determining the amount of material damage to be recovered from the defendant in favor of the plaintiff, the court of first instance proceeded from the fact that material damage is subject to recovery without taking into account value added tax, since in this case actual damage is compensated, and the plaintiff materials for carrying out No construction or technical work was purchased and no repair work was carried out.

The panel of judges cannot agree with this conclusion of the court for the following reasons.

As stated above, Part 1 of Art.

Delivery of goods with discrepancies in quantity and quality

15 of the Civil Code of the Russian Federation establishes that a person whose right has been violated may demand full compensation for the losses caused to him, unless the law or contract provides for compensation for losses in a smaller amount.

Moreover, in accordance with Part 2 of this article, losses are understood as expenses that a person whose right has been violated has made or will have to make to restore the violated right, loss or damage to his property (real damage), as well as lost income that this person would have received under normal conditions of civil circulation if his right had not been violated (lost profit).

According to the explanations contained in paragraph 13 of the Resolution of the Plenum of the Supreme Court of the Russian Federation dated June 23, 2015 No. 25 “On the application by courts of certain provisions of Section I of Part One of the Civil Code of the Russian Federation”, when resolving disputes related to compensation for losses, it is necessary to keep in mind, that the actual damage includes not only the expenses actually incurred by the relevant person, but also the expenses that this person will have to make to restore the violated right.

Similar explanations were previously given in paragraph 10 of the Resolution of the Plenum of the Supreme Court of the Russian Federation and the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 1, 1996 N 6/8 “On some issues related to the application of part one of the Civil Code of the Russian Federation.”

The amount of expenses that the plaintiff will have to make to restore the violated right (the cost of restorative repairs) is indicated in the conclusion of the forensic examination in the amount of 14,259 rubles, taking into account overhead costs in the estimated profit and taking into account value added tax in the amount of 14,259 rubles.

Current legislation does not contain restrictions regarding the inclusion of value added tax in the calculation of damage.

Recovery from the defendant of the cost of restoration of residential premises, taking into account value added tax, meets the principle of full compensation for damage caused to the plaintiffs’ property, established by the norms of the Civil Code of the Russian Federation.

Thus, there are no grounds for excluding value added tax from the cost of restoration repairs.

On the procedure for recording transactions in the event of theft of goods

The organization contacted the internal affairs authorities with a statement about the theft. Based on the results of operational investigative activities, a criminal case was initiated against an individual who is not an employee of the organization. Some of the goods were returned to the organization, but no documents were drawn up for such a transfer.

The write-off of the stolen goods will be reflected in the accounting records by posting D-t account 94 K-t account 41. Also, the amount of the shortage must be increased by the amount of value added tax on this product: by posting D-t account 94 K-account 19 - if the value added tax was not reimbursed from the budget; posting D-t sch.94 K-t sch.68 - if the value added tax was reimbursed from the budget. The basis for these records should be inventory materials in accordance with clause 27 of the Regulations on maintaining accounting and financial statements in the Russian Federation, approved by order of the Ministry of Finance of Russia dated July 29, 1998 N 34n, and clause 1.5 of the Methodological guidelines for the inventory of property and financial obligations, approved by order of the Ministry of Finance of Russia dated June 13, 1995 N 49. The results of the inventory must be reflected in the accounting and reporting of the month in which the inventory was completed (clause 5.5 of the Inventory Guidelines).

In cases where property belonging to an organization is stolen by an unknown person, a criminal case is initiated into the theft or investigative measures are taken. The fact of theft of material assets is recognized only on the basis of a court decision.

Let's consider several possible options

- The person guilty of the theft of goods has been identified by a court decision (sentence). In accordance with Art. 15 of the Civil Code of the Russian Federation, compensation for losses associated with theft of valuables is made entirely by the culprit. Moreover, a loss means, in addition to the expenses that the organization will have to make to give the valuables a marketable appearance (in case of broken packaging, contamination, etc.), also lost profits (lost income that the organization would have received by selling the goods if they were not stolen).

In this case, the following entries are made in the organization’s accounting:

Dt account 76 subaccount “Calculations for compensation of material damage” Dt account 94 - the cost of the stolen goods is written off (including VAT), subject to compensation by the guilty party.

If the cost of stolen goods is recovered from the guilty person at a price exceeding their book value (if, when filing cases in court, the amount of damage was declared to be 5,000 rubles, and the purchase price of the goods was 4,000 rubles), then the difference between the value of the stolen goods, reflected on account 76, and their value reflected on account 94, is reflected as follows:

D-t 76 subaccount “Calculations for compensation of material damage”, K-t 98 “Deferred income” - for the amount of the difference between the declared damage and the cost of stolen goods in the amount of 1000 rubles. (5000 rub. - 4000 rub.);

Dt 98 “Future income”, Kt 91 “Other income and expenses” - debt collected from the guilty person in excess of the cost of the stolen goods in the amount of 1000 rubles.

- The guilty person has not been identified or the court rejected the claim due to its groundlessness.