INN/KPP

The rules for filling out invoices, approved by Government Resolution No. 1137 of December 26, 2011, do not determine which checkpoint should be indicated in the invoice issued to a separate unit: the parent organization or a separate unit.

ATTENTION! As of January 1, 2019, the invoice form has changed. See here for details.

In this case, in line 6b “TIN/KPP” the Ministry of Finance of the Russian Federation recommends indicating the KPP of a separate unit (see letters of the Ministry of Finance of Russia dated 05/04/2016 No. 03-07-09/25719, dated 02/26/2016 No. 03-07-09/11029, dated 09/05/2014 No. 03-07-09/44671).

How to enter information?

The following elements are required to be completed:

- post office index;

- name and type of subject of the Russian Federation;

- name of the locality;

- Street;

- House number;

- structure;

- frame.

Grammatical and spelling errors are allowed, which make it possible to unambiguously correctly evaluate the information received, for example:

- the postal code appears at the end of the address line;

- an error in writing the abbreviation - not “Krasnova street”, but “Krasnova street”;

- the presence of commas between the names and numbers of the house and office;

- capital letters instead of caps.

What does a correctly completed column look like?

A correctly completed column looks like this:

- 185000, REPUBLIC OF KARELIA, CITY OF PETROZAVODSK, KOROMYSLOVAYA STREET, 15, 8.

- 198231, CITY OF SAINT PETERSBURG, ORDZHONIKIDZE STREET, BUILDING 16, LETTER B, OFFICE 87.

- 653023, ALTAI REGION, CITY BARNAUL, STREET IVAN BRONEVOY, 12 D.

The following photo shows an example of filling out address lines in an invoice:

Buyer's name

The buyer of goods (work, services) purchased by an organization for its branches and other separate divisions (or through them) is a legal entity represented by the parent organization. Therefore, the invoice is issued to the parent organization, and in line 6 “Buyer” its details are indicated (see letters of the Ministry of Finance of Russia dated May 4, 2016 No. 03-07-09/25719, dated May 15, 2012 No. 03-07-09/55 , Federal Tax Service of Russia for Moscow dated October 23, 2009 No. 16-15/1099)9, FAS North Caucasus District dated April 1, 2009 in case No. A63-675/2008-C4-17).

In her interview, the nuances of issuing an invoice through a separate division are discussed in detail by the Advisor to the State Civil Service of the Russian Federation, 2nd class, O. S. Duminskaya. Check out the official's opinion by receiving a free trial access to ConsultantPlus.

If representatives of one party to the transaction are different organizations

Situations are possible when one person acts as a supplier, but the cargo is actually sent from the warehouse of another. This occurs, in particular, during transit deliveries, when the goods are sent to the recipient without registration at the warehouse of the intermediary seller. In this case, in fact, there are not two, but three parties involved in the transaction :

- supplier (seller);

- sender of the cargo;

- buyer-consignee.

In the event that the shipper and the seller do not coincide with each other, this fact must be reflected in the invoice indicating the name, address and details of each of them. Lack of data may result in the tax deduction not being provided.

IMPORTANT : Transactions are also possible where the buyer and consignee do not match. In this case, complete data must also be provided for each of them.

Now you know what to do in situations where the seller and the shipper are different legal entities. The same applies to cases where the buyer and consignee are different organizations.

In the materials of our specialists you can find out many interesting details about the invoice. Read about what codes are in an invoice, how to indicate transaction codes and various quantities in a document, why and in what cases an order is needed to sign invoices, how to fill out the “country code” column, and also what a customs declaration or number is customs declaration.

Buyer's location

From October 1, 2017, changes were made to the invoice form and the rules for filling out invoices (see Resolution of the Government of the Russian Federation dated August 19, 2017 No. 981). According to the new rules, in line 6a of the invoice you need to write: “The address indicated in the Unified State Register of Legal Entities, within the location of the legal entity” (subparagraph “k” of paragraph 1 of the Rules for filling out invoices as amended by the resolution of the Government of the Russian Federation dated August 19, 2017 No. 981).

Until 10/01/2017, officials recommended that when preparing invoices, indicate in line 6a “Address” the address of the buyer - a legal entity represented by the parent organization (see letters of the Ministry of Finance of Russia dated 02/26/2016 No. 03-07-09/11029, Ministry of Finance of Russia dated 26.02 .2016 No. 03-07-09/11029).

There are currently no official clarifications on the procedure for indicating the address when issuing an invoice to a separate division using the new form. But analyzing in totality clause 3 of Art. 55 Civil Code of the Russian Federation and sub. “k” clause 1 of the Rules for filling out invoices as amended. Decree of the Government of the Russian Federation dated August 19, 2017 No. 981, it can be assumed that in the situation under consideration, in line 6a “Address” of the invoice, the address should be given:

- a separate division that is not a representative office or branch must indicate the address of the parent organization entered in the Unified State Register of Legal Entities;

- branch or representative office specified in the Unified State Register of Legal Entities.

Read about the consequences of an error in specifying address data in the following materials:

- “Incorrect address information on an invoice does not result in loss of deduction rights”;

- “Address on the invoice: what is not an error.”

When is it necessary to write details?

The specifics of filling out an invoice depend on the specific agreements under which it is used. The fact is that we can talk about the consignor and the consignee only in the case when the actual transfer of goods (cargo) takes place under the contract. If we are talking only about the provision of services, the corresponding terms are simply not used.

In this case , the columns relating to the seller and buyer are always filled in in the invoice . This is due to the requirements established by Art. 169 of the Tax Code of the Russian Federation, and the terminology used in the Code. According to it, any person who provides services or transfers goods is considered a seller, regardless of who he is from the point of view of the Civil Code - actually a seller, a performer, etc. The same applies to the buyer.

Name and address of the consignee

If the consignee of the goods is a separate division of the organization (for example, a branch), line 4 “Consignee and his address” of the invoice indicates the details of this division (see letters of the Ministry of Finance of the Russian Federation dated May 4, 2016 No. 03-07-09/25719, dated April 13 .2012 No. 03-07-09/35). A similar point of view was expressed by officials earlier, regarding invoices issued according to the rules of Decree of the Government of the Russian Federation dated December 2, 2000 No. 914 (letters of the Federal Tax Service of Russia for Moscow dated March 24, 2009 No. 16-15/028080, dated March 20, 2008 No. 19-11/026593, Ministry of Finance of Russia dated 02.11.2011 No. 03-07-09/36).

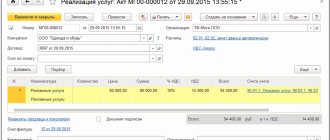

For a sample of filling out an invoice addressed to a branch, see below

The procedure for filling out an invoice for services is different. You can familiarize yourself with a sample of filling out an invoice for the purchase of services by a branch of an organization from an individual entrepreneur in the material prepared by ConsultantPlus experts. Get trial access to the system and study the information for free.

How to fill out the lines correctly?

If it concerns the shipper. According to the rules established by the current edition of Resolution No. 1137, the lines relating to the shipper are filled in as follows :

- The full name is indicated, but an abbreviation is also allowed.

- The address is indicated according to the Unified State Register of Legal Entities.

- If he and the seller are one person, then, according to paragraphs. “e” clause 1 of section I of the resolution, in the corresponding line you can write “he”. If the sender of the goods is not the seller, but another person, the mail address of the shipper is indicated. Finally, if the invoice is issued under an agreement relating not to goods, but to services or work, nothing is written on the line - a dash is placed.

- If the document is issued by an agent acting on his own behalf, but purchasing goods from two or more sellers, in the line “Consignor” all of them are indicated, but separated by a semicolon.

Now about situations when we fill out lines about the consignee. Resolution No. 1137 establishes similar standards for the consignee :

- The name is indicated - full or abbreviated.

- The address according to the Register is indicated.

- If the invoice is for services, a dash is placed in the column concerning the recipient of the cargo. The wording “aka” is not provided for by the resolution.

- If there are two or more consignees, the names and addresses of each are indicated separated by a semicolon.

When issuing invoices in practice, the question arises about the procedure for indicating the appropriate checkpoint of the consignee in cases where the buyer under the supply agreement is the parent organization, and the actual consignee is a separate division of this organization. Oddly enough, until now, the uncertainty in law enforcement practice on this simple and even “technical” issue has not been properly eliminated: the contradictory position reflected in official clarifications only adds “fuel to the fire.” What should you do in this situation and what consequences may arise in case of an error?

Legal meaning of indicating checkpoint on the invoice

According to paragraph 2 of Art. 169 of the Tax Code of the Russian Federation, invoices are the basis for the acceptance of VAT amounts presented to the buyer by the seller for deduction when the requirements established in the form and details of the invoice are met.

So, paragraph 5 of Art. 169 of the Tax Code of the Russian Federation stipulates that the invoice issued for the sale of goods (work, services) must indicate, in particular: the name, address and identification numbers of the taxpayer and the buyer; name and address of the shipper and consignee.

As stated in paragraph. 2 p. 2 art. 169 of the Tax Code of the Russian Federation, errors in invoices that do not prevent tax authorities from identifying the seller, buyer of goods (work, services), property rights, the name of goods (work, services), property rights, their value, as well as the tax rate and the amount of tax presented to the buyer is not a basis for refusing to accept tax amounts for deduction.

Failure to comply with invoice requirements not provided for in paragraph 5 of Art. 169 of the Tax Code of the Russian Federation cannot be a basis for refusing to accept for deduction the tax amounts presented by the seller.

As the Constitutional Court of the Russian Federation indicated in its Determinations of February 15, 2005 No. 93-O and No. 87-O of April 18, 2006, within the meaning of clause 2 of Art. 169 of the Tax Code of the Russian Federation, compliance of the invoice with the requirements established by paragraphs 5 and 6 of this article allows us to determine the counterparties to the transaction (its subjects), their addresses, the object of the transaction (goods, works, services), the quantity and volume) of goods supplied (shipped) ( works, services), the price of goods (works, services), as well as the amount of accrued tax paid by the taxpayer and subsequently accepted by him for deduction. Thus, the purpose of the invoice is to establish a certain range of information. If the invoices for which the tax deduction is being disputed contain complete and reliable information about the seller and make it possible to establish all the specified information, then the refusal to deduct is unlawful.

The indication of the checkpoint in the invoice of the Tax Code of the Russian Federation is not provided [1], which is largely explained by the fact that this indicator is not an “identifying” tax-significant feature specifically in relation to the taxpayer. The checkpoint is assigned not only to the taxpayer, but also to its separate divisions that are not VAT payers, that is, the checkpoint itself is determined only by accounting purposes and does not give rise to the obligation to pay tax. That is, although the checkpoint indicates that the document in which it is mentioned refers to a separate unit, the checkpoint is rather of a technical nature.

So, if the TIN (taxpayer identification number) identifies the taxpayer, then the checkpoint does not identify the taxpayer himself, cannot serve the purpose of such identification and is an additional indicator. This conclusion can be made based on the purposes of introducing it into tax legislation and the procedure for forming this indicator.

As stated in the Order of the State Tax Service of the Russian Federation dated November 27, 1998 No. GB-3-12/309: “ in connection with the peculiarities of accounting for taxpayers - organizations defined by the provisions of paragraph. 2 p. 1 art. 83 of the Tax Code of the Russian Federation, in addition to the taxpayer identification number (TIN) of the organization, a reason code for registration is entered, which consists of the following sequence of numbers from left to right: code of the state tax inspectorate that registered the organization at its location, the location of its branch and (or) a representative office located on the territory of the Russian Federation, or at the location of the real estate and vehicles owned by it (NNNN); registration reason code (PP); serial number of registration for the corresponding reason (XXX). The structure of the reason for registration code is a nine-digit digital code: NNNNPPXXX.” Taking into account the above, the checkpoint cannot refer to the “identification number” referred to in paragraph 5 of Art. 169 of the Tax Code of the Russian Federation.

The form of the invoice and the procedure for filling it out on the basis of clause 8 of Art. 169 of the Tax Code of the Russian Federation are established by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137 (hereinafter referred to as Resolution No. 1137).

The specified Resolution No. 1137, specifying the provisions of Art. 169 of the Tax Code of the Russian Federation[2], it is stipulated that line 6b of the invoice used in VAT calculations reflects the taxpayer identification number and the reason code for registering the taxpayer-buyer. However, in this case we are talking about the checkpoint of the taxpayer -buyer. In turn, with regard to VAT, separate divisions of an organization do not have taxpayer status, which follows from the norms of Chapter. 21 of the Tax Code of the Russian Federation (Article 143 of the Tax Code of the Russian Federation) and has been repeatedly confirmed by financial authorities[3]. Consequently, formally, taking into account the literal meaning and systemic interpretation of the above norms of legislation, there are no grounds for reflecting the checkpoint of the actual consignee – a separate unit. In this case, the legislation does not contain “irremovable doubts, contradictions and ambiguities” (Clause 7 of Article 3 of the Tax Code of the Russian Federation), which do not allow the taxpayer to choose the correct model of action that complies with the law: according to the direct instructions of the legislation, the buyer’s checkpoint must be indicated in the invoice , and not a separate unit - the actual consignee.

In addition, based on the civil law content of the concluded contracts, separate divisions also cannot be recognized as the buyer if they indicate that the parent organization is the buyer. In turn, as the Constitutional Court pointed out, in order to determine tax consequences, it is necessary to take into account their civil legal basis[4], i.e. separate divisions as independent economic entities do not participate in contractual supply relations. Reflecting the checkpoint of a separate division would mean that it is the buyer of goods, which does not correspond to the concluded agreement. Different checkpoints would make it possible to differentiate the buyer, but if from a legal point of view it is only one person (the parent organization, as reflected in the contract [5]), then reflecting the checkpoint of a separate division is meaningless and is determined only by the purposes of “internal” accounting of the movement of the delivered goods to the buyer's structural unit.

Conflicting explanations

Based on the literal content of the rules for issuing invoices (Article 169 of the Tax Code of the Russian Federation and Resolution No. 1137), one should critically evaluate the explanations of financial authorities that do not have the force of legislative acts[6].

The existing clarifications of the Russian Ministry of Finance do not fill any gaps and do not eliminate contradictions in the legislation, but, on the contrary, create uncertainty for taxpayers. Thus, an analysis of official explanations shows the lack of a uniform approach to the issue under consideration.

On the one hand, the Ministry of Finance of Russia indicated that “in the case of the acquisition of goods (work, services) by the parent organization for its divisions, line 6b “TIN/KPP of the buyer” indicates the KPP of the parent organization” (letters dated 08/07/2012 No. 03-07 -11/260, dated January 26, 2012, No. 03-07-09/03).

Other explanations take the opposite approach. For example, in a letter dated 02.11.2011 No. 03-07-09/36 “oINN/KPP of the buyer” the KPP of the corresponding division is indicated.” A similar conclusion is contained in letter No. 03-07-09/55 dated May 15, 2012 (this position, as expressly stated in letter No. 03-07-09/29204 dated July 24, 2013, has not changed to date), at the same time, the Ministry of Finance rejected the link to the clarification previously issued by it, indicating the following: “with regard to the Letter of the Ministry of Finance of Russia dated January 26, 2012 N 03-07-09/03, ... according to which in the case of the acquisition of goods (works, services) by the parent organization for its divisions on line 6b “TIN/KPP of the buyer” the KPP of the parent organization is indicated, then the specified Letter is a response to a private request from the taxpayer to fill out the specified line of the invoice when the parent organization purchases goods (works, services), which are subsequently subject to transfer to a separate division"[7]. This approach is also reflected in a number of earlier letters from the Russian Ministry of Finance (2009-2012).

At the same time, such differences in explanations do not seem to indicate the presence of “irremovable doubts, contradictions and ambiguities” (clause 7 of Article 3 of the Tax Code of the Russian Federation), since the taxpayer must be guided by the norms of legislation, within the meaning of which, as shown above, the indication The buyer’s checkpoint is not a determining detail for VAT purposes and, in principle, relates only to the taxpayer party to the transaction[8], and not to the actual consignee.

Do invoices need to be corrected?

Regarding the need to make corrections to invoices in terms of reflecting checkpoints, it should be noted that the rules for filling out invoices indicate that correction of invoices is possible in case of errors or distortions. At the same time, we can talk about distortions and errors if the legislation on taxes and fees associates the occurrence of any consequences with such errors or distortions, i.e. the significance of such requisites and its mandatory nature must be established.

In other words, an error/distortion is a situation when the invoice does not reflect what should have been reflected in accordance with the established rules for filling it out. If there is no direct obligation to reflect exactly such details and in this order, then there is no error, and, consequently, no grounds for making corrections or replacing the invoice.

An incorrect checkpoint or its absence in the invoice does not prevent the application of a VAT deduction

Regardless of which checkpoint the organization puts on the invoice, this circumstance is not recognized in current law enforcement practice as a basis for refusing to apply deductions.

Materials from judicial practice do not indicate the emergence of a risk in the application of tax deductions, although the very presence of such arguments on the part of the tax authorities, in principle, indicates that the emergence of such claims cannot be completely excluded. At the same time, given the position of the courts, the likelihood of resolving such a dispute in favor of the taxpayer is high.

In particular, rejecting the arguments of the tax authorities, the courts rely on the fact that Art. 169 of the Tax Code of the Russian Federation does not provide for the mandatory indication of the checkpoint in the invoice, and, therefore, incorrect indication or absence of the checkpoint does not interfere with the right to apply tax deductions[9].

This approach is enshrined not only in the Determination of the Supreme Arbitration Court of the Russian Federation dated October 10, 2008 No. 12585/08, but also in the practice (subsequent and previous) of lower courts, as evidenced, for example, by the resolution of the Federal Antimonopoly Service of the Moscow District dated September 7, 2011 No. A40-136255/10-129-436, dated 04/23/2009 No. KA-A40/3582-09, dated 09/22/2006 No. KA-A40/8042-06, FAS of the East Siberian District dated 03/18/2008 No. A33-6296/07-F02-967/08, FAS of the North-Western District dated April 13, 2007 No. A42-5675/2006 (Determination of the Supreme Arbitration Court of the Russian Federation dated August 3, 2007 No. 9457/07 denied transfer to the Presidium ), 9AAS dated December 18, 2009 No. 09AP-24725/2009-AK, 4AAS dated April 22, 2010 No. A19-24868/09 (left unchanged by the resolution of the Federal Antimonopoly Service of the East Siberian District dated July 21, 2010 No. A19- no. 09AP-12910/2006-AK (left unchanged by the resolution of the Federal Antimonopoly Service of the Moscow District dated December 29, 2006 No. KA-A40/12851-06), etc.

Moreover, even in cases where the courts agree that an erroneous reflection or absence of a checkpoint is a defect, they recognize such an invoice defect as insignificant and not preventing the application of deductions on these invoices (Resolution 10AAS dated November 16, 2011 No. A41- 5915/11, 12AAS dated October 31, 2008, No. A12-8136/08-s29, etc.).

This practice has been maintained over recent years and is stable.

Options

Thus, in situations where the buyer under the supply contract is the parent organization, and the actual consignee is a separate division of this organization, one of three options can be chosen in relation to issued invoices:

— indication of the checkpoint of the parent organization. Such actions will formally comply with both Resolution No. 1137 and will not conflict with the civil obligation (the content of the concluded supply agreement). This approach can be justified by reference to the relevant clarifications of the Russian Ministry of Finance;

— indication of the checkpoint of a separate unit. Despite the fact that this approach is also reflected in a number of letters from the Russian Ministry of Finance, it does not directly follow from Resolution No. 1137;

- indication of two checkpoints simultaneously (a separate division - the actual recipient of the goods and the parent organization - the buyer under the contract) by entering additional details into the approved invoice form. This approach is also allowed by the Russian Ministry of Finance[10].

[1] In cases where the legislator attached legal significance to the instructions of the checkpoint, this is directly indicated in the relevant norms of the Tax Code of the Russian Federation (in particular, paragraphs 9, 15, 18, 19 of Article 204 of the Tax Code of the Russian Federation in relation to excise taxes).

[2] As follows from the content of these rules, the requirements for the invoice regarding the indication of the checkpoint, reflected in the Resolution, significantly complement the provisions of Art. 169 of the Tax Code of the Russian Federation. At the same time, such a contradiction must be resolved in favor of Art. 169 of the Tax Code of the Russian Federation, which, as shown below, is generally adhered to by the courts. So, for example, 4AAS in its resolution dated April 22, 2010 No. A19-24868/09 (left unchanged by the resolution of the FAS of the East Siberian District dated July 21, 2010 No. A19-24868/09) indicated the following: “the fact of incorrect indication The code of the reason for registration in disputed invoices has no legal significance for assessing the legality of applying tax deductions for value added tax, since Decree of the Government of the Russian Federation of December 2, 2000 No. 914 is a by-law , which, according to Article 4 of the Tax Code Code of the Russian Federation, cannot supplement or amend legislative acts on taxes and fees ." The Federal Antimonopoly Service of the North Caucasus District also spoke in this vein, which in its resolution dated 06/04/2008 No. F08-3055/2008: “in this norm [sub. 2 clause 5 art. 169 of the Tax Code of the Russian Federation] there is no direct indication of the mandatory reflection of the checkpoint between the seller and the buyer in the invoice. The requirement for mandatory affixing of the checkpoint in the invoice is established only by clause 12 of the Decree of the Government of the Russian Federation dated 02.16.2004 No. 84 “On amendments to the Decree of the Government of the Russian Federation dated 02.12.2000 N 914”: in lines 2b of the invoice “TIN seller” and 6b “TIN of the buyer”, it is necessary to indicate the checkpoint of the seller and buyer, respectively. However, Article 169 of the Tax Code of the Russian Federation directly states that failure to comply with the requirements for filling out an invoice, not provided for in paragraphs 5 - 6 of Article 169 of the Tax Code of the Russian Federation, is not a sufficient basis for refusing to accept for deduction or reimbursement of value added tax . No changes have been made to the Tax Code of the Russian Federation regarding the need to affix checkpoints on the invoice; the main requirement is only to affix the name, address and taxpayer identification number. Consequently, the absence of a checkpoint or its incorrect indication is not a basis for refusal to accept tax amounts for deduction, since it is not provided for by the Tax Code of the Russian Federation" (Determination of the Supreme Arbitration Court of the Russian Federation dated October 10, 2008 No. 12585/08 denied transfer to the Presidium).

[3] In particular, in letters of the Ministry of Finance of Russia dated November 2, 2011 No. 03-07-09/36, dated May 15, 2012 No. 03-07-09/55, etc. Also, based on clause 5 of Art. . 174 of the Tax Code of the Russian Federation, separate divisions do not submit a tax return for VAT (such a declaration is submitted at the location of the parent organization for the entire organization as a whole, i.e. without dividing the tax among separate divisions), in addition, Ch. 21 of the Tax Code of the Russian Federation does not provide for payment of VAT at the location of separate divisions. In addition, in paragraph 5 of Art. 169 of the Tax Code of the Russian Federation, the invoice details indicate “identification numbers of the taxpayer and the buyer,” i.e. The legislator has in mind precisely the taxpayers who are parties to the transaction, and not their separate divisions. Taken together, these legislative provisions allow us to conclude that for VAT purposes, the reflection of a separate division in the invoice is not legally significant.

[4] Thus, from the legal position formulated in Resolution No. 5-P of March 13, 2008, it follows that the tax obligations of organizations are a direct consequence of their activities in the economic sphere and are therefore inextricably linked with it; The emergence of tax obligations, as a rule, is preceded by the organization’s entry into civil legal relations, i.e. tax obligations are based on civil law relations or are closely related to them. This legal position is reproduced by the Constitutional Court of the Russian Federation in later Resolutions (in particular, in Resolution No. 6-P of 01.03.2012).

[5] For example, the justification for reflecting a particular checkpoint with reference to the content of the agreement is contained in the resolution of the Federal Antimonopoly Service of the Moscow District dated May 22, 2009 No. KA-A40/4421-09.

[6] According to the letter of the Ministry of Finance of Russia dated 08/07/2007 No. 03-02-07/2-138, the letters it sends are of an informational and explanatory nature on the application of the legislation of the Russian Federation on taxes and fees and do not interfere with following the norms of the legislation on taxes and fees in an understanding different from the interpretation set out in them.

[7] The Russian Ministry of Finance adheres to the same approach in general and in relation to the seller’s side.

[8] In fact, this rule is consistent with the procedure for paying VAT and reporting on this tax, which is “closed” to the parent organization, and not to a separate division, as shown above.

[9] Naturally, if in the invoices on which the organization accepts VAT for deduction, the remaining details are reflected correctly, in full compliance with the requirements of the law (Article 169 of the Tax Code of the Russian Federation and Resolution No. 1137).

[10] Letter dated July 24, 2013 No. 03-07-09/29204.