An act of offset is usually drawn up in cases where there is mutual debt between counterparty enterprises. The type of debt does not matter - it can be financial or in the form of any other material assets. However, when drawing up an act of offset, the most important condition is that the counterclaims are of a homogeneous nature (for example, monetary claims on both sides).

The act is drawn up by mutual agreement of the parties, at the request of one of them.

- Form and sample

- Free download

- Online viewing

- Expert tested

FILES

Most often, the netting act is used by representatives of small and medium-sized businesses facing financial problems. This option offers them the opportunity to mutually “write off” debts in a competent and legal way, or to conclude transactions through a simple exchange of any equivalent material values. However, there are a number of situations when drawing up an act of offset is not possible. In particular:

- if the debt arose in connection with the collection of alimony;

- if the debt is formed in connection with the contribution of funds to the authorized capital;

- if the debt occurred as a result of compensation for harm caused to health or life;

- if the debt arose during the performance of lifelong maintenance obligations;

- the debt loses its significance if the statute of limitations for it has expired;

- other cases, in accordance with the law of the Russian Federation or provided for by written contractual relations between the parties.

What is an act of offset?

First, let's look at the purpose.

An act of offset of mutual obligations is an official document between two counterparties about the write-off of debts or obligations towards each other.

The main goal is to avoid disputes. At the same time, other problems are being solved:

- Legal disposal of debts and obligations;

- Preservation of working capital;

- Reduction of financial transactions, including savings on fees for interbank transfers.

Both full and partial offset of mutual obligations between organizations or individuals are allowed.

Example:

Company A has a debt to company B in the amount of 10,000 rubles, but at the same time, receivables (from company B) are also 10,000 rubles. Both companies act as both a debtor and a debtor to each other, with the same amount of debt. If both parties agree, they can sign an act of offset, thereby writing off mutual debts.

If one of the companies has a debt of not 10,000, but, say, 7,000 rubles, only partial offset is possible. In this case, the Act also records the balance in the amount of 3,000 rubles - it will have to be returned separately within the allotted time frame.

Triple (multilateral) offset of mutual claims

Is it possible to carry out mutual settlement between several organizations? The unequivocal answer is yes. And this right is given by Article 421. The Civil Code of the Russian Federation, which states that the parties can enter into an agreement, both provided for and not provided for by law or other legal acts.

At the same time, according to clause 4 of Art. 420 of the Civil Code of the Russian Federation, to contracts concluded by more than two parties, the general provisions on the contract apply, unless this contradicts the multilateral nature of such contracts. A sample of such an agreement is shown above in Figure 1. Read also the article: → “”.

Multilateral netting rules:

- the deadline for fulfilling the obligations of each party has already arrived;

- offset is made for the amount of the smallest debt;

- the agreement contains the circumstances of the offset for all three or more parties.

An example of triple netting of organizations on OSNO

- On May 15, LLC “A” shipped goods to LLC “B” in the amount of 350 thousand rubles. (including VAT 53.39 thousand rubles).

- On May 16, “B” shipped materials to LLC “V” in the amount of 250 thousand rubles. (including VAT 38.14 thousand rubles).

- On May 17, “B” provided 200 thousand rubles. (including VAT 30.51 thousand rubles).

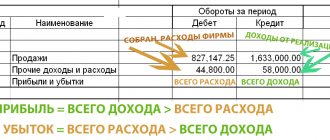

According to the terms of the contracts, the payment period must occur the next day after the provision of services or shipment of goods. As of June 1, none of the contracts have been paid. The parties agreed to repay debts through mutual settlements and drew up a multilateral agreement (see Figure 1). The offset will be carried out for the amount of the smallest debt, that is, for the amount of 200 thousand rubles. (including VAT 30.51 thousand rubles). Accountants will make the following entries (see table 3).

Table 3 – Business transactions between organizations LLC “A”, LLC “B” and LLC “B”:

| № | Business transaction | Amount, thousand rubles | Account correspondence | |

| Dt | CT | |||

| 1 | 2 | 3 | 4 | 5 |

| Accounting for LLC "A" | ||||

| 1 | Revenue from sales of goods of LLC "B" is reflected | 350 | 62settlement with LLC “B” | 91-1 |

| 2 | VAT charged | 53,39 | 90-3 | 68-2 |

| 3 | The cost of services performed by LLC “V” is reflected | 169,49 (200/118*100) | 26 | 60settlement with LLC "V" |

| 4 | “Input” VAT on services is reflected | 30,51 | 19 | 60settlement with LLC "V" |

| 5 | Input VAT accepted for deduction | 30,51 | 68-2 | 19 |

| 6 | Mutual settlement reflected | 200 | 60settlement with LLC "V" | 62settlement with LLC “B” |

| 7 | LLC "B" transferred the balance of the debt after offset | 150, incl. VAT 22.88 | 51 | 62settlement with LLC “B” |

| the debt to LLC "V" after offset is considered fully repaid | ||||

| Accounting for LLC "B" | ||||

| 1 | Goods received from LLC “A” were capitalized | 296,61 (350/118*100) | 41 | 60settlement with LLC “A” |

| 2 | “Input” VAT on purchased goods is reflected | 53,39 | 19 | 60settlement with LLC “A” |

| 3 | Input VAT accepted for deduction | 53,39 | 68-2 | 19 |

| 1 | 2 | 3 | 4 | 5 |

| 4 | Reflected revenue from the sale of materials of LLC "V" | 250 | 62settlement with LLC "V" | 91-1 |

| 5 | VAT charged | 38,14 | 90-3 | 68-2 |

| 6 | Offset reflected | 200 | 60settlement with LLC “A” | 62settlement with LLC "V" |

| 7 | LLC "V" transferred the balance of the debt after offset | 50 incl. VAT 7.63 | 51 | 62settlement with LLC "V" |

| 8 | The balance of debt to “A” has been paid | 150 incl. VAT 22.88 | 60settlement with LLC “A” | 51 |

| Accounting for LLC "V" | ||||

| 1 | Materials received from LLC “B” have been capitalized | 211,86 (250/118*100) | 10 | 60settlement with LLC "B" |

| 2 | “Input” VAT on purchased materials is reflected | 38,14 | 19 | 60settlement with LLC "B" |

| 3 | Input VAT accepted for deduction | 38,14 | 68-2 | 19 |

| 4 | Reflected revenue from the sale of materials of LLC "V" | 200 | 62settlement with LLC “A” | 90-1 |

| 5 | VAT charged | 30,51 | 90-3 | 68-2 |

| 6 | Offset reflected | 200 | 60settlement with LLC "B" | 62settlement with LLC “A” |

| 7 | The balance of the debt to “B” has been paid | 50 | 60settlement with LLC "B" | 51 |

| the receivables of LLC “A” after offset are considered fully repaid | ||||

In what cases is it needed?

The specifics of terminating an obligation by offset are noted in Art. 410 of the Civil Code of the Russian Federation. To do this, three mandatory conditions must be met:

- Firstly, there must be counterclaims to each other - that is, under at least two different agreements. In one case, the organization acts as a debtor, and in the second, as a creditor (the second is similar).

- Secondly, the homogeneity of the requirements - otherwise the act of offset will not have legal force. That is, you cannot “exchange” monetary obligations for services or work. If you have a debt to your counterparty of 3,000 rubles, then your opponent must also have a financial debt to you.

- Thirdly, the deadline for execution has already arrived, the time of demand has not been specified or the moments of demand have been determined.

The execution of the document guarantees the legal conduct of business transactions between two companies or individuals. If the Federal Tax Service or another body wants to challenge the transaction, the Act will act as evidence in favor of the participants in the netting of obligations.

Tax and accounting for this operation

In order to correctly calculate the amount of taxes paid, it is necessary to take as a basis the date of receipt of funds for the shipment of goods, the date of signing the act.

Important: amounts subject to offset on the basis of the act are subject to accrual of tax liabilities, since they are included in income.

The following entries are used in the balance sheet to reflect the offset:

- Provision of services or sale/shipment of goods Dt 62 Kt 90;

- Reflection of the offset amount on a certain date or write-off of debt - Dt 60 Kt 62.

When is it not suitable?

The act cannot always be drawn up. The most obvious situation is when one of the parties does not agree to the offset. In this case, coercion does not work.

Other situations where offsets are prohibited by law are noted in Art. 411 of the Civil Code of the Russian Federation - this includes:

- Alimony debts;

- Heterogeneity of obligations (for example, debt for services in exchange for credit offset or the use of different currencies);

- Expiration of deadlines for execution - the issue will be resolved in court;

- Debt for compensation for damage to health;

- Insolvency (bankruptcy) of one or both counterparties;

- Other situations that violate the law.

There is no point in even trying to conclude an act of mutual offset of obligations - it will not have legal force, and the parties may run into fines.

How to correctly draw up an act of mutual settlement between organizations?

The legislation does not approve a unified form. But there are requirements for primary documents, which are described in detail in Art. 9 Federal Law No. 402 “On Accounting”.

What sections does the contents of the Settlement Certificate consist of:

- Introductory part

The “cap” reflects the name – “Act of Settlement of Mutual Claims”. Below indicate the city and date of the document.

Next comes information about the parties: the first and second companies. In both cases, you need to specify the organizational and legal form (LLC, JSC, individual entrepreneur, etc.), then the full name and position of the authorized employee, as well as the basis document (for example, Charter, power of attorney). It's enough.

- Main part

Here you need to indicate on the basis of which agreements the mutual obligations of the parties arose. For example, a contract or service agreement. Be sure to enter the number and date of conclusion of such agreements. The amounts owed are indicated below: first in numbers and then in words.

Next, the parties inform about their agreement to offset, indicating the form - full or partial. If the second option, then it is necessary to record the remaining debt and the timing of its transfer to the counterparty’s current account.

- Final part

The document is signed by both authorized persons, indicating their full name, position and personal signature. There is no need to put a stamp; starting from 2021, this is an optional attribute when approving documents. But keep in mind that the Federal Tax Service may require the seal of a legal entity.

Other nuances

The act of offset of mutual obligations is drawn up in at least 2 copies. If other interested parties are involved in the transaction, copies are prepared for them as well. Each copy must be endorsed with the signatures of both parties.

The law classifies the act of offset as primary accounting documentation. Its shelf life is at least 5 years (Article 29 of Federal Law No. 402). For the Federal Tax Service, the shelf life is 3 years. This is necessary so that subsequently there are no misunderstandings regarding the accounting and tax accounting of the company.

An alternative to a bilateral act is to offset mutual obligations unilaterally. To do this, the accountant of one of the companies sends a statement of offset to the counterparty. In order to have proof of sending, it is better to use mail (registered or valuable mail). If the other party has no objections, the mutual offset of obligations will take place from the date specified in the application. And if there is no date, then from the date on which the application was received.

Stages of mutual settlement and their documentary support

Offsetting is carried out in stages (see Table 2), and the number of stages varies depending on the number of parties and the method of its execution, and each stage is supported by the appropriate document (for offsetting, like any accounting operation, must be documented).

Table 2 – Settlement stages:

| Stage | Stage name | Document | Characteristics of the stage |

| 1 | 2 | 3 | 4 |

| I | Identifying mutual obligations | Act of reconciliation of accounts | An act of reconciliation of settlements is drawn up with a breakdown of all agreements concluded between counterparties and the total amount of debt is displayed |

| II* | Exchange of reconciliation reports | Reconciliation acts are certified by the signatures of the responsible persons of the organizations participating in the mutual settlement (director of the organization, chief accountant) and sealed | |

| III* | Writing and sending an application for a mutual offset offer (for unilateral offset) | Settlement application | In the application, it is important to indicate the amounts of the contracts for which the offset will take place, and also indicate that the debt will be written off for a smaller amount (if the amounts are different). The application itself must be sent by registered mail, because in the event of legal disputes, it is important for the organization sending it to prove that the application was received by the addressee. |

| IV* | Compliance with homogeneity requirements | Accounting certificate for calculating exchange rate differences on funds in a foreign currency account | If monetary obligations are carried out in different currencies, then they must be converted into the same currency. |

| V | Signing the act of mutual offset (in case of multilateral offset) | Act (agreement) on mutual settlement | As in the statement of offset, it is important to indicate the amounts of the agreements, designate the amount of offset, the signatures of the responsible persons of all parties and the seal. |

| VI | Accounting entries | Offsetting act | Creation of a debt adjustment in the database (with corresponding postings) and, consequently, a document - an act of mutual settlement (the data of which, as a rule, is taken as a basis when creating a document from the previous stage) |

* – indicates an optional or intermediate stage

It is important that all stages of the test are supported by appropriate cover letters. For example, party “A” sends party “B” a proposal for mutual settlement along with reconciliation acts, party “B” gives a positive response, then the company’s lawyers draw up an agreement, authorized persons (directors, chief accountant) sign it, and accountants display this business operation by postings in the accounting database.