By law, companies that accept payments for goods, services or work in the form of cash must use cash registers in their activities. Moreover, each transaction recorded with the participation of the cash desk is confirmed by a paper check, which contains the following data: number, date and essence of the transaction, as well as the amount that was spent on it.

All actions performed over a certain period of time using a cash register are included in the cashier-operator’s journal.

- Form and sample

- Free download

- Online viewing

- Expert tested

FILES

What goals and objectives does the document solve?

The journal is a means of recording all transactions performed using a cash register. It contains information about both the receipt and expenditure of funds.

In cases where an organization has several cash registers, a journal is kept for each of them separately.

Generally speaking, having a magazine allows you to solve several different problems at once. For example, with the help of a journal, the head of an enterprise can quickly determine at any time how much money passed through the cash register for a specific period, and tax service employees, during inspections, have the opportunity to quickly compare cash register readings and figures from reporting documents with information from the journal.

Rules for registration and filling

When preparing a cashier-operator's journal, it is important to pay attention to the following details:

- KM-4 must be flashed for the entire book or just the sheets.

- The signature on the control sheet must be from the individual entrepreneur or the head of the organization. It must be certified by a seal, if the latter is used by the institution.

- Each sheet in the book must be numbered, starting from the first. There is no need to number pages.

- On the last sheet there must be a note: “In the journal there are numbered, laced and signed (and sealed) ... sheets.” Part of this text must be included on the checklist.

How to correctly fill out the cashier-operator’s journal (you will see a sample of a specific entry below)? The rules are as follows:

- You can only write in the book with a ballpoint or ink pen with dark blue ink.

- Entries are made in strict chronological order. One line is one cash day.

- The source for records is only the Z-report - the information should not be the result of independent calculations. If several such reports were made during a cash day, then data for each of them must be entered into the book.

- Each entry must be certified by the signature of the cashier, individual entrepreneur and manager.

- The book should not contain corrections or erasures.

If a cashier-operator makes an error in an entry that has already been made, you can correct it by following the instructions below:

- Erroneous data must be crossed out, then the correct information must be indicated next to it, as well as the date of correction.

- The cashier himself, as well as his immediate supervisor, certifies the mark with his signature.

- If the scale of the error is measured over several pages or sheets, then crossing them out crosswise is allowed.

If all blots are corrected according to the specified scheme, then they should not be punishable for the employee.

Do I need to register?

Like a cash register, the journal must be registered with the tax authorities.

Even the first filling of the journal occurs at the same time as the cash register is registered (the inspector punches a check with the amount of 1 ruble 11 kopecks - this value is not subsequently taken into account by either accountants or tax authorities).

To ensure that the inspector does not refuse to register a cash register, a number of other documents must be provided along with the device itself and the magazine:

- application requesting registration of the cash register;

- certificate of a legal entity or individual entrepreneur;

- KKM passport;

- rental agreement for retail space (if the company does not have its own square meters);

- cash register service agreement concluded with a specialized center, etc.

A complete list of documents can be obtained from the territorial tax service.

Replacing with a new one and making changes

If the magazine has expired, then it must be “redeemed” at the tax office when registering a new one. Such a replacement can be made with the submission of an application for renewal of the journal by any of the company’s employees who has a power of attorney on behalf of the manager, certified by a notary. It is also important to have an old magazine and KKM registration card with you.

Form ADV-2 is sent to the territorial body of the Pension Fund of the Russian Federation in the event of a change in the last name, first name, or patronymic.

We tell you how to draw up an order for incentives in the T-11 form - in this article.

Entries in the new journal should continue the order of the old one. The remainder is transferred to the new document. The journals must be changed at the end of the year, but these requirements are not mandatory.

If questions arise, you can contact the tax office or the administrator, since there are cases when managers or tax specialists may express some wishes regarding a particular issue regarding filling out. It is important to remember that maintaining a log is a responsible task that affects the integrity of the reporting.

What is the penalty for not having a cashier-operator’s journal?

Keeping a journal is a legal requirement, so inspectors during on-site tax audits must look at its presence and content. Failure to register a journal may result in a fine (although this penalty is not specified in the law).

It should be noted that conflicts often occurred between business representatives and tax authorities on this issue, leading to court. And, as practice has shown, the administrative penalty for the fact that the enterprise did not keep a log of the cashier-operator was removed from him in most cases.

Error correction

Any enterprise must observe cash discipline, otherwise the violator faces administrative liability. Correcting an error in a document is allowed, however, it is often easier to fill it out again than to correct an erroneous entry.

With the cashier's journal, things are a little more complicated. It has to be maintained over a long period of time with strict adherence to chronology, for this reason it will not be possible to completely rewrite the document. Nevertheless, corrections are allowed on the basis of Resolution of the State Statistics Committee of the Russian Federation dated December 25, 1998 No. 132.

If an error is found, it must be corrected using one of the following methods:

- If an error is discovered during the current shift, the incorrect entry is crossed out completely and a new one is entered into the journal on the next line. An erroneous entry must be crossed out with one line so that, if necessary, it remains readable.

- If a long-standing error is discovered, the incorrect number must be corrected to the correct one.

There is no fine for corrections that were completed in accordance with the established procedure. Federal Law “On Accounting” dated December 6, 2011 No. 402-FZ in paragraph 8 of Art. 10 requires, next to the correction, to indicate the date of the changes, as well as the details of the responsible person and his signature. Only those responsible for maintaining the journal can make corrections.

Features of the document

Since 2013, unified templates for primary documents have been abolished, so today employees of organizations and enterprises have the opportunity to choose whether to keep a cashier-operator journal in free form, develop their own document form, or use the unified, previously mandatory form KM-4 . The majority, I must say, follow the third path, since the standard form contains all the necessary details and lines, which means there is no need to waste time on creating the structure and content of the journal.

The document should be kept in paper (printed) form. In this case, all its sheets must be numbered and fastened together using a thick thread (but not with a stapler). You can use a ballpoint pen of any dark color to fill out the journal (other writing tools - felt-tip pens, pencils, etc. are unacceptable).

On the last page of the document, you must indicate the number of sheets, put a stamp (unless, of course, the use of stamps is enshrined in the company’s accounting policy), and the signature of the responsible person (accounting department specialist or chief accountant).

Entries in the journal are made strictly chronologically (without gaps), while blots and errors are extremely undesirable.

If such an oversight does occur, the incorrect data should be corrected by carefully crossing out the incorrect information and entering the correct information, making o next to it. All adjustments must be dated and certified by the signature of the cashier-operator and the chief accountant.

The book can be maintained either on a regular basis (if a retail outlet or enterprise operates every day) or as needed.

If there were no transactions involving a cash register during the accounting period, you do not need to fill out the form.

Examples of some Z-reports and information on them for filling out the KM-4 form.

| Mercury 180K | Alpha 400K | Mercury 130K | Kasby 02K | AMC 100K |

Examples of filling out the Cashier-Operator Log on different cash registers:

Elwes-MK:

Is it necessary to fill out the cashier-operator’s logbook if nothing was punched at the checkout?

If the cash register did not display any amounts during the current day, then it is not necessary to make a report, especially since many cash registers do not allow you to make a Z-report. In a word, if you do not work on a cash register, then you do not need to fill out the cashier-operator log.

But, if you still want to write something down in the cashier-operator’s journal, then remove the zero check and make an evening Z-report, and then enter it in the cashier-operator’s journal.

When do you need to fill out the cashier-operator log?

The cashier-operator's journal is filled out immediately after the Z-report is taken. This can be once a day, for example in the evening - at the end of the working day. Or maybe your store is open around the clock and the shift ends in the morning, then the report is taken in the morning.

Is it possible to make several reports per day?

If you have two or three shifts per day, then you respectively take out two or three reports per day, but the most important thing is that each of the Z reports be entered as a separate line in the cashier-operator’s journal. This results in several records with the same date, but with different shift numbers.

If the cashier forgot to withdraw Z - report.

If the report was not taken in the evening, it doesn’t matter; it can be taken in the morning the next day or even the next day. In this case, in the cashier's journal, the operator needs to enter the date taken from the Z-report and spend the money on the date when it was withdrawn. Or, if the money has already been posted in the cash book, you can put the required date in the cashier’s journal, and ask the cashier to write an explanatory note in free form addressed to the director - this will force the cashier to be more careful next time.

If the cashier accidentally removed several extra reports during the day.

If several evening Z-reports for the day were accidentally taken at the cash register, then each one needs to be entered into the cashier-operator’s book separately; several reports will be issued under different numbers, but for the same date. Typically these are zero amount reports. You can also ask the cashier to write an explanation for educational purposes.

Is it possible to recover a lost Z-report?

Z - the report can be restored in two ways:

- Create a fiscal memory report. To do this, you need the tax inspector’s password; if you don’t know it, it’s better to call a cash register mechanic who will help you get the report. Do not try to remove the fiscal report yourself, as your cash register may be blocked if you enter the tax inspector's password incorrectly. The fiscal report will give you information only on the total amount for the day, that is, it will not contain information on each purchase for the day.

- Make a report on ECLZ . The EKLZ stores all information on all cash receipts punched on the cash register. That is, from the ECLZ block you can extract detailed information for any working day. Remember that the EKLZ block changes once a year, so information can only be obtained from the current block.

Corrections in the cashier's journal.

Each error in the cashier-operator's journal must be certified by the signature of the person responsible for maintaining the journal. That is, next to each correction you need to write: “believe the corrected one” and sign.

Are the cashier's journal and the cash book the same thing?

No. A cash book is another document that individual entrepreneurs and organizations are also required to have in order to maintain accounting records.

Fine for the absence of a cashier's journal.

Tax inspectors try from time to time to fine entrepreneurs for the absence or failure to fill out a cashier-operator's register, charging them under Article 15.1 of the Code of Administrative Offenses of the Russian Federation, and the fine under this article is rather large: from 40,000 to 50,000 rubles. So there were several court proceedings (one of them: No. A56-9691/2005 dated July 28, 2005), which entrepreneurs won each time. But how many entrepreneurs did not file a lawsuit against the illegal actions of tax officials remains a mystery. Therefore, decide for yourself whether you need to keep a journal or not.

And it looks completely ugly when tax inspectors try to bring the absence of a cashier-operator’s journal under Art. 14.5 Code of Administrative Offences. In my practice, there was one such case in the Leningrad region. The entrepreneur chose not to contact the tax authorities and paid a fine of 4,000 rubles. For organizations it would be 40,000 rubles.

There is also Article 120 of the Tax Code, which talks about gross violation of the rules for accounting for income and expenses. But failure to keep a journal for a cashier-operator is not a gross tax violation. Although some tax authorities also refer to this article when trying to put pressure on an entrepreneur so that he pays a fine.

Correctly filling out the cashier's journal will not save you from tax fines if you WANT to pay them))).

What should you do after filling out the cashier/operator log?

Prepare a certificate-report from the cashier and transfer the data to the cash book.

How to register a cashier's journal.

The cashier's journal is tied to a specific cash register. Therefore, the journal is registered along with the cash register registration. When the magazine comes to an end, you need to buy a new one, stitch it and number it, and then go to the tax office and have it certified. The certification of KM 4 journals is carried out by the operational control departments in the relevant Interdistrict Tax Inspectorate where the cash register was registered. The old completed log must be kept in the organization’s archives for 5 years. Although its storage became meaningless with the introduction of EKLZ - now all information is stored on electronic media.

Examples of a certified cashier's journal.

Where to register the cashier-operator's journal.

At the tax office - in the operational control department of the MIFTS (cash register registration department), in which the cash register was registered. For individual entrepreneurs - at the place of registration, and for organizations (LLC, OJSC, CJSC, etc.) at the place of registration of the enterprise or separate division.

Documents required for registering a new cashier-operator journal.

Different tax offices may have different rules regarding the documents presented. The law also does not specify the necessary documents for registering a replacement journal. In each specific case, it is better to call the tax office and ask what they want. Here are several types of documents that tax authorities in St. Petersburg require:

- passport (form) to the cashier.

- old journal of the cashier-operator.

- new cashier-operator's journal, stitched and numbered

- registration card for the cash register

- passport of the person presenting the documents and a power of attorney, if this is not the head of the enterprise.

First entry in the journal.

During the initial registration of the cashier-operator’s journal along with the cash register, the tax inspector makes the first entry in the journal, on the removed Z - a report and punched 1 ruble, 11 kopecks, although some tax authorities do not do this, but simply certify the journal with a signature and stamp.

An example of the first entry that the tax inspector leaves when registering the KM-4 journal.

The person responsible for maintaining the cashier-operator's journal.

Appointed by order of the director if the director does not want to be responsible for its maintenance. Usually this is a cashier, administrator or chief accountant. It would be a good idea for a manager to create a job description for a cashier-operator. In practice, no one fills out this column and tax inspectors do not find fault with it. If the column is not filled out, responsibility for maintaining it automatically falls on the head of the company or individual entrepreneur.

Types of cashier-operator journals.

I've met two types. Samples of cashier-operator logs:

- Vertical magazine. Pros: more lines on the page - enough for a larger number of records - less often you will have to change it at the tax office. Disadvantages: the columns are too narrow - large amounts do not fit.

- Horizontal magazine. Pros: easy to fill - wide lines that can accommodate large amounts. Cons: enough for fewer records - will have to be changed frequently.

How long does the cashier's journal last?

horizontal journal contains about 50 sheets and 20 lines on each sheet. 20 multiplied by 50 equals 1000, which means the magazine is enough for about a thousand days or shifts.

The vertical magazine has from 29 to 40 lines and 50 pages, that is, it is enough for about 2000 days (shifts).

You will notice that columns 6 and 9 are too narrow (especially in a vertical journal) to write large amounts of savings in them, and columns such as 5 and 15 are too wide for their meanings. Could Russian officials have come up with something smarter?

How to register a return in the cashier's journal.

Refunds at the cash desk are issued in column 15. If there were several returns for the current day, then they are all summed up and filled in with one amount. When returning, it is not necessary to punch out refund receipts at the checkout (although you can do this for beauty), but you must fill out the KM-3 form.

A detailed description of how to process a return can be found in this article.

An example of filling out a return in KM-4 (returns for a total amount of 1000, it does not matter how many returns there were): Please note that columns 11 (deposited in cash) and 14 (deposited in total) are less than the amount of returns.

Registration of sales by bank card / non-cash / credit

If you make sales using bank cards through bank terminals, or accept money through a checkbook, or by any other non-cash payment, then this money also needs to be entered at the cash register. In the evening Z-report you will have a separate line showing the number of sales by bank transfer and the total amount for the day by bank transfer. These two parameters must be written down in columns 12 and 13 of the cashier’s journal.

Columns 12 and 13 are responsible for breaking through funds not for cash payments - that is, by any other means:

- with a bank card - the entry of funds received through the bank terminal must occur twice: 1 - at the bank terminal itself 2 - at the cash register

- travelers checks

- sales on credit, etc.

There is no need to enter into the journal funds that were received into a non-cash bank account.

In column 12 - write the number of checks by bank transfer. Column 13 shows the total amount of checks by bank transfer. In column 11 - deposited in cash, the amount must be less than in column 14 by the amount in column 13, that is:

Sample document

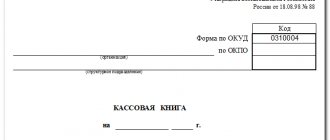

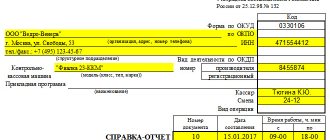

At the beginning of the document, on the title, it is written:

- name of the organization, its address, as well as (on the right) codes: OKUD, OKPO, OKPD, INN number;

- The cash register on which the log is kept: its name (model, brand), numbers (manufacturer and registration);

- the period during which the information specified in it was entered into the journal;

- designate the employee responsible for creating the journal.

In the second part of the document, in the table, the following are entered in order:

- day-month-year of filling, and also, if the cash register operates in two shifts - shift number;

- department (here you can put dashes if the cash register serves one department, or enter all the department numbers to which the checks “went” during the current shift);

- Full name of the employee sitting at the cash register;

- serial number of the control counter at the time of shift delivery (i.e. serial number of the Z-report - its type depends on the cash register model);

- the values of the control counter, the amount of cash that has passed through the cash register since its registration with government agencies, plus the amount received during the current shift are recorded;

- The signature of the administrator and the cashier is immediately placed (if this is the same person, then you need to sign in both cells);

- the last column includes the amount of revenue for the previous day.

Next, enter into the form

- amount deposited in cash

- the amount returned to customers due to the fact that cash receipts were not used,

- signatures of responsible persons.

Cash book for online cash register

The cash book keeps records of all amounts received and spent: revenue, cash issued, cash deposited at the bank.

Individual entrepreneurs maintain a cash book at will and can refuse it. But for companies, a cash book is required, even if there is an online cash register.

How to keep a cash book for online cash registers

According to the Decree of the State Statistics Committee of Russia dated August 18, 1998 No. 88, the cash book is kept in the KO-4 form. But the company can approve its form according to its accounting policies.

What does a cash book look like?

The cash book can be in 3 formats:

- paper;

- electronic with file printout;

- only electronic on PC.

The cash book on paper forms must be stitched and numbered. It is operated by a cashier throughout the working day. He fills it out, having received receipt and expenditure orders from the accounting department. They allow the cashier to receive and issue funds.

How to flash a cash book and its sample

In the electronic version, the cash book is also filled out by the cashier or a responsible person appointed by management. An electronic signature issued to an official in accordance with the law dated 04/06/11 No. 63-FZ is used for it.

The cash book is filled out only once a day when funds are posted to the company. For example, if salaries were issued through the cash register on May 1 and May 15, then the corresponding dates will be recorded in the book.

If you don't keep records, the tax office may fine you. According to paragraph 1 of Art. 15.1 Code of Administrative Offenses of the Russian Federation:

- for organizations - a fine of 40–50 thousand rubles;

- for individual entrepreneurs and heads of companies - 4–5 thousand rubles.

Step-by-step cash book maintenance

Is it possible to make corrections to the cash book?

Yes, but only on paper forms. To make corrections, cross out the incorrect entry and enter the correct value. You cannot erase entries in the book. According to Instructions No. 3210-U, all corrections are certified by the cashier or chief accountant.

Corrections cannot be made to a book formatted and signed in electronic format.

How to correct an error in the cash book

How many cash books should be kept?

If you are an individual entrepreneur and optionally keep a cash book, then one is enough for you.

For organizations, the number of cash books depends on the number of branches, according to Directive No. 3210-U. If they are not there, then keep 1 book, even when combining tax regimes.

After compiling the journal

Since the journal is an accounting document, the procedure for its content and storage is determined either by law or by internal regulations of the organization. Regarding the storage of a document during the period of its validity, one thing can be said - it should be located either in the accounting department or next to the cash register in a place inaccessible to strangers.

After the journal expires, it must be transferred to the enterprise archive, where it must remain for at least three years, then it can be disposed of in compliance with the procedure prescribed in the legislation of the Russian Federation.

What papers were required to register cash register?

Before the release of changes affecting the law “On the use of cash registers...” dated May 22, 2003 No. 54-FZ, the purchase of a cash register entailed 2 important consequences for the business entity: its registration with the tax authorities according to the order of the Ministry of Finance of Russia dated June 29, 2012 No. 94n and at the same time registration of the corresponding journal of the cashier-operator. To carry out both operations, a common package of documents was required:

- an application drawn up in the prescribed form;

- an agreement with the company that will provide the service;

- registration certificate for the cash register;

- the journal form itself;

- power of attorney for the person submitting the papers for registration.

This list was unified and required in any case, however, a specific department of the Federal Tax Service could request additional papers for it. For example, a contract for the purchase of equipment, a passport for a secure electronic control tape, a book for registering visits to a technical specialist. The equipment version passport and the insert for it could not be provided on the basis of the letter of the Federal Tax Service of Russia dated July 31, 2013 No. AS-4-2 / [email protected] The absence of a registered cash register entailed punishment for the subject under Art. 120 of the Tax Code of the Russian Federation and Art. 15.1 Code of Administrative Offenses of the Russian Federation.

Features of cash payments

The content of the article

When paying in cash, they use equipment registered with the Federal Tax Service. The cash register itself and the EKLZ (electronic control tape) are subject to registration. A summary of data on incoming, outgoing transactions and balances is entered into the journal daily. equipment was not used during a work shift , no records are kept.

The journal is submitted for control to the Federal Tax Service in the following situations:

- Re-registration of a cash register card.

- The end of a magazine and the opening of a new book.

- Purpose of checking cash discipline during an office or field control event conducted by the Federal Tax Service.

An organization can purchase, register and install any number of cash registers. It is necessary to distinguish the operating cash desk of an enterprise from the cash register cash register.

Cash received through the machine:

- Must be taken into account on the day of admission. Funds in the cash drawer can only be stored within the limits of small change received from the organization's cash desk at the beginning of the cash day according to a cash receipt order.

- Can only be returned to the buyer on the day of receipt. Absent at the beginning and end of the cash register shift.

- Subject to delivery to the cash collector during the shift or to the company's cash desk using a cash receipt order at the end of the day after the shift closes.

Violation refers to gross errors in compliance with cash discipline and entails a fine on the cashier (3-4 thousand rubles) and the enterprise (40-50 thousand rubles).

To facilitate the work of the cashier-operator, as well as to record goods, returns and balances in the Russian Federation and abroad, a barcode system is used. It is not prescribed by law, but in practice, store chains simply refuse to work with products that are not assigned a unique combination of symbols. To register a barcode, just go to the website https://rossertcentr.ru/shtrikh-kodirovaniye.

The nuances of journaling in various situations

Upon return

Cash received by a cashier using a cash register must be deposited at the cash desk of an organization or individual entrepreneur. Funds are not stored and cannot be used by the cashier after the cash register shift closes. If during a cash register shift a buyer appears who wishes to return the goods , the money can be returned to him from the cash register drawer. To carry out the refund, the cashier draws up an act of form KM-3. Later, the refund is made through the company's cash desk.

Features of returning goods by the public and receiving funds:

- The buyer has the right to return the goods if the items do not match the range, size or color. The return procedure is regulated by the Law “On Protection of Consumer Rights”. There is a list of items that cannot be returned.

- To receive funds for the delivered goods, the buyer must submit an application to the head of the trading enterprise.

- 14 days are provided for consideration of the application and refund.

In this situation, it is rarely possible to provide a refund through cash register. Refunds of cash received from enterprises are made through a cash register on the day of purchase of goods, through a cash register or bank account on subsequent days.

When acquiring

Acquiring – payment for goods using payment cards . The company receives funds to its current account. Amounts received by non-cash means are recorded by the cashier in a separate column in the cashier's journal. The balance on the Z-report will not correspond to the amount of cash.

Equipment for payments using cards is provided by the bank institution with which the service agreement has been concluded. The disadvantage of using payments is that the bank charges a percentage for cash management services from each payment. When making payment, the buyer receives a cash receipt.

Failure to keep a journal is a gross violation of cash discipline rules. If a violation is detected, the Federal Tax Service may impose a fine on the cashier and the enterprise. A similar fine is charged if a book is lost. The log can be restored using cashier reports or X-reports, which are printed by equipment service companies.

How to reflect a refund in the cashier's journal

Cash orders

There are two types of orders: for receipts and for expenses. As you might guess from the name, receipts are used when money is received, and expenses are used when money is issued. The order is drawn up in one copy by an accounting employee and signed either by the chief accountant or an authorized employee.

A check is attached to the receipt, which must be signed by the cashier and accountant. Also, it must be affixed with the organization's seal. It is issued to the person who deposited money into the cash register.

Read more about the receipt order in the article.

Read more about the expense order in the article.

Tips for filling

- If the amount must be indicated in words, it must be done in capital letters. Kopecks are written in numbers.

- Documents can be filled out either on a computer or manually.

- Incorrectly filled in information in cash register papers can be corrected. This is how it is done. An incorrect entry is crossed out with a neat line. The correct entry is made above or next to it. Here they write “believe what is corrected.” The company manager and chief accountant must sign next to this entry.

- If a document contains blots, clerical errors or corrections by a proofreader, it is considered invalid.

New documents required to be completed

Federal Law No. 54-FZ introduced two completely new cash documents into use. The first of them is called a correction check and is necessary if an excess of the recorded revenue is detected as a result of the change. In addition, this document must be drawn up in the event of a power outage, when payments to customers are made in cash. It should be remembered that failure to use a cash register is an administratively punishable crime. While this document will allow you to avoid a fine. But this opportunity should not be abused; for each such check, the tax inspector may demand documentary explanations.

The second document is a check with the sign “return of receipt” . A similar check is issued in the event of a refund to the client for purchased products or services received. The document is drawn up regardless of the form in which the funds were received from the consumer: cash or electronically.

In addition, the widespread introduction of online cash registers justified the emergence of other fiscal documents. First of all, these are reports of opening and closing shifts ; according to the law, no more than 24 hours should pass between operations of one shift. If the shift opening report is not generated, the cash register will not print cash receipts. The same thing happens if the shift exceeds a day. A report appeared informing about the closure of the fiscal drive, that is, a device installed in the online cash register and storing all cash documents in encrypted form. If you need to remove the drive from the cash register, for example, when its memory is full, you must be sure that all transaction documents have been transferred to the tax service.

Advance reporting

This reporting is needed in order to take into account the money that is issued for business expenses. This document is drawn up by the accounting employee and the reporting employee in one copy.

The reverse side of the report should include a list of documents that can confirm that the expenses were incurred. These can be various receipts, transport tickets, and so on. Also, these documents must be attached to the report and numbered in the sequence in which they are listed in the reporting.

How to keep a cash register on a computer

This version of the document has in many ways a similar algorithm for filling out a cash register (a sample form is located below) in paper format. As a rule, the computer version of the document is filled out on standardized KO-4 forms in programs such as Word or Excel. During the day, the cashier enters entries into the form in a manner similar to filling out a journal manually. At the end of the shift, he must print out the completed form in two copies and also take them to the accountant for verification, along with all orders entered through the cash register. Once a quarter or year, printed forms must be bound and numbered. The number of sheets is indicated on the stitching, as well as the signature of the responsible accountant and the head of the enterprise, and everything is sealed with the seal of the organization.