All policyholders are required to submit 4-FSS for the 2nd quarter of 2021. This is not a tax report and is devoted exclusively to social insurance issues. It reflects the amount of accrued and paid contributions for compulsory insurance against accidents at work and occupational diseases (AS and PP) and a number of other information. You will find an example of filling out the 4-FSS in our material. We will also tell you about the deadlines for submitting the 4-FSS for the 2nd quarter of 2021 (that is, for the first half of the year).

We determine the obligation to submit 4-FSS for the six months

To find out whether you need to take the 4-FSS, consider a few examples:

- IP Salikhov R.E. engages in business activities without the use of hired force. It applies the simplified taxation system (STS). Absence of R.E. Salikhov from the staff. employees eliminates the need to submit 4-FSS.

- IP Trukhnin M.V. carries out vehicle washing activities. Applies UTII and has 7 employees. He is obliged to report to Social Insurance in form 4-FSS in the generally established manner.

- IP Samokhvalov A.T. uses the labor of individuals. Only GPC agreements are drawn up with them, which do not stipulate the employer’s obligation to pay contributions for injuries. An individual entrepreneur should not submit 4-FSS under such conditions.

- Toreador LLC employs 98 people. The company uses OSNO. She is required to report quarterly to Social Security on contributions for injuries.

- PJSC "Children's Goods" registered with the tax authorities in May 2021. The company applies the Unified Agricultural Tax. Until the end of June, she did not manage to hire a single employee. At the same time, the obligation to submit a report on injuries to the Social Insurance Fund remains for her. The calculation will be zero.

Examples show that the obligation to submit 4-FSS does not depend on:

- organizational and legal form of the insured;

- applicable tax regime.

The absence of employees on staff allows only individual entrepreneurs not to take 4-FSS. In this case, companies submit a zero report to social insurance.

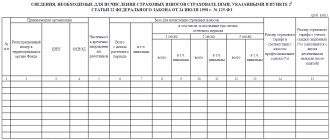

Table 5 “Information about the assessment results”

Here data is provided on the total number of jobs that are subject to assessment, as well as the number of workers who are employed in hazardous or hazardous work.

| 3 columns lines 1-6, 7 | Number of recipients of benefits in excess of mandatory Number of workers who used their days off to care for disabled children |

| 3, 4, 7, 10, 13, 16, 19 columns | Line 1-2 – number of days paid Line 3-5 – payments Line 6 – number of benefits paid in excess of mandatory ones |

Nuances of filling out 4-FSS: title page

Let's continue the conversation about 4-FSS using one of the previously discussed examples.

Toreador LLC is preparing to submit reports to the Social Insurance Fund for the 2nd quarter. For this the company:

- Uses the report form from the order of the Federal Social Insurance Fund of the Russian Federation dated September 26, 2016 No. 381 (as amended on June 7, 2017).

- All fields with missing information are crossed out.

- The composition of the report is determined by the following algorithm: the minimum acceptable reporting set includes the title page, tables 1, 2 and 5, and tables 1.1, 3 and 4 are filled out and submitted only if indicators are available. Since Tornado LLC does not have such indicators, for the first half of 2021 it will fill out 4-FSS in the minimum allowable volume.

- At the end of the half-year, “06” will be entered in the “Reporting period (code)” field.

- In the “Average number of employees” field, indicate the value calculated using a special methodology used when filling out statistical reporting (Rosstat order No. 772 dated November 22, 2017).

The methodology for calculating the indicator for filling out the field “Average number of employees” (Nsr) is as follows:

- To determine the Chsr, Tornado LLC collected information for January-June:

| Period | Number of employees* | Person-days | Hours per month | |

| January | From 01.01.2018 to 15.01.2018 | 98 | 3038 | 98 |

| From 01/16/2018 to 01/31/2018 | 98 | |||

| February | From 02/01/2018 to 02/15/2018 | 98 | 2744 | 98 |

| From 02/16/2018 to 02/28/2018 | 98 | |||

| March | From 03/01/2018 to 03/15/2018 | 98 | 3038 | 98 |

| From 03/16/2018 to 03/31/2018 | 98 | |||

| April | From 01.04.2018 to 15.04.2018 | 98 | 2775 | 93 |

| From 04/16/2018 to 04/30/2018 | 87 | |||

| May | From 05/01/2018 to 05/15/2018 | 98 | 3038 | 98 |

| From 05/16/2018 to 05/31/2018 | 98 | |||

| June | From 06/01/2018 to 06/15/2018 | 95 | 2850 | 95 |

| From 06/16/2018 to 06/30/2018 | 95 | |||

*Different numbers of employees in different periods are due to their absence from work for various reasons (for example, due to going on unpaid leave)

- Taking into account the fact that Tornado LLC had no part-time employees in the reporting half-year, the average for the half-year will be:

HR = (98 + 98 + 98 + 93 + 98 + 95) / 6 = 97 people.

The fields on the title page dedicated to the number of working disabled people and workers engaged in harmful and dangerous work are crossed out. There are no such employees at Tornado LLC.

Table 4

This sheet is filled out only by those enterprises where accidents occurred or occupational diseases were discovered during the reporting period:

- On page 1 information about the total number of NS is entered. This value must coincide with form N-1 (approved by Resolution of the Ministry of Labor dated October 24, 2002 No. 73).

- On page 2, fatal accidents are listed.

- On page 3, data on recorded cases of occupational diseases is entered.

- On page 4 enter the sum of page 1 and page 3.

- On page 5, data is entered on cases that resulted in only temporary disability.

NS are taken into account in the reporting period when the examination was carried out.

Fill out tables 1, 2 and 5 Calculation

To fill out Table 1 of the 4-FSS calculation, you need to understand what is the basis for calculating contributions for injuries. Law No. 125-FZ (Clause 1, Article 20.1) will help us with this: the object of taxation of contributions is payments and remuneration in favor of individuals:

- under employment contracts;

- under GPC agreements, the subject of which is the performance of work (provision of services);

- under copyright contracts.

Payments under GPC agreements and author's orders are included in the database if the text of the agreement specifies the customer's obligation to pay insurance premiums.

To determine the base for calculating contributions (BNV), it is necessary to divide all payments into 2 parts:

- “OVS” - payments subject to contributions “for injuries” (Article 20.1 of Law No. 125-FZ).

- “NVS” - non-taxable amounts (Article 20.2 of Law No. 125-FZ).

To calculate BNV, the simplest mathematical subtraction operation is used:

BNV = OVS – NVS

There are nine lines in Table 1 of Form 4-FSS, which are filled in with the following data:

| Table row 1 | What does it reflect? |

| 1 | OBC |

| 2 | NBC |

| 3 | BNV |

| 4 | BNV for payments to disabled people (including from line 3) |

| 5 | The data for filling out the lines (the amount of the insurance tariff, discounts or surcharges, the date the tariff was established) is taken from the notification received from the Social Insurance Fund |

| 6 | |

| 7 | |

| 8 | |

| 9 |

Let's continue the example of Tornado LLC. Considering that NBC = 0 (there were no non-contributory payments in the first 6 months of the year), we have OBC = BNB. The contribution rate established by Social Insurance is 0.2% (data are shown in the table):

| OBC | Amount, rub. | Contributions, rub. |

| Amounts subject to contributions (total for half a year) | 18 946 477,88 | 37 892,96 |

| including for the last 3 months of the reporting period | 9 371 718,38 | 18 743,44 |

| for April | 2 965 090,44 | 5 930,18 |

| for May | 3 016 213,07 | 6 032,43 |

| for June | 3 390 414,87 | 6 780,83 |

Before filling out Table 2, specialists from Tornado LLC verified mutual settlements with the Social Insurance Fund and collected information from bank statements on insurance payments, broken down for each month of the second quarter.

For Table 5 of the Calculation, information about the special assessment and medical examinations performed at the beginning of the year was provided by employees of the company’s HR department.

How Tornado LLC will reflect this data in 4-FSS, see the sample below:

Table 3 “Expenses for OSS from NS at work and occupational diseases”

| Line 1, 4 and 7 | Expenses incurred under OSS from NS and occupational diseases |

| Substrings 2 and 5 | Expenses for external part-time workers |

| Substrings 3, 6 and 8 | Expenses to another organization |

| Line 9 | Expenditures on preventive measures to reduce injuries at work |

| Line 11 | The amount of benefits accrued but not paid, except for benefits accrued in the last month |

| Column 3 | Paid days of incapacity for work due to national emergency and occupational diseases |

| Column 4 | Expenses since the beginning of the year, offset against contributions to OSS from the National Social Security and occupational diseases |

How to submit 4-FSS and what to do if the report is not accepted

The following example will help us understand the 4-FSS reporting deadlines:

According to the data of the previous billing period, the number of individuals in whose favor contributions for injuries were calculated and paid was:

- in Medvezhiy Ugol LLC - 15 people;

- in Tornado LLC - 98 people;

- at IP Trukhnina M.V. — 7 people

All policyholders plan to report for the 2nd quarter of 2021 to Social Insurance in electronic form. According to paragraph 1 of Art. 24 of Law No. 125-FZ, such a report must be sent no later than July 25, 2018.

However, LLC “Medvezhiy Ugol” and IP Trukhnina M.V. there is a choice: they can report not only electronically, but also on paper (since the number of specified policyholders does not exceed 25 people).

If a paper 4-FSS is issued, you need to focus on another valid reporting date - 07/20/2018. No later than this date, the report must be accepted by FSS specialists, otherwise policyholders cannot avoid fines.

Pushing the date of submitting 4-FSS closer to the deadline reporting dates is dangerous. If errors are found in the calculation, it will be considered failed.

Among the most common errors identified when submitting electronic 4-FSS are:

- impossibility of decrypting the report file or checking the digital signature (error code (EC) “10” or “11”);

- incorrect format of the policyholder's registration number or FSS department code in the certificate (KO “15” or “16”);

- incorrect file name or format (KO “505” or “508”);

- the file has a zero size (KO "518").

These and other shortcomings in 4-FSS need to be corrected, which may take some time. For example, when it is necessary to reissue a certificate or resolve an error. Submitting the 4-FSS in advance will allow you to calmly correct any identified errors and report to Social Insurance on time.

Deadline for submitting 4FSS for the 3rd quarter of 2021

The method of reporting depends on the number of personnel of the employing structure. Current legislation offers two possible options:

- The number of employees is up to 25 people inclusive

The organization has the right to choose: submit the report electronically or on paper. The deadline for submitting the form for the 3rd quarter is October 22, 2018. It is moved to this date because October 20 is a Saturday, a non-working day.

- Number of personnel more than 25 people

The only possible way is electronic submission of the form. The deadline for submitting 4FSS for 9 months of 2021 is 10.25.18. There are no transfers because this is a working day - Thursday.

Paper submission of reports assumes that the completed form is brought to the Federal Tax Service by the director of the company, private entrepreneur or other authorized person acting under a power of attorney drawn up in accordance with existing regulations. The document is considered received from the moment when the copy remaining with the business entity is marked with acceptance. The second submission option is to send the documentation by Russian post.

If a company submits a 4FSS report for 9 months of 2021 electronically, it generates a file that is certified with an electronic signature. The latter is issued in advance at the certification center. The company pays the established fee and collects a package of documents confirming the authority of the person for whom the electronic signature is being made,

It is then possible to submit a report via TKS if the company has an agreement with an operator, for example, with the Kontur system. The document is considered submitted when the acceptance receipt arrives.

If there is no agreement with operators, the 4FSS report for the 3rd quarter of 2018 can be submitted through the official FSS website. The employer first creates a file in XML format, then sends it to the Fund for review. The form is considered submitted when it has passed formal inspection and the recipient has sent a receipt.

The third way to submit reports electronically is to bring them to the Fund on a flash drive. 4-FSS for the 3rd quarter of 2021 must be certified with an enhanced digital signature, after which the data is transferred to authorized government employees who carry out their primary control.

4-FSS report in 2021

The most important thing: conclusions

Calculation 4 – FSS must be submitted by all organizations and individuals that pay income to individuals. This calculation must be submitted to the territorial body of the Federal Social Insurance Fund of the Russian Federation no later than July 25, 2021 (if submitted electronically) and July 20 (if submitted in paper form).

In the calculation, it is necessary to fill out the title page and tables 1, 2, 5. You also need to fill out (clause 2 of the Procedure for filling out calculation 4 - FSS):

- table 1.1 - if you temporarily sent your employees to another organization or to an individual entrepreneur under a personnel supply agreement;

- table 3 - if you paid insurance coverage to individuals, for example, temporary disability benefits due to an industrial accident;

- Table 4 - if you had any accidents at work during the reporting period.

Read also

06.01.2018

How to submit an updated report?

The need to submit an updated 4-FSS calculation for the 3rd quarter of 2018 arises for an economic entity in the following situations:

- there were errors in the original version;

- Some data were incomplete or missing, which led to an underestimation of insurance premiums.

If inaccuracies in the original file do not lead to an underestimation of the amount of premiums, the policyholder has the right to provide an “adjustment” of his own free will; the law does not oblige him to do this. Experts are unanimous in their opinion that in order to avoid disputes with the Fund, it is better to submit an adjustment form.

According to the provisions of 125-FZ, the updated calculation of 4-FSS for 9 months of 2018 is submitted to the Fund on the form that was valid at the time of drawing up the original form.

Current legislation assumes that the “clarification” indicates an adjustment number other than “000”. For example, if a company submits an adjustment document for the first time, it is entered “001”, if it is repeated – “002” and so on in order. The report is filled out completely, and not just those tables in which the business entity wishes to make changes. Attached to it is a covering letter, drawn up in any form, explaining what changes the policyholder made and for what reason.