Payment of dividends is made from net profit, based on the decision of the founders. The calculation of net profit is made only after the end of the financial year, however, the organization can make a decision regarding the payment of dividends once a quarter, once every six months or once a year. The financial results report contains information on the amount of net profit for the reporting year in line 2400. As for all retained earnings (in relation to the reporting and previous period), it is indicated in line 1370 of the balance sheet.

If we consider dividends declared for the reporting year (in the absence of accounting entries), then information about them is included in the Explanations to the financial statements and balance sheet. In this case, dividends paid during the reporting period are separately entered into section III of the balance sheet, a line to be determined independently (Letter of the Ministry of Finance of Russia No. 07-05-06/302 dated December 19, 2006). Dividends for the reporting year are indicated in parentheses in line 3327 of the Statement of Changes in Capital.

Payment of distributed funds can be made in the form of:

- Money;

- property (including real estate);

- interest on preferred shares, etc.

The charter of the enterprise must describe how dividends are distributed: in accordance with the share of the participant (shareholder), or the distribution will be carried out in another way.

Taxation of dividends

Dividends received from participation in Russian organizations are subject to a number of taxes.

For residents of the Russian Federation:

- Personal income tax (personal income tax) applies to shareholders (participants) who are residents of the Russian Federation. They are subject to personal income tax at a rate of nine percent.

- Income tax. Russian participating enterprises (shareholders) of Russian and foreign firms must be subject to income tax at a rate of nine percent and zero percent, respectively.

For foreign participants:

- Personal income tax. Phys. persons who are not considered tax residents of the Russian Federation are taxed at a rate of fifteen percent.

Consultations: Corporate income tax

The transfer of personal income tax must be made on the day of payment of dividends to shareholders (participants) or within the next day after withdrawal of funds from the current account for payment of dividends. The transfer of income tax is made no later than the next day after the dividends were transferred.

Russian enterprises that are tax agents (organizations that are the source of receipt and payment of income) are required to provide income tax reporting.

Income from dividends received and issued, as well as the calculation of income tax, are indicated in the income tax return as follows:

- In the case of payment of dividends to a Russian organization: subsection 1.3 of section 1 of the income tax declaration contains the calculation of tax on certain types of income, while Sheet 03 (calculation of income tax, which is withheld by the tax agent - the source of payment of income) includes certain types of income. Information on tax calculation is given in paragraph 2 of Art. 275 of the Tax Code of the Russian Federation, and the rules for filling out sheet 03 are indicated within the framework of Order of the Federal Tax Service of Russia dated November 26, 2014 No. MMV-7-3/

- When receiving dividends from a Russian or foreign enterprise: sheet 04 (calculation of corporate income tax on income, which is calculated according to rates that differ from the rate presented in paragraph 1 of Article 284 of the Tax Code of the Russian Federation) contains information on dividend income from their participation in other organizations.

If you require more detailed explanations about the application of the zero percent income tax rate, about dividends that are received and issued in kind, or about how dividends and their calculations are reflected in tax and accounting reports, please contact us for a free consultation by calling 8(812) 425- 24-05.

Was the article useful? Share on social networks!

Do you want to receive new information in a timely manner?

Subscribe to our newsletter

Tax Code of the Russian Federation), and income tax on dividends - no later than the day following the day of transfer of dividends (clause 4 of Article 287 of the Tax Code of the Russian Federation). The amounts of accrued taxes on dividends are not reflected in tax accounting. How to reflect personal income tax on dividends in tax accounting "1C: Accounting 8" Income of individuals from equity participation in the activities of an organization received in the form of dividends and the amount of calculated tax on this income for the purpose of reporting personal income tax are registered in the program for each individual using the document Tax accounting operation for personal income tax, which is available from the journal All documents for personal income tax in the Employees and salary section (Fig. 4). Rice. 4.

Deadlines for issuing interim dividends

According to the general rules, the deadline for issuing dividends for an LLC cannot exceed 60 days from the date of adoption and signing of the relevant decision (Clause 3, Article 28 of the LLC Law). In accordance with paragraph 6 of Art. 42 of the Law on JSC, the period for paying dividends to a nominal holder and a trustee who is a professional participant in the securities market, who are registered in the register of shareholders, should not exceed ten working days, and to other persons registered in the register of shareholders - 25 working days from the date on which the persons are determined entitled to receive dividends.

If during this period the shareholder (participant) has not received the money, he is given three years from the expiration of this period to submit a claim to the organization for reimbursement of part of the profit. The charter may indicate a longer period for submitting a claim, but it cannot exceed five years (clause 9 of article 42 of the Law on JSC, clause 4 of article 28 of the Law on LLC).

Please note that if dividend payment deadlines are violated, shareholders (participants) have the right to demand interest for the use of other people's funds (Article 395 of the Civil Code of the Russian Federation).

Accounting for paid and received dividends in “1c: accounting 8” ed. 3.0

Attention

Consequently, they are not subject to insurance contributions for compulsory pension insurance, compulsory social insurance in case of temporary disability and in connection with maternity, as well as compulsory health insurance. The income in question is also not subject to insurance contributions for compulsory social insurance against industrial accidents and occupational diseases.

How to calculate income tax and personal income tax on dividends Since January 1, 2014, the formula for calculating the income tax that needs to be withheld from a Russian organization has been changed. Now it is contained in paragraph 5 of Article 275 of the Tax Code of the Russian Federation (amended by Federal Law No. 306-FZ of November 2, 2013).

The same formula is applied when calculating personal income tax withheld from residents of the Russian Federation (Article 214 of the Tax Code of the Russian Federation).

Insurance premiums

Insurance premiums are not charged on the amount of dividends. It does not matter to whom they are paid - the founders who work in the company, or participants who do not work in the organization. The fact is that the object of taxation with insurance premiums is payments and other remuneration in favor of individuals within the framework of labor relations and under civil contracts, the subject of which is the performance of work or the provision of services (Article 420 of the Tax Code of the Russian Federation). Payment of dividends, including to company employees, does not occur within the framework of labor relations. This means that such payments are not subject to insurance premiums.

There is also no need to charge insurance premiums for compulsory social insurance against industrial accidents and occupational diseases (clauses 1, 2, Article 20.1 of the Federal Law of July 24, 1998 No. 125-FZ “On compulsory social insurance against industrial accidents and occupational diseases ").

Please note: since the payment of dividends to members of the company, even if they are its employees, does not occur within the framework of labor relations or relations within the framework of civil contracts, the subject of which is the performance of work or the provision of services, then dividends do not need to be reflected in the calculation of insurance premiums neither as part of the total amount of payments, nor as part of the amount of non-taxable payments.

Dividends: taxation issues and reflection in financial statements

284 Tax Code of the Russian Federation. The total amount of dividends subject to distribution does not include the amount of dividends payable to a foreign organization and (or) a non-resident individual of the Russian Federation (clause 6 of article 275 of the Tax Code of the Russian Federation, clause 3 of clause 3 of article 284 and clause 3 of article 224 dividend amounts due:

- Russian organizations (including those using the simplified tax system, unified agricultural tax and UTII) are subject to income tax at a rate of 9 percent;

- Russian organizations that for at least 365 consecutive calendar days own at least half of the authorized capital of the dividend-paying organization are subject to income tax at a rate of 0 percent;

- foreign organizations are subject to income tax at a rate of 15 percent (taking into account the specifics provided for in Article 275 of the Tax Code of the Russian Federation);

- individuals who are tax residents of the Russian Federation are subject to personal income tax at a rate of 9 percent;

- Individuals - non-residents of the Russian Federation are subject to personal income tax at a rate of 15 percent.

Income tax on dividends, including those received from foreign organizations, is paid to the federal budget (clause 2 p.

Payment of dividends leads to tax agency

The organization that pays dividends is recognized as a tax agent. If dividends are received by a shareholder (participant) - a legal entity, then tax agency for income tax arises (clause 3 of Article 275 of the Tax Code of the Russian Federation). In the case when the recipients of dividends are individuals, the organization is a tax agent for personal income tax (clause 3 of article 214 of the Tax Code of the Russian Federation).

Once a company is recognized as a tax agent for income tax or personal income tax, then it is the company that must calculate the appropriate amount of tax, withhold it from the income of the shareholder (participant) and transfer it to the budget (clause 3 of article 214, clauses 1, 2 of article 226, Clause 3 of Article 275 of the Tax Code of the Russian Federation).

Dividend rates

Let's start with the situation when the shareholders (participants) of the organization are individuals. Here, the personal income tax rate will depend on whether the owner is recognized as a tax resident of the Russian Federation or not. If yes, then the tax rate will be 13% (clause 1 of Article 224 of the Tax Code of the Russian Federation). If dividends are received by a shareholder (participant) who is not recognized as a tax resident of the Russian Federation, then the personal income tax rate will be 15% (clause 3 of Article 224 of the Tax Code of the Russian Federation).

The income tax rate will also depend on whether the company receiving the dividends is recognized as a tax resident of the Russian Federation or not. If the shareholder (participant) is a Russian organization (and therefore a tax resident of the Russian Federation), then a rate of 0 or 13% may be applied to the amount of income received.

Zero taxation is possible if, on the day of making the decision to pay dividends, the organization receiving dividends has continuously owned for at least 365 calendar days at least a 50 percent contribution (shares) in the authorized (share) capital (fund) of the organization paying dividends or depository receipts giving the right to receive dividends in an amount corresponding to at least 50% of the total amount of dividends paid by the organization (subclause 1, clause 3, article 284 of the Tax Code of the Russian Federation). In letter No. 03-03-06/1/26032 dated May 30, 2014, specialists from the Ministry of Finance of Russia noted that when determining the 365-day period, it is possible to take into account the period of ownership of the contribution (share) of the organization receiving dividends from the moment the ownership of shares issued by the organization is transferred to it. organization paying dividends.

If the above conditions are not met, then a rate of 13% is used (subclause 2, clause 3, article 284 of the Tax Code of the Russian Federation).

For shareholders (founders) who are not tax residents of the Russian Federation, the income tax rate will be equal to 15% (subclause 3, clause 3, article 284 of the Tax Code of the Russian Federation).

Please note: for both personal income tax and income tax, the above tax rates apply unless other rates are established in international treaties on the avoidance of double taxation (Article 7 of the Tax Code of the Russian Federation).

Deadlines for payment of withheld taxes

As we have already said, the tax agent must pay to the budget the calculated and withheld income tax (NDFL) on dividends of shareholders (participants). Income tax is transferred no later than the day following the day of payment of dividends (clause 4 of article 287 of the Tax Code of the Russian Federation).

As for personal income tax, the deadline for transferring the tax to the budget will depend on the organizational and legal form of the organization paying dividends. If dividends are paid by an LLC, then personal income tax is transferred to the budget no later than the day following the payment (clause 6 of Article 226 of the Tax Code of the Russian Federation). But for JSC a different deadline is established - no later than a month from the date of payment of dividends (clause 4 of Article 224, subclause 3 of clause 9 of Article 226.1 of the Tax Code of the Russian Federation).

Where to show dividends paid on the balance sheet

The source for paying dividends is the company's net profit. It is calculated at the end of the financial year, although the decision to pay income to participants (founders) can be made once a quarter, every six months or a year.

Important

How operations for accrual and payment of dividends are reflected in the company’s accounting and reporting will be discussed in this publication. The basis for accrual of these incomes in the accounting of the organization are the minutes of the meeting of participants with the decision made on payment within the established time frame and an accounting certificate calculating the amounts due to each of the owners.

To combine information on accrued and paid dividends, use account 75/2 “Settlements with founders” and the subaccount “Settlements for payment of income”. If this type of income is received by a company employee, then account 70 “Payments with personnel for salaries” is used.

Since the amount of dividends to be distributed for all participants is the same, the calculation of the amount of income tax in the form of dividends of CJSC "InvestSoyuz" and the amount of personal income tax on income in the form of dividends of individual residents of the Russian Federation will be the same: H = 1,000,000 / (4,000 000 – 1,000,000) x 9% x (3,000,000 – 2,730,000) = RUB 8,100. The amount of personal income tax on income in the form of dividends of a non-resident individual of the Russian Federation (Tereshchenko E.N.) is calculated as follows: N = 1,000,000 x 15% = 150,000 rubles. How to accrue and pay dividends in “1C: Accounting 8” Reflection of accrued dividends to legal entities and individuals, as well as the accrual of income tax and personal income tax in the program is registered by the document Operation (Accounting and National Accounting), which is available via the hyperlink of the same name from the section Accounting, taxes, reporting (see Fig. 1). Rice. 1.

Reporting year – 2013; Line 010 – 4,000,000; Line 030 – 1,000,000; Line 041 – 3,000,000; Line 043 – 2,000,000; Line 070 – 2,730,000; Line 071 – 2,730,000; Line 091 – 90,000; Line 100 – 8 100; Line 120 – 8,100. The value in lines 040 and 090 is calculated automatically using the formulas specified in the indicators.

10): Line 010 – name of the legal entity - recipient of dividends; Line 020 – address of the location of the dividend recipient; Line 030 – information about the head of the organization - a participant in the company; Line 040 – contact phone number; Line 050 – date of transfer of dividends; Line 060 – amount of transferred dividends; Line 070 – the amount of income tax withheld when performing the duties of a tax agent. Rice. 10. Dividends distributed to participants (shareholders) are reflected in the financial statements as follows:

- in the balance sheet they reduce the amount of accumulated profit on line 1370 “Retained earnings (uncovered loss)” in the period of dividend accrual;

- in the statement of changes in capital (if prepared) - on a separate line 3327 “Dividends” in the period of accrual of dividends;

- in the cash flow statement (if compiled) - on a separate line 4322 “Payments - total for the payment of dividends and other payments for the distribution of profit in favor of the owners (participants)” in the period of actual payment of funds.

Who pays and withholds taxes on dividends A Russian organization paying dividends is recognized as a tax agent (clause 3 of Article 275 of the Tax Code of the Russian Federation).

Info

How to accrue received dividends in “1C: Accounting 8” Registration of received dividends in accounting is carried out manually using the document Operation (accounting and NU) on the date of the decision made by the general meeting of shareholders (Fig. 12). Rice. 12. Registration of dividends received in accounting Reflection of the amount of dividends received in the PR resource (the constant difference in the assessment of the obligation) in this case is necessary, otherwise the key rule of the ratio of transaction amounts will be violated (BU = NU + PR + VR), which will inevitably lead to errors in accounting

After performing routine operations to close the month (March), the program will generate the following transactions for calculating income tax (Fig. 13): Fig. 13. Movements of the regulatory document Calculation of income tax for March Using the document Operation (accounting and NU), you can reverse the entries for accrual of PNA and conditional income tax expense calculated from the amount of dividends received reflected in accounting (Fig. 14). Rice. 14. Manual adjustment of the routine operation for calculating income tax for March Registration of dividends received in tax accounting is carried out manually using the document Operation (accounting and accounting) on the date of actual receipt of funds according to the bank statement (Fig.

15). Rice. 15. Registration of dividends received in tax accounting Reflection of the amount of dividends received in the PR resource (the constant difference in the assessment of the liability) in this case is also necessary, otherwise the key rule of the ratio of transaction amounts will be violated (BU = NU + PR + VR).

What are the terms for repaying the founders' debt?

Dividends (partial and full amount of net profit) are paid to shareholders or members of the company periodically - once a quarter, six months or a year. This is done according to a resolution adopted by the joint meeting.

It can be accepted strictly if the following provisions are followed (MoF of the Russian Federation dated September 20, 2010 No. 03-11-06/2/147; Article 43 Law No. 208-FZ and Article 29 Law No. 14-FZ):

- accounting data for the reporting period show absolute profit;

- the authorized capital (AC) has been paid;

- the size of net assets is greater than the size of the charter capital and the reserve fund (for a joint-stock company, the excess of the prices of preferred shares over the par value is a plus), this should not change after the payment of income;

- there are no prerequisites for bankruptcy, and they will not exist after payment;

- the repurchase of shares under the existing conditions of the company's members has been completed;

- all those who left the company were paid for their parts (for LLC);

- the conditions for payment are taken into account: initially payments are made on preferred shares that have advantages, then on the remaining preferred shares, then on the rest.

The meeting makes a decision on payment, and then formalizes the minutes:

- amount of cash payments;

- type and date of payment;

- the amount of amounts for each specific type of shares (for joint stock companies);

- date when the list of society members will be compiled.

The founders of the company are liable for debts only with their own share in the authorized capital, and not with the property in general

According to available information, the meeting of members of the company determines the amount of payment for each specific participant, the decision depends on:

- the type and number of shares held by the participant;

- the size of his share in the company (provided that the charter does not provide for another form of distribution).

If a legal entity involves only one member of the company, then the minutes of the meeting will replace the decision made by a single participant.

Among the forms of payment, cash is preferable, but another is possible - in the form of property, but it is identical to sale and is extremely unprofitable from a tax point of view (letter of the Ministry of Finance of the Russian Federation No. 03-11-09/405).

Payment terms cannot cross borders:

- in a joint-stock company – 10 (for the main holder and trusted manager) and 25 (for other members of the company) working days from the date on which the list of participants was adopted;

- in an LLC – 60 days from the date of the resolution of the meeting.

If a participant does not have property to cover his debts, creditors have the right to demand that the entire part of the founder-debtor be allocated from the authorized fund

If a member of the company is not paid his due portion within the prescribed period, then he has the right to claim his funds for 3 years (if determined by the charter, the period can be extended to 5 years) from the moment:

- resolution decisions (for JSC);

- the end of a period of 60 days (for LLC).

After 3 and 5 years, amounts that have not been claimed will be returned to the organization's net profit.

Reflection of transactions with dividends in accounting

The basis for accrual of these incomes in the accounting of the organization are the minutes of the meeting of participants with the decision made on payment within the established time frame and an accounting certificate calculating the amounts due to each of the owners.

To combine information on accrued and paid dividends, use account 75/2 “Settlements with founders” and the subaccount “Settlements for payment of income”. If this type of income is received by a company employee, then account 70 “Payments with personnel for salaries” is used. The corresponding account is account 84 “Retained earnings”.

Accounting entries are made separately for each participant. The main wiring is as follows:

| Operation | D/t | K/t |

| At the end of the year | ||

| Retained earnings have been generated | ||

| On the date of the decision on payment | ||

| Income accrued to each owner | 75/2 (70) | |

| On the dividend payment date | ||

| Paid from the cash register or from a current account | 75/2 (70) | 50, 51 |

| Taxes withheld from accrued amounts (NDFL) | 75/2 (70) | |

| On the date of transfer of taxes to the budget | ||

| Taxes transferred |

Dividends from Russian LLCs

The article from the magazine “MAIN BOOK” is current as of March 7, 2014 N.A.

In practice, there is a prejudice that dividends are only allowed to be distributed at the end of the year.

Matsepuro, lawyer

The Letters from the Ministry of Finance mentioned in the article can be found: The remaining after-tax profit in an LLC can be distributed among the participants as dividends.

We recommend reading: At what distance from the property line can you build a house?

This is a rather labor-intensive process. First you need to calculate the amount of net profit that can be used for dividends. Then the participants must decide on the payment of dividends.

Then, the LLC, as a tax agent, is obliged to withhold tax from the amounts of dividends paid and transfer it to the budget. And even this is not the end - you need to report dividends to the Federal Tax Service.

Accountants have to solve all these problems. For the general meeting of participants, the accounting department of the LLC must prepare for them information about the amount of its net profit according to accounting records; .

This is the amount on line 1370 of the accounting

Dividends on balance sheet

To reflect the amounts of retained earnings (credit balance of the 84th account), line No. 1370 is allocated in the 3rd liability section of the balance sheet. At the end of the year, it records the total amount of profit (both for the reporting year and for previous periods), starting from the moment of existence companies. In this line, retained earnings will be reflected minus accrued but unpaid dividends for the reporting year.

Dividends are reflected in the balance sheet only if they are accrued and paid during the year. We are talking about so-called interim dividends. The sum total of all interim dividends,

paid in the reporting year for which the statements are prepared are recorded in the same place (in the “Capital” section) in a separate numbered line, enclosed in parentheses. Usually it is assigned the following serial number (for example, 1371, 1372).

Dividends declared at the end of the year are usually announced after the financial statements are approved. Consequently, this fact becomes an event after the reporting date, which means that such dividends cannot be recorded in the balance sheet.

Following the recommendations of PBU 7/98, companies that declared annual dividends based on the results of work, in the period of time between the reporting date and the date of approval of the reporting forms for the year, disclose information about accrued dividends in an explanatory note to the balance sheet. Of course, no accounting entries are made during the reporting period either.

How to pay dividends? | The company is right Respect

ANSWER:

Source of publication: Glavnaya Kniga Publishing House, 2014

HOW MUCH OF PROFIT CAN BE DISTRIBUTED AS DIVIDENDS?

Participants of an LLC (JSC) can distribute as dividends the amount reflected in the balance sheet on line 1370 “Retained earnings”. This is the profit of both the reporting year and previous years (clause 1 of the Federal Tax Service Letter dated 10/05/2011 N ED-4-3/ [email protected] ).

The amount reflected on line 1370 can be distributed as dividends in full:

– if there is no balance on balance sheet line 1320 “Own shares purchased from shareholders”;

– if there is a remainder for this line, but the following condition is met:

Dividends in the income statement

We remind you that the source of dividends is net profit. Information about its availability and amount as of the reporting date is contained in line 2400 of report No. 2. The accrual and payment of dividends are not reflected in this form, since this report was created to inform the user about the amounts and sources of profit and loss. Dividends do not form profit (they are paid out of it), much less are they considered expenses. As a category related to the reduction of capital, dividends are reflected in the statement of capital flows (SFC), and their payment is recorded in the statement of cash flows (CFDS) after the payment has been made.

Let's summarize. The amounts of dividends are reflected in the financial statements as follows:

- If they are accrued but not paid, then:

- in the balance sheet they reduce the amount of profit reflected in line 1370 “NP”;

- in the UDC in line 3327 “Reduction of capital - dividends” (when compiled by the company);

- During the payment period:

- in the ODDS on line 4322 “Payments for the payment of dividends and other payments for the distribution of profits in favor of owners (participants).”

Category: Banks

Postings when the founder pays the debt of the enterprise

The debt for dividends accrued to the founders is reflected in the accounting entry (entries are made on the date of adoption of the resolution by the participants):

- Dt 84 Kt 75 – dividend amounts are accrued for members of legal entities and individuals who are not employees of the organization paying the income;

- Dt 84 Kt 70 – dividend amounts are accrued for those who are employees of the income payer.

On the date of payment, a tax is charged, which is withheld upon payment (according to analytics, a division is made by type of tax):

- Dt 75 Kt 68 - for participants who are not employees (personal income tax);

- Dt 70 Kt 68 – for participants who work for the payer (personal income tax).

Dividends were paid on the date of payment, divided by members of the company:

- Dt 75 Kt 51 (50) - for members who do not work at the payer enterprise;

- Dt 70 Kt 51 (50) – for recipients of employees of the payer enterprise.

Taxes paid on the date of payment of dividends (divided by members and type of tax): Dt 68 Kt 51 .

Unclaimed dividends were written off to profit, the deadlines for which had expired: Dt 70 (75) Kt 84.

Similar articles:

Which line of the balance sheet shows contributions to the property of the LLC?

Which account are business expenses recorded in?

Which account is the interest on the loan reflected in?

What should you do when preparing a calculation of insurance premiums for people on maternity leave? In the calculation of insurance premiums, all income is reflected in line 030, including benefits (up to 1.5 and 3 years) and maternity benefits. There are 6 ND in the report

Gazprom will pay dividends for 2021 of 8.04 rubles. or 20% of profit according to IFRS

Line 630 “Debt to participants (founders) for payment of income”

Home/ Accounting statements/ Line 630

Line 630 of financial statements

refers to

the balance sheet

up to 2011.

Line 630 “Debt to participants (founders) for payment of income”

This line reflects the balance of account 75 “Settlements with founders” subaccount 75-2 “Settlements for payment of income”. This is the amount of the organization's outstanding debt for dividends due for payment.

When compiling the balance sheet for 2009, this line shows the amount of dividends accrued for payment if in the specified period a general meeting of shareholders (participants) of the company was held to distribute dividends and an appropriate decision was made.

The distribution of net profit for the payment of dividends is reflected by the accounting entry:

Debit 84 subaccount “Net profit of the reporting year” Credit 75 subaccount “Calculations for dividends” - reflects the amount of net profit allocated for the payment of dividends.

If the founder (participant) of the company is also its employee, the dividends due to him and other similar payments are accrued on account 70 “Settlements with personnel for wages” subaccount “Income from participation in capital”. The credit balance of this subaccount should be reflected on line 630.

Please note: a loan received by an organization from the founder is reflected in accounting in the same way as any other loan - on account 66 “Settlements for short-term loans and borrowings” or 67 “Settlements for long-term loans and borrowings”. In the balance sheet, the unrepaid amount of such a loan is shown as part of accounts payable: on line 510 (if the loan is long-term) or line 610 (if the loan is short-term) together with the interest accrued under the agreement. Line 630 is intended only to reflect debt to the founders for income from participation in the authorized capital.

Main rules

Business participants have the right to net income from it among themselves. Then the question arises of how to calculate the profit that can be disposed of in this way. In this case, the accountant's task is quite simple. There are two ways:

- just look at column 1370 of the balance:

- see the credit balance of account 84. It has the same name (see figure above).

Note that accounting for dividend payments implies that it is possible to divide both the net income of the past year and previous periods.

In practice, there is a prejudice that dividends are only allowed to be distributed at the end of the year. Nothing like this. For example, Law on LLC No. 14-FZ allows you to divide net income for each quarter. Basically, it depends on the success of the business. Also see “Dividend Payment Timing”.

useful links

►Economic literature◄ ►Methodology of financial analysis◄ ►Forms of financial statements◄ ►The largest joint stock companies in Russia◄

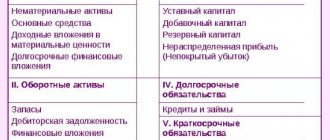

The third section of the balance sheet liability “Capital and reserves” consists of the following items.

| III. Capital and reserves | Line code |

| Authorized capital (80) | |

| Own shares purchased from shareholders (81) | |

| Additional capital (83) | |

| Reserve capital (82) | |

| including: | |

| reserves formed in accordance with legislation | |

| reserves formed in accordance with the constituent documents | |

| Retained earnings (uncovered loss) (99) | |

| Total for Section III |

The table presented above reflects the diagram of the third section of the balance sheet liabilities, indicating the accounts, the balances of which are reflected in the corresponding line of the balance sheet.

“Authorized capital” (line 410).

This article shows the amount of the authorized capital (account balance 80 “Authorized capital”) in accordance with the provisions of the constituent documents. An increase or decrease in the authorized capital is made only after changes have been made in the prescribed manner to the constituent documents (charter) of the organization (organization).

According to the line “ Own shares purchased from shareholders”

shows the balance of the value of the organization’s own shares, which are purchased from shareholders, recorded on account 81 “Own shares (shares)”.

“Additional capital” (line 420).

This line shows the amount of increase in the value of the organization’s property reflected in the asset balance sheet, identified based on the results of their revaluation, as well as the amount of share premium of joint-stock companies (i.e., amounts received in excess of the nominal value of the company’s outstanding shares (minus the costs of their sale) ) and targeted financing received in the form of investment funds. Since the authorized capital is fixed in the constituent documents, it became necessary to take into account the increase in the equity capital of an economic entity. Account 83 “Additional capital” is intended for these purposes.

“Reserve capital” (line 430).

Personal income tax reporting

As we have already said, companies paying dividends are recognized as tax agents for personal income tax. This means that, according to paragraph 2 of Art. 230 of the Tax Code of the Russian Federation are required to submit to the tax authorities:

— information about the income of an individual in form 2-NDFL (approved by order of the Federal Tax Service of Russia dated October 30, 2015 No. ММВ-7-11/ [email protected] ;

— calculation according to form 6-NDFL (approved by order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11 / [email protected] ).

Form 2-NDFL

Let's start with the fact that JSCs that pay dividends to their individual shareholders do not have to submit information in Form 2-NDFL. The fact is that such organizations are recognized as tax agents on the basis of Art. 226.1 Tax Code of the Russian Federation. And in paragraph 4 of Art. 230 of the Tax Code of the Russian Federation states that in this situation, tax agents submit information to the tax authority in the form, manner and time frame established by Art. 289 of the Tax Code of the Russian Federation for the presentation of tax calculations by tax agents for income tax. As we said above, Appendix No. 2 to the income tax return is filled out for these purposes. This is precisely the position taken by the tax authorities (letter dated 02/02/2015 No. BS-4-11/ [email protected] ).

As for LLCs, such organizations fill out form 2-NDFL. Moreover, if dividends were taxed at a tax rate of 13%, then in section 3 “Income taxed at the rate of 13%” and section 5 “Total amounts of income and tax”, the dividend amounts are reflected together with other income taxed at the specified rate. Specialists of the Federal Tax Service of Russia drew attention to this point in a letter dated March 15, 2016 No. BS-4-11/ [email protected]

Thus, if a 15% rate was applied to dividends, then you need to fill out Section 3 and Section 5 separately (Chapter I of the Procedure for filling out Form 2-NDFL).

Let us remind you that for dividends the income code is 1010. The amount of dividends is indicated in full, including personal income tax.

Form 6-NDFL

Dividends are shown in calculations in form 6-NDFL for the period in which they were actually paid (subclause 1, clause 1, article 223 of the Tax Code of the Russian Federation). Accrued but unpaid dividends are not reflected in the calculation.

In section 1 you need to indicate:

- on line 010 - tax rate (13 or 15%);

- on lines 020 and 025 - the entire amount of dividends paid in the reporting period, together with personal income tax;

- on line 030 - deduction from dividends, if applied;

- on lines 040, 045 and 070 - personal income tax on dividends.

Please note: if a company uses different tax rates when taxing dividends, then you will need to fill out lines 010-050 of section 1 of the calculation separately.

In section 2, in a separate block of lines 100-140, all dividends paid on one day are reflected, indicating:

- in line 100 - the date of payment of dividends;

- in line 110 - dates of personal income tax withholding;

- in line 120 - the deadline for transferring personal income tax;

- in lines 130 and 140 - the amount of dividends together with personal income tax and the amount of withheld tax.

Dividends paid on the last working day of the reporting period are not shown in section 2, since their payment deadline falls on the next reporting period. Therefore, they are reflected in section 2 for the next quarter (letter of the Federal Tax Service of Russia dated November 2, 2016 No. BS-4-11 / [email protected] ).