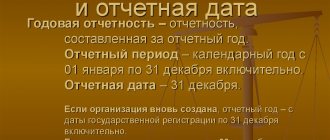

Forms of annual financial statements

- Balance sheet (form No. 1);

- Report on the financial results of the enterprise (reporting form No. 2);

- Statement of changes in capital (form No. 3);

- Cash flow statement (reporting form No. 4);

- Appendix to the balance sheet (reporting form No. 5) and auditor's report (required only for those who are required to conduct annual audits).

Small businesses have developed their own accounting submission forms:

- Simplified Balance Sheet (Form No. 1);

- Simplified report on the financial activities of the enterprise (reporting form No. 2).

| Preparation and submission of reports for individual entrepreneurs and LLCs Cost of reporting

|

Management reporting

Stages of formation and preparation of management reporting

- Diagnostics of the existing control system

- Creation of a management reporting methodology

- Design and approval of the company's financial structure

- Formation of a budget model

- Approval of budget policy

- Audit of accounting systems

- Automation

Important aspects when preparing management reporting: forms and examples. Management reporting is one of the most important sources of obtaining information about the company’s performance, based on a set of financial, sales, marketing, production and other indicators.

Information in management reporting should be economically interesting and actively used by managers, founders and business owners. The data disclosed in management reporting is necessary for the analysis of all activities. This helps to timely identify the reasons for possible deviations from the parameters set by the business strategy, as well as show reserves (financial, material, labor, etc.) that have not been used by the company until this time.

Below are 7 stages of formation and preparation of management reporting.

Step 1. Diagnostics of the existing management system in the company

This stage is necessary to analyze the organizational structure of the company; the format of process modeling is determined. If the company has business process diagrams and their descriptions, these documents are analyzed and the main problem areas that require optimization are identified.

| Diagnostic goals | Search for systematic approaches to increasing the efficiency of management reporting |

| Classification and analysis of existing reporting forms |

|

| Improving the quality and reducing the time required to obtain output analytical information necessary for making quality management decisions. | Analytical reports are of high value when they can be obtained in a short time and contain information in a form that best meets the needs of the employee who makes decisions based on this report. |

| Increasing the reliability of stored information. | To make decisions, you must rely only on reliable information. It is not always possible to understand how reliable the information presented in the reports is; Accordingly, the risk of making poor-quality decisions increases. On the other hand, if an employee does not bear official responsibility for the accuracy of the information entered, then with a very high degree of probability he will not treat the information with due care. |

| Increasing the analytical value of information. | A non-systematic approach to entering and storing information leads to the fact that, despite the fact that large amounts of information are entered into the database, it is almost impossible to present this information in the form of reports. Non-systematicity here means the input of information by employees without the development of general rules, which leads to a situation where the same information is presented to different employees in a different form from each other. |

| Elimination of inconsistency and inconsistency of information | If there is unclear clarity regarding the division of responsibilities and rights between employees to enter information, the same information is often entered multiple times in different departments of the company. In combination with a non-systematic approach, the fact of duplication of information may even be impossible to determine. Such duplication makes it impossible to obtain a complete report based on the entered information. |

| Increasing the predictability of obtaining a certain result | Decision making is almost always based on assessing information from past periods. But it often happens that the necessary information was simply never entered. In most cases, it would not be difficult to store missing information if someone assumed in advance that it would someday be needed. |

| Result | Based on the diagnostics and decisions made, job descriptions are finalized, existing business processes are reengineered, reporting forms that do not provide information for data analysis are eliminated, KPI indicators are introduced, accounting systems are adapted to obtain actual data, and the composition and timing of management reporting are fixed. |

Step 2. Creating a management reporting methodology

This stage is necessary for delegating authority in terms of drawing up operating budgets and determining the responsibility of specific financial responsibility centers (FRCs) for drawing up certain budget plans (segments of management reporting).

Figure 1. Sequence of stages in constructing a management reporting methodology.

Goals and objectives solved as a result of the implementation of management reporting in the company:

- Establishing and achieving specific key performance indicators (KPIs);

- Identification of “weak” links in the organizational structure of the company;

- Increasing the performance monitoring system;

- Ensuring transparency of cash flows;

- Strengthening payment discipline;

- Development of an employee motivation system;

- Prompt response to changes: market conditions, sales channels, etc.;

- Identification of the company's internal resources;

- Risk assessment, etc.

The composition of management reports depends primarily on the nature of the company's activities. As practice shows, the composition of management reporting (master report) usually includes:

- Cash flow statement (direct method);

- Cash flow statement (indirect method);

- Gains and losses report;

- Forecast balance (managerial balance);

Figure 2. Example of a management reporting structure.

Figure 3. Relationship between the classifier of management reports and management accounting objects.

Consolidation of budgets

The preparation of consolidated management reporting is a rather labor-intensive process. Consolidated financial management reporting considers a group of interrelated organizations as a single whole. Assets, liabilities, income and expenses are combined into a common management reporting system. Such reporting characterizes the property and financial position of the entire group of companies as of the reporting date, as well as the financial results of its activities for the reporting period. If the holding consists of companies that are not connected with each other at the operational level, then the task of consolidating management reporting is solved quite simply. If business transactions are carried out between the companies of the holding, then in this case not everything is so obvious, because it will be necessary to exclude mutual transactions so as not to distort the data on income and expenses, assets and liabilities at the holding level in the consolidated statements. The company's budget policy needs to consolidate the rules and principles for eliminating VGOs.

Therefore, it is more expedient to use information systems. For these purposes, you can use the “WA: Financier” system. The system allows you to eliminate intra-company turnover at the level of processing primary documents and quickly obtain correct information, which simplifies and speeds up the process of generating management reporting and minimizes errors associated with the human factor. At the same time, the reconciliation of intragroup turnover, their elimination, the execution of corrective entries and other operations are carried out automatically.

Example of management reporting: Company A owns company B 100%. Company A sold goods for the amount of 1,500 rubles. The purchase of this product cost company A 1000 rubles. Company B paid for the goods delivered in full. At the end of the reporting period, Company B did not sell the product and it is included in its reporting.

As a result of consolidation, it is necessary to eliminate the profit (500 rubles) that the company has not yet received and reduce the cost of inventories (500 rubles).

To exclude VGOs and profits that Company B has not yet earned. Adjustments need to be made.

Result of management reporting consolidation

Figure 4. Forecast balance (managerial balance).

Determination of key performance indicators (KPI – Key performance indicators)

The introduction of key control indicators allows you to manage financial responsibility centers by setting limits, standard values or maximum boundaries of accepted indicators. The set of performance indicators for individual central financial districts significantly depends on the role of this center of responsibility in the management system and on the functions performed. The indicator values are set taking into account the company’s strategic plans and the development of individual business areas. The system of indicators can take on a hierarchical structure, both for the company as a whole, and with detail down to each center of financial responsibility. After detailing the top-level KPIs and transferring them to the levels of the Central Federal District and employees, staff remuneration, etc. can be linked to them.

Figure 5. Example of using key company indicators.

Control and analysis of management reporting and execution

For the execution of budgets included in management reporting, three areas of control can be distinguished:

- preliminary;

- current (operational);

- final.

The purpose of preliminary control is to prevent potential budget violations, in other words, to prevent unreasonable expenses. It is carried out before business transactions are carried out. The most common form of such control is the approval of requests (for example, for payment or shipment of goods from a warehouse).

Current control over budget execution involves regular monitoring of the activities of financial responsibility centers to identify deviations in the actual performance indicators from those planned. Conducted daily or weekly based on operational reporting.

Final control of budget execution is nothing more than an analysis of the implementation of plans after the close of the period, an assessment of the financial and economic activities of the company as a whole and for management accounting objects.

In the process of executing budgets, it is important to identify deviations at the earliest stages. Determine what methods of preliminary and current budget control can be used in the company. For example, introduce procedures for approving requests for payment or release of materials from the warehouse. This will allow you to avoid unnecessary expenses, prevent budget failure and take action in advance. Be sure to regulate control procedures. Create a separate budget control regulation. Describe in it the types and stages of inspections, their frequency, the procedure for revising budgets, key indicators and ranges of their deviations. This will make the control process transparent and understandable, and will increase executive discipline in the company.

Figure 6. Monitoring the implementation of planned indicators of management reporting.

Step 3. Design and approval of the company's financial structure

This stage includes work on the formation of classifiers of budgets and budget items, the development of a set of operating budgets, planning items and their relationships with each other, and the imposition of types of budgets on the organizational units of the company’s management structure.

Based on the organizational structure of the company, a financial structure is developed. As part of this work, financial responsibility centers (FRCs) are formed from organizational units (divisions) and a model of the financial structure is built. The main task of building the financial structure of an enterprise is to get an answer to the question of who should draw up what budgets in the enterprise. A correctly constructed financial structure of an enterprise allows you to see the “key points” at which profits will be formed, taken into account and, most likely, redistributed, as well as control over the company’s expenses and income.

The Financial Responsibility Center (FRC) is an object of the company’s financial structure that is responsible for all financial results: revenue, profit (loss), costs. The ultimate goal of any central financial institution is to maximize profits. For each central financial district, all three main budgets are drawn up: a budget of income and expenses, a cash flow budget and a forecast balance (managerial balance sheet). As a rule, individual organizations act as central financial districts; subsidiaries of holdings; separate divisions, representative offices and branches of large companies; regionally or technologically isolated types of activities (businesses) of multi-industry companies.

Financial accounting center (FAC) is an object of the company’s financial structure that is responsible only for some financial indicators, for example, income and part of the costs. For the DFS, a budget of income and expenses or some private and functional budgets (labor budget, sales budget) are drawn up. The DFS can be the main production workshops participating in unified technological chains at enterprises with a sequential or continuous technological cycle; production (assembly) shops; sales services and divisions. Financial accounting centers may have a narrow focus:

- marginal profit center (profit center) - a structural unit or group of units whose activities are directly related to the implementation of one or more business projects of the company that ensure the receipt and accounting of profit;

- income center - a structural unit or group of units whose activities are aimed at generating income and do not include profit accounting (for example, a sales service);

- investment center (venture center) - a structural unit or group of units that are directly related to the organization of new business projects, profits from which are expected in the future.

- cost center is an object of the financial structure of an enterprise that is responsible only for expenses . And not for all expenses, but for the so-called regulated expenses, the expenditure and savings of which the management of the Central Bank can control. These are departments that serve the main business processes. Only some auxiliary budgets are drawn up for central planning. The auxiliary services of the enterprise (housekeeping department, security service, administration) can act as a central protection center. A cost center may also be referred to as center (cost center) .

Figure 7. Design of the company's financial structure.

Step 4. Formation of a budget model

There are no strict requirements for the development of a classifier of internal management reporting. Just as no two companies are exactly alike, no two budget structures are exactly alike. Unlike formalized financial statements: a profit and loss statement or a balance sheet, management reporting does not have a standardized form that must be strictly followed. The structure of internal management reporting depends on the specifics of the company, the budget policy adopted by the company, the wishes of management regarding the level of detail of articles for analysis, etc. We can only give general recommendations on how to draw up the optimal structure of management reporting.

The structure of management reporting should correspond to the structure of the company's daily activities. See also “Classification of costs in management accounting”

Figure 8. Scheme of interaction of budget forms using the example of the simplest budget model.

Classification of items using the example of a Cash Flow Statement

Figure 9. Execution of the cash flow budget (CF (BDDS)).

Step 5. Approval of budget policy and development of regulations

Budget policy is formed with the aim of developing and consolidating the principles for the formation and consolidation of indicators for these items and methods for their assessment. This includes: determination of the time period, planning procedures, budget formats, action program of each of the participants in the process. After developing the budget model, it is necessary to move on to regulating the budget process.

It is necessary to determine which budgets are formed in the company and in what sequence. For each budget, it is necessary to identify a person responsible for preparation (a specific employee, a central federal district) and someone responsible for the execution of the budget (the head of a department, a head of a central federal district), and set limits, standard values or maximum boundaries for the performance indicators of a central federal district. It is imperative to form a budget committee - this is a body created for the purpose of managing the budget process, monitoring its execution and making decisions.

The next step is to transfer the planning, execution and completion phases to the schedule. The formed plan - schedule will be the budgeting regulations for the enterprise.

Figure 10. Enterprise budgeting planning phases.

Step 6. Audit of accounting systems

At the stage of development and approval of the composition of the company’s management reporting, it is also necessary to take into account that the classifier of budget items must be sufficiently detailed to provide you with useful information about the company’s income and expenses. At the same time, you need to understand that the more levels of detail are allocated, the more time and labor costs will be required to compile management reporting, budgets and reports, but the more detailed analytics can be obtained.

It is also necessary to take into account that as a result of developing a management reporting methodology, adaptation of accounting systems may be required, because To analyze budget execution, planned indicators will have to be compared with available actual information.

Videos of past webinars on the topic “Management Accounting / IFRS”

Look

Step 7. Automation

This stage includes work on selecting a software product, creating technical specifications, implementation and maintenance of the system.

Date of last update: 08/25/2016 16:07

See also “Responsibilities of a financial manager”

Requirements for the preparation of annual financial statements

The main requirement is the reliability of the data, i.e. the indicators must be so reliable that any user of the reporting (whether external or internal) should not doubt the indicators of the enterprise’s economic activity.

The requirement for timeliness of data also affects the quality of the annual reporting; data must be reflected exactly in the reporting period in which they occurred.

Also, all indicators must be comparable, i.e. There must be an interconnection between these forms and accounting registers and declarations.

The principle of completeness indicates that all reporting data must be reflected in full; if completeness is lacking, then this fact must be reflected in the explanatory note.

What information must be included in the LLC's annual report?

Sample annual report of LLC

Be sure to include a section on the state of net assets in the LLC's annual report. Information in it is provided for the last three completed financial years, including the reporting year, with indicators of the dynamics of changes in net assets and authorized capital. If the LLC has existed for less than three years, information is indicated for each completed financial year (clause 1, clause 3, clause 3, article 30 of the LLC Law).

In order for society members to evaluate the company’s activities over the past year, we recommend:

- include the following information in the annual report:

— about the company — registration data of the LLC, structure of management bodies, name of the industry in which the company operates;

- about the results of the company's work - the main results achieved: financial, investment, strategic, for example, agreements and agreements with partners;

— about the prospects for the development of society — about plans and goals for a certain period of time (several periods);

- about payments of profit to participants - whether profit was paid to the participants of the company or not, if it was paid, then in what volume;

- about the director - full name, expiration date, length of service;

- attach to the annual report:

— report on interested party transactions;

— annual accounting (financial) statements;

— auditor’s report on the accounting (financial) statements (if any);

— conclusion of the audit commission (if any).

Contents of the balance sheet

The balance sheet is compiled on the basis of the General Ledger data for accounts and subaccounts at the end of the reporting period. In small businesses, many do not maintain a General Ledger, but fill out a Business Transaction Book. For those who keep records using software, all accounting registers, as well as the balance sheet, are generated automatically. You just have to compare the data. It should be noted that some balance sheet items are filled out by balance, for example 50 “Cash Office”, 51 “Cash Account”, etc. The main document for filling out the balance sheet is PBU 4/99.

How is the annual accounting statement approved?

Approval of the annual financial statements is documented in the minutes of the general meeting of shareholders or participants of the LLC. If there is only one participant in the LLC, the approval of the annual financial statements is formalized by the decision of the LLC participant.

Legislative requirements for the procedure for drawing up minutes of the general meeting of shareholders and participants of an LLC were approved, respectively, clause 2 of Art. 63 of Law No. 208-FZ and Art. 181.2 of the Civil Code.

The minutes of the general meeting of shareholders indicate:

- place and time of the general meeting of shareholders;

- the total number of votes possessed by shareholders - owners of voting shares of the company;

- the number of votes held by shareholders participating in the meeting;

- chairman (presidium) and secretary of the meeting;

- meeting agenda.

The minutes of the general meeting of LLC participants must indicate:

- date, time and place of the meeting;

- information about persons who took part in the meeting;

- voting results for each item on the agenda;

- information about the persons who carried out the vote count;

- information about persons who voted against the meeting’s decision and demanded that this be recorded in the minutes.

However, in addition to the above requirements, one more thing has been established - the decision of the general meeting of participants must be notarized (clause 3 of Article 67.1 of the Civil Code of the Russian Federation). This requirement applies to solutions:

- non-public joint-stock company;

- OOO.

But notarization of decisions of participants of a non-public JSC or LLC is not necessary if the charter of these organizations establishes a rule on an alternative method of certifying the decision.

For a non-public JSC, an alternative is to certify the decision by the registrar who maintains the JSC register and performs the functions of the counting commission.

For an LLC, an alternative method is:

- signing of the protocol by all participants (or part of the participants);

- or the use of technical means that make it possible to reliably establish the fact of a decision being made, for example, using a video recording of a meeting;

- or using another method that does not contradict the law.

At the same time, the very decision of the general meeting of participants of a non-public JSC or LLC, according to which an alternative method of confirmation will be applied to the decisions of the company, also requires notarization (clause 2 of the Review of judicial practice on certain issues of application of legislation on business companies (approved by the Presidium of the Supreme Courts of the Russian Federation 12/25/2019)).

This rule that an alternative method of confirmation must be notarized applies as of December 26, 2019.

If, before December 26, 2021, the organization had already decided on an alternative method of certifying the meeting’s decision, then, in the opinion of the Federal Notary Chamber, it should also be notarized (FNP letter dated January 15, 2020 No. 121/03-16-3).

Contents of the income statement

The content of the financial results report contains such indicators as:

- profit from activities;

- operating income and expenses;

- on non-operating income and expenses;

- about extraordinary income and expenses.

This form is compiled mainly according to the indicators of accounts 90 “Sales” and 91 “Other income and expenses”. Also, this form must correspond to the indicators in the Profit Declaration.

znatpravo.ru

The annual report is prepared in free written form.

It is mandatory to include only information on net assets in the annual report.

To do this, provide information on the dynamics of changes in the size of net assets for the last three completed financial years, as well as their comparison with the authorized capital. If the size of your net assets is less than the authorized capital, you must indicate the reasons and factors that led to this situation, and a list of measures to correct it.

Otherwise, you can include any information in the annual report depending on the purposes of its preparation and the needs of participants for information that allows them to evaluate the results of the company’s activities.

Contents of the statement of changes in equity

This report is divided into sections.

- Section 1 “Capital” contains data such as the balances of the Authorized Capital, Reserve Capital, Additional Capital, and Reserve Fund.

- Section 2 “Reserves for future income” and section 3 “Evaluated reserves” contain data on reserves for vacations, doubtful debts, etc. formed at the beginning of the year.

- In section 4 “Change in capital” there is data on the amount of capital and its change.

Deadline for submitting the CEO's report to the founders

The director of the company by virtue of Art.

40 of the Law “On Limited Liability Companies” dated 02/08/1998 No. 14-FZ is accountable only to the meeting, since it is it that approves his candidacy. The charter of the LLC specifies the powers of the director and his legal status. The annual report is presented by the general director during the company's annual general meeting, a meeting of which on this issue is held no earlier than 2 months and no later than 4 months after the end of the financial year, by virtue of clause 2 of Art. 34 of Law 14-FZ.

The legislator does not define the concept of “financial year”, however, in Art. 14 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ, the term “reporting year” is used, which lasts from January 1 to December 31. Accordingly, the financial year will be equal to the calendar year. Therefore, the general meeting of participants must be held no later than April 30 of the year following the reporting year.

However, the legislator in Art. 15 of Law 402-FZ obliges the company to submit annual financial statements to the statistics body no later than 3 months from the end of the reporting year. This means that the director must report to the general meeting no later than the end of March of the year following the reporting year in order to submit it to the statistics body.

Structure of the annual report of a joint stock company

The list of information that is subject to disclosure in the annual report, i.e., the composition of the annual report of the joint-stock company, is determined by the JSC independently, taking into account the provisions of Federal Law No. 208-FZ dated December 26, 1995 and other legal requirements.

So, for example, a section on the state of net assets must be included in the annual report of a joint-stock company if, at the end of the second or each subsequent reporting year, the value of the net assets of the joint-stock company turned out to be less than its authorized capital (Clause 4, Article 35 of the Federal Law of December 26, 1995 No. 208 -FZ).

For those JSCs that are required to disclose information, the content of the annual report is regulated by the Regulations, approved. CBR 12/30/2014 No. 454-P.

This Regulation applies to:

- public JSC;

- non-public joint-stock companies that carry out public offerings of bonds or other securities;

- non-public joint-stock companies with more than 50 shareholders.

What the annual report of such JSCs should contain is specified in clause 70.3 of the Regulations. The information disclosed in the annual report, in particular, includes:

- information about the position of the joint-stock company in the industry;

- priority areas of activity of the JSC;

- report of the board of directors (supervisory board) on the results of the development of the joint-stock company in the priority areas of its activities;

- information on the volume of each type of energy resource used by the JSC in the reporting year (nuclear energy, thermal energy, electrical energy, electromagnetic energy, oil, motor gasoline, diesel fuel, heating oil, natural gas, coal, oil shale, peat and etc.) in kind and in monetary terms;

- JSC development prospects;

- report on the payment of declared (accrued) dividends on JSC shares;

- description of the main risk factors associated with the activities of the JSC;

- a list of major transactions completed by the JSC, indicating for each transaction its essential conditions and the management body of the JSC that made the decision to consent to its completion or its subsequent approval;

- list of interested party transactions completed by the JSC in the reporting year;

- composition of the board of directors (supervisory board) of the joint-stock company;

- information about the person holding the position of the sole executive body of the JSC (director, general director, chairman, manager, management organization, etc.) and members of the collegial executive body of the JSC;

- main provisions of the JSC policy in the field of remuneration and compensation of expenses;

- information on the approval of the annual report by the general meeting of shareholders or the board of directors (supervisory board) of the joint-stock company.

We confirm the accuracy and approve the report

The reliability of the data contained in the annual report of the JSC must be confirmed by the audit commission (clause 3 of Article 88 of the Federal Law of December 26, 1995 No. 208-FZ).

In general, the annual report of a JSC must be approved by the general meeting of shareholders (clause 11, clause 1, article 48 of the Federal Law of December 26, 1995 No. 208-FZ). However, it is first approved by the board of directors or supervisory board of the company. And if the JSC does not have a board of directors (supervisory board), the annual report is subject to preliminary approval by the person performing the functions of the sole executive body of the JSC. And this must be done no later than 30 days before the date of the annual general meeting of shareholders (clause 4 of article 88 of the Federal Law of December 26, 1995 No. 208-FZ). Let us remind you that the annual meeting of shareholders is held within the time limits established by the charter of the joint-stock company, but no earlier than 2 months and no later than 6 months after the end of the reporting year (clause 1, article 47 of the Federal Law of December 26, 1995 No. 208-FZ) .

However, the charter of a joint-stock company may entrust approval of the report exclusively to the board of directors or the supervisory board. And then the general meeting of shareholders no longer approves it (clause 13.1, clause 1, article 65 of the Federal Law of December 26, 1995 No. 208-FZ).

Annual report of the director of an LLC - sample and procedure for preparation

The legislator does not approve either the sample document or the requirements for its preparation, transferring the right to clarify the contents of the report to the company itself by indicating this in the constituent documents.

The report can be printed on the organization's letterhead and include several sections. It is signed by the director of the company and is not subject to mandatory publication.

Let's look at the approximate structure of the report:

- General information about the enterprise.

- Report on the implementation of decisions of the board of directors and participants of the LLC.

- Report on personnel policy.

- Contract work report.

- Report on the execution of the company's budget.

- Analysis of society's expenses/income.

- Report on investment activities.

- Conclusions.

- Applications.

NOTE! In some cases (if this is provided for by the organization’s charter), the director submits only the annual accounting report for approval (you can read more about this in the article “The procedure for preparing annual accounting reports”). Since the legislator does not specify what exactly should be contained in the text of the document, the meeting, at its discretion, can accept it as a report from the director to the company.

A sample of the CEO's annual report to the founders can be downloaded here:

Thus, the report of the director (or general director) to the founders is drawn up by him and contains an analysis of the company’s activities for the reporting year. A report must be drawn up and brought to the attention of the general meeting by the end of March of the year following the reporting year.