Let's find out the meaning of the term. This is an event in any organization, in wholesale and retail trade, to search for discrepancies between the fixed working capital recorded in the accounting register and their actual availability. Discrepancies often cause difficulties for the chief economist, because he will have to cover the shortfall in assets from employees in equal shares. And the excess can be used in the manner prescribed in the company’s charter. The incident is recorded in the ledger in the reporting period when the inspection took place. Let's figure out together what it is to capitalize surpluses during inventory, posting, why they appear and how to properly capitalize them.

Audit nuances and purpose

A comparison of information about the material base put on the balance sheet and reflected in the original document and their condition on the day when the reconciliation occurred is mandatory. The timing and procedure of the operation is determined by the manager, except in cases where this is prescribed by the Law of the Russian Federation “On Accounting” No. 402 and Order of the Ministry of Finance No. 34-n of 1998. If there are discrepancies, then measures are prescribed to eliminate the difference that can be taken according to a pre-drawn up and approved plan.

The fact of excess is noted in the accounting department, warehouse papers, where the discrepancy was revealed.

Tasks of inventory of fixed assets

The frequency and sequence of inventory of fixed assets at the enterprise is enshrined in its accounting policy. It is carried out by an inventory commission specially appointed by the head of the enterprise. During this process the following goals should be achieved:

- monitoring the correctness of the preparation of primary documentation on the movement of fixed assets;

- establishing the presence of the organization’s property at the places of operation and storage, as well as its condition;

- detection of unused, missing or unaccounted for objects;

- control of the correct determination of the value of property in accounting and their reflection in the balance sheet of the organization.

For what reasons do they appear?

Inspection helps to detect discrepancies between the recorded money and its actual availability today. They can be in the form of money, valuables, raw materials for production, movable and immovable property. The inventory commission, not interested in financial turnover, draws up a statement and submits it to the director for consideration. And he, in turn, sets the accounting department the task of ensuring that the department correctly capitalizes and records the excess in the accounting book. An eyeliner is needed when taking inventory of identified surplus fixed assets and materials.

Business Solutions

- shops clothing, shoes, groceries, toys, cosmetics, appliances Read more

- warehouses

material, in-production, sales and transport organizations Read more

- marking

tobacco, shoes, consumer goods, medicines Read more

- production

meat, procurement, machining, assembly and installation Read more

- rfid

radio frequency identification of inventory items More details

- egais

automation of accounting operations with alcoholic beverages Read more

Main reasons:

- If the reconciliation was carried out inaccurately.

- Large production volumes can lead to errors. When distributing products in a warehouse to customers, there is a high probability of unaccounted deliveries.

- An insufficient amount of working finance is introduced.

- Errors in warehouses when taking into account the issue of materials and products. That is, they issued a smaller batch than expected.

- During the release of goods, some models were accidentally replaced by others.

Dangerous middleman

But there are cases when, during an investigation, it turns out that the shortage did not arise through the fault of the receiving or sending party. After all, there is often an intermediary between two warehouses or companies - a carrier. The liability of a transport company is regulated by Chapter 40 of the Civil Code of the Russian Federation. Thus, Article 796 of the Civil Code of the Russian Federation states that the forwarder is liable for damage to goods unless he proves that the shortage of cargo occurred due to circumstances that the carrier could not prevent and the elimination of which did not depend on him.

In case of loss of transported goods, its cost is reimbursed in full. If only damage to the product was discovered, then the amount of compensation should cover the price by which the value of the product was reduced. In addition, the contractor returns to the sender the funds that were transferred for the service.

It should be remembered that documents on the reasons for the failure of the cargo, drawn up by the carrier, are taken into account by the court along with other documents that may serve as the basis for the liability of the carrier, sender or recipient of the cargo.

Verification steps

Everything must be carried out according to the plan drawn up by the leader. Moreover, the stages are observed in the following order:

- Preparation period. An order from the director is issued, which specifies the deadline for carrying out what is considered. A special commission of several people is created, where a chief is appointed. Those persons who will be responsible if inconsistencies are found during the inspection are determined.

- It all starts with creating an inventory of existing production property with a description of its appearance today.

- A comparison sheet is created, which reflects the information obtained during the inspection, as well as the information captured in the original documents.

- In case of discrepancy, a report is drawn up where everything will be indicated.

- Based on the data received, a certificate is issued. In addition, changes are made to the balance sheet, where missing money or other valuables are written off. And capitalized surpluses identified during inventory in a budgetary institution, VAT and profit are reflected by the accountant’s posting.

The inventory company must report at each stage to the head of the company and the chief economist.

Finding the culprit

If a shortage is detected, the company's management must decide at whose expense the damage will be written off. There are few options: if a company employee is to blame for the shortage of goods, then the company’s loss will be covered from the employee’s salary. But keep in mind that inspectors scrutinize these operations carefully. Questions may arise not only regarding taxation and accounting for deductions, but also regarding the legality of punishing an employee.

If the director nevertheless decides to cover the shortfall at the expense of the employee, it is necessary to take into account that there are several types of financial liability: full, limited or collective. Full compensation for damage is possible in several cases:

- when the law contains a direct reference to compensation in the event of a shortage of valuables entrusted to the employee on the basis of an agreement or a one-time document;

- when the damage was caused under alcohol, drug or toxic intoxication;

- when the damage was caused due to criminal actions recorded by a court verdict or as a result of an administrative offense;

- in case of disclosure of secret information or failure of the employee to fulfill his official duties;

- when full financial responsibility is established by an employment contract concluded with the head of the company, his deputy and the chief accountant.

If a collective agreement has been concluded with the guilty employees, then the goods are entrusted to all personnel. On this basis, the shortage can be withheld from a group of people.

Why is the inspection carried out?

It solves multiple problems that arise during the operation of an enterprise and its employees:

- The financially responsible person should be replaced periodically.

- It's no secret that large plants and factories sometimes employ "unclean" employees. If premises and workshops are not equipped with a security camera, then frequent reconciliations help to identify facts of theft.

- Force majeure also occurs when a farm suffers from various natural disasters (hail, flood, fire due to lightning).

- Questions when there is a change of management, sale of movable and immovable property, leasing, rental of premises or vehicles.

- Before drawing up the annual report, there must be control.

In addition to the above reasons for conducting a recount, the most common is constant monitoring of the condition and quantity of property of the enterprise. Therefore, a schedule for the procedure is drawn up in advance once a year. Typically this includes three to four inspections throughout the year.

When to take an inventory

Inventory is carried out before drawing up annual financial statements, but this is not the only case when it is necessary (clause 3 of article 11 of Federal Law dated December 6, 2011 No. 402-FZ (hereinafter referred to as the Accounting Law), clause 27 of the Regulations, approved by Order Ministry of Finance dated July 29, 1998 No. 34n).

For example, an inventory must be carried out regularly to identify food products, medicines and other goods with an expired shelf life (clause 4 of article 5 of the Law of the Russian Federation of 02/07/1992 No. 2300-1). If an inventory is not carried out in the cases established by law or is carried out untimely, for example after the dismissal of a financially responsible person, then the company:

- will not be able to bring the resigned employee to financial responsibility (Determination of the Judicial Collegium for Civil Cases of the Armed Forces of the Russian Federation dated May 7, 2018 No. 66-KG18-6);

- will not be able to take into account losses from shortages as part of tax expenses (Articles 252, 265 of the Tax Code of the Russian Federation, Resolution of the Ninth Arbitration Court of Appeal dated November 1, 2018 No. 09AP-51247/2018).

Who is appointed to the verification commission?

For maximum objectivity and to avoid collusion between inspectors, uninterested specialists from different fields of activity are usually invited. For example, if a warehouse is being inspected, then a warehouse worker who knows what is located and where is allowed to be present. In addition to him, two people working in other departments are involved. This could be: a workshop foreman, a commodity specialist or a finance specialist. Recently, third parties are often invited for examination, since for a reward they will not commit a crime and will conduct a high-quality inspection.

What to do if the inspection reveals excess

When discrepancies are discovered, the established inspection committee carefully studies the audit extracts, finds out the reasons for this, and draws up a report of violations. Next, the employees draw up a protocol, which states the results of the work done, the reasons, explanatory notes from the financially responsible persons and the conclusions of the specialists.

Next, the document is referred to the manager who studies the issue. And he decides with the chief accountant how best to carry out the postings. The reporting indicates the data that was recorded during the comparisons. The annual report must also reflect and document the surpluses identified in the cash register during the inventory.

If there are discrepancies, then funds should be accounted for at the market price valid for today. All invoices received from contractors are raised. If there are none, then you can find out prices in another way, for example, look at advertisements or request information from the statistics department.

For correct reporting, the accountant should capitalize the received data using postings.

Audit

The process is carried out in stages, compliance is strictly regulated:

- A commission of three people who are not interested in money circulation is formed.

- The director's order will contain items on the composition of the inspection committee, the reasons for the process, and the date of implementation of audit actions.

- Next is an inventory of all property.

- The last one is a comparison of established facts and information reflected in the balance sheet. The results are written down in a separate form, which refers to the manager to determine further orders.

Business Solutions

- the shops

clothes, shoes, products, toys, cosmetics, appliances Read more

- warehouses

material, in-production, sales and transport organizations Read more

- marking

tobacco, shoes, consumer goods, medicines Read more

- production

meat, procurement, machining, assembly and installation Read more

- rfid

radio frequency identification of inventory items More details

- egais

automation of accounting operations with alcoholic beverages Read more

What to do if found

This situation occurs when accounting is incorrect. Rarely, but thefts are detected. You need to properly understand all the documentation. To do this, the accounting department writes off the shortage or enters it into the “Expenses” section, and the excess is capitalized. It is very important to carry out the entire procedure on the day of control. In addition, the director’s order to initiate an inspection is the main document for resolving the issue.

A sample order for the posting of surplus during inventory is not provided by government agencies. Therefore, the form can be varied and approved in accordance with the internal charter of the enterprise.

How the director's instructions are carried out

How to correctly capitalize surplus fixed assets identified during inventory, liners: D 10, 41, 01, 50 K 91-1 9 (they are used for correct reporting).

- If misgrading occurs, then it is possible to offset the missing and excess goods.

- If there is a lack of finances, they are repaid by the efforts of people who are endowed with financial responsibility. You can act in other ways; the difference in amounts is sent to account 91-1 marked “Other expenses”. Keep in mind that this is done at the time of audit and market value is taken into account.

How to take inventory

Since 2013, it is not necessary to use unified forms of primary documents (clause 4 of Art. Law on Accounting).

In our opinion, it is safest to develop your own document forms for recording inventory results, taking as a basis the forms approved by Goskomstat. Your forms must be approved in the annex to the organization’s accounting policy or by order of the individual entrepreneur (clause 4 of Article of the Law on Accounting, clause PBU 1/2008).

If violations are made during the documentation of the inventory, the following consequences may occur:

- the impossibility of bringing the perpetrators to financial responsibility (letter of the Ministry of Finance dated December 30, 2019 No. 03-11-11/103406);

- refusal of inspectors to take into account the shortfall in tax expenses (letter of the Ministry of Finance dated December 24, 2014 No. 03-03-06/1/66948);

- accrual of VAT on the value of the shortage during a tax audit (Resolution of the AS Far Eastern Military District dated January 24, 2019 No. F03-5265/2018).

What to do with excess materials, raw materials and goods

Often, excess raw materials or products delivered to wholesale warehouses remain in production. The last day on which you can capitalize excess materials (cash or accrual method) in the annual report is no later than the 31st day of the last month.

In this case, the accounting department has to decide how to reflect the surplus during inventory and at what price to capitalize it. To do this, they include non-operating expenses in the cost of excess items, and also compare invoices or study offers on the market in a specific area.

Write-off as expenses

In the absence of culprits, the amounts of the shortfall that were recorded in the original account 94 “Shortages and losses from damage to valuables” are written off to the debit of subaccount 91 “Other income and expenses.”

The write-off procedure is given in Article 12 of the Federal Law “On Accounting”. Example: A fire occurred at the warehouse of Tekhnik JSC, as a result of which a batch of computer equipment was destroyed. They carried out an inventory, as a result of which the commission found that equipment worth 60,000 rubles had deteriorated. The fire inspection authorities concluded that the fire occurred as a result of a lightning strike, that is, there were no perpetrators. The company's accountant makes the following entries: Debit 94 Credit 41 in the amount of 60,000 rubles. – the cost of burnt equipment was written off based on the inventory results to the shortage account; Debit 91 (99) Credit 94 - the amount of the shortfall resulting from the fire is written off as company expenses.

Excess production materials

The law of the Russian Federation very clearly states that an enterprise can include no more than 24 percent of the price of goods or raw materials from the market price in costs. You will not hear specific demands from Federal Tax Service employees. The only thing that needs to be taken into account is the impossibility of including in the enterprise’s expenses the entire cost of excess materials identified by the commission. You will most likely have to sell them off. And to avoid problems with the tax authorities, take into account the previously established price on the sales market.

Step-by-step instruction

On July 01, the Organization carried out a scheduled inventory of inventory items. The commission identified surpluses:

- Roman blind “Bamboo” – 3 pcs. (market price 800 rub./piece);

- magnets for curtains “Rose” – 10 pcs. (market price 100 rubles/piece).

On the same day, the surplus was capitalized.

Let's look at step-by-step instructions for creating an example. PDF

| date | Debit | Credit | Accounting amount | Amount NU | the name of the operation | Documents (reports) in 1C | |

| Dt | CT | ||||||

| Capitalization of surplus goods as a result of inventory | |||||||

| July 01 | 41.01 | 91.01 | 3 400 | 3 400 | 3 400 | Capitalization of surplus goods at market value | Posting of goods |

Fixed Asset Usage Details

Control means not only a comparison of the information obtained in the process about the product, materials, raw materials base with the information recorded in the primary statutory documentation, but also the recalculation of fixed capital.

In this case, a completely different technique is used:

- Excesses are classified as unrealized income.

- Assets that are under repair are described in a statement in the INV/10 form, which indicates the price of repair work.

- For property leased or for temporary storage, a document is drawn up, in which all relevant papers from the counterparty will be attached, confirming the legality of the action.

- A special commission draws up a report on operating systems that cannot be restored and are unsuitable for use.

- If the book price of capital has changed in one direction or another, then this fact is also displayed.

- The funds must be equated to the income that could not be realized, and appropriate depreciation must be charged on it within the limits of the value declared by the market and actual depreciation.

Large surplus

The inventory process sometimes reveals not only excess materials, but also “additional” fixed assets. Here one of the professional jokes immediately comes to mind.

A boiler house was built using unaccounted funds. Then they realized: you need to put it on balance, you can’t hide it during verification. The resourceful chief accountant decided to take advantage of the ongoing inventory and included the following clause in the act: “During the inventory, a boiler room was discovered on the territory of the enterprise.”

In practice, unaccounted-for boiler houses are rare, but surpluses on smaller fixed assets may well be detected during inspection, especially in large enterprises with a complex structure and accounting system.

In the general case, a discovered object of fixed assets is valued in the same way as an object of material reserves, i.e. at market value (clause 36 of the Guidelines for accounting of fixed assets, approved by order of the Ministry of Finance of the Russian Federation dated October 13, 2003 No. 91n).

A situation may arise when an asset is on the balance sheet, but the accounting does not reflect the modernization carried out (completion, etc.). In this case, it is necessary to estimate the costs of the work and increase the cost of the asset by them. To estimate costs, you can use information about the cost of similar work available to the company, or use the services of an appraiser.

For all options for assessing fixed assets, use available information on prices for similar property. The actual condition and degree of wear and tear of specific items identified as surplus should be taken into account.

Conclusion

We tried to tell you and show you with specific examples what inventory surplus is, how capitalization occurs and how income tax and VAT are calculated. We recommend that you use software, for example, from . The program will help you organize your workplace correctly and prevent fatal failures in reporting. Qualified specialists will provide free consultations on installation and configuration.

Here is a visual demonstration of property inventory in organizations using Mobile SMARTS and a set of equipment.

If your enterprise uses “1C: Accounting” in any delivery, “1C: UPP” or 1C for a construction organization, and you plan to carry out inventory only on barcodes (you will not use RFID), then a special driver for inventory is completely suitable for you from Cleverens, the delivery package of which includes all the programs and processing necessary for both printing labels and working with the data collection terminal.

If you are planning to implement RFID, then another program is suitable for you - Cleverence: Property Accounting. Number of impressions: 6039

Surpluses and shortages during inventory: accounting and documents

In order to truly represent the financial state of affairs of an organization, regardless of the form of ownership, it is necessary to have reliable data about all the property at the disposal of this organization: how much of it is, what condition it is in, whether it was valued correctly.

Then the actual balances of the property are compared with the accounting data. This process of checking assets and liabilities is called an inventory.

Inventory of property and its sources is an accounting operation that every accountant encounters in his work. This article will help you learn the basic rules of inventory, the timing and procedure for conducting them, the procedure for recording the results, as well as how surpluses and shortages are taken into account during inventory.

The content of the article:

1. Inventory and its regulatory regulation

2. When is the inventory taken?

3. Types of inventories

4. The procedure for carrying out inventory in accounting

5. Preparation of primary accounting documentation for recording inventory results

6. Registration of results: documents after inventory

7. How are inventory results reflected in accounting?

8. Carrying out an inventory in the 1C: Accounting program

9. Accounting for shortages during inventory

10. VAT on shortages during inventory

11. How to capitalize surplus during inventory

12. Inventory of property using an example

13. Accounting entries during inventory - continue the example

So, let's go in order. If you don't have time to read a long article, watch the short video below, from which you will learn all the most important things about the topic of the article.

(if the video is not clear, there is a gear at the bottom of the video, click it and select 720p Quality)

We will discuss the topic further in the article in more detail than in the video.

Inventory and its regulatory regulation

Inventory is a certain sequence of practical actions to document the presence, condition and assessment of the property and obligations of an organization in order to ensure the reliability of accounting and reporting data.

Inventory is legally regulated by the following documents:

- “On Accounting” - Federal Law No. 402-FZ of December 6, 2011. (with changes and additions);

- “Regulations on accounting and financial reporting in the Russian Federation” - Order of the Ministry of Finance No. 34n dated July 29, 1998;

- PBU 1/2008 - “Accounting policies of the organization”;

- “Guidelines for inventory of property and financial obligations” - Order of the Ministry of Finance No. 493 of June 13, 1995;

- “On the procedure for approving norms of natural loss during the storage and transportation of inventory items” - Decree of the Government of the Russian Federation No. 814 of November 12, 2002;

- “Methodological recommendations for the development of norms for natural loss” - Order of the Ministry of Finance No. 955 of March 31, 2003.

The main reasons for discrepancies between actual availability and accounting data are:

- — inaccuracies in the acceptance or disposal of property;

- — errors in primary documents, incorrect reflection of documentary data in analytical and synthetic accounting;

- — direct abuses of financially responsible persons.

When is inventory taken?

Inventory can be mandatory or voluntary. All organizations and individual entrepreneurs maintaining accounting records are required to conduct an inventory in the following cases:

- Before preparing annual financial statements;

- In case of change of the financially responsible person;

- When buying, selling, leasing property;

- In case of liquidation or reorganization of the organization;

- If facts of damage or theft of property are revealed;

- In case of various emergency situations.

Before drawing up annual financial statements, organizations are required to conduct a full inventory of property and liabilities. Such an annual inventory must be carried out by the organization no earlier than October 1 of the reporting year.

For some types of property, other inventory deadlines are established. According to paragraph 27 of the Accounting Regulations, approved by Order of the Ministry of Finance of Russia dated July 29, 1998 No. 34n “On approval of the Regulations on accounting and financial reporting in the Russian Federation,” inventory can be carried out for:

- fixed assets - once every three years;

- library collections - once every five years.

Types of inventories

A voluntary inventory can be carried out in a situation provided for by the organization’s accounting policy or by order of the manager; these documents determine the cases, number and timing of inventories in the reporting year.

The appendix to the accounting policy for conducting inventories includes:

- — schedule of scheduled and unscheduled inventories (including mandatory) in the reporting year,

- — dates of scheduled inventories,

- - a list of property and liabilities checked during each inventory.

Types of inventories can be presented in table form:

| Criterion | Inventory type | Distinctive features of inventory |

| According to the obligatory | Mandatory | Carried out mandatory in accordance with the legislation of the Russian Federation |

| Initiative | Carried out by decision of the manager | |

| By frequency | Planned | Carried out within the time limits established by the inventory procedure |

| Unscheduled | Carried out by decision of the head of the organization outside the approved plan to ensure additional control over the safety of certain types of property, or the need for it is provided for by law | |

| By coverage | Full | All property and liabilities are subject to inventory |

| Partial | One or more types of property and liabilities are subject to verification | |

| By method | Natural | Consists of direct observation of objects and determining their quantity by counting, weighing, measuring, etc. |

| Documentary | Consists of checking documentary evidence of the presence of objects |

The procedure for carrying out inventory in accounting

All primary documents related to the inventory of property are officially approved by Resolution of the State Statistics Committee of Russia dated August 18, 1998 No. 88. You can use them by approving them in the accounting policy. The organization has the right to record surpluses and shortages during inventory in its document forms if they contain all the details required by Federal Law No. 402-FZ of December 6, 2011, and they are approved as part of the accounting policy.

The procedure for carrying out inventory in accounting is divided into the following stages:

- Preparatory stage;

- Creation of an inventory commission;

- Carrying out inventory;

- Registration of inventory results.

Let's look at these stages in more detail.

First, you need to draw up an administrative document on the inventory . This may be an order, resolution or instruction signed by the head of the organization (Form INV-22). This administrative document must list the composition of the inventory commission, the timing of the inventory, a list of property and liabilities subject to recalculation and reconciliation.

The order must be registered in the order register (INV-23) and handed over to the chairman of the commission. Next, you need to take receipts from financially responsible persons stating that all material assets have been taken into account and the documents have been submitted to the accounting department.

An inventory commission is created on the basis of the administrative document on the inventory . Such a commission must include at least two people, one of whom is the chairman of the commission.

The inventory commission includes:

- representatives of the organization's administration;

- accounting employees;

- other specialists (engineers, economists, technicians, etc.).

The absence of at least one member of the commission during the inventory serves as grounds for declaring the inventory results invalid.

The commission may include not only employees of this organization, but also invited independent experts, for example, from a third-party audit company. In the case where only the manager is listed in the organization, then all responsibilities for conducting an inventory and recording its results are assigned to him.

When there is a large volume of work, working inventory commissions are specially created to simultaneously carry out an inventory of property.

Preparation of primary accounting documentation for recording inventory results

Within the time limits specified in the administrative document, the inventory commission carries out an inventory of property and their sources. It is important to remember that during the inventory, no other operations on the movement of the inspected OS or inventory items should be carried out!

The results of the recalculation process are recorded in a special inventory list or act in duplicate, which are signed by all members of the commission and submitted to the accounting department.

The inventory results are entered into special inventory records or acts in a unified form. Fixed assets are entered in the INV-1 form, inventory items - INV-3, etc. Let me remind you that all forms of primary accounting documentation for accounting for inventory results that you use, regardless of whether they are standard or not, are approved as part of the accounting policy.

INV-3:

If during the inventory, discrepancies were identified between accounting data and the actual balances of property and liabilities, then they are entered into the matching statements in the form INV-18 and INV-19. Comparison statements are compiled only for property, during the inventory of which deviations from the accounting data were identified. It reflects the discrepancies between the indicators according to accounting data and inventory records.

INV-19:

Registration of results: documents after inventory

The final results of the inventory are summarized in the statement of results identified by the inventory in the INV-26 form. Discrepancies identified during the inventory between the actual availability of property and accounting data are reflected in the accounting accounts.

All documents after the inventory are signed by members of the inventory commission, the chairman of the commission and the accountant who accepted the primary documents from the chairman.

How are inventory results reflected in accounting?

So, all the primary documents have been drawn up and submitted to the accounting department, the accountant is faced with the task of performing the necessary operations to reliably reflect in the accounting surpluses and shortages during the inventory. How are the inventory results reflected in accounting? What transactions are processed?

First of all, the accountant must know whether the person responsible for the shortages has been identified: the method of accounting for the shortages depends on this. Shortages within the limits of natural loss norms can be attributed to production and distribution costs, and everything that exceeds the norms is attributed to the guilty parties.

If the guilty parties are never identified, or the court refuses to recover damages from them, the shortfalls are included in the financial results. Where exactly the accounting department will allocate the shortages is decided by the head of the organization in an order issued based on the results of the inventory.

The surplus is immediately included in the financial results, and capitalization is carried out at market prices as of the current date. For the purpose of calculating income tax, surpluses and shortages identified during inventory are considered non-operating income and expenses.

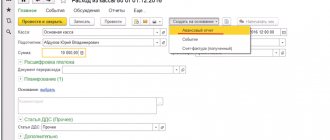

Carrying out an inventory in the 1C: Accounting program

How to register an inventory in the 1C program: Accounting 8th ed. 3.0, watch the video.

Accounting for shortages during inventory

Most often, it is shortages that are identified during inventory. Accounting for shortages during inventory is kept on account 94 “Shortages and losses from damage to valuables.”

Debit 94 – Credit 01, 10, 43, 41 - the shortage is reflected based on the inventory results

Afterwards, the circumstances of the case are clarified, whether there are guilty persons, and whether they agree with compensation for the deficiency. If necessary, the case is considered in court.

When the guilty person reimburses the cost of the missing inventory items, account 94 is closed through account 73 “Settlements with personnel for other operations”:

Debit 73 – Credit 94 – the shortfall is attributed to the guilty party

If the culprit is not identified, the accountant attributes the shortfall to account 91 “Other income and expenses”:

Debit 91-2 – Credit 94 – the shortfall is charged to other expenses

VAT on shortages during inventory

VAT previously accepted for deduction is subject to restoration in the cases listed in paragraph 3 of Art. 170 Tax Code of the Russian Federation. But writing off the shortage based on the results of the inventory is not included in the list of transactions from the above-mentioned article of the Tax Code. The shortage may be detected due to theft, fire, expiration date, etc.

Therefore, according to the Supreme Arbitration Court of the Russian Federation, there is no need to restore VAT on shortages during inventory.

But the Ministry of Finance often holds the opposite opinion, for example, Letter No. 03-03-06/1/1997 dated 01/21/2016 states that inventory and materials, when written off due to shortages, are not subject to further use, which means VAT on them must be restored.

However, the Ministry of Finance does not always recommend adhering to this rule. In Letter GD-4-3/ [email protected] dated May 21, 2015. It has been clarified that when property is disposed of due to a fire, VAT does not need to be reinstated. In addition, there is no need to restore VAT if low-quality inventory items are destroyed to ensure safety and sale of quality products (Letter of the Ministry of Finance No. 03-07-11/34617 dated 08/23/2013)

Thus, if the disposal of property occurs due to theft, damage, shortage, loss, etc. or they cannot be used in the future due to defects or expiration, then there will be no need to restore VAT (Decision of the Supreme Arbitration Court of the Russian Federation No. 3943/11 of May 19, 2011 and No. GD-4-3/21097 of November 26, 2013 and Letter of the Ministry of Finance No. 03 -01-13/01/47571 from 07.11.2013).

At the same time, exclude the possibility of a claim from the tax authorities due to the clarifications in Letter No. 03-03-06/1/1997 dated 01/21/2016. not worth it. In any case, YOU take the side of taxpayers, so it is possible to defend your right in court.

How to capitalize surplus during inventory

Surplus may at first glance seem like a good result of inventory. However, this is not at all true. After all, they could have formed in the event of incorrect capitalization of inventory items, or incomplete shipment of goods to customers, or write-off of inventory items for production. That is, surpluses, as well as shortages, indicate poor quality work by financially responsible persons and the accountant.

How to capitalize surpluses identified during inventory? We have already noted earlier that they are non-operating income and are recorded on account 91 in correspondence with the accounts of this or that property. To register the operation of capitalizing surpluses, the following transactions are used:

Debit 10, 01, 50, etc. — Credit 91-1

If, as a result of the inventory, surpluses of fixed assets subject to depreciation were identified, then depreciation should be calculated as for purchase: from the first day of the month following the month of discovery.

Since the cost of the surplus is included in non-operating income in account 91-1, it is income subject to income tax.

How to capitalize goods identified during inventory in the 1C program: Accounting 8 ed. 3.0, watch the video.

Surpluses and shortages during inventory taking as an example

Let's consider all of the above about property inventory using an example.

Fialka LLC, engaged in wholesale trade and applying a general taxation system, carried out an inventory of goods and materials in a warehouse when changing the financially responsible person. As a result, surpluses and shortages were identified.

Surplus:

Product 1 – 10 pcs. 200 rub. (market value at the inventory date)

Disadvantages:

Product 2 – 5 pcs. 300 rub.

Product 3 – 8 pcs. 50 rub.

Goods received from Gladiolus LLC are taxed at a rate of 18%.

Before the start of the inventory, an order was issued by the head of Fialka LLC, which indicated the reason for the inventory, the date of start, end and registration of the inventory results, and the composition of the inventory commission. The order was brought to the attention of all members of the inventory commission and the chief accountant against signature.

As a result of the inventory, an inventory was filled out according to the INV-3 form, which was stitched, numbered, signed by members of the inventory commission and sealed by the organization. When comparing the inventories with the statements provided by the accounting department, surpluses and shortages were identified during the inventory, as a result of which the chairman of the inventory commission compiled a comparison sheet INV-19 indicating the discrepancies between the accounting data and the actual availability of inventory items in quantitative and monetary terms.

Having summed up the results of the inventory, the inventory and matching sheets were submitted to the accounting department and the chief accountant, together with the chairman of the inventory commission, signed the inventory results.

During the inspection of the primary documents, the chief accountant determined that the shortage arose as a result of incorrect capitalization of inventory items in the accounting records by the accountant responsible for this section of accounting. Based on a memo from the chief accountant to the manager, an order was issued to repay the cost of the shortage at the expense of the wages of the inventory accountant.

Accounting entries during inventory - continue the example

Debit 94 - Credit 41 - in the amount of 1500 rubles. – Product 2 is written off.

Debit 94 - Credit 41 - in the amount of 400 rubles. – Product 3 is written off.

Debit 73 - Credit 94 - in the amount of 1900 rubles. – The amount for the shortage of goods and materials is attributed to the guilty party.

Debit 70 - Credit 73 - in the amount of 1900 rubles. – The amount of the shortfall in wages was withdrawn from the guilty person.

In order to avoid disagreements with the Federal Tax Service, the accountant decided to restore VAT for the shortage:

Debit 19 - Credit 60 - in the amount of 342 rubles. — VAT was restored for the shortage identified as a result of the inventory.

As a result of the above accounting entry, a line will appear in the sales book indicating the invoice for the receipt of these inventory items from the supplier and the amount of VAT calculated based on the total cost of written-off inventory items:

1900 rub. *18% = 342 rub.

Surplus inventory items were capitalized with the following accounting entry:

Debit 41 - Credit 91-1 - in the amount of 2000 rubles. – The surplus of Product 1 has been capitalized.

So, as a result of the inventory, income was received in the amount of 2000.00 rubles. The overall result of the inventory: profit is 2000 rubles, the loss is compensated by the guilty person at the expense of his wages.

Thus, inventory is a part of business life that every accountant will be forced to face in practice sooner or later. Always remember that all surpluses and shortages during inventory must be documented and confirmed by the signatures of responsible persons and the seal of the organization.

If you have an unclear situation when accounting for surpluses or shortages identified during inventory, we invite you to comment in order to jointly resolve your difficulties.

Surpluses and shortages during inventory: accounting and documents