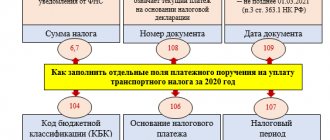

Tax legislation obliges persons who own vehicles to annually accrue and pay tax. The frequency of this procedure increases if the region has provided for mandatory advance payments of transport tax based on the results of each quarter.

Each time, when calculating a tax liability in relation to a vehicle, an organization is faced with the need to reflect the results obtained in accounting using double entries on accounting registers. Postings are made upon the fact of the calculation (tax accrual), as well as upon the transfer of the accrued tax amount to the local budget (tax payment).

Since the responsibility for maintaining accounting falls only on organizations, the question of correctly reflecting the accrual and payment of transport tax in accounting arises only before legal entities. Individuals with the formation of an individual entrepreneur must pay tax on their vehicles, but they do not need to reflect this information using accounting entries.

How is transport tax calculated?

The obligation to independently calculate tax is assigned only to legal entities.

For individual entrepreneurs and individuals, this calculation is made by the Federal Tax Service (Clause 1 of Article 362 of the Tax Code of the Russian Federation). The calculation of transport tax involves the application of a rate to the tax base, taking into account the time the transport is in the payer’s ownership. In some cases, an increasing coefficient is also applied (clause 2 of Article 362 of the Tax Code of the Russian Federation).

Please note that the tax must be paid not by the one who uses the vehicle, but by the one who owns it. Even if the owner has issued a power of attorney to drive the vehicle, the authorized person does not pay tax.

Tax is calculated for the full month during which the vehicle is owned by the payer. Until 2021, the month of registration and deregistration was considered a full month for which the tax was calculated. Starting in 2021, a registration month is considered complete if the vehicle is registered before the 15th day inclusive. The month of deregistration is considered complete if the object is deregistered after the 15th day.

See the material “If the owner of a vehicle changes in the middle of the month, only one of the owners pays the tax for that month.”

For example, if a car was purchased and registered on April 15, 2018, then the transport tax for 2021 was calculated for the buyer for the period of ownership of the car starting from April 2018, and for the seller - until March 2021 inclusive.

To learn how to determine the transport tax base, read the article “How is the transport tax base determined?”

Regional benefits

As noted earlier, each region has its own list of benefits for paying transport tax. In order to find out which toll benefits are relevant for a particular region, you need to contact the local tax office directly, where they are required to provide a full list of benefits.

If it turns out that a person falls under one or several categories at once, then it is necessary to submit a personal application for benefits. In this application, you must provide a link to the section of regional legislation on the basis of which the citizen is entitled to a benefit. In addition, you need to indicate what kind of vehicle the person owns. In this case, the brand with the registration number of the vehicle and so on must be reported. You will also need to attach all copies of documents that confirm the fact that the person is the legal owner of the vehicle. You will also need copies of a document that confirms the identity of the owner and his rights.

All citizens who have the right to benefits, if there are several objects of taxation, are, as a rule, exempt from paying tax on one of the vehicles at their personal discretion.

Calculation of transport tax: postings

According to PBU 10/99 (approved by order of the Ministry of Finance of Russia dated May 6, 1999 No. 33n), transport tax is considered an expense for a normal type of activity. How exactly it will be shown in accounting depends on where the transport is used.

In general, transport tax is reflected in accounting by the following entries:

- Dt 20, 23, 25, 26, 44 Kt 68 - tax or advance payment has been accrued;

- Dt 68 Kt 51 - tax payment has been made.

If a unit of transport is used in an activity unrelated to the main one, the tax accrual on it is reflected in other expenses (clause 11 of PBU 10/99). In this case, in accounting it will look like this: Dt 91.2 Kt 68.

Do not forget to properly prepare the primary documents before making accounting entries. An accountant's certificate is a document that reflects the tax or the accrued advance payment for it.

The payer must indicate exactly how this tax will be reflected in the accounting policies in the accounting policy.

For the latest changes in the document regulating the main issues of formation of accounting policies, read the material “PBU 1/2008 “Accounting Policies of the Organization” (nuances).”

Results

Independent calculation of transport tax is a thing of the past for legal entities. But they will continue to keep records of tax accrual and payment, reflecting it in accounting entries. In accounting, tax usually forms expenses for activities performed. In tax accounting, it is included in costs that reduce the base for income tax or simplified tax system with the object “income minus expenses.” When combining taxation regimes, the tax may be distributed.

Sources:

- Tax Code of the Russian Federation

- Order of the Ministry of Finance of Russia dated May 6, 1999 No. 33n

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Tax accounting of transport tax

To calculate income tax, transport tax is taken into account in other expenses that are associated with production and sales (clause 1 of Article 264 of the Tax Code of the Russian Federation).

When calculating the simplified tax system with the object “income”, the amount of transport tax is not taken into account, since expenses do not matter for its calculation (clause 1 of article 346.18 of the Tax Code of the Russian Federation). When simplified with the object “income minus expenses,” transport tax is included in expenses (Article 346.16 of the Tax Code of the Russian Federation). Unpaid transport tax cannot be taken into account when calculating the simplified tax system.

Read more about the tax under the simplified tax system in the article “Transport tax under the simplified tax system: calculation procedure, terms, etc.”

As for UTII, the amount of imputed tax does not depend on the amount of transport tax, since its calculation is done without taking into account income received and expenses incurred.

If the payer uses OSNO and UTII together and transport is used in both taxation regimes, the tax amount must be divided. When using transport in only one of the modes, such separation is not necessary. If transport was used in activities related to OSNO, it can be taken into account to reduce income tax, if with UTII, the imputed tax cannot be reduced.

To correctly distribute the transport tax between the two regimes, you need to calculate what part is the income for each type of activity. To calculate the portion of income under OSNO, you must do the following: divide the amount of income under OSNO by income from all types of activities. The transport tax related to OSNO is determined by multiplying the amount of transport tax and the share of income received from OSNO. Transport tax related to activities on UTII is calculated in the same manner, using in this calculation the amount of income received on UTII. The sum of the results obtained from both calculations should give the total amount of accrued tax.

About the division of expenses when simultaneously applying the simplified tax system and UTII, read the material “The procedure for separate accounting for the simplified tax system and UTII.”

Federal benefits

Federal benefits include those specified in section No. 358 of the Tax Code. Thus, the legislation reflects categories of transport, and not only automobiles, that cannot be taxed. So, these include the following vehicles:

- Boats with oars.

- Specially equipped cars that are intended for disabled people. In this case, the engine power of such a device should not exceed one hundred horsepower.

- Sea, and, in addition, river vessels that carry out fishing.

- Cargo and, in addition, passenger ships, which are designed to transport citizens by sea or river. The listed vehicles must belong to a specialized institution that carries out such transportation.

- All kinds of specialized agricultural equipment, from tractors, self-propelled combines, to livestock and milk tankers, as well as machines for transporting fertilizers and poultry. Moreover, all types of transport provided must be registered in the name of the organization that carries out agricultural activities. If this vehicle is used for other purposes, then the tax will have to be paid.

- Transport that is owned by executive authorities and is used for operational work involving military, as well as activities equivalent to such.

- Stolen or wanted cars. But at the same time, it is necessary to have a document available that will confirm the fact of the loss. The corresponding paper is issued by authorized bodies.

- Helicopters, as well as airplanes that belong to medical institutions and sanitary services.

- Various vessels according to the registry.

Transport tax accounting

Account 68 “Calculations for taxes and fees”, provided for in the Chart of Accounts, is used, among other things, for reflecting and accounting for transport tax. You should create a subaccount to account 68 specifically for postings for calculating transport tax.

For each vehicle, the amount of transport tax payable to the budget at the end of the tax period, in accordance with clause 2 of Art. 362 of the Tax Code of the Russian Federation is calculated separately.

Therefore, it is advisable in accounting to reflect the accrued amounts in the accounts of the corresponding costs - either for production or as part of other expenses. The choice of a specific corresponding account will depend on where exactly the transport is used: in auxiliary or main production, in which particular division.

If transport is used in the main production, then the transport tax is classified as ordinary expenses and its accrual is reflected in correspondence with accounts for accounting for ordinary expenses 20 (23, 25, 26, 44 ...).

Let's look at the accounting entries for transport tax:

| Debit | Credit |

>Transport tax accounting

This video is unavailable

Friends! Please support my project! Tell your friends and acquaintances about my YouTube channel https://www.youtube.com/channel/UCxqU. Ask them to subscribe to my channel and support me ❤ Share my videos on your social networks