a list of bonuses relevant for a particular company;- a note on the frequency of issuance of specific bonuses, as well as the grounds for their provision;

- compiling a list of employees who will directly relate to the bonus procedure;

- fixation of indicators based on which the specific amount of the premium is calculated;

- formulas by which the accountant will have to calculate the amount of bonuses;

- a list of grounds on which a subject may lose the right to receive any type of bonus;

- a description of the procedure within which an entity can make a claim against an employer on the basis of an understatement of the amount of the premium.

It is important to note that the legislation does not provide strict regulation regarding the procedure for calculating and issuing bonuses. However, there are a number of statutory recommendations that employers can rely on when developing local regulations. In particular, in Letter of the Ministry of Labor of the Russian Federation No. 14/1/B/911 dated September 21, 2016. The following basic recommendations are reflected in the context of the personnel bonus procedure :

- It is appropriate to formulate incentives for subjects taking into account their production in 15 or more days;

- issuing bonus amounts is appropriate when a specific employee achieves certain results in his professional activities, which can be highly valued;

- fixation in the local regulation “On Bonuses” of a longer period for the payment of regular bonuses than reflected in Art. 136 of the Labor Code of the Russian Federation, is not a violation of the law, and remains in the department of the employer.

The presence of accepted monthly bonuses at the enterprise does not exclude the possibility of additional bonuses for employees, for example, for each quarter or year. The frequency and amount of additional funds issued depends on the order of the manager.

How are salaries calculated?

Wages are a quantitative expression of work performed. That is, during a specific period of time, an employee performs some work. For this he receives payment, that is, a salary.

Its size is specified in the employment contract. But the law sets a minimum threshold below which the employer cannot lower the monetary reward. In this case, the employee must work a full month at full production.

The employment contract specifies the value indicated in the staffing table. It is drawn up by the responsible employee and approved by management. The procedure for awarding bonuses to employees is prescribed in the relevant Regulations for the enterprise.

All time worked must be accounted for accordingly. For this purpose, there is a time sheet in which management notes presence/absence at the workplace, full/part-time. At the end of each month, the timesheet is submitted to the appropriate department for payroll calculation.

The main document for calculating wages is the payslip, for payment – the payslip. These documents record not only the accrual procedure, but also deductions and bonuses.

How is the bonus included in the calculation of average earnings?

The rules for calculating average earnings contain Art. 139 of the Labor Code of the Russian Federation and the Regulations on the specifics of the procedure for calculating the average salary, approved by Decree of the Government of the Russian Federation of December 24, 2007 No. 922.

They oblige all payments that form the employer’s remuneration system, including bonuses, to be taken into account in this calculation. However, due to the fact that bonuses, unlike salaries, can be accrued at intervals exceeding a month, taking them into account has a number of features, depending on:

- from the completeness of the calculation period;

- the duration of the period for which bonuses are accrued;

- correspondence between the periods for calculating average earnings and calculating bonuses;

- the fact of accounting (non-accounting) of actual work time during the bonus period;

- the existence of a prohibition on taking into account more than one payment accrued in the same period for the same indicator at the same frequency.

For more information about the rules for taking bonuses into account when calculating average earnings, read the material “Are bonuses taken into account when calculating vacation pay?” .

What are the salary supplements?

An allowance is a separate type of payment intended to additionally stimulate employees to work. For example, there is a bonus for continuous work experience at a given enterprise. Sometimes it is necessary to give a person a salary increase, and he will go to study courses and improve his qualifications.

The bonus is voluntary. Its accrual and payment is the employer’s right, not an obligation. Depending on the activity of the enterprise, allowances may be as follows:

- "for mentoring." Paid to those who have worked for many years at one enterprise and have now taken upon themselves (in addition to the main functions) the training of young employees;

- "for qualification." Paid only to those specialists who have a high level of qualifications, which is confirmed by relevant documents and training;

- of a personal nature. For example, a certain valuable employee decided to quit. To retain him, management decides to pay him bonuses;

- “for having an academic degree or title.” If an employee is a candidate of sciences, then this is a reason to give him an additional salary;

- “for access to state secrets.” Relies on those employees who are related to government or diplomatic structures and work with information related to state secrets;

- "for knowledge of foreign languages." If an enterprise exports products abroad, then having an employee with knowledge of the language on staff is a necessity.

Important! Supplements may be temporary. They can be appointed by order of the manager at any time. But before these allowances are cancelled, the employee must be warned.

Types of awards and their differences

Systematic bonuses assume a regular nature, with constant payment throughout the year.

The reason for such encouragement may be the successful solution of problems within one’s competence (reducing the cost of electricity, fuel).

Sometimes continuity of work and seniority within a particular organization is important. An employer interested in retaining personnel may assign separate payments fixed in standards and regulations approved in addition to the employment contract.

You can receive a bonus payment for the work done. The assessment period can be a month, a year, a quarter. An annual reward often practiced by successful companies is called the “thirteenth” salary.

In order to consistently receive a merit bonus, it is necessary to fulfill the plans and requirements of the employer from month to month, from quarter to quarter. In case of unsatisfactory work, mistakes, or improper attitude to work, the employer has the right to refuse payment.

For the work done

The most common type of bonus is the accrual of funds for the completion of some important production task. Recipients can only be a specific list of persons who have received the employer’s assignment.

The reasons for bonuses are:

- unscheduled work;

- saving resources, reducing enterprise costs;

- reduction of deadlines;

- accident prevention;

- other important achievements for the entire enterprise.

Bonuses can be determined as a fixed value or as a percentage of average earnings.

Collective or individual

Despite the individual consideration of each payment case, bonuses can be given not just to one person, but to an entire team. For example, for the outstanding achievements of the group, the success of the department, the completion of the workload by the team.

One-time incentives

Among one-time payments to employees, remuneration of employees in connection with the celebration of any memorable day, holiday, or anniversary is allowed.

In fact, the payment is not related to work exploits and achievements, but it is still an incentive option, retaining valuable employees and creating additional employment value.

The date or event selected for assigning the bonus can be chosen at the discretion of management.

How a fine is issued using a bonus system

Although the law does not provide for the possibility of fining employees, the organization can formalize the punishment as a refusal or reduction in bonuses. For example, companies where punctuality is important are ready to fine up to 25% of labor income, and for a serious offense, including absenteeism, the reduction reaches 50%.

What is salary

Some workers do not see the difference between salary and wages. But it's not always the same!

When an employee first gets hired, he signs an employment contract. It indicates exactly the salary. That is, a certain fixed fee, from which the calculation will be made if the employee decides to go on vacation or go on sick leave. It is from this amount, without any allowances or additional payments, that benefits will be calculated.

What is the minimum salary

In Russia there is such a thing as the minimum wage - the minimum wage. That is, if an employee worked a full month, did not get sick, did not go on vacation, did not take it at his own expense, etc., he cannot be paid less than the amount established by the state at the legislative level.

Not so long ago, the minimum wage was equal to the subsistence level. This became necessary due to the constant rise in inflation. In addition, a person cannot earn less than he needs to feed himself and pay for utilities.

The minimum wage is set once a year. In 2021, its value is 11,280 rubles. That is, with full employment, a person cannot theoretically earn less than this amount.

There is also the concept of “minimum wage”. This is the smallest amount of money that an employee in a particular region of residence can receive for his work. This indicator is used to calculate mandatory insurance contributions to the PRF, Social Insurance Fund and medical insurance.

The minimum wage cannot be lower than the minimum wage. If, according to the data, such an incident occurred in a certain region, then the salary indicator will be equal to the minimum wage.

In addition to the minimum wage, the employer can make allowances and additional payments, award bonuses and other payments.

Bonuses based on payout source

On this basis, bonuses are divided not those amounts of expenses for which:

- are included in the cost of products (works, services) produced and sold by the company;

- are attributable to the company's profits.

Here it is correct to briefly dwell on the economics of the enterprise. Finished products are produced and sold. The proceeds from its sale are income. The costs incurred for its production, including the payment of workers, are the cost of production.

If we subtract the cost from the income from the sale of products, we will make a profit. After paying taxes, we will receive net profit.

Therefore, the first type includes bonuses related to the employee’s work, regardless of whether they are included in the wage fund or not. This type of bonus is partly beneficial to the company, since it thus kills two birds with one stone: the team is happy and taxable profit is legally reduced.

The second type includes incentives not related to the performance of job duties , listed in paragraph B of the previous section of this article.

What is a premium

In Art. 129 of the Labor Code of the Russian Federation states that bonuses are included in wages. A bonus is an additional monetary reward, a payment for any differences one employee has over another. The nature of the bonus is such that it relates to incentive payments.

Its payment is also not the responsibility of the employer, it is his right. The procedure for paying bonuses to employees is regulated by local regulations of the enterprise. As a rule, the employer additionally develops and approves the Regulations on bonus payments to employees.

Important! If there is a local regulation that states that it is necessary to reward employees for exceeding the volume of completed products, then the employer is obliged to do this. If there is no such record, then payment is at the discretion of management.

If management does not fulfill its obligations regarding mandatory bonus payments to employees, the latter can file a complaint against them with regulatory authorities, in particular, with the labor inspectorate. It is possible to demand the collection of unpaid amounts, as well as compensation for each day of delay, only in court.

What is the award for?

The management of the enterprise is not prohibited from making additional cash payments not only for production achievements, but also on certain dates, for example, an anniversary, retirement, or the New Year. But, if we consider the issue from a taxation point of view, it is easier not to pay a premium, but to provide financial assistance. It is not subject to income tax.

In addition, management may simply decide to give bonuses to some or all employees for no reason. This is not prohibited by law!

Prize according to the Labor Code of the Russian Federation

Payment of a bonus according to the labor code is a measure of rewarding an employee for a job well done, qualifications or overtime. This type of payment is not mandatory, and its size is determined by the capabilities of the manager. Employee bonuses are introduced to encourage work and conscientious performance.

The legislation does not have specific rules for this type of payment. The bonus, in accordance with the Labor Code of the Russian Federation No. 191 Federal Law, refers to one of the types of incentives for conscientious work. An employee can also receive a valuable gift, a day off, a certificate, or a title. The type and amount of gratitude is determined by the company. The types of bonuses are prescribed in collective and labor agreements, local acts, and orders of the organization.

Common mistakes in terms of remuneration in employment contracts

Some employers make the following mistakes when paying their employees. This could have dire consequences. Such errors include the absence in the employment contract of a specific figure that indicates the employee’s salary. Management often does this:

- makes a reference in the employment contract to a local regulatory act that specifies the amount of his salary or tariff rate. The most common option is a reference to the staffing table;

- makes no mention at all about the financial side of the issue.

Such actions are a violation of labor laws. The Labor Inspectorate, conducting scheduled and unscheduled inspections, will immediately identify these violations. For this, the employer will be held accountable in the form of a fine. If he continues to commit the same offenses, the fine will be several times greater.

Remuneration is an essential condition of the employment contract. Its change, especially downward, is possible only with the written consent of the employee himself.

Results

The bonuses that are present in the description of the wage system approved by the employer form part of the employee’s salary and, as part of this salary, must be indicated in the employment agreement with the employee.

This can be done either by referring from the text of the employment contract to the internal regulatory act on bonuses, or by recording the terms of bonuses directly in the provisions of the employment agreement. The bonus, which is part of the payment for labor, is taken into account when calculating average earnings. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Are the employer’s actions to deprive employees of bonuses legal?

In accordance with the Labor Code of the Russian Federation:

- A bonus is an incentive payment, i.e. payment different from the concept of wages;

- the bonus system is established by the collective agreement and (or) other LNA;

- as an INCENTIVE, the employer has the RIGHT (i.e., he decides himself, if this does not contradict the LNA) to give a bonus to one or another employee or not.

Note:

it must be borne in mind that depriving an employee of a bonus will be illegal as a disciplinary measure.

Those. if the employer issued an order to deprive the employee of a bonus as a disciplinary sanction, then such an order may be canceled as illegal. But if the employee does not perform or improperly performs his job duties, the employer has the right not to give the employee a bonus at the end of the month, that is, make a decision without indicating a specific violation.

Conclusion:

The employer has the right to decide not to pay the bonus at its discretion. This decision must be properly formalized.

The article was written and posted on June 27, 2021. Added - 08/07/2018, 12/09/2018

ATTENTION!

Copying the article without providing a direct link is prohibited. Changes to the article are possible only with the permission of the author.

Bonuses to employees in accordance with labor and tax laws

From the article you will learn:

1. How to document the accrual of bonuses to employees in order to avoid problems during tax and labor inspections.

2. What premiums can be taken into account in tax expenses under OSNO and simplified tax system.

3. What legislative and regulatory acts regulate the procedure for calculating bonuses and including them in expenses for taxation.

Employees' wages, as a rule, consist of several parts: wages (for hours actually worked, for the amount of work actually completed, etc.), compensation payments and incentive payments. Incentive payments include bonuses to employees. Splitting the salary into a fixed part and a bonus part is in the interests of both the employer and the employee. The employer has the opportunity to stimulate employees to achieve higher indicators and results, and at the same time not overpay them if such indicators are not achieved. And for employees, the bonus part of their wages is a real opportunity to receive greater rewards for their work. That is why almost all organizations and individual entrepreneurs-employers provide for the payment of bonuses to employees, and bonuses often make up the largest part of wages. Given this fact, the calculation and payment of bonuses is the object of increased attention during inspections by the tax inspectorate and the state labor inspectorate. How to bring the calculation of bonuses into compliance with labor and tax laws and avoid problems during audits - read on.

What the tax inspectorate is interested in regarding bonuses to employees is whether wage costs (including the payment of bonuses) are legally classified as expenses that reduce the taxable base for corporate income tax or the single tax paid in connection with the application of the simplified taxation system.

What the state labor inspectorate is interested in is whether the rights of workers have been violated when calculating and paying them wages (including bonuses).

All bonuses to employees are subject to insurance contributions to the Pension Fund, Social Insurance Fund, and Compulsory Medical Insurance Fund (Clause 1, Article 7 of Federal Law No. 212-FZ of July 24, 2009), therefore, when checking the Social Insurance Fund and Pension Fund of the Russian Federation, inspectors are usually interested in the total amount of accrued bonuses without detailed analysis.

Documentation of awards

According to the Labor Code of the Russian Federation, establishing bonuses for employees is the right of the employer, and not his responsibility. This means that the employer has the right to approve a remuneration system that provides for a bonus component (salary-bonus, piece-rate-bonus system, etc.) and document this fact. Please note that if the employer’s internal documents establish a remuneration system that includes bonuses, then in this case the calculation and payment of bonuses to employees, according to internal agreements, is the responsibility of the employer. Failure to fulfill this obligation may result in justified complaints from employees and serious claims from the labor inspectorate. In this regard, it is important to correctly document the procedure and conditions for bonus payments to employees.

What documents need to reflect the conditions and procedure for bonuses to employees:

1. Employment contract with the employee. Terms of remuneration, including incentive payments, which include bonuses, are mandatory for inclusion in the employment contract (Article 57 of the Labor Code of the Russian Federation). At the same time, it must clearly follow from the employment contract under what conditions and in what amount the bonus will be paid to the employee. There are two options for stipulating bonus conditions in an employment contract: fully specify the conditions and procedure for bonuses, or make a reference to local regulations that contain this information. It is advisable to use the second option, to provide a reference to local regulations in the employment contract, because when making changes to the conditions for rewarding employees, you will only need to make appropriate changes to these documents, and not to each employment contract.

2. Regulations on remuneration, regulations on bonuses. In these local regulations, the employer establishes all the essential conditions for bonuses to employees:

- the ability to accrue bonuses to employees (remuneration systems);

- types of bonuses and their frequency (for results based on the results of work for a month, quarter, year, etc., one-time bonuses for holidays, etc.)

- a list of employees who are entitled to certain types of bonuses (all employees of the organization, individual structural units, individual positions);

- specific indicators and methodology for calculating bonuses (for example, a certain percentage of salary for fulfilling a sales plan; a fixed amount and specific holiday dates, etc.);

- conditions under which the premium is not awarded. Thus, if an employee is given a bonus for conscientious performance of job duties in a fixed amount, then the employee can be deprived of this bonus only if there are sufficient grounds (failure to perform or improper performance of duties provided for in the job description; violation of internal labor regulations, safety regulations; violation resulting in disciplinary action and etc.);

- and other conditions established by the employer. The main thing is that all the conditions for bonuses for employees in the aggregate do not contradict each other and make it possible to unambiguously determine which of the employees, when and in what amount the employer is obliged to accrue and pay a bonus.

3. Collective agreement. If, at the initiative of the employer and employees, a collective agreement is concluded between them, then it must also indicate information on the procedure for paying bonuses to employees.

! Please note: in addition to the fact that the employee signs the employment contract, the employer must, upon signature, familiarize him with the regulations on remuneration, regulations on bonuses, and the collective agreement (if any).

Inclusion of bonuses in tax expenses under OSNO and simplified tax system

Labor costs for taxation purposes under the simplified tax system are accepted in the manner prescribed for calculating corporate income tax (clause 6, clause 1, clause 2, article 346.16 of the Tax Code of the Russian Federation). Therefore, when including labor costs (including the payment of bonuses) in expenses that reduce the taxable base for income tax and the simplified tax system, one should be guided by Article 255 of the Tax Code of the Russian Federation.

“The taxpayer’s expenses for wages include any accruals to employees in cash and (or) in kind, incentive accruals and allowances, compensation accruals related to working hours or working conditions, bonuses and one-time incentive accruals, expenses associated with the maintenance of these employees, provided for by the norms of the legislation of the Russian Federation, labor contracts and (or) collective agreements” (paragraph 1 of article 255 of the Tax Code of the Russian Federation). According to paragraph 2 of Art. 255 of the Tax Code of the Russian Federation, accepted labor costs for tax purposes include “accruals of an incentive nature, including bonuses for production results, bonuses to tariff rates and salaries for professional skills, high achievements in work and other similar indicators.” In addition, as a general rule, expenses in tax accounting are recognized as justified and documented expenses incurred by the taxpayer (Article 262 of the Tax Code of the Russian Federation).

Thus, having combined all the requirements of the Tax Code of the Russian Federation, we come to the following conclusion. Expenses for bonuses to employees reduce the tax base for income tax and the single tax paid in connection with the application of the simplified tax system, while simultaneously meeting the following conditions:

1. Payment of bonuses must be provided for in the employment contract with the employee and (or) in the collective agreement.

We discussed above the procedure for reflecting bonus conditions in an employment contract: either stipulating them in the employment contract itself, or referring to the employer’s local regulations. Not all employers conclude a collective agreement with employees, however, if one does exist, it should also provide for the possibility of paying bonuses and the procedure for bonuses.

! Please note: one order from the manager to pay bonuses is not enough to include bonuses in expenses. Bonuses for employees must be provided for in the employment contract with the employee and (or) in the collective agreement. Otherwise, tax authorities have every reason to remove “premium” expenses and charge additional income tax or tax under the simplified tax system. This position of the tax authorities is confirmed by numerous court decisions in their favor.

2. There is a need for a direct relationship between the awarded bonus and the employee’s “production results”, that is, the bonus must be economically justified and related to the receipt of income by the organization or individual entrepreneur.

Thus, special attention must be paid to the wording according to which bonuses are calculated. For example, bonuses for an anniversary (New Year, vacation, etc.), as well as bonuses for high achievements in sports, for active participation in the public life of the company, etc. have nothing to do with the results of the employee’s labor activity, therefore their acceptance for tax accounting is unlawful (Letter of the Ministry of Finance of Russia dated April 24, 2013 N 03-03-06/1/14283). If bonuses are awarded, for example, for specific labor indicators (fulfillment/exceeding of the sales plan, production plan, etc.), for the implementation of proposals that brought economic benefits, then they can undoubtedly be taken into account in tax expenses. In addition, if the amount of bonuses is confirmed by calculations (for example, a percentage of the amount of contracts with new clients, the amount of profit received, etc.), then inspectors will have no chance to remove the costs of paying such bonuses.

! Please note: bonuses are often awarded to employees with approximately the following wording: “For the timely and conscientious performance of their duties.” If you want to include bonuses in tax expenses, it is better not to use this wording, because the timely and conscientious performance of one’s work duties is the responsibility of the employee, and not the object of additional incentives. In this case, the tax authorities will most likely remove such expenses. Therefore, if it is impossible to provide specific labor indicators for calculating a bonus, then it is better to indicate “For work results based on the results of the month (quarter, year, etc.).” In this case, it is possible to defend the right to include such premiums in tax expenses.

Another point: the source of payment of bonuses. If profit is indicated as the source of payment of the premium, or as the basis for calculation, but a loss is actually received, then such premiums cannot be taken into account as expenses for taxation.

3. The accrual of bonuses must be properly completed.

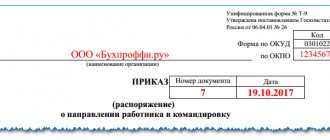

The basis for awarding bonuses to employees is the bonus order. To draw up an order on bonuses, you can use the unified forms: Order (instruction) on encouraging an employee (Unified Form No. T-11) and Order (instruction) on encouraging employees (Unified Form No. T-11a), which are approved by the Resolution of the State Statistics Committee of the Russian Federation dated 05.01. 2004 No. 1 “On approval of unified forms of primary accounting documentation for recording labor and its payment.” However, from January 1, 2013, it is not necessary to use unified forms (clause 4, article 9 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting”). Therefore, an order for bonuses can be drawn up in any form that is approved by the organization.

Download: Form No. 11-T Form No. 11-Ta Order on bonuses in any form

The main thing you need to pay attention to when filling out an order for bonuses:

- the incentive motive must correspond to the type of bonus specified in the employment contract, local regulations, collective agreement (with reference to these documents);

- it should be clear from the order which employees the bonus is awarded (specific employees indicating their full name);

- the amount of the bonus for each employee must be indicated (the amount of the bonus must correspond to the calculated data);

- It is necessary to indicate the period for calculating the bonus.

4. It is better to issue bonuses to the head of an organization (who is not its sole founder) not by order of the head himself, but by the decision of the founder (general meeting of founders).

This is due to the fact that the employer in relation to the head of the organization is its founders. Accordingly, it is within their competence to establish the conditions for payment of bonuses and its amount to the manager.

Reflection of bonuses in accounting

In accounting, the accrual of bonuses is reflected in the same way as all wages in account 70 “Settlements with personnel for wages” in correspondence with cost accounts (20, 26, 25, 44). Since bonuses to employees are subject to personal income tax, bonuses are paid minus the withheld personal income tax.

If you find the article useful and interesting, share it with your colleagues on social networks!

If you have any comments or questions, write to us and we’ll discuss them!

Legislative and regulatory acts:

1. Labor Code of the Russian Federation

2. Tax code

3. Federal Law No. 212-FZ of July 24, 2009 “On insurance contributions to the Pension Fund of the Russian Federation, the Social Insurance Fund of the Russian Federation, the Federal Compulsory Medical Insurance Fund”

4. Letter of the Ministry of Finance of Russia dated April 24, 2013 N 03-03-06/1/14283

You can find out how to familiarize yourself with the official texts of documents in the Useful sites section.