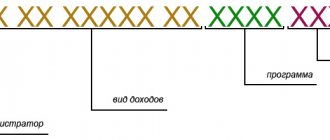

A budget classification code is a combination of numbers that characterizes a monetary transaction. This is a convenient way to group budget revenues from organizations and individual entrepreneurs. BCCs from January 2021 are determined by Order of the Ministry of Finance dated 06/08/2020 No. 99n (as amended on 10/12/2020). BCCs for contributions to compulsory social insurance are indicated in Appendix No. 1.

The cloud service Kontur.Accounting helps generate payment orders with current BCCs for paying taxes.

Get free access for 14 days

We will tell you how to choose a code for transferring insurance premiums.

When was the BCC for insurance premiums last updated?

Since 2021, the bulk of insurance premiums (except for payments for accident insurance) began to be subject to the provisions of the Tax Code of the Russian Federation and became the object of control by the tax authorities.

As a result of these changes, in most aspects, insurance premiums were equated to tax payments and, in particular, received new, budgetary BCCs. The presence of a situation where, after 2021, contributions accrued according to the old rules can be transferred to the budget, required the introduction of special, additional to the main, transitional BCCs for such payments.

As a result, from 2021, there are 2 BCC options for insurance premiums supervised by the Federal Tax Service: for periods before December 31, 2021 and for periods after January 2021. At the same time, the codes for contributions to accident insurance that remain under the control of the Social Insurance Fund have not changed.

Read more about KBK in this material.

From April 23, 2018, the Ministry of Finance introduced new BCCs for penalties and fines on additional tariffs for insurance premiums paid for employees entitled to early retirement. KBK began to be divided not by periods: before 2017 and after - as before, but according to the results of a special labor assessment.

We talked about the details here.

From January 2021, BCC values were determined in accordance with Order of the Ministry of Finance dated June 8, 2018 No. 132n. These changes also affected codes for penalties and fines on insurance premiums at additional tariffs. If in 2021 the BCC for penalties and fines depended on whether a special assessment was carried out or not, then at the beginning of 2021 there was no such gradation. All payments were made to the BCC, which is established for the list as a whole.

We talked about the nuances in the material “From 2021 - changes in the KBK.”

However, from April 14, 2019, the Ministry of Finance returned penalties and fines for contributions under additional tariffs to the 2021 BCC.

In 2021, the list of BCCs is determined by a new order of the Ministry of Finance dated November 29, 2019 No. 207n, but it has not changed the BCC for contributions. Find out which BCCs have changed here.

Thus, the last update of the BCC on insurance premiums took place on April 14, 2019. Nothing else has changed yet, and these same BCCs will be in effect in 2021 (Order of the Ministry of Finance dated 06/08/2020 No. 99n).

All current BCCs for insurance premiums, including those changed as of April 14, 2019, can be seen in the table by downloading it in the last section of this article.

How to avoid mistakes in KBK

Every accountant can make a mistake. You can copy the KBK incorrectly, look at it in the wrong source, or simply make a typo. Happens to everyone. We advise you to adhere to a number of principles, thanks to which you can always make payments correctly:

- Make the template once in the banking program. Today, almost all banks have implemented such convenient functionality.

- Get an electronic reference book, there are many of them. They will allow you to receive up-to-date information without unnecessary searching. The pleasure is not free, but penalties for mistakes also cost money.

- Check the KBK periodically on the tax service website. There you can generate the correct payment order for the company completely free of charge, and then compare it with what order was actually drawn up.

- You can select the KBK that you entered and copy it into the search bar on the Internet. The search engine identifies what the code is. This way you can understand the correctness of entering the BCC.

BCC for insurance premiums in 2020–2021 for the Pension Fund of Russia

Payment of insurance premiums to the Pension Fund is carried out by:

- Individual entrepreneurs working without hired employees (for themselves);

- Individual entrepreneurs and legal entities hiring workers (from the income of these workers).

At the same time, payment of a contribution by an individual entrepreneur for himself does not exempt him from transferring the established amount of payments to the Pension Fund for employees and vice versa.

Individual entrepreneurs who do not have staff pay 2 types of contributions to the Pension Fund:

- In a fixed amount - if the individual entrepreneur earns no more than 300,000 rubles. in year. For such payment obligations in 2020-2021, KBK 18210202140061110160 (if the period is paid from 2017) and KBK 18210202140061100160 (if the period until 2017 is paid) are established.

IMPORTANT! The income of an individual entrepreneur on UTII for the purpose of calculating fixed insurance premiums is imputed income, not revenue (letter of the Ministry of Finance of the Russian Federation dated July 18, 2014 No. 03-11-11/35499).

- In the amount of 1% of revenue that exceeds RUB 300,000. in year. For the corresponding payment obligations accrued before 2021, KBK 18210202140061200160 has been established. But contributions accrued in 2017–2021 should be transferred to KBK 18210202140061110160. That is, the code is the same as for the fixed part (letter from the Ministry of Finance of Russia dated 04/07/201 7 No. 02-05-10/21007).

Find out about the current fixed payment amount for individual entrepreneurs by following the link.

Individual entrepreneurs and legal entities that hire employees pay pension contributions for them, accrued from their salaries (and other labor payments), according to KBK 18210202010061010160 (if accruals relate to the period from 2017) and KBK 18210202010061000160 (if accruals are made for the period before 2021) .

You will find a sample payment order for contributions to compulsory pension insurance for employees in ConsultantPlus. If you do not already have access to this legal system, a full access trial is available for free.

Budget classification codes for taxes for 2021-2022

The BCCs for the taxes indicated in the tables below have not changed in recent years (the same for 2021 and 2021). So that you can easily and quickly find the CBC you need (among the most popular ones), we have divided them into groups:

KBK table for personal income tax for 2021-2022

| Personal income tax on employee income | 182 1 0100 110 |

| Penalties for personal income tax on employee income | 182 1 0100 110 |

| Personal income tax fine on employee income | 182 1 0100 110 |

| Personal income tax on individual entrepreneur income on OSNO | 182 1 0100 110 |

| Penalties for personal income tax on income of individual entrepreneurs on OSNO | 182 1 0100 110 |

| Personal income tax fine on income of individual entrepreneurs on OSNO | 182 1 0100 110 |

KBK income tax table

| Purpose of payment | Mandatory payment | Penalty | Fine |

| To the federal budget (except for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the budgets of the constituent entities of the Russian Federation (except for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the federal budget (for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| To the budgets of the constituent entities of the Russian Federation (for consolidated groups of taxpayers) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 11 |

| When implementing production sharing agreements concluded before October 21, 2011 (before the law of December 30, 1995 No. 225-FZ came into force) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of foreign organizations not related to activities in Russia through a permanent representative office | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of Russian organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the income of foreign organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From dividends from foreign organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| From the profits of controlled foreign companies | from the profits of controlled foreign companies | from the profits of controlled foreign companies | from the profits of controlled foreign companies |

KBK for VAT

| Payment type | Tax | Penalty | Fine |

| VAT on goods (work, services) sold in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| VAT on goods imported into Russia (from the Republics of Belarus and Kazakhstan) | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| VAT on goods imported into Russia (payment administrator - Federal Customs Service of Russia) | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

What to do if KBK made a mistake when paying a tax or contribution? Find out the answer to this question in the Ready-made solution from ConsultantPlus by receiving free trial access to the system.

BCC 2021-2022 for special regimes (simplified taxation, imputation, patent, agricultural tax), trade tax and tax on gambling business will be as follows:

| Name KBK 2021-2022 | KBK for transferring tax or contribution | KBK for penalties | BCC for fine |

| Single tax under the simplified tax system “income” | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Single tax under the simplified tax system “income minus expenses” (including minimum tax) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| UTII | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Unified agricultural tax | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Trade fee | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Patent (city district budget) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Patent (municipal district budget) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Patent (for residents of Moscow, St. Petersburg, Sevastopol) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Gambling tax | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

BCC for property taxes (transport, land, property tax)

| Name of KBK | KBK for transferring tax or contribution | KBK for penalties | BCC for fine |

| Transport tax for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Transport tax for individuals | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for legal entities (for Moscow, St. Petersburg, Sevastopol) | 182 1 06 06 031 03 1000 110 | 182 1 06 06 031 03 2100 110 | 182 1 06 06 031 03 3000 110 |

| Land tax within the boundaries of urban districts for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on land within the boundaries of inter-settlement territories for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on land within the boundaries of rural settlements for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on land within the boundaries of urban settlements for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for plots within the boundaries of urban districts with intra-city division for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for plots within the boundaries of intracity districts for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Property tax for individuals (for Moscow, St. Petersburg, Sevastopol) | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of urban districts | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of inter-settlement territories | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of rural settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of individuals located within the boundaries of urban settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of organizations (not included in the unified gas supply system) | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of organizations included in the unified gas supply system | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

There are a number of changes in the BCC for excise duties, but the main codes remain the same:

| Name of KBK | KBK for transferring tax or contribution | KBK for penalties | BCC for fine |

| Excise taxes on ethyl alcohol produced in Russia from food raw materials (except for those listed in the following paragraphs) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on ethyl alcohol produced in Russia from food raw materials (distillates of wine, grape, fruit, cognac, Calvados, whiskey) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on ethyl alcohol produced in Russia from non-food raw materials | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian-made alcohol-containing products | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian beer | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian alcoholic products with an ethyl alcohol content of more than 9% (except for beer and various wines) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian alcoholic products with a share of ethyl alcohol up to 9% (except for beer and various wines) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian wines | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian motor gasoline | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on Russian diesel fuel | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

What BCCs for FFOMS contributions are established in 2020–2021

Contributions to the FFOMS, as well as contributions to the Pension Fund, are paid by:

- IP - for yourself;

- Individual entrepreneurs and legal entities - for hired employees.

Contributions for individual entrepreneurs to the FFOMS are paid for themselves using BCC 18210202103081013160 (if related to the period from 2021) and BCC 18210202103081011160 (if related to the period until 2021).

For hired employees, individual entrepreneurs and legal entities must pay contributions to the Federal Compulsory Medical Insurance Fund using KBK 18210202101081013160 (for payments accrued from 2021) and KBK 18210202101081011160 (for accruals made before 2021).

You will find a sample payment order for compulsory medical insurance contributions for employees in ConsultantPlus. You can get a trial full access to K+ for free.

Changes for a simplified tax system

If tax is paid for the period after 2021, a single BCC will apply. Previously, there was a separate code for the basic and minimum taxes.

Income

The main BCC is 18210501011011000110. If for periods before 2011, then 18210501012011000110.

Income minus expenses

BCC for income minus expenses:

| Code | Payment |

| 18210501021011000110 | After 2011 |

| 18210501022011000110 | Until 2011 |

| 18210501050011000110 | Min. tax for periods up to 2021 |

| 18210501030011000110 | Min. tax for periods before 2011 |

What BCCs for insurance premiums are established for the Social Insurance Fund in 2020–2021

Payments to the Social Insurance Fund are classified into 2 types:

- paid towards insurance for sick leave and maternity leave;

- paid towards insurance for accidents and occupational diseases.

Individual entrepreneurs working without hired employees do not list anything in the Social Insurance Fund.

Individual entrepreneurs and legal entities working with hired personnel make payments for them:

- for sick leave and maternity insurance - using KBK 18210202090071010160 (if we are talking about accruals made since 2017) and KBK 18210202090071000160 (if accruals were made before 2017) - contributions are administered by the Federal Tax Service;

- for insurance against accidents and occupational diseases - in the amount determined taking into account the class of professional risk by type of economic activity, using BCC 393 1 0200 160 - contributions are transferred directly to the Social Insurance Fund.

Individual entrepreneurs and legal entities concluding civil contract agreements with individuals pay only the second type of contributions, provided that this obligation is specified in the relevant agreements.

A sample payment order for contributions to OSS from VNiM for employees can be found in ConsultantPlus. You can get a trial full access to K+ for free.

Read more about the specifics of calculating insurance premiums when signing civil contracts in the article “Contract and insurance premiums: nuances of taxation .

Filling out a payment form when paying a fine

The differences between paying the tax amount and the penalty amount lie in filling out several fields of the payment order:

- Field 106 “Basis of payment” when paying penalties acquires the value “ZD” in case of voluntary calculation and repayment of debts and penalties, “TR” - at the written request of the supervisory authority or “AP” - when accruing penalties according to the inspection report.

- Field 107 “Tax period” - you need to put a value other than 0 in it only when paying a penalty on a tax claim. In this case, the field is filled in according to the value specified in such a requirement.

- Fields 108 “Document number” and 109 “Document date” are filled in in accordance with the details of the inspection report or tax requirement.

As for the BCC (field 104), for penalties on contributions paid to the Federal Tax Service in 2020-2021, they are as follows:

| Insurance type | KBK |

| Pension | 182 1 0210 160 |

| Medical | 182 1 0213 160 |

| For disability and maternity | 182 1 0210 160 |

And for contributions for injuries, which remain under the jurisdiction of the FSS, the KBC for penalties is 393 1 0200 160.

How to meet the payment deadline for social contributions, read in this material .

Results

Insurance premiums intended for extra-budgetary funds are required to be paid by both individual entrepreneurs and legal entities. BCC for insurance premiums for 2020–2021 when making payments, you should use only current ones - this is an important factor in the timely recording of payment by its recipient.

Sources:

- Tax Code of the Russian Federation

- Order of the Ministry of Finance of Russia dated November 29, 2019 No. 207n

- Order of the Ministry of Finance of Russia dated 06/08/2018 No. 132n

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Consequences of errors when paying penalties

Since the latest changes came into force, the Treasury and the Federal Tax Service have jointly organized work to independently clarify payments that were assigned the status of unclear in the system (letter from the Federal Tax Service dated January 17, 2017 No. ZN-4-1 / [email protected] ). Therefore, if funds are received into the budget account using incorrect details, the treasury will send the payment where it is needed. But this does not apply to all errors. For your convenience, we have prepared a table for determining further actions depending on the type of error made:

| Error in payment order | Consequences |

| TIN, KPP, recipient's name, field 104, 106, 107, 108, 109 | Payment is subject to automatic verification. To speed up the process, you can write a clarifying letter to the tax office. |

| Payment details (account number, BIC, bank name) | Payment will not be credited to your personal account. You need to write a letter to the bank to cancel the payment if it has not yet been executed, or contact the Federal Tax Service to return it. In the second case, it is recommended to duplicate the payment using the correct details to avoid arrears. |

| Amount of payment | If the payment is made for a large amount, then you need to write a letter to offset the overpayment to another cash register company. If you paid less than necessary, then you need to make an additional payment |

KBK for payment of fines

A fine is an additional charge to the amount of debt for insurance contributions for complete non-payment of the premium. This sanction is imposed only for non-payment of compulsory medical insurance funds at the end of the year. The amount of the fine depends on the time the fee is not paid:

- for the first violation - 20% of the debt amount;

- for secondary and subsequent payments - 40% of the debt amount.

When paying a fine for contributions to health insurance for an individual entrepreneur for himself, the receipt indicates KBK 18210202103083011160.