Accounting software under the simplified tax system: postings

Accounting for the company's software is regulated by the basic accounting standards - the Law “On Accounting” dated December 6, 2011 No. 402-FZ and PBU 14/2007. When purchasing exclusive rights to software, the company becomes the owner of the program. If the software meets the criteria for an intangible asset specified in clause 3 of PBU 14/2007 (the object is separated from other assets, is used in the company’s activities for more than a year, is capable of bringing benefits to the company, its value is reliably determined, and its sale is not expected within a year), then it is accounted for at actual cost as part of intangible assets on account 04. Costs incurred will be written off by monthly depreciation over the useful life period established by the company. The service life of the software is determined based on the period of time when the operation of the asset is most profitable for the company, and can be reviewed annually.

Initially, the costs of purchasing software are accumulated in accounting on the account. 08 (D/t 08 - K/t 60, 76), and upon commissioning they go to the debit of the account. 04 (D/t 04 - K/t 08). Write-off of the cost of software is fixed by depreciation every month during the useful life - D/t 20.26, 44 - K/t 05.

If the program was purchased under a simple (non-exclusive) license, this means that the company received the right to use the software for a certain time, and the right to dispose of it remains with the developer. Since the program will not be the property of the company, it cannot be recognized as an intangible asset. In this case, the costs of its purchase are reflected as follows:

- deferred expenses (FBP) (D/t 97 – K/t 60, 76) and are written off evenly every month if the purchase is paid for in a one-time payment (D/t 20,26,44 – K/t 97);

- current expenses, if the company makes periodic payments for using the program (D/t 20.26.44 – K/t 60.76).

The estimated cost of the purchased license is taken into account on the company's balance sheet, for example, in the debit of account 012. Software costs are written off in the manner prescribed by the company, after commissioning and documentation of the installation of the program. Expenses for installing, configuring, and maintaining software are recognized in accounting as current costs and are written off in the reporting period when they were incurred (D/t 20.26.44 – K/t 60.76).

Supply of non-exclusive rights to software

Copyrights for all types of computer programs (including operating systems and software packages), which can be expressed in any language and in any form, including source text and object code, are protected in the same way as copyrights for works of literature.

A computer program is a set of data and commands presented in an objective form, intended for the operation of a computer and other computer devices in order to obtain a certain result, including preparatory materials obtained during the development of a computer program, and the audiovisual displays generated by it.

A non-exclusive right to computer programs, that is, a property right on a non-exclusive basis, implies the limited right of its owner to use such programs within the limits specified by the contract. Non-exclusive rights to use computer programs are transferred by concluding a license agreement with the copyright holder of these programs.

In accordance with paragraph 1 of Article 1286 of the Civil Code of the Russian Federation, under a license agreement, one party - the holder of the exclusive right to a computer program (licensor) grants or undertakes to provide the other party (licensee) with the right to use this program within the limits provided for by the agreement. According to paragraph 2 of paragraph 1 of Article 1235 of the Civil Code of the Russian Federation, the licensee can use the program only within the limits of those rights and in the ways provided for by the agreement. The right to use such a program not expressly stated in the license agreement is not considered granted to the licensee.

By virtue of paragraph 3 of Article 1235 of the Civil Code of the Russian Federation, the license agreement indicates the territory in which the use of the program is permitted. If the license agreement does not indicate the territory in which the use of the program is permitted, the licensee has the right to use it throughout the Russian Federation.

The period for which the license agreement is concluded cannot exceed the period of validity of the exclusive right to the work (clause 4 of Article 1235 of the Civil Code of the Russian Federation). If the license agreement does not specify its validity period, the agreement is considered to be concluded for five years, unless otherwise provided by the Civil Code of the Russian Federation. In case of termination of the exclusive right, the license agreement is terminated.

In accordance with paragraph 4 of Article 1286 of the Civil Code of the Russian Federation, a paid license agreement must necessarily stipulate the amount of remuneration for using the program or the procedure for calculating such remuneration. Such an agreement may provide for the payment of remuneration to the licensor in the form of fixed one-time or periodic payments, percentage deductions from income (revenue) or in another form.

According to paragraph 6 of Article 1235 of the Civil Code of the Russian Federation, the essential terms of the license agreement are:

- subject of the contract

- ways to use the program

The transfer of the exclusive right to a work to a new copyright holder is not a basis for changing or terminating the license agreement concluded by the previous copyright holder on the basis of paragraph 7 of Article 1235 of the Civil Code of the Russian Federation.

Please note that license agreements, by virtue of paragraph 1 of Article 1236 of the Civil Code of the Russian Federation, may provide for:

- granting the licensee the right to use the program while reserving the licensor’s right to issue licenses to other persons (simple (non-exclusive) license)

- granting the licensee the right to use the program without retaining the licensor’s right to issue licenses to other persons (exclusive license)

Unless otherwise provided in the license agreement, the license is assumed to be simple (non-exclusive). In addition, the same agreement, in accordance with paragraph 3 of Article 1236 of the Civil Code of the Russian Federation, may simultaneously contain the terms of an exclusive and non-exclusive license for different ways of using the program.

Do you have any suggestions on how to improve our products? Write to us about it! We will make the necessary changes and provide you with a new version completely free of charge .

1990-2019 © JSC NPP Granit Center - innovative solutions in the field of automation of military registration 115088, Moscow, Novoostapovskaya, 5 building 14

Call us: +7 (495) 912-3579 extensions: 1, 3 65914, 3 65921, 3 65963 | Contacts

When copying resource materials, a direct link to the source is required

[1]

The program was developed jointly with Sberbank-AST CJSC. Students who successfully complete the program are issued certificates of the established form.

You will learn about current changes in the Constitutional Court by becoming a participant in the program developed jointly with Sberbank-AST CJSC. Students who successfully complete the program are issued certificates of the established form.

A budgetary educational institution, under an agreement for the supply of programs for electronic computers (hereinafter referred to as computers), acquires: - non-exclusive rights to software worth RUB 31,000.00; — software distribution kit (CD) worth RUB 400.00; — certificate of activation of the technical support service for a period of 1 year in the amount of RUB 43,400.00. The supplier prepared the following documents for these products: - an act of transfer of rights in the amount of RUB 31,0000.00; — invoice for RUB 43,800.00. with two items highlighted (CD worth RUB 400.00 and a technical support service activation certificate for a period of 1 year worth RUB 43,400.00).

How to correctly reflect the receipt and payment of these goods (services) in accounting?

Rationale for the conclusion:

1. Non-exclusive rights to the software

2. Software distribution (CD)

If the transfer of the right to use software is accompanied by the transfer on the basis of separate documents (in this case, an invoice) of tangible media indicating their value, then these tangible media, in accordance with the provisions of Instruction No. 157n, can be accounted for at the generated initial (actual) cost in the accounting accounts fixed assets or inventories. For example, CDs and DVDs included in the delivery package can be taken into account as part of inventories in account 105 06 “Other inventories” and written off from the balance sheet when issued to responsible persons. Accordingly, in accounting, the cost of the CD should be attributed to article 340 “Increase in the cost of inventories” of KOSGU. It is advisable to reflect information about the delivery set in the appropriate Card (f. 0504041).

Tax accounting of software costs under the simplified tax system

In order to recognize exclusive rights to software as an intangible asset in tax accounting, the following conditions must be met (clause 4 of article 346.16, clause 1 of article 256 of the Tax Code of the Russian Federation):

- their cost must exceed 100,000 rubles,

- useful life - more than 12 months,

- the property is depreciated and used for its own needs.

Expenses for this asset are written off quarterly in equal amounts during the tax period (year) after payment and acceptance of the software for accounting.

An asset acquired with periodic payment delineation during the term of the agreement cannot be classified as an intangible asset (clause 8, clause 2, article 256 of the Tax Code of the Russian Federation). The costs for such software are written off upon each subsequent payment.

If a non-exclusive right to use the software has been acquired, then in tax accounting the expenses are written off immediately after payment and acceptance of the asset for accounting as part of the RBP.

General taxation system

The procedure for paying personal income tax for individual entrepreneurs using the general taxation system is regulated by the provisions of Chapter 25 of the Tax Code of the Russian Federation.

In this case, the concept of expense is not used, by which taxable income can be reduced by reducing the tax base. Instead, the concept of deduction is established for individual entrepreneurs on the OSN. There are different categories of personal income tax deductions - investment, property, professional, social, property, standard and social.

Important

How to take into account income when switching from UTII to simplified tax system?

In a situation where an individual entrepreneur purchases computer programs and databases and makes payments under a license agreement, these costs can be taken into account when generating the individual entrepreneur’s professional deduction. They must be supported by documents confirming the fact of purchase.

The composition of expenses that an individual entrepreneur can take into account for a professional deduction for personal income tax is similar to the composition of expenses that are taken into account when determining the income tax base. The Tax Code allows licensing payments for obtaining the non-exclusive right to use computer programs and databases to be classified as other expenses associated with production and sales. Thus, due to these costs, it is possible to reduce the personal income tax base for an individual entrepreneur.

Examples of software accounting (STS)

Example 1

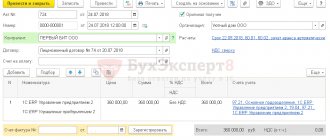

In April 2021, the enterprise acquired the exclusive right to software worth 150,000 rubles, paying in full and installing the software in April. The asset is recognized in the structure of intangible assets, the useful life is set at 3 years (36 months). In accounting, software costs will be written off by depreciation over 3 years. Postings:

| Operations | D/t | K/t | Sum |

| Purchasing software | 08 | 60 | 150 000 |

| Payment | 60 | 51 | 150 000 |

| Putting software into operation as intangible assets | 04 | 08 | 150 000 |

| From May 2021 to April 2021, depreciation is calculated monthly (150,000/36) | 20 | 05 | 4166,67 |

In tax accounting, the accountant will write off the costs of purchasing an asset before the end of the tax year, distributing the costs quarterly - in the 2nd, 3rd and 4th quarters, 50,000 rubles each. (150000/3), and reflecting them in KUDiR.

License for the right to use cryptographic accounting entries

For most cultural institutions, electronic reporting on taxes and insurance contributions is mandatory.

Institutions with a small number of staff, which have the right to choose the method of reporting, also prefer electronic methods of transmission. No wonder.

The advantages of the electronic method of submitting reports are obvious: reducing the time for sending reports, the convenience of drawing up and checking reports using electronic software, the ability to send reporting forms without leaving your workplace.

To generate and submit electronic reporting, an institution must purchase special software, as well as an electronic signature certificate. We will discuss the procedure for reflecting such expenses in accounting and tax accounting in this article.

The content of electronic reporting services provided by specialized telecom operators may vary. Mainly such services include:

1) transfer of non-exclusive rights (license) to use the program, as well as data encryption (cryptographic information protection);

2) production of an enhanced qualified electronic signature (ES certificate).

As part of contracts providing for the submission of electronic reporting (access to secure electronic document management systems), additional services may also be provided:

— technical (service) maintenance of software;

— visit of a specialist to install and configure the software product;

- program update;

— use of a secure communication channel;

- other services.

Let's take a closer look at the procedure for accounting for expenses for paying for basic services that ensure the submission of electronic reporting.

Accounting

Purchase of licensed software. In accordance with paragraphs.

Electronic signature

2 p. 1 art. 1225 of the Civil Code of the Russian Federation, a software product is recognized as the results of intellectual activity, which are granted legal protection.

The right to use a software product is exercised on the basis of a concluded license agreement, according to which one party - the holder of the exclusive right to the software (licensor) grants the other party (licensee) the right to use the software within the limits provided for by the agreement.

Source: https://berkutgun.ru/licenzija-na-pravo-ispolzovanija-skzi/

Program "1C 7.7" for simplified tax system

For fans of the software “1C: Accounting 7.7” there is also a special configuration “USN”. Version 7.7 is regularly updated, like version 8, but is significantly inferior to it in the number of useful functions and capabilities.

Thus, only in “1C: Accounting 8” will a taxpayer be able to organize in one information base the accounting of several enterprises using different taxation systems. In addition, the new version of the program supports all types of complex accounting, the work of assistant utilities is organized, it is possible to create special sub-accounts for organizing analytical accounting and manually changing transactions, as well as a lot of other advantages.

If you are already using Seven, then it will be useful for you to know that the development company offers its clients a low-cost and simplified transition from one version of the program to another. For those who are just planning to purchase software, it is better to immediately opt for the 8th version of 1C: Accounting. Moreover, the basic version of the 1C program for maintaining records according to the simplified tax system has long been discontinued from sale. Buy "1C: Accounting 7.7". Today it is possible only in the PROF version, which is much more expensive than the basic version of 1C: Accounting 8. You also need to take into account that the seven is updated only if there is a concluded agreement for information technology support, and the basic version of “1C: Accounting 8” can be updated independently without additional costs.

"1C: Accounting 8": simplified cost accounting

To automate accounting under the simplified taxation system, management chose the software product “1C: Accounting 8”, which allowed us to solve the main problems:

- The ability to maintain a general and simplified taxation system in one program, in case the taxation system changes in the future

- Speeding up the data entry and processing process

- Automatic generation of a book of income and expenses based on entered documents and manual entries

In application solutions (standard configurations) intended for organizations using a simplified taxation system, accounting is fully supported. This is necessary, first of all, for the organization itself to make a decision by the owners on the distribution of net profit and the accrual of dividends and income from participation.

The company chose “Income reduced by expenses” as the object of taxation. In this case, in order to recognize expenses in order to reduce the tax base, it is necessary:

- Monitor the fulfillment of all conditions for their recognition

- Correctly determine the moment of recognition of expenses

- Create an entry in the books of income and expenses when recognizing these expenses

To solve these problems, “1C: Accounting 8” maintains tax accounting of expenses (according to the simplified tax system). Consistent completion of the relevant documents will allow the automatic generation of a book of income and expenses at the end of the reporting (tax) period.

Setting up accounting according to the simplified tax system will be performed in the “Accounting policy (tax accounting)” form (menu “Enterprise” -> “Accounting policy” -> “Accounting policy (tax accounting)”), where on the “Basic” tab the flag “Use of a simplified system” is set Taxation", which makes the "STS" tab available for filling out. On this tab, the object of taxation is determined: “Income” or “Income reduced by the amount of expenses” and the procedure for recognizing expenses (the composition of events, the occurrence of which is a prerequisite for recognizing an expense as reducing the tax base). The fact is that some conditions for recognizing expenses are controversial.

Thus, the Ministry of Finance of Russia, in letter dated August 17, 2006 No. 03-11-02/180, added one more condition necessary for recognizing expenses for the purchase of goods when applying the simplified tax system - the goods must not only be paid to the supplier and sold, but also paid for by the buyer. We note on our own that the last condition does not directly follow from the norms of the Tax Code of the Russian Federation. The financial department made this conclusion based on an analysis of the provisions of Article 346.17 of the Tax Code of the Russian Federation, which regulates the moment of recognition of income.

In “1C: Accounting 8” the user can choose whether to wait for the buyer’s payment to be recognized as an expense or not. In the latter case, you will have to defend your position in court.

The main types of expenses and requirements for the recognition of these expenses are given in Table 1. The list of requirements for some types of expenses is determined in the form “Accounting policy (tax accounting)” on the tab of the simplified tax system (see Fig. 1), some of them are mandatory, and some can be adjusted by the user.

Table 1

| Type of consumption | Requirements (expenses are recognized at the latest) |

| Services | Third party service reflected |

| Paid to supplier | |

| Settlements with employees | Salary accrued |

| Wages paid | |

| Calculations for taxes and contributions | Taxes (contributions) accrued |

| Taxes (contributions) are transferred | |

| Materials | Materials received from supplier |

| Materials paid to supplier | |

| Materials transferred to production | |

| Goods | Goods received from supplier |

| Goods paid to supplier | |

| Goods sold to buyer | |

| Goods paid for by the buyer | |

| Additional costs (based on materials) | Increase the cost of materials and are included in expenses as part of them |

| Future expenses | Deferred expenses reflected |

| Paid to supplier | |

| Part of the expenses is written off (only the written-off part can be accepted as expenses) | |

| Intangible assets | Received NMA |

| Paid to supplier | |

| Fixed assets | Arrival of OS |

| OS commissioning | |

| Paid to supplier | |

| Separation of the principal's revenue from income | When payment is received from the buyer, the payment document is analyzed and if it contains consignment goods, the amount of accepted income is reduced by their sales value. Information about revenue for consignment goods is added to the “Content” field of the KUDiR register entry |

Automatic accounting according to the simplified tax system is provided by several specialized accumulation registers.

Registers are an element of the organization of tax accounting, designed to systematize and accumulate information about the income and expenses of an organization. They record data on the presence and movement of any quantities: material, monetary, etc. The registers used for accounting according to the simplified tax system store information about parties, the state of mutual settlements and balances of unrecognized expenses. Movement through registers is generated automatically when posting documents.

The list of expenses that reduce the tax base for a single tax is determined by Article 346.16 of the Tax Code of the Russian Federation. In accordance with paragraph 2 of Article 346.17 of the Tax Code of the Russian Federation, expenses are recognized subject to their actual payment. Therefore, control of the status of mutual settlements for tax accounting purposes is carried out in a separate register “Mutual settlements of the simplified tax system”.

To account for expenses subject to tax accounting, the configuration uses the accumulation register “Expenses under the simplified tax system.” This register stores information about expenses for which all the conditions necessary for their acceptance for tax accounting have not yet been registered (reflected in the “Income and Expense Accounting Book”). To obtain information about what specific conditions are missing, you can use the “List/Cross-tab” report (menu “Reports” -> “List/Cross-tab”), and in the “Accounting section” field you should select the value “ Expenses under the simplified tax system."

To move correctly through the registers, you need to pay attention to filling out documents.

The documents may indicate the procedure for reflecting expenses in tax accounting. To do this, use the “Expenses in NU” attribute, which can take the following values:

- Accepted - expenses comply with the requirements of Article 346.16 of the Tax Code of the Russian Federation

- Not accepted - expenses do not meet the requirements of Art. 346.16 Tax Code of the Russian Federation

- Distributed - for organizations transferred to UTII for one or more types of activities. This is how expenses are reflected that comply with the requirements of Article 346.16 of the Tax Code of the Russian Federation and are accepted, but cannot be attributed to a specific type of activity and are subject to distribution

If, when an expense is received or written off, the document does not contain the “Expenses in NU” attribute, then the procedure for reflecting expenses in tax accounting is determined by the type of transaction (for example, sale of goods), or the operation is not a tax accounting event (for example, transfer of goods to commission).

Thus, in general, in order to recognize expenses in tax accounting, it is necessary that:

- The expense was not not accepted according to the conditions of receipt

- The expense was not unacceptable under the write-off conditions

- All events provided for recognition as expenses by the norms of Chapter 26.2 of the Tax Code of the Russian Federation were reflected

Let's consider how, as a result of the implementation of the 1C:Accounting 8 program, the process of recognizing expenses for purchased goods, expenses for services of third-party organizations and for purchased materials in Absolut-XXI LLC was automated.

Example 1. Recognition of expenses on purchased goods

Goods were received from the supplier LLC “1” for a total amount of 10,000 rubles, according to the advance payment listed earlier.

In accounting, this operation is reflected by the following entries:

- Document “Outgoing payment order” with the “Paid” checkbox: Debit 60.02 Credit 51 - 10,000 rub. (advance payment transferred);

- Document “Receipt of goods and services”: Debit 41.01 Credit 60.01 - 10,000 rubles. (goods arrived); Debit 60.01 Credit 60.02 - 10,000 rub. (advance credited).

We will generate a “List/Cross-Table” report for the accounting section “Expenses under the simplified tax system” to obtain a list of unfulfilled conditions for accepting an expense. For this receipt, the line “Not written off” was created in the amount of 10,000 rubles.

Subsequently, half of the received goods were sold to the buyer LLC “2” for the amount of 15,000 rubles. After posting the document “Sales of goods and services”, the following entries were generated in accounting:

Debit 90.02 Credit 41.01 - 5,000 rub. (Cost written off); Debit 62.01 Credit 90.01 - 15,000 rub. (Revenue received)

In the actual sales report, the second line “Not paid by the buyer” is formed in the amount of 15,000 rubles.

Let us reflect the operation of receiving payment from the buyer in the document “Outgoing Payment Order” with the “Paid” checkbox:

Debit 51 Credit 62.01 - 15,000 rub.

In the report there will be a line for the receipt “not written off” in the amount of 5,000. A line is created in the books of income and expenses for the recognition of expenses for the acquisition of inventory and materials in the amount of 5,000 rubles.

Example 2. Recognition of expenses for third-party services and purchased materials

LLC “3” carried out work to repair the car in the amount of 2,000 rubles, including replacement of spare parts in the amount of 1,000 rubles.

These transactions will be reflected in accounting through the documents “Receipt of goods and services” and will generate the following transactions:

Debit 26 Credit 60.01 - 2,000 rubles; Debit 10.05 Credit 60.01 - 1,000 rub.

In the report on the balances of the register “Expenses under the simplified tax system”, one line is formed for services provided in the amount of 2,000 rubles. and the second line for the receipt of spare parts from about in the amount of 1,000 rubles. (see Fig. 3).

After paying the debt to the supplier, only one line will remain in the report for the receipt of spare parts in the amount of 1,000 rubles. A line is created in the books of income and expenses to recognize expenses for services of third-party organizations in the amount of 2,000 rubles. We will write off materials using the document “Request-invoice”: Debit 26 Credit 10.05

A line is created in the books of income and expenses for the recognition of expenses for the acquisition of inventory and materials in the amount of 1,000 rubles. (see Fig. 4).