BSO is a strict reporting form, analogous to a cash receipt. From July 1, 2019, the BSO can be printed only through the online cash register and the mandatory details of the cash receipt must be indicated in it. This is a requirement of Federal Law 54, the law on the use of cash register equipment.

Strict reporting forms were converted into electronic form so that sales information was transferred from the online cash register to the tax office. This is how the Federal Tax Service sees the company’s income and checks whether the entrepreneur pays taxes correctly.

For operating without an online cash register or trading in violations, the tax office issues a fine. If the BSO does not contain the required details - a fine of 1,500 to 3,000 rubles, for failure to issue a BSO to the buyer - a warning or a fine of 2,000 rubles.

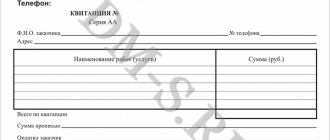

BSO details in accordance with the old version of 54-FZ

- indication of the name of the form

- indication of the six-digit number, series

- indication of the name of the company that issued the BSO to the client, full name of the individual entrepreneur

- indication of the address of the company or individual entrepreneur

- indication of the TIN of the company or individual entrepreneur

- indication of the type of service and its cost

- indication of payment for the service

- settlement terms of the company and the client

- indication of the position and full name of the cashier, his signature

- company seal

BSO forms in accordance with Resolution No. 359 are produced in a printing house or generated using special automated systems.

The list of details is provided in two copies.

Business entities (transport enterprises, cinemas, zoos) can use simplified forms of BSO.

Instead of BSO - POS terminal

Operations for carrying out payment transactions through a POS terminal are subject to the Law “On activities for accepting payments from individuals carried out by payment agents” dated 06/03/2009 No. 103-FZ. Note that POS terminals include devices that allow you to use bank cards when paying for purchases.

If payment is made using a POS terminal, then a strict reporting form does not need to be issued instead of a cash receipt if the terminal is connected to a cash register that generates a receipt. If equipment is used that does not generate a cash receipt, then a BSO is issued.

More information about postings when using POS terminals at an enterprise can be found in the article “Posting debit 57 credit 57 (nuances)” .

When using a POS terminal by taxpayers specified in clause 8 of Art. 7 of Law No. 290-FZ provide buyers with BSO generated by cash register or an automatic payment system in the form used by such a taxpayer before the entry into force of Law No. 290-FZ (or printed forms approved by the accounting policy of the enterprise or (for some cases) by law).

How to take into account forms according to the old version of 54-FZ

It is necessary to take into account BSOs that are produced in the printing house. If they are produced using an automated system, their accounting is carried out through hardware and software tools, as well as under the supervision of the taxpayer.

To work with printed forms, you need a special BSO accounting book. Its sheets must be stitched, numbered, certified by the director and chief accountant of the company, and stamped by the organization.

The head of the company and his subordinate enter into an agreement. From now on, an employee of the company must maintain a BSO and receive funds from the company’s clients to whom services are provided. The employee must fill out the BSO in accordance with Resolution No. 359.

Reception of printing BSOs at the enterprise is carried out by a special commission.

BSOs are always stored in a safe place.

Will all BSOs be affected by changes in legislation on cash register systems?

Until now, we have been talking about BSO as documents confirming the fact of accepting cash. However, BSO also refers to other documents not related to cash payments. Thus, the instructions for the application of the Chart of Accounts, approved by Order of the Ministry of Finance dated October 30, 2000 No. 34n, states that the BSO accounted for in off-balance sheet account 006 includes subscriptions, diplomas, certificate forms, etc.

Law 54-FZ does not regulate the circulation of these types of BSO. At the same time, in Art. 1.1 of the new edition of this law states that the BSO is a document containing information about the monetary settlement and confirming the fact of its implementation.

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

Therefore, all types of BSO that are not related to the execution of settlements in 2018 will be formed and used in the old way - on the basis of current regulatory accounting documents.

Strict reporting form according to the new version of 54-FZ

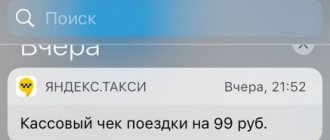

BSO and cash receipt are similar. The main difference between the BSO is that it is generated electronically, and an automated system is used that sends data on settlements between companies and clients via the Internet to the tax service.

Advantages of the new type of BSO

However, you need the Internet to use it. |

Advantages of using BSO for individual entrepreneurs

What is the superiority of strict reporting forms for private entrepreneurs over cash receipts? Everything is obvious:

- Firstly, there is no need to buy a cash register, which, for a moment, does not cost two hundred rubles at all. A new cash register will cost the company owner an amount equal to at least ten thousand rubles.

- Secondly, the entrepreneur receives an exemption from the necessary registration of cash register equipment with the tax office, not to mention training of all employees to work with cash register systems.

- Thirdly, if an entrepreneur is not tied to a specific place and he has to go, for example, to a client’s house to do hair or makeup, then filling out a receipt will be more comfortable than carrying around a cash register for knocking out receipts .

- Fourthly, the absence of a cash register automatically eliminates the need to pay for its service.

There are many advantages of using strict reporting forms. What can you say about the shortcomings?

BSO details according to the new version of 54-FZ

- indication of name

- indication of the serial number for the cashier's work shift

- indication of the address of the organization where the payment was made

- indication of the company name, full name of the individual entrepreneur

- Taxpayer INN

- indication of the taxation system

- indication of a specific calculation indicator

- name of the services provided to the client

- indication of cost per unit of service provided

- indication of the total invoice amount for services

- indication of a specific form of payment

- indication of the position and full name of the person who accepted the payment from the client

- indication of the registration number of the automated BSO generation system

- indication of the serial number of the drive

- indication of the fiscal indicator of the BSO

- indication of the website address where you can request information about the calculation

- telephone or email (when transmitting BSO only electronically)

- indication of data on the fiscal document

- specifying information about the work shift

- indication of the fiscal indicator for the message

How the online cash register for BSO is used, taking into account changes in 2021

The use of strict reporting forms when dealing with cash proceeds remains the right of the seller, and not an obligation. The abolition of the typographic format is proof of this.

Details of cash receipts and BSO also indicate that documents generated using cash register equipment have equal legal force. They are allowed to be used starting in 2021. Sellers of alcohol and excisable goods require a receipt indicating the nomenclature.

If the region in which the businessman works is officially recognized as a remote area (there are interruptions in the Internet), then the details include the address of the site where the authenticity of the purchase is verified.

The main indicator is the requirements for those businessmen who are obliged to make the transition to online cash registers within a certain time frame, to make cash payments as transparent and legal as possible.

In turn, manufacturers of cash register equipment have provided the possibility of generating forms not only using a cash register, but also a fiscal registrar. Printing can be done on a regular printer.

For those who combine several types of activities: services and trade, issuing cash receipts is more convenient, where the nomenclature can include the type of work, services, as well as the taxation system that is applied (PSN, UTII).

For those entrepreneurs who only provide services to the public, the transition to online cash registers gives them the opportunity to compare the cost of devices and legal requirements, making a decision to continue using or abandon BSO.

Who may not use forms and cash receipts

BSO is a document that is issued only when services are provided to you. But entrepreneurs may not formalize it and not use other types of cash register systems during:

- shoe repair, painting

- providing services for carrying things at train stations, airports, sea and river ports, etc.

It should also be remembered that 54-FZ in the old and new versions allows some persons not to use cash registers if they are selling:

- goods at fairs

- tickets, newspapers, magazines

- ice cream

- seasonal vegetables, fruits and goods in tank trucks

In what cases can you replace a cash receipt with a BSO?

- cash payments are made to the population

- provision of services

- activities on UTII or PSN before the deadline established by law for the transition to online cash registers

When you cannot replace a cash receipt with a BSO:

- if the client is a legal entity,

- if there is no sale of goods.

Watch the video, which explains in detail in what cases BSO should not be used

Conclusion

The strict reporting form is an excellent alternative to online cash register in cases where this is permitted by law. The choice between online cash registers and BSO depends on the specifics of a particular type of business.

GO TO ONLINE CASH CATALOG

By contacting our company, you can receive a full range of necessary services:

- Electronic signature for registering an online cash register.

- Connection to OFD

- Registration of an online cash register with the Federal Tax Service

- Connection and support of EGAIS

- Subscriber support for Online cash registers

- Submission of declarations on alcohol and beer to FSRAR.

Did you like the article? Share it on social networks.

- Olgp 03/06/2020 13:23

Comment Good afternoon, tell me, is it still not clear that in 2020 BSO for laundry services can be used in printing or only online?Answer

- Anyuta 03/06/2020 15:58

Comment Hello. Online only.

Add a comment Cancel reply

Also read:

Marking of leftover tires and tires

The deadline for marking tire residues is approaching.

Manufacturers and importers no longer produce or import these goods without Data Matrix codes. A deferment has been provided for retailers and wholesalers. But soon there will not be a single unmarked tire left on the territory of the Russian Federation to be sold. Deadlines for marking tires and tires Let's consider up to what date marking of leftover tires and tires is allowed. Mandatory labeling… 691 Find out more

Data collection terminal for marking

The data collection terminal for labeling is used when reading Data Matrix codes from the packaging of goods controlled by the Chestny ZNAK system.

The device is a mini-computer and a barcode scanner - “two in one”. The device allows you to read codes on the sales floor, during inventory, and warehouse operations. Data collection terminal at low prices A large selection of data collection terminals from the most popular manufacturers of cash register equipment at low prices... 565 Find out more

Self-employed in 2021 - clarification of the law

Self-employed people will receive new opportunities in 2021.

We will tell you who the self-employed are, who can take advantage of the tax regime, what tax benefits are provided, how to get them, what taxes you need to pay, and what will change in 2021. Since October, the special regime “Professional Income Tax” has been in effect in all regions. Regulates the application of the tax regime of Federal Law No. 422 of November 27, 2018. Now residents of any locality… 973 Find out more

What changes in the accounting procedure for BSO?

Based on clause 4 of Art. 5 of Law No. 54-FZ (as amended by Law No. 290-FZ), which prescribes the transfer of data on the use of cash registers to the tax office in electronic form, it is logical to assume that now records of issued BSO and cash register receipts are kept in the memory of cash register equipment or automatic devices, forming into files suitable for transfer to the Federal Tax Service. In addition, fiscal drives, which should be installed on cash registers and automatic payment acceptance systems, generate such data and transmit it to fiscal data operators.

The procedure for installing fiscal drives is described by Law No. 290-FZ. First of all, this applies to organizations and individual entrepreneurs that are subject to the general taxation system and the simplified tax system. Last but not least, the transition to an automatic procedure for the transfer of fiscal data has been established for those who use UTII and PSN - until 07/01/2019, such entrepreneurs may not use fiscal drives and form BSO according to the old procedure: print in a typographical way or using existing AS for BSO .

The accounting of forms by everyone who uses BSO instead of cash receipts is carried out in the manner prescribed in Decree of the Government of the Russian Federation dated May 6, 2008 No. 359. Interestingly, this resolution prohibits keeping a BSO accounting journal in electronic form. Clause 13 of the resolution prescribes keeping records in a special book, which must be laced, its sheets numbered, signed by the head and chief accountant of the enterprise or individual entrepreneur and sealed. This order is consistent with the above-described features of the practical use of printed BSOs. And this same procedure demonstrates another nuance associated with the ability to use only electronic BSOs.

More information about the procedure for recording and storing BSO that exists today can be found in the material “Procedure for recording and storing strict reporting forms.”

Let's take the situation with tickets to entertainment events again. The vast majority of such BSOs are sold through intermediaries. For example, the leader in ticket sales MDTZK (Moscow Directorate of Theatrical and Entertainment Events) once made a “technological breakthrough” - it organized automated ticket sales. All MDTZK ticket offices are equipped with special electronic equipment; “tickets” from theaters and similar enterprises are received, in fact, in the form of electronic information about the availability and cost of seats. The BSO printout upon purchase is carried out by the MDTZK cash desk employee (he also accepts money). A report on tickets sold, which the theater will use to calculate its revenue, is generated only later.

That is, electronic BSOs are quite common between the theater and the distributor. But another question arises: at what point and how will the theater itself generate revenue from tickets sold through an intermediary, which should be recorded in the fiscal accumulator? And what should be recorded in the storage device of the intermediary who prints out the ticket on his speaker? Moreover, the intermediary is neither the owner of the tickets being sold, nor the one who will actually provide services for the sold BSO.

Similar questions will arise in all areas where BSO is traditionally implemented through intermediaries - in sports and entertainment, health resorts, tourism, transport services for the population, etc.

More information about the procedure for recording and storing BSO that exists today can be found in the material “Procedure for recording and storing strict reporting forms.”

The sum of it all

When paying in cash, issuing to the client a receipt from the merchant as confirmation of payment instead of a check issued by cash register or other documents provided for in case of exceptions is illegal. In any case, the main document is considered to be only a cash receipt. It can be replaced by a BSO, sales receipt or “other document” only in situations provided for by law. PKO is a primary accounting document that has its own meaning - registration of cash transactions within the activity.

Simplicity

There are no paper contracts required and it is completely legal. We are always nearby, and you are always confident during inspections!

our clients

Our pride is our clients who print strict reporting forms with us. These are real companies that you can check by TIN, and which use BSO-123. You can contact them to find out how they are working with us, for example.

IP Danilova Daria Mikhailovna

Phone: +7 (926) 118-8775 Taxpayer Identification Number: 246213131659

IP Lyakhovchuk Galina Ivanovna

Phone: +7 (395) 433-0060 Taxpayer Identification Number: 381900123334

LLC Strela

Phone: +7 (953) 754-6443 Taxpayer Identification Number: 5118002386

IP Smoliy I.V.

Phone: Taxpayer Identification Number: 261900941359

LLC "TC "INSTRUMENT-SERVICE"

Phone: +7 (812) 702-0187 Taxpayer Identification Number: 7826673404

IP Kodzhimonyan Georgy Arturovich

Phone: +7 (918) 702-8881 Taxpayer Identification Number: 151603505520

IP Pavlova Ksenia Aleksandrovna

Phone: +7 (919) 435-1088 Taxpayer Identification Number: 312827070115

Here is only a small part, more in the general list.

Blog

- Happy New Year! [ February 5, 2021 15:51 ]

- We're alive! [ February 26, 2021 11:36 ]

- The law on the extension of BSO-123 has been adopted! [ 9 January 2021 09:35 ]

- Happy New Year 2018! [ December 30, 2021 16:48 ]

- BSO-123 remains with you until July 2021 [ November 22, 2017 17:09 ]

Go to Blog

Incorrect electronic receipt

When accepting expenses for tax accounting, should the accountant verify the details of the cash receipt in accordance with Article 4.7 of Law No. 54-FZ? If it is discovered that the KMM check does not comply with all the requirements for registering a check according to the new rules (for example, the Federal Tax Service Inspectorate website will not be reflected), in this case can such a check be accepted for expenses and tax accounting? Or is it considered an incorrectly executed primary document and is not subject to acceptance as expenses and reduction of the tax base?