Admission

Strict reporting forms are printed or generated using automated systems (clause 4 of the Regulations approved by Decree of the Government of the Russian Federation of May 6, 2008 No. 359).

Forms produced by printing must be recorded by name, series and numbers in the document form accounting book. The form of such a book for commercial organizations has not been approved. Therefore, the organization needs to develop it independently. You can take the following as a basis for developing your own document form:

- book form for recording documents of strict reporting OKUD 0504819;

- form of the book of accounting of strict reporting forms OKUD 0504045.

The sheets of the book of accounting forms must be numbered, laced, signed by the head and chief accountant of the organization, and also sealed.

This follows from paragraph 13 of the Regulations, approved by Decree of the Government of the Russian Federation dated May 6, 2008 No. 359, and letter of the Ministry of Finance of Russia dated August 31, 2010 No. 03-01-15/7-198.

Accounting for forms produced using automated systems is carried out automatically using software that allows you to obtain information about issued strict reporting forms. In this regard, when generating strict reporting forms in an automated way, the organization must comply with the following requirements:

- the automated system must be protected from unauthorized access, identify, record and store all operations with the document form for at least five years;

- When filling out and issuing a document form, the automated system stores the unique number and series of its form.

This is stated in paragraph 11 of the Regulations, approved by Decree of the Government of the Russian Federation of May 6, 2008 No. 359.

Receive the BSO on the same day with an acceptance certificate. It can be drawn up, for example, according to the form approved by the GMEC protocol of June 29, 2001 No. 4/63-2001. The act must be approved by the head of the organization and signed by members of the commission for the acceptance of strict reporting forms. The composition of the BSO acceptance committee is fixed by order of the head of the organization. Such rules are provided for in paragraph 15 of the Regulations approved by Decree of the Government of the Russian Federation of May 6, 2008 No. 359.

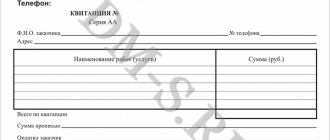

How to fill out the BSO

The regulations set out a number of requirements for filling out this document:

- clear, legible, without discrepancies;

- corrections are not allowed;

- at least in two copies.

What to do if the BSO is damaged

Made a mistake in a strict reporting document? This document cannot be thrown away because it is numbered. You are supposed to cross out the damaged form and hand it in at the end of the working day along with the proceeds and the current BSO (copies and counterfoils). They will be attached to the BSO Account Book.

Sometimes it happens that the form is filled out correctly, but the client refused the service at the last moment and therefore did not pay for it. With such a BSO you should do the same as with a damaged one: cross it out and hand it in at the end of the day in its entirety: 2 copies with the same number (or a copy and a spine).

NOTE! If the forms are not printed, but generated by an automated system, then opposite the damaged form should be written. Printed invalid BSOs are subject to recording and destruction in the usual manner.

Storage

The head of the organization must, by order, appoint someone responsible for the storage and issuance of strict reporting forms. An agreement on full financial responsibility must be concluded with this employee and conditions must be created for him to store SSO. Strict reporting forms must be stored in metal cabinets, safes or specially equipped rooms, which are sealed or sealed daily. Such rules are established by paragraphs 14 and 16 of the Regulations, approved by Decree of the Government of the Russian Federation of May 6, 2008 No. 359.

Situation: when organizing the accounting and storage of strict reporting forms, is it necessary to apply the instructions approved by the protocol of the State Interdepartmental Expert Commission on Cash Registers (GMEC) dated June 29, 2001 No. 4/63-2001?

Answer: yes, it is necessary.

Minutes of the GMEC dated June 29, 2001 No. 4/63-2001 have not been canceled to date. However, it was drawn up on the basis and during the validity of regulatory legal acts that have lost their force. Therefore, it can be applied to the extent that does not contradict the Regulations approved by Decree of the Government of the Russian Federation of May 6, 2008 No. 359.

Storage and destruction of strict reporting forms

The shelf life of BSO (tear-off document spines) should not be less than 5 years. The storage location is a specially equipped room or metal safes that exclude the possibility of damage or theft. Along with the spines and additional copies, records are also kept of damaged and unusable copies.

After the expiration of the established period, the forms must be destroyed, but not earlier than a month from the date of the last inventory. The inventory results are subject to registration.

A separate act is drawn up for the destruction of documents that are no longer suitable and have expired. Signed by management when creating a special commission. The composition of the commission is not regulated by law. It is advisable to assume that the members may be the manager, representatives of the accounting service, the financially responsible person, and personnel employees. The same destruction conditions are provided for damaged copies.

Accounting: acquisition of BSO

Reflect the purchase of strict reporting forms in accounting with the following entries:

Debit 10 (15) Credit 60

– the receipt of strict reporting forms is reflected;

Debit 20 (23, 25, 26, 44...) Credit 10 (16)

– strict reporting forms were transferred to the organization’s divisions for use (at the time of transfer of the forms for reporting).

Such rules are established by paragraph 22 of the instructions approved by the GMEC Protocol of June 29, 2001 No. 4/63-2001, and paragraph 15 of the Regulations approved by Decree of the Government of the Russian Federation of May 6, 2008 No. 359.

The receipt of strict reporting forms should also be reflected in off-balance sheet account 006. This is explained by the fact that the movement of such documents requires additional control (Chart of Accounts). Reflect the BSO on the balance sheet in a conditional valuation. Such rules are established in the Instructions for the Chart of Accounts. The conditional valuation can be equal to the actual price or any other value, for example 1 rub. The procedure for determining the conditional valuation is fixed in the accounting policy for accounting purposes (clause 4 of PBU 1/2008).

Organize analytical accounting on account 006 according to the places where strict reporting forms are stored (divisions, responsible persons), for example, you can enter the following subaccounts: “BSO in accounting”, “BSO in the department” (Chart of Accounts). Reflect the movement of the BSO on the balance sheet based on the intake control sheet. It is on the basis of this document that it is necessary to conduct turnover on account 006. Check the data on the control sheets monthly with the accounting book of strict reporting forms. Such rules are established by paragraph 22 of the instructions approved by the GMEC Protocol of June 29, 2001 No. 4/63-2001.

Fundamentals of legislation

The main object for accounting forms are the services specified in the classifier of services for organizations and enterprises (OK002-93).

Starting from January 2021, a new classifier of types for conducting economic activities was introduced under the editorship of the first classifier. In connection with this introduction, OK002-93 lost its legal effect. The legislative document that regulates the accounting of BSO today is Government Decree No. 359 of 05/06/2008.

Due to changes in the legislative framework in 2021, strict accounting forms will be transferred to electronic form. The forms that are currently in use will lose their legal force and, therefore, will no longer comply with the norms and requirements of the law. After 07/01/2018, the entrepreneur is obliged to convert the BSO into electronic form with the installation of special software for posting transactions with consumers and tax authorities.

Accounting: BSO movement

In accounting, reflect the movement of strict reporting forms with the following entries:

Debit 006 subaccount “BSO in accounting”

– strict reporting forms were capitalized in off-balance sheet accounting in conditional valuation;

Debit 006 subaccount “BSO in the department” Credit 006 subaccount “BSO in accounting”

– strict reporting forms were handed over to the department employee for reporting;

Credit 006 subaccount “BSO in the division”

– strict reporting forms in off-balance sheet accounting were written off.

In addition to the forms issued to customers instead of a cash register receipt, on account 006 take into account:

- check books;

- liter petrol coupons;

- work books;

- vouchers received by the organization in the branches of the FSS of Russia;

- other similar documents.

Once the BSO is completed, it becomes the primary document. If such a document was paid for at the expense of the organization and indicates an unfulfilled obligation in relation to it, then such documents are called monetary and are recorded in account 50-3 “Cash documents”. Such documents include:

- travel documents (air and train tickets);

- cash coupons for gasoline;

- vouchers purchased by the organization;

- other similar documents.

An example of reflecting in accounting and taxation the receipt and use of strict reporting forms

CJSC Alfa provides laundry services and uses strict reporting forms.

On August 23, Alpha purchased 100 strict reporting forms “Work Order”, the total cost of which was 236 rubles, including VAT - 36 rubles. During the remainder of the month, 28 forms were issued. The organization keeps records of materials without using accounts 15 and 16. On the off-balance sheet account, strict reporting forms are taken into account in the conditional valuation of 1 ruble.

Alpha determines income and expenses using the accrual method. Income tax is paid monthly. Due to the fact that the procedure for accounting for expenses on strict reporting forms is not established in Chapter 25 of the Tax Code of the Russian Federation, the accounting policy for tax purposes of Alpha stipulated that these expenses are included in material expenses and are indirect when calculating income tax.

The purchase of forms was reflected in accounting with the following entries:

Debit 10 Credit 60 – 200 rub. (236 rubles – 36 rubles) – strict reporting forms have been capitalized;

Debit 19 Credit 60 – 36 rub. – VAT is allocated from purchased forms;

Debit 68 subaccount “Calculations for VAT” Credit 19 – 36 rubles. – accepted for deduction of VAT on forms;

Debit 006 – 100 rub. – strict reporting forms were capitalized for the balance sheet in the conditional valuation;

Debit 20 Credit 10 – 56 rub. (200 rubles/piece: 100 pieces × 28 pieces) – strict reporting forms were handed over to the responsible person;

Credit 006 – 28 rub. – strict reporting forms issued to clients were written off.

The accountant recorded these printed forms in the book of strict reporting forms.

In tax accounting, the cost of 28 issued forms is 56 rubles. was included in expenses in August.

Application of strict reporting forms

When providing services to individuals, strict reporting forms are allowed. This affects settlements with the population, which are carried out in cash or using plastic payment cards.

When working with legal entities, the use of forms is not provided. Under these conditions, calculations are carried out using cash registers.

Both organizations and individuals have the right to use strict reporting forms. persons when carrying out business activities.

Who has the right to use BSO?

| Subjects | Tax system | Possibility of using BSO | note |

| Organizations | BASIC | Yes | When making payments to the population |

| IP | BASIC | Yes | |

| Organizations | simplified tax system | No | No retail sales possible |

| IP | simplified tax system | No | |

| Organizations | UTII, trade tax | Yes | When making payments to the population |

| IP | UTII, trade tax, patent | Yes |

For those who are allowed to use BSO, these documents are equivalent to a cash register receipt and enable management to save on the purchase and maintenance of a cash register.

At the same time, the use of forms must be observed in accordance with the law, otherwise fines of 3,000 - 4,000 for individuals will be imposed. individuals, 30,000 - 40,000 - relative to organizations.

In addition to BSO, which are receipts for settlements with the population, forms of this type also include other documents, such as work books, sick leaves, travel documents, orders, coupons.

BASIC: income tax

Situation: how to take into account the costs of purchasing strict reporting forms when calculating income tax?

The answer to this question depends on the type of forms.

For some strict reporting forms, special expense items are provided. Thus, take into account the costs of purchasing check books as part of the costs of banking services (subclause 15, clause 1, article 265 of the Tax Code of the Russian Federation). The financial department recommends using this approach for organizations using the simplified approach (letter of the Ministry of Finance of Russia dated May 25, 2007 No. 03-11-04/2/139). This conclusion can be extended to organizations that apply the general taxation system (clause 2 of Article 346.16 of the Tax Code of the Russian Federation). Both with the accrual method and with the cash method, take into account the costs of purchasing check books at the time of payment (subclause 3, clause 7, article 272, clause 3, article 273 of the Tax Code of the Russian Federation). See also the entries reflecting the costs of bank services.

According to strict reporting forms used instead of cash registers, the tax accounting procedure is not clearly established in the legislation.

On the one hand, the costs of purchasing strict reporting forms can be classified as material costs on the basis of subparagraph 2 of paragraph 1 of Article 254 of the Tax Code of the Russian Federation. This is explained by the fact that these costs are associated with payments for services rendered, i.e., the purchased forms are used for production needs.

On the other hand, these costs can be taken into account as part of office expenses and attributed to other expenses (subclause 24, clause 1, article 264 of the Tax Code of the Russian Federation). A similar point of view is expressed by the Russian Ministry of Finance in a letter addressed to organizations using the simplified system (letter dated May 17, 2005 No. 03-03-02-04/1/123). The conclusions of the financial department can be extended to organizations that apply the general taxation system (clause 2 of article 346.16 of the Tax Code of the Russian Federation).

Thus, the organization must independently decide whether to classify such expenses as material or other (clause 4 of Article 252 of the Tax Code of the Russian Federation). Fix your choice in your accounting policy for tax purposes (Article 313 of the Tax Code of the Russian Federation).

Working outside the cash register: who can?

Strict reporting forms are an alternative way to record payments in cash or by card when cash register is not used. Clause 3 Art. 2 of Federal Law No. 54-FZ of May 22, 2003 “On the use of cash register equipment when making cash payments and (or) payments using payment cards” allows such accounting for certain categories of individual entrepreneurs or organizations. Those engaged in certain activities have the right to use BSO instead of checks, namely:

- sells press and related products at kiosks (newspapers and magazines should make up more than half of the assortment);

- sells securities;

- sells lottery and city transport tickets;

- provides food to pupils and students, as well as employees of educational institutions;

- engages in trade in specially designated places, such as markets, fairs, exhibition complexes, etc. (separate pavilions, shops, tents, etc. inside such places are subject to other requirements);

- peddles or sells from carts (except for complex equipment and perishable food products);

- offers tea and similar products in train carriages;

- makes it possible to purchase medicines at paramedic stations in rural areas;

- sells ice cream from trays, soft drinks, beer, butter, etc. spilling from tanks, waddling live fish and vegetables;

- accepts glass containers and scrap (except metal);

- offers to buy religious products and literature in specially designated places (temples, church shops, etc.), provides services for worship;

- sells stamps at their face value.

ADDITIONALLY. It is allowed not to use cash registers, using BSO instead of checks, for those entrepreneurs who operate in hard-to-reach areas (their list is approved by regional legislation).

BASIS: VAT

VAT on purchased strict reporting forms can be deducted if the following conditions are met:

- the tax is presented by the supplier;

- strict reporting forms were purchased for transactions subject to VAT;

- strict reporting forms are accepted for registration;

- there is an invoice for them.

This is stated in Article 171 of the Tax Code of the Russian Federation.

For more information about this, see Under what conditions can input VAT be deducted?

The exception to this rule is when:

- the organization enjoys VAT exemption;

- uses forms in VAT-free transactions.

In these cases, include input VAT in the cost of strict reporting forms. This follows from paragraph 2 of Article 170 of the Tax Code of the Russian Federation.

Documentation of BSO inventory

To document the inventory of strict reporting forms, Russian legislation provides for form No. INV-16, approved by Resolution of the State Statistics Committee No. 88 of 08/18/1998. Its use is not mandatory (information of the Ministry of Finance of the Russian Federation No. PZ-10/2012), however, this form is one of the most convenient documents that allows you to record the results of an inventory of strict reporting forms. The provisions of Resolution No. 88, which regulate the procedures for circulation of Form No. INV-16 in an enterprise, can also be taken into account by organizations and individual entrepreneurs.

Thus, an inventory compiled on the basis of form No. INV-16 can be generated in two copies, on which the participants of the inventory commission, as well as financially responsible persons, sign. The first copy of the document remains in the accounting department, the second - with the financially responsible person who accepts strict reporting forms for safekeeping.

Before the start of the inventory, the organization, represented by the manager, requests from the financially responsible persons responsible for the safety of the BSO, receipts confirming that by the start of the inventory, strict reporting forms were submitted to the accounting department.

For more information about other types of inventory provided for by the legislation of the Russian Federation, read the article “How to conduct an inventory before annual reporting?” .

simplified tax system

If a simplified organization pays a single tax on income, then the costs of purchasing strict reporting forms do not affect the tax base. Such organizations do not take into account any expenses (clause 1 of article 346.14, clause 1 of article 346.18 of the Tax Code of the Russian Federation).

If an organization pays a single tax on the difference between income and expenses, include the input VAT presented by the supplier when purchasing strict reporting forms as expenses (subclause 8, clause 1, article 346.16 of the Tax Code of the Russian Federation).

Situation: how can a simplified organization take into account the cost of strict reporting forms? The organization pays a single tax on the difference between income and expenses.

The answer to this question depends on the type of forms.

For some strict reporting forms, special expense items are provided. Thus, take into account the costs of purchasing checkbooks as part of the costs of banking services (subclause 9, clause 1, article 346.16 of the Tax Code of the Russian Federation). A similar point of view is expressed by the Russian Ministry of Finance in letter dated May 25, 2007 No. 03-11-04/2/139. Take these expenses into account when calculating the single tax after they have been paid (clause 2 of Article 346.17 of the Tax Code of the Russian Federation).

According to strict reporting forms used instead of cash registers, the tax accounting procedure is not clearly established in the legislation.

On the one hand, the costs of purchasing strict reporting forms can be classified as material costs (subclause 5, clause 1 and clause 2, article 346.16, subclause 2, clause 1, article 254 of the Tax Code of the Russian Federation). This is explained by the fact that these costs are associated with payments for services rendered, i.e., the purchased forms are used for production needs.

On the other hand, these expenses can be classified as office expenses (subclause 17, clause 1, article 346.16 of the Tax Code of the Russian Federation). A similar point of view is expressed by the Russian Ministry of Finance in letter dated May 17, 2005 No. 03-03-02-04/1/123.

Peculiarities of pricing when providing services

Today, employment in the service sector predominates over other sectors. This is a feature of the post-industrial economy, especially in developed countries.

Services are sometimes defined as intangible goods consumed where they are produced. They cannot be transferred or resold. Enterprises that sell the least tangible services can most freely set prices for them. The quality of a service is assessed through its price. The price of a service is much more an indicator of quality in the eyes of the consumer than the price of a product.

OSNO and UTII

Strict reporting forms can be used both in the activities of an organization subject to UTII and in activities on the general taxation system. As a rule, it is known what type of activity the calculations for which a strict reporting form is drawn up, used instead of cash registers, are related to. Accordingly, the costs of purchasing forms and the amount of VAT paid can be determined on the basis of direct calculation. This procedure follows from paragraph 4 of Article 149, paragraph 9 of Article 274 and paragraph 7 of Article 346.26 of the Tax Code of the Russian Federation.

In some cases, it is impossible to determine in what type of activity BSOs are used. Therefore, the costs of their acquisition cannot be directly allocated. In this case, distribute them in proportion to the share of income from each type of activity (clause 9 of Article 274 of the Tax Code of the Russian Federation). The need to use this method may arise, for example, when distributing expenses according to a checkbook.

VAT, which can be deducted on distributed expenses for social security, is calculated according to the methodology established in paragraphs 4 and 4.1 of Article 170 of the Tax Code of the Russian Federation.

To the received share of expenses for the activities of an organization subject to UTII, add the amount of VAT that cannot be deducted (subclause 3, clause 2, article 170 of the Tax Code of the Russian Federation).

Inventory and write-off

BSO require a special approach not only to the issues of their storage and accounting. It is very important for an accountant to know how to write off strict reporting forms. In case of damage or detected defects, such forms cannot simply be thrown away.

Monitoring of the state of the BSO is carried out during an inventory, during which it is necessary to check the presence and safety of copies/spoofs of forms, the absence of defects, corrections, the correspondence of the amounts in copies/spinners to the data of statements or cash reports, etc. Based on the results of the inventory, a statement of discrepancies is generated (form 0504092) , on the basis of which the detected damaged or defective BSO is written off. The procedure has a strictly defined order. The first step is to prepare an act on the write-off of strict reporting forms. It can also be drawn up in any form, however, budgetary institutions most often use the established form (form 0504816). The act must list the members of the commission, the period for which the write-off occurs, and the date. In addition, you should indicate the numbers of the documents being written off, their series and reasons for writing off. After this, strict reporting forms must be destroyed. The date of destruction is also recorded in the act. The document must be signed by all members of the commission and approved by the head of the institution.

conclusions

The write-off of BSO is carried out by the business entity in strict accordance with the approved regulations. Such forms may be deregistered for various reasons.

The basis for write-off may be either the end of the mandatory storage period or extraordinary circumstances.

An important role in this case is given to the correct execution of all necessary documents, as well as strict adherence to the prescribed procedure.

The management of an economic entity is responsible for the correctness and legality of all necessary procedures.