From February 1, 2021, stores will begin issuing cash receipts with a new mandatory list of details. Previously, individual entrepreneurs were given a temporary deferment to comply with the law regarding the indication of the name of goods. They had the privilege of a simplified procedure for drawing up fiscal checks and could issue a check without deciphering the product or service.

Question and answer Why is there a QR code on the receipt?

The benefit was established by Federal Law dated July 3, 2016 No. 290-FZ. The deferment ends in February, and all cash receipts will be required to contain more detailed purchase information.

The concepts of “cash register” and “cash register”: essence and differences

First, a little theory. Let’s start our discussion with the concepts of “cash register” and “cash register”. Most mistakes and misconceptions are due precisely to the fact that their meaning is often confused.

So, the cash desk is all transactions of an individual entrepreneur (or organization) carried out in cash. These can be either income transactions (receipt of income) or expenditure transactions (spending funds for various purposes). All cash transactions must be recorded on cash register. In fact, all individual entrepreneurs and organizations have a cash register; exceptions are very rare: even if all transactions are carried out by bank transfer, you can withdraw money for some business expenses, for example, for the purchase of office supplies.

“Cashier” is a kind of imaginary “wallet” where money comes in and where it comes from for expenses. For organizations, the concept of “cash” looks easier to understand, since in accounting according to the chart of accounts there is a special account 50 “Cash”, which records all cash transactions.

Cash register is a cash register equipment necessary for making cash payments for goods (or services) sold to a client, that is, the machine itself, which issues a check.

The definition from the law generally goes like this:

Cash register equipment - electronic computers, other computer devices and their complexes that provide recording and storage of fiscal data in fiscal drives, generate fiscal documents, ensure the transfer of fiscal data and print fiscal documents on paper in accordance with the rules established by the legislation of the Russian Federation on application of CCT.

Let's immediately note the important differences:

- According to the cash register, only cash received from customers for goods or services purchased from you is recorded; at the cash register, all cash receipts are considered receipts - revenue from the cash register for the day, withdrawals of money from the current account, and so on.

- You cannot spend money from the cash register - there is no expense part, money for expenses can be issued exclusively from the cash register.

Conclusion: cash register is not equivalent to cash register - these are different concepts that mean different things. Cash desk is all cash transactions of an entrepreneur or organization (a kind of “big wallet”), cash register is the actual machine for accepting money from a client and issuing a check. The connection between the two concepts can be easily shown: at the end of the day, the store’s revenue from the cash register is handed over to the cash register of the individual entrepreneur (organization), the transaction is formalized by the receipt.

And also transfer this money to the bank into your current account and how often?

There may be money in the cash register within the limit that you set yourself in the manner prescribed by the above provision No. 373-P, and Everything in excess is surrendered on the day of excess, because, in accordance with clause 1.4. of the specified provision (373-P): “A legal entity or an individual entrepreneur is obliged to keep cash in bank accounts in banks in excess of the cash balance limit established in accordance with paragraphs 1.2 and 1.3 of this Regulation (hereinafter referred to as available funds). Accumulation by a legal entity or individual entrepreneur of cash in the cash register in excess of the established cash balance limit is allowed on days of payment of wages, scholarships, payments included in accordance with the methodology adopted for filling out federal state statistical observation forms, into the wage fund and social payments (hereinafter referred to as other payments), including the day of receipt of cash from a bank account for the specified payments, as well as on weekends and non-working holidays if a legal entity or individual entrepreneur conducts cash transactions on these days. In other cases, accumulation of cash in the cash register in excess of the established cash balance limit by a legal entity or individual entrepreneur is not allowed.” Up to the limit, money can be kept in the cash register as long as you like.

Regulatory regulation of the issue

So, we divided the “cash register” and “cash register” among ourselves. Now we will divide the legislative acts regulating these issues. Let us especially highlight two of them:

- Law No. dated May 22, 2003 “On the use of cash register systems when making cash payments...” No. 54-FZ - regulates the use of cash register systems.

- Directive of the Central Bank dated March 11, 2014 “On the procedure for conducting cash transactions...” No. 3210-U regulates the management of the cash register.

Having studied the documents, we conclude that all individual entrepreneurs and organizations have a cash register, that is, cash transactions (exceptions may occur, but very, very rarely), and therefore everyone must conduct them. Only individual entrepreneurs who take into account income/expenses and physical indicators in accordance with the norms of the Tax Code of the Russian Federation (for example, in KUDIR) have the right not to draw up documents for the cash register (receipt, consumables, cash book).

Conclusion: we repeat once again, “cash register” is not equal to “cash register”. The obligation to fill out a cash book has absolutely nothing to do with the mandatory use of cash registers when accepting payments from clients in cash. It is quite possible that you have a cash register, as required by law, but you, as an individual entrepreneur, enjoy the right not to process cash transactions. Or, conversely, you, as an individual entrepreneur, fall under one of the exceptions of Law No. 54-FZ and do not use cash registers, for example, when issuing BSO to individuals, but register cash transactions for receipts, filling out receipts and a cash book for control purposes.

Is a seal required for an individual entrepreneur or LLC?

Many individual entrepreneurs have received permission to work without stamps, and since it is not a mandatory detail on a check, such organizations can issue it without a stamp. The main thing is that all other details are present. But many people insistently demand its presence, refusing to believe that such a paper is valid. In such a case, it is better to have your own stamp.

LLCs cannot carry out their activities without a seal, and since their sales receipts in most cases are supported by an invoice, on which it is required, it must also be present on the accompanying papers.

Cash receipt and PKO

The differences described above allow us to conclude that there is a difference between two documents - the PKO and the cash receipt.

A cash receipt is a document issued by a cash register. What is its meaning? For the client, the check is confirmation that the individual entrepreneur has received money from him. Accordingly, in the future, the buyer will be able to file a claim with a receipt if the product turns out to be of poor quality. For individual entrepreneurs, knocking out a check is confirmation of the acceptance of cash, that is, in fact, confirmation of the formation of the amount of total sales revenue.

PKO is a primary accounting document used to record cash transactions. The meaning of a receipt order is completely different: it is used directly to record cash flow within your business (or within an organization).

This form looks like this:

Conclusion: PKO is not equivalent to a cash receipt and cannot replace it. With the help of PKO, they register the receipt of funds from various sources, rather than receiving money from customers at the cash register for purchased goods.

Now let's move on to the question itself: is it possible to issue the buyer only a receipt from the PKO? We will try to give a detailed answer. We will rely directly on Law No. 54-FZ.

conclusions

A cash receipt order and a check are used in the system of cash transactions of a business entity. However, they are not interchangeable settlement documents, since the scope of their application in practice differs significantly.

The receipt issued by the seller is the main document certifying the fact of payment by the client for the purchased goods. Its replacement with a PKO receipt cannot be considered legal for cash payments with customers.

As a financial document, the PKO has a specific purpose - to formalize the fact of accepting cash into the cash desk of a business entity. In other words, through PKO, cash transactions are processed exclusively within the enterprise.

What do we have in the source data?

- Cash register systems should be used by organizations and individual entrepreneurs if they make payments in cash, bank cards, or electronic means of payment;

- if all your sales go through a current account (non-cash payment), cash register is not used, as it is simply not needed;

- There are exceptions to the general rule when cash registers may still not be used: provision of services to the public (they may not use cash registers until 07/01/2021);

- specifics of activity or location;

- payment of tax on imputation or patent.

- We have already talked about all the exceptions in the previous article.

- Each of the exceptions to the CCP Law is accompanied by some condition, the fulfillment of which is mandatory (what must be issued instead of a check and how this document must be drawn up).

Conclusion: the main document that serves as confirmation of payment by the client for goods and services is a cash receipt. If the Cash Register Law obliges you to use a cash register, you are required to issue a check; if you may not use a cash register, but you have one (you fall under an exception, but do not use it) – you are required to issue a check.

It turns out that the presence of a cash register obliges the individual entrepreneur to issue the buyer a check, and not some other document. Let's talk about a few more situations:

- you must use a cash register, you have it, but you don’t knock out a check;

- you have the right not to use cash register, but you have it (you don’t use this right) and you don’t knock out a check;

- you must have a cash register, but you don’t have it, and therefore you cannot issue a check.

All these cases are classified as violations of the law. Failure to use cash registers and failure to punch a check are considered violations and will ensure that you are held accountable even when you do issue some document to the buyer (a certain form, a receipt from the PKO, and so on).

Everything is pretty clear here. Now let's get back to exceptions. Each of the exceptions to the CCP Law is accompanied by special requirements. These requirements are as follows:

- in a situation with the provision of services to the public (that is, individuals), cash register systems may not be used, but only on the condition that each client receives a completed BSO from the entrepreneur;

- when using UTII or a patent, you can do without a cash register, but issue a sales receipt or other document at the client’s request. These documents must contain all the details established by law;

- if the activity or location is specific, it is allowed not to issue anything at all.

Conclusion: what can be given to the buyer instead of a cash register receipt if there is no obligation to use a cash register? There are only three options:

- BSO;

- sales receipt or other document, but with a mandatory set of details;

- don't give anything away.

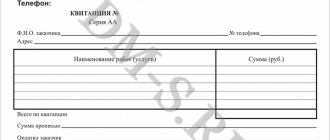

How to fill out a sales receipt form for an individual entrepreneur without a cash register

Filling out the receipt form when purchasing goods does not present any difficulties. When purchasing one unit of any product, you should cross out the blank lines so that no one can enter unnecessary data into them. It can be difficult to process a receipt for the purchase of a large number of items. Although there is a way out here:

An individual entrepreneur's check is a document known to many, but not everyone can cope with filling it out. It is evidence of the completion of a purchase and sale transaction and complements the main list of all purchased goods. It is not a strict reporting form; it has only auxiliary value . In most cases, it is used when a cash receipt is not available.

PKO instead of BSO

Is PKO suitable for the listed options? Let's consider the first two points: BSO and “other document”.

I’ll say right away that the BSO has its own requirements for mandatory details (clause 2 of the Russian Government Decree No. 359 of 05/06/2008), in addition, it must be approved by the individual entrepreneur (or LLC) and printed in a printing house. There are similar requirements for “other documents” (the list of details is given in paragraph 1 of Article 4.7 of Law No. 54-FZ as amended on July 3, 2016).

Now let's talk further. If the transaction of accepting cash for goods is processed by the PKO, the client will then receive a receipt for the PKO. Can it replace the BSO or “other document”? No, it cannot, because the lists of mandatory details of these documents differ from the details of the receipt form.

Is it possible to modify the form of the receipt for the PKO so that it meets at least the requirements that apply to the “other document”? This is only possible in theory; in practice there are several significant snags:

- The type of PKO has been approved, it is drawn up according to form No. KO-1 - who will finalize the unified form? There are few people willing.

- In order for a receipt for a PKO to pass as a BSO, it needs not only to be finalized, but also to have the forms printed in a printing house - especially since no one will do this.

- There is one more important point, even more theoretical than the previous ones. Provided that the first two points are fulfilled (let’s imagine this), we will essentially receive a new document. The original purpose of PKO is to record cash transactions at the cash register. Will our new document still be considered suitable for processing cash transactions, since it will be different from KO-1? Will the modified PKO remain legitimate for its original purpose? The issue is very controversial.

Conclusion: there can be a lot of theoretical reasoning on this issue, we have absolutely no need for it. In practice, there is only one conclusion: a receipt from the recipient cannot replace the BSO or “other document” that must be issued to the client if the individual entrepreneur has the right not to use the cash register.

Now let's turn to the last option, when the individual entrepreneur may not give anything to the buyer. In fact, if an individual entrepreneur is not obliged to issue anything to a client, but issues a receipt for a receipt, this does not directly contradict Law No. 54-FZ.

But let's pay attention to this. A receipt from a PKO can only be issued when the cash goes directly to the “cash desk” of the individual entrepreneur (or organization). Let us remind you that it is possible not to issue anything to the buyer only in case of exceptions related to the specific nature of the activity and location.

It turns out that “cash office” practically does not fit in with this exception. For example, an individual entrepreneur cannot receive money at the “cash desk” in any way if he is engaged in retail trade or from tanks, or selling products at a fair. It turns out that issuing a receipt to the client to the receipt in this case indirectly contradicts clause 3 of Law No. 54-FZ.

Conclusion: in this case, theoretically, it is still possible to issue a receipt to the PKO without violating anything. But this possibility is so small, and the justification is so confusing, that it is difficult to draw a conclusion about the legality of such actions.

Filling out - required details

You can easily order a sales receipt form from any printing house or print it on your computer and print it out as needed. Each person can design columns and rows in their own way; there is no single form, the main thing is that space is allocated for all the necessary information.

Example of filling by hand:

Sample of filling out a sales receipt

The check can be filled out either in printed form or by hand; this must be done by the seller upon completion of the transaction.

Each form must indicate:

- Full details of the company selling the goods, its name, detailed address and Taxpayer Identification Number;

- Form number and date of issue;

- Full name of the product, general name of the product group, manufacturer's brand, personal number or article number. There are as many lines, or even pages, as needed to enter all the data;

- Number of units purchased;

- Price per unit;

- The sum of all purchases of the same type, as well as the total cost;

- Seller's full name, position and clear signature;

- Seal, but due to the fact that many individual entrepreneurs are now allowed to work without seals and stamps, this item is optional.

The sum of it all

When paying in cash, issuing to the client a receipt from the merchant as confirmation of payment instead of a check issued by cash register or other documents provided for in case of exceptions is illegal. In any case, the main document is considered to be only a cash receipt. It can be replaced by a BSO, sales receipt or “other document” only in situations provided for by law. PKO is a primary accounting document that has its own meaning - registration of cash transactions within the activity.

What is the penalty for missing the required information on a check?

Fiscal receipts must be updated by February 1, 2021. Otherwise, the entrepreneur faces a fine. For the lack of necessary information and for errors in the cash receipt, a fine of 1,500 to 3,000 rubles is provided for officials and from 5,000 to 10,000 rubles for organizations.

Failure to send a cash receipt to the buyer, at his request, in electronic form by email or phone number will result in a warning or a fine of 2,000 rubles from individual entrepreneurs and 10,000 rubles from an organization.

Logbook

For more competent and accurate accounting, all issued checks can be recorded in the registration book. For this purpose, you need to take both a self-made accounting book and one specially designed for this. In a homemade one, you can make columns and their names in a way that will be convenient for filling them out, without missing out on important information and avoiding unnecessary things.

In the finished sales receipt register, all columns already have names:

- date of;

- serial number;

- client name;

- sum;

- buyer's signature.

Most stores focus more on the items being purchased rather than the buyer himself. But everyone decides for themselves what and how to enter in the registration log. Keeping a journal is not strictly necessary, but there are times when the information recorded in it plays an important role. Therefore, you should not be lazy and start such a magazine.

What are the requirements for strict reporting forms?

For certain types of activities, strict reporting forms are approved by the relevant department. The areas of application of the approved forms include (we list everything, not only for individual entrepreneurs):

- tourist services;

- insurance;

- pawnshop services;

- gasification and gas supply services;

- veterinary services;

- services of cinema and film distribution institutions;

- services of theatrical and entertainment enterprises, concert organizations, philharmonic groups, services of circus enterprises and zoos, museums, parks (gardens) of culture and recreation, etc.;

- services for the transportation of passengers and luggage (all types of transport), including services for organizing river trips, taxi services, etc.;

- services for the provision of parking lots (parking spaces) on a paid basis;

- services provided by budgetary organizations.

If the activity falls into the specified list, it is necessary to use the forms strictly in accordance with the approved form (links to the necessary documents are at the end of the article).

If a special form has not been approved for the business area, the form can be developed independently , but with mandatory compliance with the requirements of Resolution No. 359.

All of the requirements below for strict reporting forms are correct, unless otherwise provided by law (that is, unless a special form and special rules are approved at the departmental level for a specific type of activity).

view the list of mandatory details of strict reporting forms

Mandatory details of strict reporting forms include:

- document name, six-digit number and series;

- last name, first name, patronymic, location (address) of the entrepreneur;

- taxpayer identification number (TIN of the entrepreneur);

- type of service;

- cost of the service in monetary terms;

- the amount of payment made in cash and (or) using a payment card;

- date of calculation and preparation of the document;

- position, surname, name and patronymic of the person responsible for the transaction and the correctness of its execution, his personal signature, seal;

- other details that characterize the specifics of the service provided and with which the individual entrepreneur has the right to supplement the document;

- information about the manufacturer of the document form (abbreviated name, TIN, location, order number and year of execution, circulation) - if the form is produced by a printing house.

Clarification. One of the mandatory details according to Resolution No. 359 on the strict reporting form is a seal. However, given that the document has less legal force than the Civil Code and federal laws: if the entrepreneur does not have a seal, then the use of strict reporting forms is possible without a seal .

You can use forms produced by a printing house or using automated systems.

see the requirements and rules for filling out when using printed forms

- the completed form must contain all the required details (see above);

- when filling out a document form, it must be ensured that at least 1 copy is completed at the same time, or the document form must have detachable parts;

- affixing the series and number on the document form is carried out by the manufacturer of the forms;

- the document form must be filled out clearly and legibly, corrections are not allowed;

- a damaged or incorrectly filled out document form is crossed out and attached to the document form book for the day on which they were filled out.

When producing forms using an automated method, additional requirements must be met. According to tax authorities, in fact, in terms of its parameters, such equipment is similar to a cash register, and compliance with the requirements of Regulation No. 359 must be confirmed by technical documentation.

view the requirements for the production of forms in an automated way

- the completed form must contain all the required details (see above);

- when filling out a document form, it must be ensured that at least 1 copy is completed at the same time, or the document form must have detachable parts;

- the automated system must be protected from unauthorized access, identify, record and store all operations with the document form for at least 5 years;

- when filling out a document form and issuing a document by an automated system, the unique number and series of its form are stored;

- at the request of the tax authorities, the entrepreneur is obliged to provide information from automated systems about issued documents;

Not every check printing machine meets these requirements. You cannot use forms printed on a computer, since when using a regular computer it is impossible to provide protection against unauthorized access (it must be not only from “third” parties, but also from the entrepreneur himself).