In this article I was going to show how to make a balance sheet from SALT. However, having figured out how I would do this, I realized that I would start using accounting rules and terms. And I’m not sure that you and I will have the same understanding of them. So, I came up with this.

I am not interested in writing a purely theoretical article. I want to engage you so that together we can go from “reviewing SALT” to filling out the balance sheet.

For this I have my own approach: when giving new knowledge, I strive to ensure that there is a repetition of the previous ones. In other words, we repeat the knowledge that serves us as a support for new ones.

I would like to note that in this series of articles about filling out a balance sheet, I will talk about general ideas, basic rules, and show how it is done. Together with me, you will go all the way to creating a balance sheet based on the OCB of a real enterprise.

So, let's go...

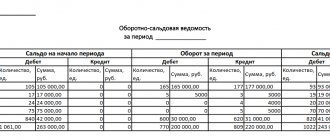

Here is the OCB of a working enterprise. In the previous article, we prepared her for creating a balance sheet .

Please note that I added two empty columns to the OCB: “Name” and “AP”. Why did I do this? I answer - For independent work, for warming up and remembering past knowledge.

Here's what we should do now:

- and open it

- In the “name” column, write the name of the account. No need to look at the chart of accounts. There is no need to achieve some exact match between the name of the account and what it is called in the chart of accounts. Just remember and write. It is enough that your name reflects the essence of the account. For example . I will call the 50th account “Cashier”. And in the chart of accounts it can be called “Enterprise Cash Office”.

- in the “AP” column for each account, indicate what it is, “A – active account”, “P – passive account” or “AP – active-passive account”. Hint : Active accounts are those that store information about what the company has and this is “what” helps the company operate and earn money. Usually “it” can be touched. Active accounts always have a debit balance or zero. Liability accounts are the debts/obligations of our company. This is simply information about the amounts owed. Passive accounts always have a credit balance or zero.

Of course, putting down “A, P and AP” is not an easy task. This requires knowledge and some reflection. I agree that there are invoices where you can issue them right away, and somewhere you can use a hint and enter the required characteristics. In any case, put it where you can do it. And fill in the remaining empty cells according to the chart of accounts. .

Once you solve the problem, compare it with what I did.

Answers are available only to subscribers!

If you are subscribed to blog updates by email, enter the access code from the last mailing letter. To receive an access code, subscribe to blog news.

Why do you need a completed document?

Every organization requires reporting, which is maintained by officials responsible for this type of activity. The report contains information showing balances, cash flows in each account and between them during the reporting period. Filling of the OSV occurs after:

- depreciation charges;

- write-off of production costs;

- tax assessments;

- formation of a financial report.

With the help of this document, items are formed in the balance sheet. He controls the correctness of the transactions made and systematizes the information expressed by them. Based on the “turnover”, facts are visible that influenced the changes that occurred in qualitative and quantitative form in the balance sheet registers. According to the data from the SALT, the digital values of various areas of activity are compared, from which it is clear what influenced the financial result of this institution.

An example that determines why a negotiable accounting instrument is needed can be presented in the following diagram:

- The enterprise is working.

- Accounting records business transactions in primary documents.

- In special journals, transactions are carried out on transactions using ledger accounts.

- Each register accumulates the same type of information.

The results of calculations are posted in standard reports, presented as balance sheets. The work of the chief accountant and the entire accounting department is not limited to this. SALT is a convenient settlement form for enterprise financiers, which they need to work with every day.

Using a table:

- analyze the company's activities;

- monitor results;

- identify and eliminate errors caused by postings.

For the head of any organization, it is necessary not only to be able to competently fill out the form, a leading economist will do this, but also to know how to read and decipher each thesis presented.

Some General Rules and Observations

I assume, reader, that you remember that accounting accounts collect and store information about the activities of a business. All information is separated according to certain criteria. So, the code and name of the accounting account serves as a separation criterion. As a result, OSV shows all the accounting accounts involved in our enterprise. From the OSV we see what information has been collected.

However, the balance sheet collects business information in a different way.

Firstly , the balance sheet divides information into ASSETS and LIABILITIES.

Secondly , within ASSET and LIABILITY, information is divided into certain groups. Each such group is an economic indicator.

Ultimately, SALT is simply regrouped on the balance sheet.

- All debit balances, and these are accounts with characteristic A, go to the “ASSET balance” section

- All credit balances, and these are accounts with characteristic P, go to the “LIABILITY” section of the balance sheet.

- Accounts with the AP characteristic are transferred to the balance sheet as follows: if there is a debit balance, it goes to an ASSET, if there is a credit balance, it goes to a LIABILITY.

The amount received in ASSET or LIABILITY is entered into the specific name of the economic indicator. The basis for including the amount in the economic indicator will be the name of the accounting account, or, when it is not clear, we will use the law on filling out the balance sheet. Well, we will start filling out the balance very soon.

Formation procedure

Purchasing a form to keep track of the movement of funds is not a problem.

They are freely available:

- on financial sites;

- in stores selling office supplies.

You can easily create such a table yourself using Excel spreadsheets.

Software systems allow you to use SALT for general accounts and with each account separately, which simplifies the accounting task. Although specialists almost never use manual labor to fill out financial papers, it is better for novice entrepreneurs to start with a fountain pen. By manually filling out the statement, you will gain a deep understanding of the essence of the operation being carried out, for which double entry is carried out. Financiers use different registers, the choice depends on the area to be analyzed and the way the data is presented.

An example is synthetic accounts. To account for them, take the initial balance with turnover, and as a result, calculate the balance at the end of the billing period.

The total amount in a correctly prepared statement consists of three parts:

- equality between income and expense, where the debit balance reflects the value of the organization at the initial stage and the receipt of assets in the credit register;

- the equivalence of debit and credit turnover is achieved by double entry, in which money entered in debit to one of the accounts is credited to the other;

- the last column consists of the equality obtained as a result of calculations, this is the price of the asset, the amount at the end of the period.

The calculator clearly monitors pairs of numerical values. If a difference is detected in at least one case, it means the register is formed incorrectly or a simple arithmetic error has occurred. Based on the synthetic accounts included in the “turnover”, the balance sheet is processed, in which the names of the sections are often the same as the accounts.

Analytical accounts in SALT are formed depending on their purpose and the characteristics of specific parameters:

- nomenclature;

- quantitative;

- categories.

This part of the reporting is not equal in terms of turnover, because cash movements occur in the same register. The balance at the beginning of the month and at the end can be in the debit or credit column, which depends on the passivity or activity of the account. For example, you can give a salary account of 70.

The types of accounts include chess OSV from synthetic accounts. “Chess” receives data from operational logs in compliance with the final equations.

This type of financial table can be described with the following description:

- Debit accounts go vertically, credit values are written in the horizontal line;

- the completed lines and columns are equal to the accounts used with the opening balance and cash flows in the reporting period;

- the accountant posts accounts according to their opening balances;

- an angular calculation is performed from the summation of income and expense;

- values for all business transactions are transferred, the amount is indicated at the intersection of interacting accounts;

- circulating numbers are also calculated with their output in the corner of the table;

- The end of the ending balance calculation is the angular total.

The balance of digital definitions is the coinciding debit turnover with the credit one. In this case, the economist correctly posted all business transactions and made correct calculations, which makes it possible to proceed to the main document.

PS

I can't get this article out of my head. There is some feeling of incompleteness, or something. The goal is clear - to lead you, the reader, to filling out the balance. Make sure you are as prepared as possible for this action. And, although I have to try to make the explanation understandable, there is still something missing in this article.

I understand that there will still be questions, but I want to keep them to a minimum. I think that I will answer some of these questions in advance. Before we start filling out the balance sheet form , I suggest working a little more with SALT.

This is what we need to do.

- we continue to work with the first column of SALT - “opening balance”

- write down the invoices that you believe collect information about our company's debts. You can immediately start writing out those bills that you know are in SALT. You can go the opposite way - cross out those accounts that are responsible for the company’s property, for what you can touch. The remaining bills are what you need.

- Issued invoices have amounts in “Debit” or “Credit”, or even both. Write out the invoice, each amount, and write what kind of debt it is - “Should our

- Remember what is called “Our Debt” in accounting. In parentheses for these names, write accounting terms for each amount. For tips, read this article.

Once you do it, compare it with what I got.

In what form is the balance sheet compiled?

The balance sheet is formed in a certain form; it belongs to the official report. If the preparation of a financial certificate is carried out for internal use, different types of accounting are used, it depends on the purpose, the data taken as the basis for the calculations.

Balance happens:

- Saldov - with data collected in a certain time period;

- negotiable - with completed operations for a limited period;

- presented on the basis of information from conducted inventories;

- calculated taking into account regulatory items (depreciation, reserves, markups) or without them;

- designed according to one professional profile, production site;

- abbreviated or complete;

- made for one enterprise or representing the financial picture of several organizations.

A report is prepared upon the request of some event in the form:

- introductory;

- liquidation;

- separating;

- unifying.

The balance of financial information can be:

- predictive;

- intermediate;

- final.

The list goes on; economists of each enterprise are allowed to use any convenient reporting form, as long as the organizational financial issue is resolved reliably, and the approach to filling out is preserved with the fundamental rules.

How to fill out a balance sheet

In order for the company to avoid fines in the future and be able to make an up-to-date and truthful forecast, it is necessary that the balance sheet be drawn up as accurately as possible, without errors or violations. Let's consider the procedure for filling out this reporting.

Rules and procedure for filling out the balance sheet

The balance sheet has several meanings for an enterprise:

- this is mandatory reporting that must be submitted to the Federal Tax Service office at the place of registration of the enterprise;

- this is a source of information that is necessary for conducting analytical research in order to make a forecast about the further development of the enterprise.

The reporting form, which is valid today, was approved by Order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n. The law provides for two forms of balance:

- complete - provides for the exclusion of individual lines for which there is no data to fill and the inclusion of additional positions, which makes it possible to increase the reliability of the report being compiled:

- simplified - used by enterprises that do not have large turnover and a large staff.

The basic rules for filling out reports are prescribed in PBU 4/99, which was approved by Order of the Ministry of Finance of the Russian Federation dated July 6, 1999 No. 43n, and read as follows:

- the source for filling out the balance sheet is the company’s accounting data;

- information must be compiled in accordance with the rules of accounting regulations and in accordance with the current accounting policies of the company;

- information must be complete and reliable.

Get 267 video lessons on 1C for free:

Rules and technique of compilation

The balance sheet shows the balance of funds for a certain time. The accounting accounts display the work of the enterprise in monetary terms; values are set from the new results obtained, which are transferred to the table.

The formation of a simplified balance sheet using a balance sheet occurs according to the following activities:

- processing of account data is carried out in order to carry out incoming and outgoing transactions to display final balances;

- a graphological system is compiled, in which the turnover of each account is recorded line by line under debit and credit;

- calculate all the figures for income and expenses, which are equated as a result;

- the total represents an inventory of all account balances;

- check the correctness of the final values, add active current accounts to the initial balance upon receipt, subtract all the values that are posted on the loan;

- for passive accounts, take the credit balance, add its current assets and subtract the values for the debit turnover;

- the resulting figure must be identical to the posting from the accounts.

The overall result consists of the final values:

- initial;

- final;

- negotiable

All amounts are recorded under the balance sheet. Its working form represents the result obtained from the total of debit balances, which is equal to the credit balance, they are withdrawn from all financial accounts.

The full balance sheet form consists of the entire list of items recommended for allocation in a specific section. Financiers of organizations are allowed to remove from the reporting those designations that are not involved in the activities of the institution, or, conversely, add information for complete reliability.

Comment on the rating

Thank you, your rating has been taken into account. You can also leave a comment on your rating.

Is the sample document useful?

If the document “Current balance (turnover sheet) for synthetic accounts” was useful for you, we ask you to leave a review about it.

Remember just 2 words:

Contract-Lawyer

And add Contract-Yurist.Ru to your bookmarks (Ctrl+D).

You will still need it!

What do the main abbreviations mean?

In accounting, abbreviations are often used that are understandable to specialists and unclear to beginners. Typically, the decoding represents the name from the first letters and indicates the working area, the name of the current funds or the economic activity of the unit. Such an abbreviation can be represented as:

- expenses for transport and procurement of materials - TZR;

- assets belonging to fixed assets - OS;

- intangible assets - intangible assets;

- production that is in an unfinished stage - work in progress;

- expenses for future periods - RBP;

- inventory items - goods and materials.

Fixed assets and intangible assets when filling out the balance sheet

Fixed assets are inextricably linked with such a concept as depreciation (accounted for in account 02). Depreciation is a gradual decrease in the initial cost of an asset associated with the operation of the asset. The depreciation process for fixed assets occurs over a certain period of time, but more than a year. As a result, everything will come to the point that the amount of depreciation will be equal to the original cost of the operating system.

Look at SALT . Account 01 records the amounts of all fixed assets at their original costs. Account 02 takes into account the depreciation amounts of these fixed assets. Now you are asking yourself, what does this have to do with the balance sheet?

It would seem that according to the rules for posting amounts from SALT to the balance sheet, we must send the amounts from the 01st account to the ASSET, and send the amounts from the 02nd account to the LIABILITY of the balance sheet. However, there is an exception for Fixed Assets.

Its essence is that before sending the amount to the balance sheet, we take the amounts from 01, subtract the amounts from 02 and send the resulting amount to where????

IN THE ASSET balance. Because depreciation can never be more than the original cost of the asset, and therefore the difference between 01-02 will always be a debit. 01 account (A) > 02 account (P). Well, in extreme cases, it will be 0.

Exactly the same situation with accounts 04 and 05. This takes into account the assets of an enterprise that do not have a physical object, like a machine or a machine. Account 04 takes into account such assets of the enterprise as licenses, the exclusive right to a patent, the exclusive right to software, etc. Their period of use is also more than 12 months and they are not intended for resale. Everything is the same as with the OS. Depreciation of Intangible Assets (IMA) is accounted for on account 05.

To finish this article, I propose to do a practical task. We'll work a little with the numbers from the OS. The task is:

- divide your sheet in a notebook or notepad into two columns: “Asset” and “Passive”

- from SALT we will work with the column “Balance at the beginning of the period”

- according to all the rules studied in this article - write out the accounting accounts and amounts, what can be classified as “Asset” and what can be classified as “Liability”

- In each column, calculate the total of all amounts

- compare the total amount of “Asset” and the total amount of “Liability”

To complete the task, you already have previously downloaded OSV. If you haven't downloaded it yet, download it here.

Perhaps now we are ready to fill out the balance sheet. We will do this in the next article. I invite you.

The concept of working capital

So, objects of labor directly used in the production process are classified as working capital. The most common assets in this block of property are monetary and material resources, which are the main participants in the release of the product. In doing so, they go through several stages:

- Inventory supplies are purchased with cash or funds from a bank account;

- At the production stage, materials and raw materials change their quality characteristics, being processed and transferring their value into the price of the product;

- At the marketing stage, the product is sold and regains its monetary form, but at the same time the profit from the sale is added to the invested value.

Thus, the technological production cycle is constantly reproduced. In addition to monetary and material resources, the company’s balance sheet also contains other current assets, which are also characterized by rapid turnover.

buhbalans_primer.jpg

Related publications

The balance sheet of an organization represents a summary statement containing information about the company's assets and liabilities. This form was approved by the order of the Ministry of Finance of the Russian Federation “On approval of PBU “Accounting statements of an organization” (PBU 4/99) dated 07/06/1999 No. 43n. This legal act contains information about what requirements apply to financial statements in general and to the balance sheet of an enterprise in particular.

Features of drawing up a balance sheet

The balance sheet cannot offset between items of assets and liabilities unless such offset is provided for by the relevant accounting provisions. This means, for example, that if at the reporting date there are accounts receivable from customers in the amount of 120,000 rubles and accounts payable to personnel for wages of 80,000 rubles in the balance sheet, these indicators should be reflected separately - 120,000 rubles - in the asset, and 80,000 rubles - in liability. It is impossible to show only the difference of 40,000 rubles (120,000 rubles – 80,000 rubles) in the balance sheet asset. However, VAT on an advance received or issued reduces, respectively, the amounts of accounts payable and receivable reflected in the balance sheet (Letter of the Ministry of Finance dated 01/09/2013 No. 07-02-18/01).

It is also important to remember that in the balance sheet the indicators are reflected in a net valuation, that is, minus the regulatory values (clause 35 of PBU 4/99). This means, for example, that fixed assets are shown on the balance sheet at their residual value (i.e., excluding depreciation), and customer receivables are shown minus the provision for doubtful debts.

Let us also recall that in the balance sheet data must be presented for at least 2 years - the reporting year and the one preceding the reporting year (clause 10 of PBU 4/99). At the same time, the balance sheet form approved by Order of the Ministry of Finance dated July 2, 2010 No. 66n provides for the reflection of data as of the reporting date, as of December 31 of the previous year and December 31 of the year preceding the previous one.

Classification of working capital

Current assets are classified depending on their characteristics. For example, they can be divided as follows

- by source of education:

- own working capital (balance sheet formula = line 1300 – line 1100), formed from company funds;

- acquired with borrowed capital (usually when financial difficulties arise);

- by degree of controllability:

- normalized, i.e. ensuring the continuity of the production process (inventory production, RBP, work in progress, finished goods);

- non-standardized, that is, in the sphere of circulation (except for finished products) and not affecting the production process (cash, accounts receivable, shipped goods).

If necessary, current assets are classified according to other criteria.