Fill out column 7

According to the Rules, in column 7 “Number and date of the document confirming payment of tax” the following is indicated:

- when importing goods into the territory of the Russian Federation - details of documents confirming the actual payment of VAT to the customs authority;

- when importing goods into the territory of the Russian Federation from the territory of a member state of the Customs Union - details of documents confirming payment of VAT to the tax authority.

For reference. Collection of indirect taxes on goods imported into the territory of one EAEU member state from the territory of another EAEU member state is carried out by the tax authority of the member state into whose territory the goods were imported, at the place of registration of taxpayers - owners of goods (clause 13 of Appendix 18 to the Treaty on the Eurasian Economic Union).

Since the Rules do not contain special provisions on the details of which documents should be given in column 7 when importing goods from states included in the EAEU, but taking into account the fact that the tax is paid to the tax authority, this column should reflect the details of documents confirming payment of VAT to the tax authority. That is, in this column you should indicate:

- or the number of the payment slip by which the tax is transferred to the budget;

- or details of the decision on offset of VAT amounts - if the obligation to pay tax is fulfilled by the taxpayer by carrying out an offset of VAT amounts by the tax authority (if the taxpayer has overpaid (collected) amounts of taxes).

Import of goods

Import of goods

Situation: how to fill out a purchase book when importing goods?

When importing goods, you need to fill out the purchase book in a special way. This is due to the fact that the foreign supplier does not issue an invoice, and the importer pays the tax at customs (tax office). Therefore, in the purchase book, instead of an invoice, the importer registers the details of a customs declaration or application for the import of goods and payment of indirect taxes (paragraphs 2–3, subitem “e”, paragraph 6 of section II of Appendix 4 to the Procedure approved by the Decree of the Government of the Russian Federation of December 26 2011 No. 1137). In this case, how to fill out each column of the purchase book, see the table below.

This procedure is confirmed by the letter of the Ministry of Finance of Russia dated February 8, 2019 No. 03-07-08/6235.

In this case, the cost of goods indicated in column 42 must be recalculated at the exchange rate on the date of registration of the customs declaration. This course can be taken in column 23 of the declaration, approved by decision of the Customs Union Commission dated No. 257.

If the accounting program does not allow you to form this indicator based on the customs value, you can take the contract value of the goods and add to it the VAT paid at customs. In private explanations, representatives of regulatory agencies allow this option.

If an organization imports goods from the countries of the Customs Union, take the indicator for filling out column 15 from the Application for the import of goods and payment of indirect taxes

An example of filling out a purchase book when importing goods. Registration of customs declaration

The Alpha organization imported a batch of full-fat cocoa paste from Germany in April.

The cost of the goods is 7000 euros.

Full-fat cocoa paste is included in the Unified Customs Tariff of the Customs Union with the HS code 1803 10 000 0. The import customs duty rate is 3% of the customs value of the goods.

The date of registration of the customs declaration is April 17, 2015. The euro exchange rate on the date of import of goods is 52.9087 rubles. per euro.

The customs value of goods on the date of import was 370,360.90 rubles. (7000 euros × 52.9087 rubles).

The customs duty amounted to 11,110.83 rubles. (RUB 370,360.90 × 3%).

The tax base for calculating VAT was RUB 381,471.73. (RUB 370,360.90 + RUB 11,110.83).

The amount of VAT payable at customs was RUB 68,664.91. (RUB 381,471.73 × 18%).

VAT was paid on April 17 (payment order No. 1501 dated).

The goods were received on April 21.

The accountant recorded data on imported goods in the purchase ledger.

An example of filling out a purchase book when importing goods. Registration of an application for the import of goods and payment of indirect taxes

The Alpha organization imported a consignment of goods from the Republic of Belarus in April. Supplier – Hermes LLC. The cost of the goods is 7000 euros. The VAT rate on imported goods is 18 percent.

The date of acceptance of goods for accounting is April 17. The euro exchange rate on this date is 52.9087 rubles. per euro. The cost of goods on the date of their acceptance for accounting (tax base for calculating VAT) amounted to 370,360.90 rubles. (7000 euros × 52.9087 rubles).

The amount of VAT payable is RUB 66,664.96. (RUB 370,360.90 × 18%). VAT was paid on April 17 (payment order dated April 17, 2021 No. 1501).

The accountant registered an application for the import of goods and payment of indirect taxes dated April 17, 2021 No. 548 in the purchase book.

Form and sample

Sample of filling out the 2021 purchase book.

Similar articles

- Transaction type code in the 2021 purchase book

- Transaction type code in the purchase book 2018

- How to fill out a purchase book under the simplified tax system - sample

- Sales book 2021 (form and sample)

- Purchase book form and sample of how to fill it out

Registration for separate VAT accounting

Registration for separate VAT accounting

For some transactions for which invoices (other documents) are issued, the law provides for a special procedure for their registration in the purchase ledger.

If an organization maintains separate VAT accounting, then register invoices in the purchase ledger only for the amount of VAT that is subject to deduction. That is, in column 15 of the purchase book, indicate the full cost of goods (work, services), which is reflected in column 9 of the presented invoice. And in column 16, indicate only the amount of VAT to which the organization has the right to deduct in the current quarter. This procedure is provided for by subparagraphs “t” and “y” of paragraph 6 of section II of Appendix 4 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137. Similar explanations are contained in the letter of the Ministry of Finance of Russia dated March 2, 2015 No. 03-07-09/ 10695.

An organization can transfer an advance (partial payment) towards future deliveries of goods (work, services, property rights), which will be used in both taxable and non-VAT-taxable transactions. In this case, the invoice received from the supplier (contractor) for advance payment (partial payment) must be registered in the purchase book for the entire amount (paragraph 5, subparagraph “y”, paragraph 6 of section II of Appendix 4 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137).

If a product is purchased that the organization will use in tax-exempt transactions, there is no need to register such an invoice in the purchase ledger. After all, the buyer will not have the right to deduct on such an invoice. This follows from the provisions of subparagraph 1 of paragraph 3 of Article 169 and paragraph 2 of Article 171 of the Tax Code of the Russian Federation.

An example of filling out a purchase book. The organization carries out taxable and VAT-exempt transactions

The organization carries out taxable and tax-exempt transactions. The organization calculates the proportion for the distribution of input VAT on goods (works, services) for general economic purposes for the current quarter.

In October, the organization was provided with waste removal services in the amount of 59,000 rubles, including VAT - 9,000 rubles. On October 29, the contractor (Proizvodstvennaya JSC) issued invoice No. 2569 to the organization for the entire amount of services provided.

These services are of a general business nature. It is impossible to determine what specific type of activity they relate to. Therefore, part of the input VAT amount is deducted, the remaining tax amount is included in the cost of services.

To distribute input VAT, the organization's accountant determined the share of tax-exempt transactions for the fourth quarter.

The volume of sales of goods during this period amounted to 1,000,000 rubles. excluding VAT, including:

- 800,000 rub. – from the sale of goods subject to VAT;

- 200,000 rub. – from the sale of goods exempt from taxation.

The share of transactions exempt from taxation was 0.2 (200,000 rubles: 1,000,000 rubles). Accordingly, the amount of tax included in the cost of garbage removal services is equal to: 9000 × 0.2 = 1800 rubles.

VAT is accepted for deduction in the amount of: 9,000 rubles. – 1800 rub. = 7200 rub.

The Master's invoice for this amount was recorded in the purchase book.

Situation: is it possible to register an invoice for the entire amount of VAT in the purchase book if an organization purchased materials intended for use in taxable and non-VAT transactions? The supplier has issued one invoice.

No you can not.

This is due to the fact that VAT is deductible only on those goods (works, services) that are used in activities subject to VAT (clause 4 of Article 170 of the Tax Code of the Russian Federation). The amount of VAT that can be deducted is determined based on the separate accounting of input VAT. In the purchase book, register an invoice for exactly this amount. The Russian Ministry of Finance made a similar conclusion in letter dated September 11, 2007 No. 03-07-11/394.

Situation: how to keep a purchase book if an organization conducts taxable and non-VAT activities? The tax amounts subject to deduction are determined at the end of the quarter as a percentage based on the cost of goods (work, services) shipped.

Register invoices issued by suppliers (performers) when shipping goods (performing work, providing services, transferring property rights) at the time of determining the amount of VAT to be deducted. That is, on the last day of the quarter. In this case, in column 16 of the purchase book, indicate the amount of tax that can be deducted in accordance with the calculation. Column 15 - the total cost of goods accepted for registration (including VAT).

This procedure follows from subparagraph “y” of paragraph 6 of section II of Appendix 4 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

Situation: how to register an invoice in foreign currency in the purchase book?

If the obligation under the terms of the transaction is expressed and paid in foreign currency, the supplier organization has the right to issue an invoice in foreign currency (clause 7 of Article 169 of the Tax Code of the Russian Federation). In the purchase ledger, such an invoice must be registered in the invoice currency. In this case, in column 14 you should indicate the name and code of the currency according to the All-Russian Classifier of Currencies, and in column 15 - the total cost of purchases (including VAT) in the invoice currency. Column 16 indicates the amount of VAT in rubles and kopecks. To do this, recalculate the amounts indicated in the invoice into rubles at the official rate in effect at the time of registration of goods (work, services) and property rights. This procedure follows from the provisions of paragraph 4 of paragraph 1 of Article 172, paragraph 5 of Article 45 of the Tax Code of the Russian Federation.

How to reflect customs VAT in the purchase book

If a company bought goods from a foreign company, and in the customs declaration the cost of the goods is reflected, for example, in dollars, and the VAT amount is in rubles, you must carefully fill out columns 14, 15 and 16.

In column 14, fill in the name and code of the currency from the customs declaration - US dollar, 840.

The information in column 15 must be filled in in dollars, and the tax amount in column 16 must be filled in in rubles.

Column 14 must be filled out if the company purchases goods for foreign currency, and the name and currency code are the same for all goods in the invoice. But the foreign seller does not prepare outgoing invoices (subparagraph “c”, paragraph 6 of Appendix 4 to Resolution No. 1137). The buyer pays VAT at customs. Therefore, it is not clear whether this column needs to be filled out. According to the Federal Tax Service specialists we interviewed, the information in the column must be filled out. And the code and name of the currency can be taken from column 22 of the customs declaration (US dollar, code 840).

In column 15 you must fill in the cost of purchases in the invoice currency. If the company does not have an invoice, there is a customs declaration. The cost of a consignment of goods is expressed in dollars. This means that in the purchase book you need to record the total cost of goods in foreign currency, increased by the amount of tax. It can be taken from column 12 of the customs declaration.

But in column 16 the amount of tax must be written down in rubles and kopecks (clause 8 of Appendix 4 to Resolution No. 1137).

Filling out the purchase book

Entries in the purchase ledger are created in the following order:

- Enter the abbreviated or full name of the consumer's company, or the full name of the consumer-entrepreneur;

- INN of the taxpayer, as well as the reason code for registration with the tax office;

- Start and end dates of the tax quarter.

Filling out the columns in the purchase book form is carried out as follows:

- 1 – number of the generated record in order;

- 2 – code of the type of transaction being performed, in accordance with the legally approved list;

- 3 – invoice number and date of its generation;

- 4 – number and date of the corrected invoice indicated in line 1a of the invoice;

- 5 – number and date of generation of the adjustment invoice;

- 6 – number and date of the correction in the adjustment invoice;

- 7 – number and date of generation of the paper, which confirms that the tax has been paid;

- Column 8 of the purchase book - the date when products or property rights were accepted for accounting;

- 9 – name of the trading company;

- 10 – INN of the tax payer, as well as the reason code for registration of the payer-seller;

- 11 – name of the agent or intermediary who purchases products under a commission contract or agency contract on his own behalf for the consignor consumer;

- 12 – INN of the tax payer, as well as the reason code for registering the intermediary specified in the previous column;

- 13 – number of the customs declaration for the sale of products that were imported into the territory of the Russian Federation from abroad;

- 14 – name and code of the currency, which is the same for all products indicated in the invoice, as well as its digital code, in accordance with the All-Russian classification;

- 15 – cost of products, in accordance with line 9 of the invoice;

- 16 – the amount of VAT, in accordance with the invoice, which is accepted for deduction in the current tax period.

Making a purchase book

Making a purchase book

Lace up the purchase book, number its pages and seal them. If the book is maintained manually, then this must be done at the initial moment of making entries in the purchase book. It is possible to maintain a purchase ledger in electronic form. However, for each quarter the book must be printed, numbered, laced and sealed. This must be done no later than the 20th day of the month following the expired quarter.

Additional sheets for the purchase book can also be maintained electronically. In this case, print out the completed sheets and staple them with the purchase book for the quarter in which the invoice was registered before the corrections were made. Moreover, the numbering of the purchase book for this quarter must be continued, taking into account additional sheets. After the purchase book, taking into account additional sheets, is stitched and numbered, seal it with the organization’s seal.

The purchase book and additional sheets to it, compiled in electronic form, should be signed with an electronic signature when transferring them to the tax office in cases provided for by tax legislation.

This procedure is established by paragraph 24 of Section II and paragraph 5 of Section IV of Appendix 4 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

Who should keep the purchase book and how?

Since the form reflects data on invoices, the responsibility for maintaining the book falls on all VAT payers (persons under the general regime), except for persons:

- entitled to exemption from added tax;

- carrying out transactions that do not require taxation.

The company independently chooses the method of maintaining the book that is convenient for itself - electronic or paper. The electronic format of the document was approved by the Federal Tax Service dated 03/04/15 by order ММВ-7-6/ [email protected] , the paper format was approved by Resolution 1137 dated 12/26/11 as amended. dated 11/29/14. If the book is filled out on paper, then at the end of the quarter all pages must be sequentially numbered. The sheets must be bound, and the book itself must be certified by the signature of the manager.

If the book is kept on electronic media, then the manager must certify it with his UKEP.

As documentation to be entered into the book is received, it is necessary to make registration entries, recording basic information about the received document in the columns of the table.

The procedure for drawing up an additional sheet

The procedure for compiling an additional sheet

When compiling an additional sheet of the purchase book, use the following algorithm.

1. In the tabular part of the additional sheet, in the “Total” line, transfer the data in column 16 from the purchase book for the quarter in which the invoice (adjustment invoice) was registered before corrections were made to it.

2. On the lines following the “Total” line, reflect the data of invoices that are canceled (i.e., data on the invoice (adjustment invoice) before changes are made to it). Indicate indicators in columns 15–16 with a minus sign.

3. In the “Total” line, summarize the total in column 16. To do this, from the indicators in column 16 in the “Total” line, you must subtract the indicators in column 16 in the line of invoices (adjustment invoices) to be cancelled.

If several corrections are made relating to one quarter, then reflect the data in columns 2–16 on the “Total” line of the previous additional sheet on the “Total” line of the subsequent sheet.

Use the “Total” line data to make corrections to the declaration.

This follows from Section IV of Appendix 4 to Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

Example of designing an additional sheet for a purchase book

In August, the accountant of Alpha LLC discovered that errors were made in the purchase book for the second quarter:

1. Incorrectly registered invoice dated June 30, 2021 No. 1200 from Master LLC in the amount of RUB 236,000. (including VAT – 36,000 rubles).

2. Invoice dated June 15, 2021 No. 560 from Hermes LLC in the amount of RUB 118,000 was not registered. (including VAT – 18,000 rubles).

On August 10, the accountant issued an additional sheet to the purchase book, in which he canceled the invoice dated June 30, 2021 No. 1200 in the amount of RUB 236,000. and registered an invoice dated June 15, 2021 No. 560 in the amount of RUB 118,000.

How to fill out a purchase book when importing if there is no invoice

When filling out the purchase book, the cost of purchases in column 15 is taken from column 9 of the invoice (subparagraph “t”, paragraph 6 of Appendix 4 to Resolution No. 1137). If a company pays VAT at customs when importing goods, then it does not have an invoice. But you cannot leave column 15 empty - the information from it falls into line 170 of section 8 of the VAT return. If the company does not fill out the column, the deduction will not be reflected in the declaration.

The Ministry of Finance in letter No. 03-07-08/6235 explained that in column 15 you can write down the customs value of the goods, taking into account duties and VAT . This information must be taken from column 12 of the customs declaration.

The consignment value is usually expressed in foreign currency. The name and code of the currency must be filled in column 14 . This information can be taken from column 22 of the customs declaration. For example, euro, 978. But the amount of tax in column 16 should be written in rubles and kopecks (clause 8 of Appendix 4 to Resolution No. 1137).

Other information must be taken from the customs declaration.

Column 3 of the purchase book indicates the customs declaration number without a date. You can take it from column A of the main sheet of the declaration. Customs officers put this number in the first line of column A of the customs declaration, i.e. in the upper right corner of the document. It consists of three parts, separated by fractions. For example, 10902040/280116/0000244 (letter of the Federal Tax Service of Russia dated No. ED-4-15/1065).

In column 7 you should write down the date and number of the order to pay customs VAT. This data is recorded in column B “Counting details” of the goods declaration.

In column 9 - the name of the foreign supplier from column 2 “Sender/Exporter” of the customs declaration.

But column 10 of the purchase book with TIN and KPP empty. Here you only need to fill in Russian numbers (see below).

Import from foreign countries

Column 7 of the purchase book.

To confirm the right to deduct VAT on imported goods, provide payment details in the Purchase Book

no longer any need

to pay tax (Letter from the Federal Tax Service dated 02/22/2019 N SD-4-3/ [email protected] ):

- in column 7 “Number and date of document confirming payment of tax” of the purchase book, put a dash

; - in column 3 “Number and date of the seller’s invoice” we indicate information about the registration numbers of the diesel engine

; - Section 8 of the VAT return is completed in the same way.

We were provided with a customs declaration, which does not indicate the numbers and dates of payments, and without them the formation of a purchase book cannot be carried out, what should I do?

Automation of affixing space

planned in 1C.

For now, enter the Purchase Book in printed form manually

.

In electronic format

For VAT returns, the presence of the element “Information about the document confirming the payment of tax” in the exchange file

is not necessary

(Letter of the Federal Tax Service dated February 22, 2019 N SD-4-3/ [email protected] ).

TD

registration number is a number assigned by Russian customs, consisting of three parts (23 characters) (clause 1, clause 43 of the Instructions on the procedure for filling out a declaration for goods, approved by Decision of the Customs Union Commission dated May 20, 2010 N 257):

- 8 characters – code of the customs post that registered the TD;

- 6 characters – TD registration date (DD.MM.YY);

- 7 characters – TD number according to the order of registration from the beginning of the year with the customs authority.

Full TD number

consists of 4 blocks (27 characters). For example, TD number 10129052/290319/0010690/

14

.

The first three blocks are the same as in the Trade House Registration Number.

4th block

- this is information about the number of the commodity item on the main or additional sheet of the TD from column 32 (clause 30 of the Instructions on the procedure for filling out a declaration for goods, approved by Decision of the Customs Union Commission dated May 20, 2010 N 257).

See also:

- Setting up and filling out the document Generating purchase ledger entries during import

- How to quickly find the details of a payment order for customs VAT to be entered into the purchase book?

- New procedure for filling out a customs declaration in connection with the transition to a Unified Personal Account (VAT section from 23:03)

- Error in specifying the customs declaration number in the invoice

- How to fill out column 15 of the purchase book when importing from foreign countries in 1C, if delivery is included in the cost of goods?

- How to fill out column 15 of the purchase book when importing from foreign countries into 1C?

- Import to non-CIS countries

- Import to the EAEU

- Purchasing services (works) from foreigners

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

- How to quickly find the details of a payment order for customs VAT to be entered into the purchase book? You need to edit the document Formation of purchase ledger entries manually...

- Setting up and filling out the document Formation of purchase book entries during import By default, the document Formation of purchase book entries is not reflected...

- Customs declaration number in the purchase book Customs declaration number for those who have never...

- Why are invoices from the current quarter not included in the purchase ledger? You do not have access to view. To gain access: Complete...

Do I need to fill out column 7 of the purchase book?

Column 7 of the purchase book must be filled out in cases where payment of tax is a prerequisite for deducting VAT (subparagraph “k”, paragraph 6 of Appendix 4 to Resolution No. 1137).

The list of such cases is limited. In particular, in column 7 it is necessary to reflect the payment details for the import of imported goods (when the buyer pays VAT at customs) (letter of the Ministry of Finance of Russia dated No. 03-07-11/15889).

The right to deduct VAT accrued on advances does not depend on the fact of payment of the tax. It arises from the seller at the time of shipment of goods on account of a previously received advance payment (clause 8 of Article 171, clause 6 of Article 172 of the Tax Code of the Russian Federation). Therefore, there is no need to transfer the payment details for prepayment from column 5 of the advance invoice to column 7 of the purchase book.

Information from documents

You can apply a deduction for import VAT if the goods are registered, are subject to use in taxable activities and you have documents in your hands confirming the payment of VAT and the actual import of goods. 2 tbsp. 171, paragraph 1, art. 172 of the Tax Code of the Russian Federation. We included the columns of the purchase book, where you need to indicate the details of the documents necessary to reflect the VAT deduction, in the first block. Depending on which country the goods are imported from, you will need a different set of such documents.

SITUATION 1. Goods were imported from countries outside the EAEU

In this case, to apply the VAT deduction and correctly fill out columns 3 and 7 of the purchase book, you will need para. 2 subp. "e", para. 2 subp. “k” clause 6 of the Rules for maintaining a purchase book:

- declaration of goods. When declaring goods in electronic form, you will need to receive a paper copy of the declaration Letter of the Ministry of Finance dated No. 03-07-15/31200 (Letter of the Federal Tax Service dated No. GD-4-3/ sent for information and use by inspectors);

- a document confirming the actual payment of VAT to the customs authority. What is it about? About the payment. But there are a number of nuances here.

ATTENTION

To reflect the deduction of “customs” VAT, the importer does not have to indicate the goods declaration number in column 13 of the purchase book.

Typically, VAT is transferred to the customs authority in advance (or to the advance BCC as part of other advance payments, or to a special BCC for VAT). However, such an advance in itself is not considered payment of tax. And only from the moment of submitting a declaration for goods to the customs authority, which will become your order to send the transferred amounts to pay tax on specific imported goods, will it be possible to talk about the actual payment of VAT. 1, 3 tbsp. 73 TK TS; pp. 1, 3 tbsp. 121 of Law No. 311-FZ (hereinafter referred to as Law No. 311-FZ).

Data on which payment order was used to transfer the amount used to pay VAT is in column B “Calculation details” of the goods declaration, sub. 46 p. 15 Instructions, approved. By decision of the CU commission dated No. 257. You will need to indicate the details of this payment order (and possibly also payment slips if, say, you had balances of unspent advances) in column 7 of the purchase book.

The Ministry of Finance, however, has repeatedly indicated that the document confirming the actual payment of VAT, as referred to in the Rules for maintaining a purchase ledger, is a confirmation issued by customs for the payment of customs duties and taxes, Appendix No. 1 to the FCS Order No. 2554; Letters from the Ministry of Finance from No. 03-07-08/33992, from No. 03-07-08/44735, from No. 03-07-08/252. Moreover, once financiers even noted that the deduction can be claimed only after receiving this document Letter from the Ministry of Finance dated No. 03-07-08/29571. The customs office issues a confirmation at the request of the payer of customs duties. 4 tbsp. 117 of Law No. 311-FZ.

The confirmation contains information as of a certain date, in particular, on which declarations, in what amount and by which payment method VAT was paid for the period of time specified in your application (not exceeding 3 years). That is, this document may contain data on the payment of VAT not only in relation to the declaration you are currently interested in. And it would be at least uninformative to enter the details of the confirmation itself in column 7. Here you need to reflect the number and date of the payment, which are indicated in the confirmation in relation to the declaration of goods you are interested in.

Here are the recommendations for filling out column 7 of the purchase book we received from the Ministry of Finance.

FROM AUTHENTIC SOURCES

LOZOVAYA Anna Nikolaevna Head of the Indirect Taxes Department of the Department of Tax and Customs Tariff Policy of the Ministry of Finance of Russia

“In column 7 of the purchase book, the importer has the right to indicate the details of the payment order confirming the transfer of funds to pay VAT to the customs authority. At the same time, in order to avoid disagreements with the tax authorities about the legality of applying a tax deduction on imported goods, the importer should obtain confirmation from the customs authority about the payment of customs duties in writing.”

ADVICE

If you are sure that your data matches the customs data, as they say, a penny is a penny, then fill out the purchase book based on the goods declaration. But in parallel, just in case, ask the customs office for confirmation of payment of customs duties and taxes. By the way, if you transferred an advance payment to the customs authority, then we advise you to ask at the same time for a report on the expenditure of funds contributed as advance payments, Appendix No. 2 to FCS Order No. 2554. The customs must provide a report within 30 days after receiving your application. 5 tbsp. 121 of Law No. 311-FZ.

Another subtle point is the payment of VAT by the customs representative (the so-called broker). The customs representative may pay the duties and taxes provided for by the customs procedure instead of the declarant, if this is provided for by the terms of the agreement concluded between the declarant and the customs representative. 5 tbsp. 60 Law No. 311-FZ; clause 3 art. 12 TK TS.

A customs representative is an organization included in a special register that carries out customs operations on behalf and on behalf of the declarant (or other interested party) subclause. 34 clause 1 art. 4, Art. 12 TK TS.

In this case, the declarant, as a rule, first transfers money to the broker to pay customs duties. The agreement with the customs representative also often provides that in the event of a shortage of the listed payments, the broker pays additional customs duties (including VAT) at his own expense, with subsequent compensation for these amounts by the importer. What payment details should the importer indicate in the purchase book: his own (to transfer money to the broker) or the broker’s (to pay “customs” VAT)?

The Rules for Maintaining a Purchase Book speak of a document confirming the actual payment of VAT to the customs authority. A payment to the customs representative is not suitable for this role. Therefore, in column 7 of the purchase book, you need to indicate the details of the document with which the broker transferred the money used to pay VAT. This data will be in column B “Calculation details” of the goods declaration, and in confirmation of payment of customs duties and taxes. The broker will probably provide you with a copy of this payment slip when reporting for the work performed.

FROM AUTHENTIC SOURCES

“If VAT on imported goods was paid by the customs representative, then the importer has the right to indicate in column 7 of the purchase book the details of the payment order confirming the transfer by the customs representative of funds to the customs authority for the payment of VAT. Payment documents for the transfer of funds by the importer to the customs representative for payment of customs duties do not need to be reflected in the purchase book. But if necessary, the importer will have to provide such documents to the tax authority.”

LOZOVAYA Anna Nikolaevna Ministry of Finance of Russia

Another difficult situation is the import of goods with the participation of an intermediary acting on his own behalf.

In this case, it is the commission agent (agent) who will file a declaration for the goods and pay VAT to the customs authority. But the deduction will be due to the importer - the principal (principal).

The Ministry of Finance, considering the situation with the payment of VAT at customs by an agent, explained that in this case, a VAT deduction can be applied on goods accepted for registration on the basis of:

- documents confirming payment of tax by the agent;

- customs declaration (its copy) for imported goods, received from the agent Letter of the Ministry of Finance dated No. 03-07-08/68143.

The details of these documents must be indicated in columns 3 and 7 of the purchase book.

In addition, financiers believe that an agreement is also necessary providing for the payment of tax by an intermediary with subsequent compensation for these amounts. Letter from the Ministry of Finance dated No. 03-07-08/297. At the same time, the Ministry of Finance does not speak about the fact of compensation of expenses as a necessary condition for deduction.

And even if by the time import VAT is reflected in the purchase book you already have a payment in hand to reimburse the intermediary’s expenses for paying VAT to the customs authority, indicating its details in column 7 will be unnecessary.

ADVICE

Ask the intermediary to request proof of payment of duties and taxes from customs. At your request, customs will not provide this document, because it was the intermediary who was the payer of customs duties.

SITUATION 2. Goods were imported from the EAEU countries - Belarus, Kazakhstan, Armenia and Kyrgyzstan

In this case, columns 3 and 7 of the purchase book must be filled out on the basis of para. 3 subp. "e", para. 3 subp. “k” clause 6 of the Rules for maintaining a purchase book:

- statements on the import of goods and payment of indirect taxes with a tax mark on payment of VAT, Appendix 1 to the Protocol on the exchange of information dated. If the application was submitted electronically, the tax office will also send an electronic message confirming the payment of VAT. In this case, there is no need to apply for a “paper” payment stamp. Letter from the Federal Tax Service dated No. ZN-4-17/;

- bills for payment of import VAT.

If you have an overpayment, you can offset it against the payment of import VAT. 2 clause 20 of Appendix No. 18 to the Treaty on the Eurasian Economic Union (signed in Astana). In this case, in the purchase book, register the decision to offset the amount of overpaid (collected) tax.

Filling out a purchase book when importing goods into the Russian Federation

The Russian Ministry of Finance provided clarification on how to indicate in column 15 of the purchase book the cost of goods imported into the Russian Federation. According to the financial department, it should reflect the customs value of imported goods, increased by the amount of customs duties, excise taxes on excisable goods and the amount of VAT.

Filling out a purchase book when importing goods into the Russian Federation

The procedure for filling out the purchase book in this case is as follows:

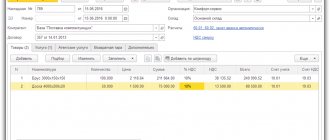

— in column 2 “Operation type code” of the purchase book, the transaction type code 19 (when importing goods from the territories of EAEU member countries) or 20 (when importing goods from the territories of third countries) is entered (Letter of the Federal Tax Service of Russia dated January 22, 2015 N GD-4 -3/ [email protected] , and from 07/01/2016 - Order of the Federal Tax Service of Russia dated 03/14/2016 N ММВ-7-3/ [email protected] ).

The ASK VAT-2 program will immediately begin to compare the amount of VAT accepted for deduction and reflected in column 16 of the purchase book with the database of the Federal Customs Service of Russia;

- in column 3 “Number and date of the seller’s invoice” of the purchase book, you must reflect the number and date of the application for the import of goods and payment of indirect taxes with marks from the tax authorities on the payment of value added tax (when imported from the territories of the EAEU member countries) and the number customs declaration for goods imported into the territory of the Russian Federation (when imported from third countries) (clause “e” of clause 6 of the Rules for maintaining a purchase book, approved by Decree of the Government of the Russian Federation of December 26, 2011 N 1137).

According to the planned amendments by the Federal Tax Service of Russia to the Decree of the Government of the Russian Federation of December 26, 2011 N 1137, column 3 of the purchase book will be filled out by the first importer. In a situation where a taxpayer purchases an imported product and receives an invoice, the customs declaration number must be indicated in column 13 of the purchase book. Only the first importer will indicate the customs declaration number in column 3 of the purchase book;

— columns 4, 5, 6 of the purchase book are not filled in in this case;

— column 7 “Number and date of the document confirming payment of tax” of the purchase book must be filled out, indicating the details of the documents confirming the actual payment of value added tax (clause “k” of clause 6 of the Rules for maintaining the purchase book, approved by the Decree of the Government of the Russian Federation of December 26. 2011 N 1137).

Documents confirming the actual payment of VAT are payment orders from the importer himself, confirming the transfer of funds to pay VAT to the customs authority; a payment order confirming the transfer by the customs representative of funds to the customs authority for the payment of VAT (payment documents for the transfer of funds by the importer to the customs representative for the payment of customs duties do not need to be reflected in the purchase book), as well as confirmation issued by the customs authority of the payment of customs duties and taxes (Appendix No. 1 to Order of the Federal Customs Service of Russia dated December 23, 2010 N 2554, Letters of the Ministry of Finance of Russia dated May 22, 2015 N 03-07-08/29571, dated June 11, 2015 N 03-07-08/33992, dated October 24, 2013 N 03-07-08 /44735, dated 08/05/2011 N 03-07-08/252). The customs authority issues a confirmation at the request of the payer of customs duties (clause 4 of article 117 of the Federal Law of November 27, 2010 N 311-FZ “On customs regulation in the Russian Federation”).

When filling out column 7, you must keep in mind that in the case of importing goods from EAEU member countries, it is possible to offset the overpayment of tax against the payment of “import” VAT. In accordance with paragraphs. 2 clause 20 of Appendix No. 18 to the Treaty on the Eurasian Economic Union (signed in Astana on May 29, 2014) if the taxpayer has overpaid (collected) amounts of taxes, fees or amounts of indirect taxes subject to refund (offset), as for imports goods into the territory of one Member State from the territory of another Member State, and when selling goods (work, services) on the territory of a Member State, the tax authority, in accordance with the legislation of the Member State into whose territory the goods were imported, accepts (takes out) a decision on their offset against the payment of indirect taxes on imported goods. In this case, a bank statement (its copy) confirming the actual payment of indirect taxes on imported goods is not presented. In this case, in column 7 of the purchase book, you must indicate the number and date of the decision to offset the amount of overpaid (collected) tax;

— column 8 “Date of registration of goods (work, services), property rights” of the purchase book must also be filled out;

— in column 9 “Name of the seller” of the purchase book, you must indicate the name of the foreign seller in accordance with the foreign trade contract (not the name of the taxpayer himself, and not the name of the customs authority, and not the name of the customs broker). But even if the taxpayer indicated the customs authority in column 9, this is not an error, since the information from column 9 of the purchase book is not uploaded to section. 8 VAT return;

— column 10 of the purchase book is not filled in when importing goods, since the foreign seller does not have an INN/KPP (clause 7 of the Rules for maintaining a purchase book, approved by Decree of the Government of the Russian Federation of December 26, 2011 N 1137). No foreign tax numbers of foreign sellers (for example, BIN in Kazakhstan, UNP in the Republic of Belarus, etc.) are TIN/KPP from the point of view of Russian tax legislation;

— columns 11, 12 “Information about the intermediary (commission agent, agent)” of the purchase book are not filled out, even if the goods were imported into the territory of the Russian Federation with the participation of an intermediary. This is because information about the intermediary is transferred from the purchase ledger to the VAT return for the purpose of matching data from intermediaries, sellers and buyers. In the case of import of goods from abroad by an intermediary, control, since there is no supplier invoice that the commission agent (agent) would reissue to the principal (principal);

— Column 13 “Customs declaration number” of the purchase book is filled in if the buyer purchases goods according to an invoice, i.e. when purchasing imported goods from a Russian supplier (that is, only for subsequent resale). Therefore, if an organization has received an invoice that contains customs declaration numbers, then column 13 of the purchase book must be filled out. When filling out this column, you need to take into account the limitation - up to 1000 character spaces in the CCD numbers, i.e. the taxpayer must use as many symbols as fit, and will have to provide explanations regarding information that does not fit when he receives a request from the tax authority;

— column 14 “Name and currency code” of the purchase book is filled out at the discretion of the taxpayer;

- in column 15 “Cost of purchases according to the invoice, the difference in cost according to the adjustment invoice (including VAT) in the currency of the invoice” of the purchase book, the customs value of imported goods is indicated, increased by the amount of customs duties, excise taxes and VAT (that is, it is indicated tax base for VAT, increased by the amount of tax), in rubles. In this case, column 14 of the purchase book is not filled in.

At the same time, the importer has the right to fill out column 15 in currency. To do this, you need to convert the paid VAT into foreign currency. And then in column 14 of the purchase book you must indicate the name and code of the foreign currency in which the amount from column 15 is expressed (clause “c” of clause 6 of the Rules for maintaining the purchase book, approved by Decree of the Government of the Russian Federation of December 26, 2011 N 1137). When importing goods from the EAEU countries, in column 15 of the purchase book, you can indicate the ruble amount of columns 15 and 20 of the application for the import of goods (clause 3 of Appendix 2 to the Protocol of December 11, 2009 “On the exchange of information in electronic form between the tax authorities of the member states of the Eurasian Economic Union on the paid amounts of indirect taxes"). In this case, column 14 of the purchase book also does not need to be filled out. And if the importer wishes to fill out column 15 of the purchase book in foreign currency, the rate from column 8 of the application for the import of goods can be used for conversion.

Let us note that the norms of the Government of the Russian Federation of December 26, 2011 N 1137 do not stipulate what information should be reflected in column 15 of the purchase book regarding the cost of imported goods. But column 15 of the purchase book is mandatory, so you can indicate in it such background information as the customs value of the goods, which was determined by the customs authority;

— in column 16 “VAT amount on the invoice, the difference in the VAT amount on the adjustment invoice, accepted for deduction, in rubles and kopecks” of the purchase book, the ruble amount of VAT is reflected, that is, the amount that was paid at customs, but only in the part that the taxpayer will claim as a deduction and reflect in section. 3 VAT returns. It can be taken from the goods declaration (or application for the import of goods).

Making changes to the purchase book

Making changes to the purchase book

If you need to make changes to the purchase book, proceed in the following order.

If you need to adjust data for the current period (before the end of the quarter), make correction entries directly in the purchase ledger. To do this, indicate the cost and tax amount of the canceled invoice with a minus sign, and enter the indicators of the new (corrected) invoice with positive values.

If the seller (executor) corrects invoices for past tax periods, then draw up an additional sheet to the purchase book for the period in which the original invoice was registered. The form of the additional sheet is given in Appendix 4 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137. In this additional sheet, the original invoice must be canceled (register its indicators with a minus sign). Register the corrected invoice in the purchase book (with a positive value) in the period when the organization has the right to a tax deduction.

This procedure follows from the provisions of paragraphs 4 and 9 of Section II of Appendix 4 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

If changes made to the purchase book reduce the amount of the previously declared VAT deduction, an updated tax return for the corresponding period must be submitted to the inspectorate (Federal Tax Service of Russia dated November 5, 2014 No. ГД-4-3/22685).

If, as a result of the adjustment, the amount of the previously declared VAT deduction increases, then the organization has a choice:

- submit an updated declaration for the relevant period (a right, not an obligation). In this case, it will be necessary to prepare an additional sheet to the purchase book for the period in which the original invoice was recorded;

- claim a deduction in the current period (within three years). In this case, make entries only in the purchase book for the reporting period;

- do nothing (for example, if the deduction amount is insignificant).

This follows from the provisions of paragraph 3 of paragraph 1 of Article 54, paragraph 2 of paragraph 1 of Article 81, paragraph 1.1 of Article 172 of the Tax Code of the Russian Federation.

Purpose of the book

The purchase ledger is a tax accounting register whose purpose is to register invoices received from sellers with input VAT. It is filled out by the company purchasing the products as these papers are received and attached to the declarations at the time of their submission to the tax office.

Reflection of an adjustment invoice in the purchase ledger can have either a positive or negative value.

For products for which a VAT tax deduction is provided, taking into account payment, in case of incomplete payment, it is necessary to make as many entries as the number of transfers were made.

If there is a need to cancel an entry that was made for previous periods, you will need to fill out an additional sheet of the purchase ledger for the corresponding period. Add. sheets are an important part of this register.

Information about counterparties (seller, intermediary)

In this block we have included columns that are intended to indicate the names and TIN/KPP of the seller (columns 9 and 10) and the intermediary.

In column 9 you must indicate the name of the foreign supplier. Some importers indicate here, for example, the name of the customs office or customs broker. It is not right. But not critical. Information from column 9 of the purchase book about the name of the seller is not transferred to section 8 of the declaration. Therefore, even if you filled out column 9 incorrectly, this will not affect the verification of the declaration in any way.

Column 10 should remain blank. 7 Rules for maintaining a purchase book. Here you can only indicate your tax identification number and checkpoint. And UNP and other foreign tax numbers of suppliers are not INN/KPP from the point of view of Russian tax legislation. And you shouldn’t try to fit them into the TIN format by adding zeros at the beginning. The program will not allow such a pseudo-TIN.

Columns 11 and 12 do not need to be filled out. Even if you used an intermediary. The Ministry of Finance confirmed this to us.

FROM AUTHENTIC SOURCES

“Since we are talking about deducting VAT on imported goods, regardless of the fact that the goods are imported with the participation of an intermediary, information about him in columns 11 and 12 of the purchase book does not need to be indicated. And in column 2 of the purchase book you should indicate code 19 or 20.”

LOZOVAYA Anna Nikolaevna Ministry of Finance of Russia

Indeed, information about the intermediary comes from the purchase ledger into the VAT return for the purpose of matching data coming from intermediaries, sellers and buyers. In the case of an intermediary importing goods from abroad, there is essentially nothing to control, since there is no supplier invoice that the commission agent (agent) would reissue to the principal (principal).