The ability to reconcile data from the income tax return with previously submitted reports, as well as with the VAT return, has been added to the Kontur.Extern service. You can compare data using the DAM form for different periods. The new feature will allow you to comply with control ratios and avoid mistakes that could lead to the accrual of penalties from the Federal Tax Service.

Ways to check your income tax return

If the organization is correctly registered in accordance with the law of the Russian Federation, it automatically becomes a taxpayer. This means that you are required to fill out a tax return for corporate income tax.

This type of document is provided based on the results of work during the reporting period. Some rent every month, others once every six months. To make it easier for an accountant to calculate this type of tax, tax officials have come up with methodological recommendations. They help in checking declarations.

There are two stages for checking a tax return for corporate income tax:

- the first stage is characterized by the fact that it is necessary to compare the tax return data with the accountant’s report, as well as with the returns for other taxes;

- the second stage is characterized by the fact that tax authorities will deal with why the company’s profits fell, but at the same time expenses increased.

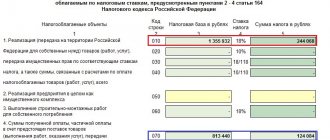

First, you need to equalize the revenue that is indicated in the income tax return with the VAT return. To do this, the values must match:

If there are discrepancies, tax officials may request that the company provide clarification. Or they will send their employee for a full check.

The next step is to check the following values:

In the case of a UST declaration, tax authorities will definitely check whether the organization justifiably removed payments to employees from expenses. Because of this, taxable profit decreases. To do this you need to check the following:

There is also an advertising tax, which the tax office will definitely check:

There will be a mandatory reconciliation with the accountant’s report, namely with forms 2 and 5 (only small institutions do not fill it out). To do this you need to compare:

It is advisable that the company does not have any discrepancies in the following operations:

If these indicators do not match, the company engages in any transactions using securities, uses market prices for exchange or non-paid transactions, also when the company’s prices are in dollars.

Tax inspectors will also analyze the following indicators:

When a company charges depreciation exactly the same in the accounting and tax statements, then the following relationship will work:

When checking a profit declaration, it is necessary to check the correctness of the values inside it. To do this, the following relationships are checked:

Whose responsibility is it to check the declarations?

Of course, first of all, this is the direct responsibility of your Federal Tax Service. Desk audits, within the framework of which the declarations submitted by you are confirmed, are one of the areas of activity of the tax authorities, their labor function.

Read more about cameras here.

But the taxpayer himself is also interested in checking tax reporting. Preliminary control makes it possible to avoid inaccuracies and errors, which, in turn, makes it possible to reduce the degree of attention paid to it by tax authorities. Therefore, it is important for everyone who interacts with controllers along the reporting line to know not only the rules for filling out declarations, but also to have information and tools suitable for checking them.

You will learn from this material what a declaration is, how it differs from an advance payment, as well as the peculiarities of submitting it to the Federal Tax Service.

Second stage of declaration verification

In order to know how to check an income tax return, tax officials have made the work of entrepreneurs a little easier. There is a verification method.

At the second stage, an economic analysis is carried out. As a rule, this stage is carried out for reputable companies that have large profits. So small firms can calm down after the first stage.

This analysis is carried out by comparing tax and accounting reports currently and the three previous years. If violations are detected, no fines will be assessed, but an inspection will definitely come to the company.

Growth rates of expenses and income

Tax officials will not like the discrepancy between the growth rate of expenses compared to the growth rate of income according to tax reporting data and the growth rate of expenses compared to the growth rate of income reflected in the financial statements. In this case, you will be a candidate for an on-site inspection (clause 4 of the Public Criteria). As a rule, the dynamics of this indicator are looked at over several periods.

Of course, there may be reasonable explanations for the discrepancies in growth rates. For example: worn-out equipment required expensive repairs or the purchase of a new one, a sharp increase in the price of goods and materials, etc.

Important points to consider

Each organization must submit an income tax return, the form of which can be found in the public domain. The company itself can choose how to submit its income tax return. Its form can be different: written form, which is made in duplicate, by mail with a complete list of attachments, or electronically.

If a company does not submit a declaration on time, a fine of 1,000 rubles will be imposed. when paying tax but not submitting an annual report; if the company has not paid the tax - 5% of its amount, but not less than 1,000 rubles.

When a company’s indicators do not match, the tax officials themselves indicate in their methodological materials that this may be due to a change in production technology. But in order not to look for any loopholes, try to fill out the declaration correctly so as not to have to check it later.

Stage 4 – calculation of the amount of conditional income/tax expense (based on BU 99 turnover for the month)

In fact, at this stage we determine how much tax we would pay if we calculated it only according to accounting data.

The tax amount is calculated as (TurnoverKt_BU_99_01_1 – TurnoverDt_BU_99_01_1)*Profit Tax Rate

Dt 68.04.2 – Kt 99.02.2 – if the tax amount is positive

Dt 99.02.1 – Kt 68.04.2 – if the tax amount is negative

After this stage, document postings are recorded so that the movements are taken into account in the next calculation stage.

General provisions on desk audits

Let us recall the main provisions of Art. 88 of the Tax Code on conducting desk tax audits. Thus, a desk tax audit is carried out at the location of the tax authority based on:

- tax returns;

- documents serving as the basis for the calculation and payment of tax, which were submitted by the taxpayer;

- other documents on the activities of the taxpayer available to the tax authority.

If, as a result of an audit, errors in filling out or discrepancies in indicators are revealed in the submitted documents, the taxpayer must be informed about this and required to make appropriate corrections within a specified period.

When conducting a desk audit, the tax authority has the right to demand from the taxpayer additional information, as well as explanations and documents that would confirm the correctness of calculation and timely payment of taxes.

Report “Analysis of the state of accounting”

The Accounting Status Analysis report is located in the Reports -> Accounting Status Analysis menu.

By going to the settings menu (Settings button), the accountant can select on the Settings tab the four types of checks provided for by the report:

- Analyze the working chart of accounts;

- Analysis of accounts to be closed;

- Analysis of accounting results;

- Analysis of accounting entries.

By default, all four types of checks are performed, but since a full analysis takes a long time, you can disable those that are not required.

The user can make adjustments to the standard settings for recognizing transactions as “invalid” - the Invalid transactions tab (Fig. 1).

Rice. 1

The Dt column indicates the debit account of the unacceptable entry, and the Kt column indicates the credit account. In the column DtExclusion and KtExclusion, you can specify accounts that are excluded during verification.

For example, if the account “01” is indicated in the Dt column, and “01, 08, 79, 83” is indicated in the KtException column, this means that all transactions on the debit of account 01 are incorrect, if the corresponding account is not the account from the list “01, 08, 79, 83."

The Comment column stores an explanation of the comment to the transaction. If the program detects an invalid posting, the text from the Comment column will be displayed in the report.

The Standard Accounting System tab displays the standard self-supporting chart of accounts, which is used to analyze the correctness of maintaining the user's chart of accounts. The user should not change the information on this tab.

The settings made by the user are saved using the OK button.

To perform the selected checks, click the Generate button.

If there are errors in any section of the report, by double-clicking on the line with the error, you can call up an account card or transaction form with the erroneous posting.

Let's take a closer look at each of the four types of checks provided for in the report.

Analyze the working chart of accounts

The program compares the working chart of accounts with the reference chart of accounts recommended by. Information about the reference chart of accounts is presented on the Reference Chart of Accounts tab of the report settings menu.

If the required account is not found in the chart of accounts, or the account's activity status has been changed, warnings will be issued. The structure of analytical accounting on the accounts involved in the algorithms for compiling regulated reporting forms is also checked.

Analysis of accounts to be closed

The accounting results at the end of the reporting period are checked. If accounts to be closed at the end of the reporting period have balances, information about such accounts is provided.

For example, they should not have a balance on the account as a whole at the end of the period of accounts 25 “General production expenses”, 26 “General expenses”, 90 “Sales”, 91 “Other income and expenses”.

The balance on such accounts is checked, and if it is detected, the report displays a message about the account number, the account balance with an explanation of the essence of the error.

Analysis of accounting results

In the process of analyzing accounting results, the following are revealed:

- erroneous balances on accounting accounts (highlighted in red in the program);

- errors in maintaining quantitative accounting (lack of balance in quantity or amount in the corresponding accounts);

- errors in the revaluation of foreign currency at the end of the reporting period (for the correct operation of this section, it is necessary to set the exchange rate at the end of the reporting period).

Let us recall that one of the characteristics of the account (subaccount) of the chart of accounts is the attribute of the account in relation to the balance sheet. In accounting, according to this characteristic, all accounts are divided into active, passive and active-passive. For example, account 01 “Fixed assets” is active, account 63 “Provisions for doubtful debts” is passive, and account 68 “Calculations for taxes and fees” is active-passive.

For active and passive accounts, compliance of the balance with the final account characteristic is monitored (on an active account, the balance should be in debit, and in a passive account, in credit).

In the 1C:Accounting 8 program, one of the operations for analyzing accounting results is to check the implementation of this rule. If this is the case, the report shows which accounts have balances that do not match the account attribute.

Accounting for inventories in the program is carried out not only in monetary terms, but also in kind. For example, such accounting is provided for in account 41 “Goods”. Accounts that support quantitative accounting are marked with a check mark in the Quantity column in the chart of accounts.

A check is performed to ensure the correctness of the balances on such accounts. It is considered an error if, for an object of analytical accounting, such an account has a “total” balance, but no quantitative balance, and vice versa: there is a balance in physical terms, but it has zero value.

For organizations that have assets and liabilities whose value is denominated in foreign currency, it is useful to check whether their valuation is correct at the end of the reporting period.

To prepare financial statements, the value of these assets and liabilities must be converted into rubles at the exchange rate in effect on the reporting date. Accounts with the sign of supporting currency accounting in the chart of accounts are marked with a checkmark in the Val column.

The routine operation Revaluation of currency funds recalculates the balances on these accounts and assigns the resulting exchange rate differences to other income or expenses. The program checks whether, at the time of performing a regulatory operation to revaluate assets and liabilities expressed in foreign currency, the current exchange rate is loaded into the database.

Analysis of accounting entries

The result of this check is a list of “suspicious” transactions from the point of view of the program. The criterion for suspicion is the list of invalid transactions presented in the report settings, on the Invalid transactions tab. If an invalid posting is detected, the program will display an error line, which will indicate which correspondence aroused suspicion and a short comment will be given.

If the organization's accounting policy for individual accounts provides for additional offsetting accounts that “expand the list of exceptions,” they must be added to the list before performing the analysis.