When was the BCC for insurance premiums last updated?

The last update of the BCC on insurance premiums took place on April 14, 2019.

Nothing else has changed yet, and these same BCCs will be in effect in 2021. But let's go in chronological order. Since 2021, the bulk of insurance premiums (except for payments for accident insurance) began to be subject to the provisions of the Tax Code of the Russian Federation and became the object of control by the tax authorities. As a result of these changes, in most aspects, insurance premiums were equated to tax payments and, in particular, received new, budgetary BCCs.

The presence of a situation where, after 2021, contributions accrued according to the old rules can be transferred to the budget, required the introduction of special, additional to the main, transitional BCCs for such payments.

As a result, from 2021, there are 2 BCC options for insurance premiums supervised by the Federal Tax Service: for periods before December 31, 2021 and for periods after January 2021. At the same time, the codes for contributions to accident insurance that remain under the control of the Social Insurance Fund have not changed.

From April 23, 2018, the Ministry of Finance introduced new BCCs for penalties and fines on additional tariffs for insurance premiums paid for employees entitled to early retirement. KBK began to be divided not by periods: before 2017 and after - as before, but according to the results of a special labor assessment.

From January 2021, BCC values were determined in accordance with Order of the Ministry of Finance dated June 8, 2018 No. 132n. These changes also affected codes for penalties and fines on insurance premiums at additional tariffs. If in 2021 the BCC for penalties and fines depended on whether a special assessment was carried out or not, then at the beginning of 2021 there was no such gradation. All payments were made to the BCC, which is established for the list as a whole.

However, from April 14, 2019, the Ministry of Finance returned penalties and fines for contributions under additional tariffs to the 2021 BCC.

In 2021, the list of BCCs is determined by a new order of the Ministry of Finance dated November 29, 2019 No. 207n, but it has not changed the BCC for contributions.

KBK taxes: for paying taxes for organizations and individual entrepreneurs on OSN

| Name of tax, fee, payment | KBK |

| Corporate income tax (except for corporate tax), including: | |

| — to the federal budget (rate — 3%) | 182 1 0100 110 |

| — to the regional budget (rate from 12.5% to 17%) | 182 1 0100 110 |

| VAT | 182 1 0300 110 |

| Property tax: | |

| - for any property, with the exception of those included in the Unified Gas Supply System (USGS) | 182 1 0600 110 |

| - for property included in the Unified State Social System | 182 1 0600 110 |

| Personal income tax (individual entrepreneur “for yourself”) | 182 1 0100 110 |

KBK taxes: for paying taxes for organizations and individual entrepreneurs in special modes

| Name of tax, fee, payment | KBK |

| Tax under the simplified tax system, when the object of taxation is applied: | |

| - “income” | 182 1 0500 110 |

| — “income minus expenses” (tax paid in the general order, as well as the minimum tax) | 182 1 0500 110 |

| UTII | 182 1 0500 110 |

| Unified agricultural tax | 182 1 0500 110 |

| Name of tax, fee, payment | KBK |

| Personal income tax on income the source of which is a tax agent | 182 1 0100 110 |

| VAT (as tax agent) | 182 1 0300 110 |

| VAT on imports from Belarus and Kazakhstan | 182 1 0400 110 |

| Income tax on dividend payments: | |

| — Russian organizations | 182 1 0100 110 |

| - foreign organizations | 182 1 0100 110 |

| Income tax on the payment of income to foreign organizations (except for dividends and interest on state and municipal securities) | 182 1 0100 110 |

| Income tax on income from state and municipal securities | 182 1 0100 110 |

| Income tax on dividends received from foreign organizations | 182 1 0100 110 |

| Transport tax | 182 1 0600 110 |

| Land tax | 182 1 06 0603х хх 1000 110 where xxx depends on the location of the land plot |

| Fee for the use of aquatic biological resources: | |

| — for inland water bodies | 182 1 0700 110 |

| — for other water bodies | 182 1 0700 110 |

| Water tax | 182 1 0700 110 |

| Payment for negative impact on the environment | 048 1 12 010x0 01 6000 120 where x depends on the type of environmental pollution |

| Regular payments for the use of subsoil, which are used: | |

| - on the territory of the Russian Federation | 182 1 1200 120 |

| — on the continental shelf of the Russian Federation, in the exclusive economic zone of the Russian Federation and outside the Russian Federation in territories under the jurisdiction of the Russian Federation | 182 1 1200 120 |

| MET | 182 1 07 010хх 01 1000 110 where хх depends on the type of mineral being mined |

| Corporate income tax on income in the form of CFC profits | 182 1 0100 110 |

KBC for payment of insurance premiums for employees from 01/01/2017

| TAX | KBK |

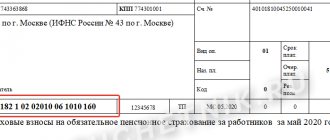

| Insurance contributions for pension insurance to the Pension Fund for employees for the payment of the insurance and funded part of the labor pension | 182 1 02 02010 06 1010 160 |

| Insurance contributions to the Pension Fund at an additional rate for insured persons employed in hazardous conditions according to List 1, for the payment of the insurance part of the labor pension | 182 1 02 02131 06 1010 160 |

| Insurance contributions to the Pension Fund at an additional rate for insured persons engaged in heavy types of work on list 2, for payment of the insurance part of the labor pension | 182 1 02 02132 06 1010 160 |

| Insurance contributions to the FFOMS for employees | 182 1 02 02101 08 1013 160 |

| Insurance contributions to the Social Insurance Fund for employees for compulsory social insurance in case of temporary disability and in connection with maternity | 182 1 02 02090 07 1010 160 |

KBK: Payment of taxes, contributions, fees Help

The budget income classification code (KBK) consists of 20 digits and includes:

- 1 - 3 digits of code

The chief administrator code (1 - 3 digits of the budget revenue classification code of the Russian Federation) consists of 3 characters and corresponds to the number assigned to the administrator of budget revenues, in accordance with the legislation of the Russian Federation, the legislation of the constituent entities of the Russian Federation and legal acts adopted by local governments .Administrators of budget revenues are:

- government authorities (including tax authorities),

- governing bodies of state extra-budgetary funds,

- Central Bank of the Russian Federation,

- budgetary institutions created by state authorities, local governments,

local government bodies,

exercising, in accordance with the established procedure, control over the correctness of calculation, completeness and timeliness of payment, accrual, accounting, collection and making decisions on the return (offset) of overpaid (collected) payments to the budget, penalties and fines on them.

As part of the budget process, budget revenue administrators monitor, control, analyze and forecast revenue from the relevant revenue source and submit revenue projections for the next financial year to the relevant financial authorities.

- 182 - Federal Tax Service

- 392 — Pension Fund of the Russian Federation

- 393 — Social Insurance Fund of the Russian Federation

- 048 — Federal Service for Supervision of Natural Resources

- 153 - Federal Customs Service...

A complete list of Codes for the chief administrators of budget revenues.

The income type code provides for the following groups:

- 1 - tax and non-tax revenues;

2 - gratuitous receipts.

The Income group includes the following subgroups:

- 01 - taxes on profits, income;

- 02 — insurance contributions for compulsory social insurance;

- 03 - taxes on goods (work, services) sold on the territory of the Russian Federation;

- 04 - taxes on goods imported into the territory of the Russian Federation;

- 05 — taxes on total income;

- 06 — property taxes;

- 07 - taxes, fees and regular payments for the use of natural resources;

- 08 - state duty;

- 09 - debt and recalculations for canceled taxes, fees and other obligatory payments;

- 10 - income from foreign economic activity;

- 11 - income from the use of property in state and municipal ownership;

- 12 — payments for the use of natural resources;

- 13 - income from the provision of paid services and compensation of state costs;

- 14 - income from the sale of tangible and intangible assets;

- 15 — administrative fees and charges;

- 16 - fines, sanctions, damages;

- 17 - other non-tax income.

The Income Type Item code further refines the Income Type Subgroup code.

The income type sub-Item code further refines the income type Item code.

Revenue elements code:

- For tax revenues, the code of the revenue element corresponds to the budget of the budget system of the Russian Federation, depending on the powers to set tax rates by federal authorities, authorities of constituent entities of the Russian Federation, authorities of municipalities in accordance with the legislation of the Russian Federation on taxes and fees.

For non-tax income, the code of the income element is determined depending on the authority to establish the amount of payments by federal authorities, authorities of constituent entities of the Russian Federation, authorities of municipalities, and management bodies of state extra-budgetary funds.

The following codes of income elements are established:

- 01 - federal budget;

- 02 — budget of a constituent entity of the Russian Federation;

- 03 - budgets of intra-city municipalities of federal cities of Moscow and St. Petersburg;

- 04 — budget of the city district;

- 05 - budget of the municipal district;

- 06 - budget of the Pension Fund of the Russian Federation;

- 07 - budget of the Social Insurance Fund of the Russian Federation;

- 08 - budget of the Federal Compulsory Medical Insurance Fund;

- 09 - budget of the territorial compulsory health insurance fund;

- 10 - settlement budget.

The Code of Subtypes of Budget Revenues (14 - 17 digits of the budget revenue classification code of the Russian Federation) consists of 4 characters.

The codes are detailed by the Ministry of Finance of the Russian Federation, financial authorities of the constituent entities of the Russian Federation, and financial authorities of local self-government.

The classification of income subtypes is coded with four characters.

For income from the collection of taxes, fees, regular payments for the use of subsoil (rentals), customs duties, customs fees and income from the collection of state duties. The subtype code is used for separate accounting of the amounts of tax (fee), penalties, monetary penalties (fines) for this tax (fee), therefore the taxpayer must independently select this code depending on the type of payment. At the same time, administrators of these incomes are obliged to inform payers of the full budget classification code in accordance with the following structure of the code for subtypes of income, in particular:

- 1000 - payment amount (recalculations, arrears and debt for the corresponding payment, including canceled ones);

2100 - fines;

Compulsory medical insurance: For insurance premiums for compulsory medical insurance of the working population, credited to the budget of the Federal Compulsory Medical Insurance Fund, it is carried out according to the budget income classification code 000 1 02 02101 08 0000 160 “Insurance premiums for compulsory medical insurance of the working population, credited to the budget of the Federal Compulsory Medical Insurance Fund medical insurance" the following codes of the subtype of budget income are used:

- 1011 - “Insurance contributions for compulsory health insurance of the working population, received from payers”;

- 1012 - “Insurance contributions for compulsory health insurance of the working population, previously credited to the budgets of territorial compulsory health insurance funds (for billing periods expired before January 1, 2012)”;

- 2011 — “Penalties on insurance premiums for compulsory health insurance of the working population, received from payers”;

- 2012 - “Penalties on insurance premiums for compulsory health insurance of the working population, previously credited to the budgets of territorial compulsory health insurance funds (for billing periods expired before January 1, 2012)”;

- 3011 - “Amounts of monetary penalties (fines) for insurance premiums for compulsory health insurance of the working population received from payers”;

- 3012 - “Amounts of monetary penalties (fines) for insurance premiums for compulsory health insurance of the working population, previously credited to the budgets of territorial compulsory health insurance funds (for billing periods expired before January 1, 2012).”

PFR: Administration of payments received by the budget of the Pension Fund of the Russian Federation in accordance with the Federal Law of April 30, 2008 No. 56-FZ “On additional insurance contributions for the funded part of the labor pension and state support for the formation of pension savings” from insured persons and employers reflected in the budget of the Pension Fund of the Russian Federation, carried out according to the budget income classification code 000 1 0200 160 “Additional insurance contributions for the funded part of the labor pension and employer contributions in favor of insured persons paying additional insurance contributions for the funded part of the labor pension, credited to the Pension Fund of the Russian Federation » using the following budget revenue subtype codes:

- 1100 - additional insurance contributions for the funded part of the labor pension, credited to the Pension Fund of the Russian Federation;

- 1200 - employer contributions in favor of insured persons who pay additional insurance contributions for the funded part of the labor pension, credited to the Pension Fund of the Russian Federation.

State registration: For the purpose of accounting for revenues administered by federal government bodies..., by type of budget income of income subgroups... 113 - income from the provision of paid services (work) and compensation of state costs,... the following codes of subtype of budget revenues are used: 6000 - federal government bodies... ( For example, Fee for providing information contained in the Unified State Register of Legal Entities, Unified State Register of Legal Entities, Unified State Register of Individual Entrepreneurs).

Complete list of budget income subtype codes.

The classification of operations of the general government sector related to budget revenues is determined by a three-digit code (18 - 20 digits of the code for the classification of budget revenues of the Russian Federation) of the classification of operations of the general government sector, which provides for the grouping of operations according to their economic content, and is represented by the following positions:

- 110 - tax revenues;

120 - income from property;

BCC for insurance premiums in 2021 for the Pension Fund of Russia

Payment of insurance premiums to the Pension Fund is carried out by:

- Individual entrepreneurs working without hired employees (for themselves);

- Individual entrepreneurs and legal entities hiring workers (from the income of these workers).

At the same time, payment of a contribution by an individual entrepreneur for himself does not exempt him from transferring the established amount of payments to the Pension Fund for employees and vice versa.

Individual entrepreneurs who do not have staff pay 2 types of contributions to the Pension Fund:

- In a fixed amount - if the individual entrepreneur earns no more than 300,000 rubles. in year. For such payment obligations in 2019-2020, KBK 18210202140061110160 (if the period is paid from 2017) and KBK 18210202140061100160 (if the period is paid until 2017) are established.

IMPORTANT! The income of an individual entrepreneur on UTII for the purpose of calculating fixed insurance premiums is imputed income, not revenue (letter of the Ministry of Finance of the Russian Federation dated July 18, 2014 No. 03-11-11/35499).

- In the amount of 1% of revenue that exceeds RUB 300,000. in year. For the corresponding payment obligations accrued before 2021, KBK 18210202140061200160 has been established. But contributions accrued in 2017–2020 should be transferred to KBK 18210202140061110160. That is, the code is the same as for the fixed part (letter from the Ministry of Finance of Russia dated 04/07/201 7 No. 02-05-10/21007).

Individual entrepreneurs and legal entities that hire employees pay pension contributions for them, accrued from their salaries (and other labor payments), according to KBK 18210202010061010160 (if accruals relate to the period from 2017) and KBK 18210202010061000160 (if accruals are made for the period before 2021) .

How to read the KBK of insurance contributions for pension insurance?

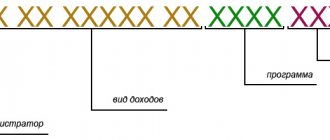

Like any other, the BCC of contributions to a pension fund includes twenty numbers, which are usually displayed as follows: XXX X XX XXXXX XX XXXX XXX. The code is divided into four groups, each of which has its own specific meaning:

- The first group is “Administrator”. It consists of 3 digits and indicates the department to which the payment is sent (the first three digits in the BCC of pension contributions are always 392, since its addressee is the Pension Fund)

- the second part of the code is “Variety of Income”. It consists of 10 numbers. The first digit of them shows the “Group” itself, so, for example, 1 means income, 2 means income on a non-refundable basis, 3 means income from business, and so on. The remaining numbers indicate “Subgroup”, “Article”, “Subarticle” and “Element”.

“Subgroup” is the two numbers following the group. “Article” is the seventh and eighth numbers, and sub-article is the signs from the ninth to the eleventh. “Element” shows the budget level, for example, federal or municipal. Or, for example, the budget of the Pension Fund.

KBK for payment of insurance contributions to the Pension Fund for employees

| TAX | KBK |

| Insurance contributions for pension insurance to the Pension Fund for employees for the payment of the insurance and funded part of the labor pension | 392 1 02 02010 06 1000 160 |

| Insurance contributions for pension insurance to the Pension Fund for employees for payment of the insurance part of the labor pension within the limit | 392 1 02 02140 06 1100 160 |

| Insurance contributions for pension insurance to the Pension Fund of the Russian Federation for employees to pay the insurance part of the labor pension in excess of the limit | 392 1 02 02140 06 1200 160 |

| Insurance contributions to the Pension Fund at an additional rate for insured persons employed in hazardous conditions according to List 1, for the payment of the insurance part of the labor pension | 392 1 02 02131 06 1000 160 |

| Insurance contributions to the Pension Fund at an additional rate for insured persons engaged in heavy types of work on list 2, for payment of the insurance part of the labor pension | 392 1 02 02132 06 1000 160 |

KBK for payment of penalties on insurance contributions to the Pension Fund for employees

| PENES, FINES | KBK | |

| Penalties, fines on insurance contributions for pension insurance to the Pension Fund for employees for the payment of the insurance and funded part of the labor pension | penalties | 392 1 02 02010 06 2100 160 |

| fines | 392 1 02 02010 06 3000 160 | |

| Penalties and fines on insurance contributions for pension insurance to the Pension Fund of the Russian Federation for employees to pay the insurance part of their labor pension within the limit | penalties | 392 1 02 02140 06 2100 160 |

| fines | 392 1 02 02140 06 3000 160 | |

| Penalties and fines on insurance contributions for pension insurance to the Pension Fund of the Russian Federation for employees to pay the insurance part of their labor pension in excess of the limit | penalties | 392 1 02 02140 06 2100 160 |

| fines | 392 1 02 02140 06 3000 160 | |

| Penalties and fines for insurance contributions to the Pension Fund of the Russian Federation at an additional rate for insured persons employed in hazardous conditions according to List 1, for the payment of the insurance part of the labor pension | penalties | 392 1 02 02131 06 2000 160 |

| fines | 392 1 02 02131 06 3000 160 | |

| Penalties and fines for insurance contributions to the Pension Fund of the Russian Federation at an additional rate for insured persons engaged in heavy types of work on list 2, for the payment of the insurance part of the labor pension | penalties | 392 1 02 02132 06 2000 160 |

| fines | 392 1 02 02132 06 3000 160 | |

How to calculate income under different tax regimes in 2021

In order to determine whether you need to pay something else for the past year to the Pension Fund of the Russian Federation or not, you need to calculate the income of the individual entrepreneur for the reporting period. If you apply only one tax regime, then there should be no problems. As a rule, by April individual entrepreneurs submit tax returns for the year, or at least they have already filled them out. In this case, the income of the individual entrepreneur, for the purpose of calculating insurance contributions to the Pension Fund in a fixed amount, is taken from the tax return:

- On OSNO - the amount in line 110 (clause 3.1) minus the amount in line 120 (clause 3.2) of sheet B

of the 3-NDFL declaration;

* - On OSNO - line 030 (clause 2.1) of sheet B of

the 3-NDFL declaration (KND Form 1151020); - On the simplified tax system - with the object of taxation Income (USN 6%) line 113 of Section 2.1.1

of the declaration; - On the simplified tax system - with the taxable object Income-expenses (15% simplified tax system), line 213 of Section 2.2

of the declaration; - On UTII - the sum of lines 100 of all Sections 2

of the declarations

for 2015

(we add up the amounts for these lines in the declarations for the 1st, 2nd, 3rd and 4th quarters); - On the Unified Agricultural Tax - line 010 of Section 2

of the declaration (Form according to KND 1151059); - On PSN - potential income - tax base (indicated in the patent).

if you don’t want disputes, you can use the previous option and pay extra fees:

If you apply the UTII regime in several municipalities at once, you need to add up the calculated income for all UTII declarations for the year in all municipalities.

If an individual entrepreneur has received several patents for different types of activities, or in different regions of Russia, it is necessary to sum up the potential income for all patents received during the year.

If you use several tax regimes simultaneously for different types of activities, then you need to add up the income from them. The resulting amount will be the total income, from which 300 thousand rubles must be subtracted. Compare the remaining amount with the 1% limit for 2015 or 2021. If the balance is less than the maximum contribution amount, divide it by 100. You will get the amount in rubles and kopecks, which must be transferred to the Pension Fund by April 1, 2016 (for 2015) or 2021 (for 2016) inclusive.

*

Taking into account the Resolution of the Constitutional Court of the Russian Federation of November 30, 2021 No. 27-P. Just don’t forget to first calculate the benefits, since you will have to pay additional personal income tax and pay tax penalties, as well as submit updated returns.

What BCCs for FFOMS contributions are established in 2021

Contributions to the FFOMS, as well as contributions to the Pension Fund, are paid by:

- IP - for yourself;

- Individual entrepreneurs and legal entities - for hired employees.

Contributions for individual entrepreneurs to the FFOMS are paid for themselves using BCC 18210202103081013160 (if related to the period from 2021) and BCC 18210202103081011160 (if related to the period until 2021).

For hired employees, individual entrepreneurs and legal entities must pay contributions to the Federal Compulsory Medical Insurance Fund using KBK 18210202101081013160 (for payments accrued from 2021) and KBK 18210202101081011160 (for accruals made before 2021).

KBK for payment of insurance premiums to the FFOMS for employees

| TAX | KBK |

| Insurance contributions to the FFOMS for employees | 392 1 02 02101 08 1011 160 |

KBK for payment of penalties on insurance premiums to the Federal Compulsory Compulsory Medical Insurance Fund for employees

| PENES, FINES | KBK | |

| Penalties and fines on insurance contributions to the Federal Compulsory Compulsory Medical Insurance Fund for employees | penalties | 392 1 02 02101 08 2011 160 |

| fines | 392 1 02 02101 08 3011 160 | |

KBK 18210202103081011160 in 2021 and 2021 for individual entrepreneurs

Taxes, state duties, insurance and social transfers are marked with a special code. This article provides information: what is the tax according to KBK 18210202103081011160, decoding 2018-2019 for individual entrepreneurs, as well as penalties and fines for payment.

Individual entrepreneurs transfer funds for insurance not only for their employees, but also for themselves. For example, for pensions - to the Pension Fund, and for medical contributions - to the Federal Compulsory Medical Insurance Fund. Each deduction corresponds to a code in the payment slip, indicating the type of deduction, where the funds are sent and to whose budget. For medical transfers from businessmen, the KBK 18210202103081011160 applies. The code is explained below.

What BCCs for insurance premiums are established for the Social Insurance Fund in 2021

Payments to the Social Insurance Fund are classified into 2 types:

- paid towards insurance for sick leave and maternity leave;

- paid towards insurance for accidents and occupational diseases.

Individual entrepreneurs working without hired employees do not list anything in the Social Insurance Fund.

Individual entrepreneurs and legal entities working with hired personnel make payments for them:

- for sick leave and maternity insurance - using KBK 18210202090071010160 (if we are talking about accruals made since 2017) and KBK 18210202090071000160 (if accruals were made before 2017) - contributions are administered by the Federal Tax Service;

- for insurance against accidents and occupational diseases - in the amount determined taking into account the class of professional risk by type of economic activity, using BCC 393 1 0200 160 - contributions are transferred directly to the Social Insurance Fund.

Individual entrepreneurs and legal entities concluding civil contract agreements with individuals pay only the second type of contributions, provided that this obligation is specified in the relevant agreements.

KBK for payment of insurance contributions to the Social Insurance Fund for employees

| TAX | KBK |

| Insurance contributions to the Social Insurance Fund for employees for compulsory social insurance in case of temporary disability and in connection with maternity | 393 1 02 02090 07 1000 160 |

| Insurance contributions to the Social Insurance Fund for employees against industrial accidents and occupational diseases | 393 1 02 02050 07 1000 160 |

KBK for payment of penalties on insurance contributions to the Social Insurance Fund for employees

| PENES, FINES | KBK | |

| Penalties and fines on insurance contributions to the Social Insurance Fund for employees for compulsory social insurance in case of temporary disability and in connection with maternity | penalties | 393 1 02 02090 07 2100 160 |

| fines | 393 1 02 02090 07 3000 160 | |

| Penalties and fines for insurance contributions to the Social Insurance Fund for workers from industrial accidents and occupational diseases | penalties | 393 1 02 02050 07 2100 160 |

| fines | 393 1 02 02050 07 3000 160 | |

FILES

KBC for insurance premiums for individual entrepreneurs “for themselves” in 2021

The Ministry of Finance, in its new order No. 132n, also updated the BCC for entrepreneurs. We are talking about fixed contributions for yourself.

KBC on contributions for individual entrepreneurs for themselves in 2021

| Payment Description | KBK contribution | KBK penalties | KBK fine |

| Contributions in a fixed amount to an insurance pension (from income within 300,000 rubles) | 182 1 0210 160 | 182 1 0210 160 | 182 1 0210 160 |

| Contributions to the FFOMS in a fixed amount | 182 1 0213 160 | 182 1 0213 160 | 182 1 0213 160 |

Changes to the BCC for compulsory medical insurance from April 23, 2018

On April 23, 2021, some KBK IP for themselves 2021 for the payment of insurance premiums changed. But the changes affected only contributions to pension funds. The initial changes occurred in February 2018 in accordance with Order of the Ministry of Finance No. 255 of December 27, 2017, in which the code for 1% deductions for themselves for entrepreneurs was changed. But already in April 2021, the decree was canceled and businessmen whose profits for the year amounted to more than 300,000 rubles are required to transfer money to the compulsory health insurance using the old KBK 1821020214006 1110160. But the codes for transferring to health insurance remained the same.

New BCCs for fines on insurance premiums for payments in 2021

| Payment Description | KBK |

| Pension contributions at basic and reduced rates | 182 1 0210 160 |

| Pension contributions at an additional tariff that does not depend on the special assessment (list 1) | 182 1 0210 160 |

| Pension contributions at an additional tariff depending on the special assessment (list 1) | 182 1 0210 160 |

| Pension contributions at an additional tariff that does not depend on the special assessment (list 2) | 182 1 0210 160 |

| Pension contributions at an additional tariff depending on the special assessment (list 2) | 182 1 0210 160 |

| Medical fees | 182 1 0213 160 |

| Social contributions | 182 1 0210 160 |

| Contributions for injuries | 393 1 0200 160 |

KBK for payment of fines

A fine is an additional charge to the amount of debt for insurance contributions for complete non-payment of the premium. This sanction is imposed only for non-payment of compulsory medical insurance funds at the end of the year. The amount of the fine depends on the time the fee is not paid:

- for the first violation - 20% of the debt amount;

- for secondary and subsequent payments - 40% of the debt amount.

When paying a fine for contributions to health insurance for an individual entrepreneur for himself, the receipt indicates KBK 18210202103083011160.

| Type of insurance premium | KBK |

| Insurance premiums for OPS | 182 1 0210 160 |

| Insurance premiums for VNiM | 182 1 0210 160 |

| Insurance premiums for compulsory medical insurance | 182 1 0213 160 |

| Insurance premiums for mandatory insurance in a fixed amount, paid by individual entrepreneurs for themselves (including 1% contributions) | 182 1 0210 160 |

| Insurance premiums for compulsory medical insurance in a fixed amount, paid by individual entrepreneurs for themselves | 182 1 0213 160 |

| Additional insurance contributions to compulsory pension insurance for employees who work in conditions that give the right to early retirement, including: | |

| – for those employed in work with hazardous working conditions (clause 1, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ) (the additional tariff does not depend on the results of the special assessment) | 182 1 0210 160 |

| – for those employed in jobs with difficult working conditions (clauses 2-18, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ) (the additional tariff does not depend on the results of the special assessment) | 182 1 0210 160 |

Where to pay in 2021

In 2021, the Federal Tax Service will continue to control the calculation and payment of insurance contributions for compulsory pension, medical and social insurance (with the exception of contributions for injuries). The listed types of insurance premiums in 2021 must be paid to the Federal Tax Service, and not to the funds.

Accordingly, the payment order for the payment of contributions in 2021 must be completed as follows:

- in the TIN and KPP field of the recipient of the funds - TIN and KPP of the tax inspectorate;

- in the “Recipient” field - the abbreviated name of the Federal Treasury body and in brackets - the abbreviated name of the Federal Tax Service;

- in the KBK field - budget classification code, consisting of 20 characters (digits). In this case, the first three characters indicating the code of the chief administrator of budget revenues should take the value “182” - Federal Tax Service.

Decoding KBK 18210202103081011160

The budget revenue classification code is a coordinating indicator for the budgets of various departments. Thanks to the code, the payer is determined, the budget to which the money will be transferred, and what the payment is used for: repayment of interest, payment of fines or the standard payment amount.

Encryption 18210202103081011160 means that compulsory medical insurance premiums are paid in a fixed amount for those employees or the businessman himself whose billing period ended before January 1, 2021. The funds are sent to the off-budget federal compulsory health insurance fund. The profit subcategory group indicates that this is a standard payment.

The code itself consists of 20 numbers, which make up seven blocks. Each block carries relevant information:

- 182 - the department to which the money is sent: Federal Tax Inspectorate.

- 1 - means the type of payment (income or expenses): tax profit or transfers to the budget.

- 02 - type of income: insurance contributions for social insurance to the Federal Compulsory Medical Insurance Fund

- 02103 - specifies the category of deductions: insurance contributions in a fixed amount for compulsory medical insurance to the budget of the local FFOMS.

- 08 - type of Russian treasury: budget of the Compulsory Medical Insurance Fund.

- 1011 - purpose of payment: standard payment for insurance contributions for compulsory medical insurance.

- 160 - generalized category of payments: deductions for compulsory social insurance from extra-budgetary funds.

BCC for insurance premiums for basic deductions in 2021

| Payment Description | KBK |

| Pension contributions at basic and reduced rates | 182 1 0210 160 |

| Pension contributions at an additional tariff that does not depend on the special assessment (list 1) | 182 1 0210 160 |

| Pension contributions at an additional tariff depending on the special assessment (list 1) | 182 1 0220 160 |

| Pension contributions at an additional tariff that does not depend on the special assessment (list 2) | 182 1 0210 160 |

| Pension contributions at an additional tariff depending on the special assessment (list 2) | 182 1 0220 160 |

| Medical fees | 182 1 0213 160 |

| Social contributions | 182 1 0210 160 |

| Contributions for injuries | 393 1 0200 160 |

Filling out a payment form when paying a fine

The differences between paying the tax amount and the penalty amount lie in filling out several fields of the payment order:

- Field 106 “Basis of payment” when paying penalties acquires the value “ZD” in case of voluntary calculation and repayment of debts and penalties, “TR” - at the written request of the supervisory authority or “AP” - when accruing penalties according to the inspection report.

- Field 107 “Tax period” - you need to put a value other than 0 in it only when paying a penalty on a tax claim. In this case, the field is filled in according to the value specified in such a requirement.

- Fields 108 “Document number” and 109 “Document date” are filled in in accordance with the details of the inspection report or tax requirement.

As for the BCC (field 104), for penalties on contributions paid to the Federal Tax Service in 2019-2020, they are as follows:

| Insurance type | KBK |

| Pension | 182 1 0210 160 |

| Medical | 182 1 0213 160 |

| For disability and maternity | 182 1 0210 160 |

And for contributions for injuries, which remain under the jurisdiction of the FSS, the KBC for penalties is 393 1 0200 160.

Calculation of penalties for insurance premiums in 2021

Since 2021, the rules for determining the amount of penalties are regulated by clause 4 of Art. 75 of the Tax Code of the Russian Federation, containing 2 calculation formulas, in which the amount of debt is multiplied by the number of days of delay and by a rate equal to:

- 1/300 of the refinancing rate - applies to individuals and individual entrepreneurs (regardless of the number of days of delay in payment) and for legal entities that are late in payment by no more than 30 calendar days;

- 1/150 of the refinancing rate - valid only for legal entities and only for a period of delayed payment exceeding 30 calendar days, while for 30 days of delay a rate of 1/300 will be applied.

“Unfortunate” contributions, which continue to be supervised by the FSS, are subject to the procedure described in Art. 26.11 of the Law “On Social Insurance against Accidents and Occupational Injuries” dated July 24, 1998 No. 125-FZ, and are calculated using a formula similar to those described above using a rate of 1/300 of the refinancing rate.

The refinancing rate in each of the above calculations is taken in its actual values during the period of delay. That is, if it changed during the calculation period, then such a calculation will be divided into several formulas using their own refinancing rates.

Consequences of errors when paying penalties

Since the latest changes came into force, the Treasury and the Federal Tax Service have jointly organized work to independently clarify payments that were assigned the status of unclear in the system (letter from the Federal Tax Service dated January 17, 2017 No. ZN-4-1 / [email protected] ). Therefore, if funds are received into the budget account using incorrect details, the treasury will send the payment where it is needed. But this does not apply to all errors. For your convenience, we have prepared a table for determining further actions depending on the type of error made:

| Error in payment order | Consequences |

| TIN, KPP, recipient's name, field 104, 106, 107, 108, 109 | Payment is subject to automatic verification. To speed up the process, you can write a clarifying letter to the tax office. |

| Payment details (account number, BIC, bank name) | Payment will not be credited to your personal account. You need to write a letter to the bank to cancel the payment if it has not yet been executed, or contact the Federal Tax Service to return it. In the second case, it is recommended to duplicate the payment using the correct details to avoid arrears. |

| Amount of payment | If the payment is made for a large amount, then you need to write a letter to offset the overpayment to another cash register company. If you paid less than necessary, then you need to make an additional payment |

Results

The rules for calculating penalties on contributions from 2021 are subject to the requirements of the Tax Code of the Russian Federation. Compliance with the special requirements for payment documents for the transfer of fines is necessary when issuing a payment order for the payment of this payment. In some cases, errors made in the payment document do not prevent the payment from being credited to the correct treasury account.

Sources

- https://nalog-nalog.ru/uplata_nalogov/rekvizity_dlya_uplaty_nalogov_vznosov/kbk_po_strahovym_vznosam_tablica/

- https://assistentus.ru/kbk/strahovye-vznosy-za-rabotnikov/

- https://xn—-btbhxcbx.xn--p1ai/pensionnyie-vznosyi/

- https://buhguru.com/strahovie-vznosy/kbk-strahovye-vznosy-2019-tablitsa.html

- https://nalog-nalog.ru/strahovye_vznosy/uplata_strahovyh_vznosov/kbk_peni_po_strahovym_vznosam/