Tax period code

In 3-NDFL, the tax period (code) is the period of time for which you are reporting. Each time period is indicated by a digital value, depending on the period for which the declaration is submitted and indicated on the title page.

| 21 | First quarter |

| 31 | Half year |

| 33 | Nine month |

| 34 | Year |

Taxpayer category code in the 3-NDFL declaration

On the title page of the form you will also find the payer category code for 3-NDFL. The categories are listed in Appendix No. 1 to the procedure for filling out reports. For ordinary citizens, the appropriate 3-NDFL taxpayer category code is “760,” and the 3-NDFL taxpayer category code “720” is allocated for individual entrepreneurs.

| 720 | An individual registered as an individual entrepreneur |

| 730 | Notary engaged in private practice and other persons engaged in private practice |

| 740 | Lawyer who established a law office |

| 750 | Arbitration manager |

| 760 | Another individual declaring income in accordance with Articles 227.1 and 228 of the Tax Code, as well as for the purpose of obtaining tax deductions in accordance with Articles 218-221 or for another purpose |

| 770 | Individual entrepreneur - head of a peasant (farm) enterprise |

Document type code in the 3-NDFL declaration

On the title page of the declaration, in the section about the identity document, indicate its code value. The full list is contained in Appendix No. 2 to the procedure for filling out 3-NDFL and in the following table.

| 21 | Russian citizen passport |

| 03 | Birth certificate |

| 07 | Military ID |

| 08 | Temporary certificate issued in lieu of a military ID |

| 10 | Foreign citizen's passport |

| 11 | Certificate of consideration of an application for recognition of a person as a refugee on the territory of Russia on the merits |

| 12 | Residence permit in the Russian Federation |

| 13 | Refugee ID |

| 14 | Temporary identity card of a Russian citizen |

| 15 | Temporary residence permit in the Russian Federation |

| 18 | Certificate of temporary asylum on the territory of the Russian Federation |

| 23 | Birth certificate issued in another state |

| 24 | Identity card of a Russian military personnel, military ID of a reserve officer |

| 91 | Other documents |

How to fill out a tax refund return?

You need to fill out the following pages:

- Title page;

- Section 1 and 2;

- Appendix to section 1 - application for tax refund/credit;

- Annex 1;

- Appendix 5.

First, the amount of tax and withheld income for the reporting year 2021 is indicated. Next, the amount of social deduction for training expenses is calculated. The next step is to calculate the personal income tax for return in section 2, after which the total amount is transferred to Section 1.

The last thing to fill out is a cover sheet and an application for a tax refund for training expenses.

Instructions for filling

The table below provides instructions for preparing a 3-NDFL declaration for tax deduction for education for 2021 - it indicates which lines to fill out and with what indicators.

Line by line filling:

| Declaration field | Instructions for filling |

| Title page | |

| Adjustment | If in 2021 the return for tuition deduction for 2021 is submitted for the first time, then 0 is entered. If the data is clarified for resubmission, then the number of adjustments is indicated. |

| Period | 34 |

| Year | 2020 |

| Tax authority | Four-digit branch code at the taxpayer's place of residence. The indicator can be found on the Federal Tax Service website by entering your address - link. |

| Taxpayer | The country code is 643 for the Russian Federation. Taxpayer category – 760 for individuals wishing to return tax based on the 3-NDFL declaration. Full name and birth information are copied in exact accordance with the passport. The identification document is a Russian passport, its code is 21. Status is indicated as 1 for Russian citizens. The telephone number must be entered with the area code; a person must always be available for communication at this number. |

| Number of pages | The number of pages of the completed declaration form and attached documents is entered after filling out 3-NDFL. |

| Credibility | If a person himself personally submits a report to the Federal Tax Service, then he needs to put 1 and sign the page indicating the date of signing. If a person entrusts this function to his representative, then enter 2, enter the full name of the authorized person and the details of the document giving the right to this action (usually a power of attorney). The completed 3-NDFL form is signed by a representative for the taxpayer. |

| Section 1 | |

| 010 | Digit 2 |

| 020 | KBK - 18210102010011000110 |

| 030 | OKTMO - if the taxpayer does not know this code, it can be viewed on the Federal Tax Service website via the link, you should enter your address, after which the corresponding OKTMO will be shown. |

| 050 | The amount of tax to be refunded in connection with the tax deduction for education is from page 160 of section 2. |

| Appendix 1 to Section 1 - contains an application for a tax refund, a new sheet that allows you to create an application inside the 3-NDFL declaration, without needing to prepare it separately. | |

| 095 | Number 1 |

| 100 | The amount of tax that needs to be returned is from page 050 of section 1. |

| 110 | KBK from page 020 section. 1. |

| 120 | OKTMO from page 030 section. 1. |

| 130 | Tax period – the year 2021 should be indicated. |

| 140 | The name of the servicing bank where the taxpayer's account is opened. |

| 150 | KBK Bank. |

| 160 | Enter code 02 if you want the money to go to your current account - to your card. Code 01 is indicated if the money should go to the deposit account. |

| 170 | Taxpayer account number. |

| 180 | Full name of the person who owns the account. |

| Section 2 | |

| 001 | 13 – tax rate. |

| 002 | 3 – other income |

| 010 | Payments for the year from adj. 1. |

| 030 | Taxable payments for the year. |

| 040 | The amount of deductions for 2021 for training is from page 200 appendix. 5. |

| 060 | Tax base including social deductions for educational services = line 030 – line 040. |

| 070 | Personal income tax from the tax base is the tax that had to be paid for 2021, taking into account the required deductions for education = line 001 * line 060. |

| 080 | Personal income tax, which was paid in fact for 2021 - from page 080 appendix. 1. |

| 160 | Personal income tax to be returned = line 080 – line 070. |

| Annex 1 | |

| 010 | 13 – personal income tax rate. |

| 020 | 07 – code of income in the form of salary. |

| 030, 040, 050, 060 | Employer details. |

| 070 | Total payments from this employer for the year - based on clause 5 of the 2-NDFL certificate. |

| 080 | The total withheld tax for the year is based on clause 5 of the 2-NDFL certificate. |

| Appendix 5 | |

| 100 | Educational expenses for children - no more than a tax deduction of 50,000 rubles. for each child per year. |

| 120 | Indicator from page 100 |

| 130 | Expenses for your own education, as well as for brothers and sisters under 24 years of age - no more than a tax deduction of 120,000 rubles. in a year. |

| 180 | Indicator from page 130. |

| 190 | Total social deduction for the year = line 120 + line 180. |

| 200 | Total deduction including standard benefits. If the 3-NDFL declaration is filled out only for a tax refund in connection with training, then the indicator from page 190 is repeated. |

Design example

Below is an example of filling out 3-NDFL in 2021, provided that in 2021 a person paid for his child’s education in the amount of 30 thousand rubles. and your training in the amount of 90 thousand rubles.

and sample filling

.

.

Region code of the Russian Federation

In the “Address and telephone” section on the title page, you must indicate the code designation of the Russian region. Find the region (code) for 3-NDFL in Appendix No. 3 to the filling procedure, or in the following table:

| 01 | Republic of Adygea |

| 02 | Republic of Bashkortostan |

| 03 | The Republic of Buryatia |

| 04 | Altai Republic |

| 05 | The Republic of Dagestan |

| 06 | The Republic of Ingushetia |

| 07 | Kabardino-Balkarian Republic |

| 08 | Republic of Kalmykia |

| 09 | Karachay-Cherkess Republic |

| 10 | Republic of Karelia |

| 11 | Komi Republic |

| 12 | Mari El Republic |

| 13 | The Republic of Mordovia |

| 14 | The Republic of Sakha (Yakutia) |

| 15 | Republic of North Ossetia-Alania |

| 16 | Republic of Tatarstan (Tatarstan) |

| 17 | Tyva Republic |

| 18 | Udmurt republic |

| 19 | The Republic of Khakassia |

| 20 | Chechen Republic |

| 21 | Chuvash Republic - Chuvashia |

| 22 | Altai region |

| 23 | Krasnodar region |

| 24 | Krasnoyarsk region |

| 25 | Primorsky Krai |

| 26 | Stavropol region |

| 27 | Khabarovsk region |

| 28 | Amur region |

| 29 | Arhangelsk region |

| 30 | Astrakhan region |

| 31 | Belgorod region |

| 32 | Bryansk region |

| 33 | Vladimir region |

| 34 | Volgograd region |

| 35 | Vologda Region |

| 36 | Voronezh region |

| 37 | Ivanovo region |

| 38 | Irkutsk region |

| 39 | Kaliningrad region |

| 40 | Kaluga region |

| 41 | Kamchatka Krai |

| 42 | Kemerovo region |

| 43 | Kirov region |

| 44 | Kostroma region |

| 45 | Kurgan region |

| 46 | Kursk region |

| 47 | Leningrad region |

| 48 | Lipetsk region |

| 49 | Magadan Region |

| 50 | Moscow region |

| 51 | Murmansk region |

| 52 | Nizhny Novgorod Region |

| 53 | Novgorod region |

| 54 | Novosibirsk region |

| 55 | Omsk region |

| 56 | Orenburg region |

| 57 | Oryol Region |

| 58 | Penza region |

| 59 | Perm region |

| 60 | Pskov region |

| 61 | Rostov region |

| 62 | Ryazan Oblast |

| 63 | Samara Region |

| 64 | Saratov region |

| 65 | Sakhalin region |

| 66 | Sverdlovsk region |

| 67 | Smolensk region |

| 68 | Tambov Region |

| 69 | Tver region |

| 70 | Tomsk region |

| 71 | Tula region |

| 72 | Tyumen region |

| 73 | Ulyanovsk region |

| 74 | Chelyabinsk region |

| 75 | Transbaikal region |

| 76 | Yaroslavl region |

| 77 | Moscow |

| 78 | Saint Petersburg |

| 79 | Jewish Autonomous Region |

| 83 | Nenets Autonomous Okrug |

| 86 | Khanty-Mansiysk Autonomous Okrug - Ugra |

| 87 | Chukotka Autonomous Okrug |

| 89 | Yamalo-Nenets Autonomous Okrug |

| 91 | Republic of Crimea |

| 92 | Sevastopol |

| 99 | Other areas, including the city and Baikonur Cosmodrome |

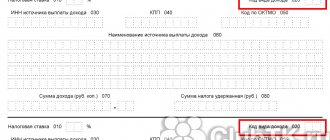

Income type code in 3-NDFL

The type of income code (020) in the 3-NDFL declaration is filled out on Sheet A “Income from sources in the Russian Federation”. The list of designations is given in Appendix No. 4 to the procedure for completing the declaration.

For example, when selling a car, the income code in 3-NDFL is “02”. For other cases, see the table:

| 01 | Income from the sale of real estate and shares in it, determined based on the price of the object specified in the agreement on the alienation of property |

| 02 | Income from the sale of other property (including a car) |

| 03 | Income from transactions with securities |

| 04 | Income from renting out an apartment (other property) |

| 05 | Cash and in-kind income received as a gift |

| 06 | Income received on the basis of an employment (civil) contract, the tax from which is withheld by the tax agent |

| 07 | Income received on the basis of an employment (civil) contract, the tax from which is not withheld by the tax agent (even partially) |

| 08 | Income from equity participation in the activities of organizations in the form of dividends |

| 09 | Income from the sale of real estate and shares in property, determined based on the cadastral value of this property, multiplied by a reduction factor of 0.7 |

| 10 | Other income |

Possible errors and problems

Of course, there may be errors when filling out the declaration, especially when submitting the document for the first time.

Let's look at the most common problems that can be avoided. When filling out the declaration, you must indicate the code corresponding to the calendar year. However, for a number of reasons, taxpayers decide to specify a shorter period that directly corresponds to the period in which the income was received. There is no need to do this, as it will be considered an error.

In addition, if you are submitting a report for a company that has already been liquidated, you must indicate a special code. The catch is that in the standard program for filling out the declaration, the default code is 34. In this case, you can fill out the declaration by hand and submit it in the correct form.

Object name code in 3-NDFL

The object name code (010) in 3-NDFL is filled out in Sheet D1 “Calculation of property tax deductions for expenses on new construction or acquisition of real estate.” Indicate the numerical designation of the purchased property.

| 1 | House |

| 2 | Apartment |

| 3 | Room |

| 4 | Share in a residential building, apartment, room, land plot |

| 5 | Land plot for individual housing construction |

| 6 | Plot of land with purchased residential building |

| 7 | Residential building with land |

Filling out Appendix 7, if the deduction is issued for the first time: section 2

Section 2 calculates the deduction amount. Actually, this is the section for which the entire declaration is filled out. And it is this that causes the greatest difficulty for those who are not used to filling out tax forms.

Some tax authorities working with payers on personal income tax returns verbally recommend that those who submit 3-personal income tax, filled out manually on paper, make entries in section 2 of Appendix 7 with a simple pencil so that they can correct something and circle it with a pen in the presence of an inspector.

The first thing anyone applying for a deduction should know is that the deduction is provided not from the personal income tax amount (as many mistakenly believe), but from the tax base. To make it clearer, let's look at an example.

Example

Petrov purchased an apartment for 3,000,000 rubles. The maximum deduction for this purchase, due to him under Art. 220 of the Tax Code of the Russian Federation - 2,000,000 rubles. In total, during the period specified in the declaration, Petrov earned 800,000 rubles, personal income tax on them amounted to 104,000 rubles. These 800,000 rubles are Petrov’s tax base. And it is precisely this that should be reduced by the amount of the deduction. In this case, the tax base can be reduced in full: 800,000 – 800,000 = 0. That is, Petrov will receive a tax refund in the amount of 104,000 rubles (800,000 × 13%). And Petrov can transfer the deduction balance of 1,200,000 (2,000,000 – 800,000) rubles to the following years.

When filling out Appendix 7 for the first time, Section 2 indicates:

- page 2.5 - tax base (Petrov from the example will put 800,000 there);

- page 2.6 - confirmed amounts of expenses by which the tax base for the period is reduced (Petrov confirmed with documents all 2,000,000 due to him, which means he will put the value that he actually uses - 800,000);

- line 2.8 - the balance of the deduction carried over to the following periods (years) (Petrov will put 1,200,000 in line 2.8, intended for the deduction that is given specifically for the purchase (construction) of the real estate itself).

Taxpayer identification in 3-NDFL

In Sheet D1, you must also select the taxpayer attribute (030).

| 01 | The owner of the property in respect of which a property deduction for personal income tax is claimed |

| 02 | Property owner's spouse |

| 03 | Parent of a minor child - owner of the property |

| 13 | A payer claiming a property deduction for expenses related to the purchase of housing in the common shared ownership of himself and his minor child (children) |

| 23 | A payer claiming a property deduction for personal income tax for expenses related to the purchase of housing in the common shared ownership of the spouse and his minor child (children) |

Example

Let's assume that E.A. Shirokova is a tax resident of the Russian Federation and not a pensioner. On January 25, 2021, Rosreestr registered her sole ownership of the apartment, which is located in Moscow on Rusakovskaya Street.

In 2021, Shirokova will apply for a property deduction for personal income tax for the first time. According to the 2-NDFL certificate from the company where she works, 550,000 rubles is the amount of payments to her, from which the employer withheld and transferred personal income tax to the budget (without all deductions).

Thus, the balance of the property deduction, which transferred to 2017, amounted to:

2,000,000 rub. (p. 120) MINUS 550,000 rub. (p. 210) = 1,450,000 rub. (p. 230).

As a result, Shirokova will be able to return for the purchase of an apartment in 2021:

550,000 × 13% = 71,500 rubles.

Below is an example of filling out Sheet D1 in 3-NDFL for 2016 , filed on March 1, 2021 by E.A. Shirokova in the Federal Tax Service No. 18 of Moscow:

Also see “Declaration 3-NDFL: how to fill out for 2021.”

Read also

01.03.2017

Budget classification code 3-NDFL

In field “020” of Section 1 “Information on the amounts of tax subject to payment (surcharge) to the budget/refund from the budget”, mark the budget classification code (BCC) of tax revenues, which is used to group items of the state budget. Find out the appropriate BCC for your case on the website of the Federal Tax Service.

In addition, you can use a service that will help you determine not only the BCC, but also the numbers of your inspection of the Federal Tax Service and the All-Russian Classifier of Municipal Territories (OKTMO).

OKTMO code - what is it in 3-NDFL?

Using OKTMO, the declaration indicates the code of the municipality at the place of residence (or registration) of the person (or individual entrepreneur). Individuals may need OKTMO of the company from which the income was received in Sheet A of 3-NDFL. Find out the number from the tax office or on the Federal Tax Service website.

If OKTMO contains less than 11 characters, then do not forget to put dashes in the remaining empty cells. Read more about the rules for filling out a tax return in the article “How to fill out 3-NDFL”.

About the author of the article

Lidia Ivanova I am the editor-in-chief of the Sashka Bukashki website. More than 15 years of experience working with legal information.

In what cases do you need to submit a certificate?

As a general rule, 3-NDFL should be filed when individuals receive income both in the Russian Federation and abroad. For example, it could be:

- proceeds received as a result of the sale of real estate,

- rent received for renting out an apartment for temporary use to other persons,

- accrued dividends,

- remuneration received as a result of labor activity, etc.

It is worth noting that the answer to the question largely depends on whether the person is employed or not. If a citizen has an official workplace, then the employer reports for him for personal income tax. In this case, the tax amount itself is deducted from wages every month.

If an individual does not have a job, then he will have to independently prepare and submit 3-NDFL to the tax authorities.