Individual entrepreneurs are required to pay insurance premiums for themselves every year; payments for compulsory health insurance and compulsory medical insurance are mandatory. If the individual entrepreneur closes within a year, then you only need to pay for the actual time spent in this status.

To calculate for an incomplete year, you need, based on the fixed annual amount of contributions, to calculate the portion attributable to the period worked as an individual entrepreneur and transfer it for yourself within 15 calendar days from the date of closure.

How to use the calculator

Instructions for using the individual entrepreneur insurance premium calculator

- By default, calculations are made for the selected whole year. If you registered an individual entrepreneur this year, or you closed it, then select a more specific start and end date for the period.

- If your income for the selected period was no more than 300,000 rubles, then you can leave the “Income for this period” field empty. The entered amount will not affect the final result.

- Click "CALCULATE". You can save the result with all the calculation details to a doc file.

About the individual entrepreneur insurance premium calculator

As soon as an individual entrepreneur has received registration in this capacity, he has obligations to the state for taxes and fees. Regardless of the taxation system he adheres to and the financial success of his business, individual entrepreneurs must annually pay contributions to insurance funds.

To calculate the amount of amounts required to be paid, you can use an online calculator, which will make this process quick and transparent.

Which KBK should I pay for?

This year, payment of insurance pension contributions for individual entrepreneurs without hired personnel is carried out at KBK:

- 18210202140061110160 – current payment;

- 18210202140062110160 – penalties;

- 18210202140063010160 – fines.

Entrepreneurs with hired staff use the following codes:

- 18210202010061010160 – current payment;

- 18210202010062110160 – penalties;

- 18210202010063010160 – fines.

KBC for paying contributions to the health insurance fund “for yourself”:

- 18210202103081013160 – current payment;

- 18210202103082013160 – penalties;

- 18210202103083013160 – fines.

Codes for employers:

- 18210202101081013160 – current payment;

- 18210202101082013160 – penalties;

- 18210202101083013160 – fines.

The entrepreneur pays into the social insurance fund only for employees. Insurance in case of injury is paid at KBK:

- 39310202050071000160 – current payment;

- 39310202050072100160 – penalties;

- 39310202050073000160 – fines.

Hotline for citizen consultations: 8-800-350-57-94

For payments to the Social Insurance Fund in case of temporary disability or maternity leave, other BCCs are used:

- 18210202090071010160 – current payment;

- 18210202090072110160 – penalties;

- 18310202090073010160 – fines.

Lists of codes for long-ago reporting periods are listed on the official website of the Federal Tax Service in the corresponding section of the menu.

This you need to know: What to do after closing an individual entrepreneur

When do you need to pay?

Insurance premiums are calculated to be paid once a year. They must be transferred by the end of the current year, that is, by December 31. Otherwise, the entrepreneur is free to choose the terms for payment: you can make one payment at any time of the year, or you can make payments in installments, again at intervals convenient for the entrepreneur. Usually, a quarterly mode of making equal shares of insurance premiums is chosen - this way the tax burden will be distributed more evenly.

If an additional contribution to the Pension Fund is provided for an individual entrepreneur (in case of income over 300,000 rubles), then it must be paid before April 1 of the next year. At the same time, the obligatory part must be paid by December 31, and until April you can “delay” with contributions calculated from the amount that exceeded the limit of 300 thousand rubles.

How to pay insurance premiums?

The payment method is chosen by the individual entrepreneur. The easiest way, and this method is the most common, is a transfer from the entrepreneur’s current account by bank transfer. You can deposit these funds from any personal account, not necessarily registered as a settlement account and linked to the activities of an individual entrepreneur. Payment in cash is also possible, just remember to keep the bank receipt to confirm payment of insurance premiums.

IMPORTANT INFORMATION! The budget classification code (BCC) for the transfer of insurance premiums has changed since 2021 - now these payments are subject to the jurisdiction of the Federal Tax Service. Both mandatory fixed payments and a contribution from increased income of more than 300 thousand must be paid to the same BCC.

What else should you do after closing?

There are a number of additional measures related to the fact of closure of business activities:

- Submitting a declaration for the last reporting period. Even with zero indicators, the document remains mandatory.

- Deregistration of cash register equipment. The procedure for resolving the issue may differ depending on the territory in which everything occurs. It is better to clarify the requirements in advance with representatives of regulatory authorities.

- Closing a current account. It is optimal when this is done after receiving all the necessary documents. From January 1, 2021, it was prohibited to terminate activities without written notification to the tax office. Violation of the rules leads to quite serious fines.

Important! The pension fund does not require notifications. Information is transmitted to services through interdepartmental interaction. After liquidation, most reports are kept for 3 years. If necessary, additional checks are organized during this time and requests are sent.

Amount of insurance premiums: calculate using a calculator

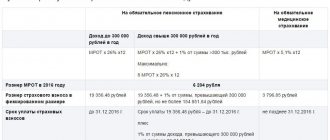

Although contributions are fixed, the amount payable changes annually. Until 2021, it was entirely dependent on the minimum wage established by the state. The object and basis for calculations do not matter.

To calculate the amount of fixed contributions using the calculator, you need to know the following basic initial indicators:

- the minimum wage value established for the reporting year at the legislative level (necessary for calculation only until 2018);

- tariffs for contributions to the Pension Fund of the Russian Federation and the Federal Compulsory Compulsory Medical Insurance Fund (constant values, required for calculation only until 2021);

- fixed amounts in the Pension Fund and the Federal Compulsory Medical Insurance Fund (for 2018-2020);

- the number of billing months for which it is planned to transfer the contribution (12 in the case of annual payment);

- income for the selected period (in rubles).

The first three indicators do not need to be entered; they are fixed in the calculator. You need to enter the start date of the reporting period and its end, the calculator will take into account the estimated time independently.

Payment of contributions when closing an individual entrepreneur in the middle of the year

Despite the timing of payment of 1% in excess of 300,000 rubles received for the previous year, closing an individual entrepreneur in the middle of the year will not relieve the entrepreneur from paying all mandatory payments. In order to avoid being brought to administrative, and even more so criminal, liability, a citizen should pay all contributions in a timely manner.

Calmness and attention to detail are the key to a successful life. Each person is capable of doing what others can do. Today, with access to the Internet, everyone can become an economist, accountant and oligarch.

How to correctly determine the amount of income from which contributions are paid?

In order to correctly enter into the appropriate window of the calculator the key indicator on which the amount of mandatory insurance payments will depend, you need to know exactly what financial results fall under the concept of “income of an individual entrepreneur” and are the basis for this calculation.

If the size of the contribution itself does not depend on the tax system, then this is decisive for determining income.

- Entrepreneurs under the general taxation system must pay contributions on the same income on which they pay personal income tax (not to be confused with the tax base; unlike the amount of income, it is reduced by tax deductions).

- Under the simplified tax system (USN), for calculating contributions, income is taken that is not reduced by the amount of expenses, even if the tax is paid according to the “income minus expenses” scheme.

- When using UTII, income for calculating insurance premiums is considered imputed, which must be calculated according to a specially provided formula, including basic profitability (it is determined by the Tax Code depending on the indicators of the object), multiplied by corrective indicators.

- The patent system takes into account potentially real income established by regional laws, and it is taken as an insurance base.

- When combining several tax systems at the same time, the amounts of income to take into account the amount of insurance premiums are added up.

Payment deadlines

UTII, simplified tax system and patent are special regimes that are used in most cases. The procedure for settlements with regulatory authorities varies depending on how exactly a particular market participant operates.

- No later than 5 days after cancellation, 3NDFL is transferred when using OSN. Payment is made within a 15-day period. No later than the 25th day of the month following the closure of the individual entrepreneur, a VAT declaration is submitted. The fee is transferred in full at once, or divided into three parts.

- The 25th day of the month after liquidation is the payment time in the case of the simplified tax system. The declaration must be submitted before the deadline. The situation is radically different when it comes to a patent. In this case, there is no obligation to submit a declaration. You just need to pay for the validity period before it ends. The tax will be recalculated if an application to terminate the activities of an individual entrepreneur is submitted at a time when the document is still valid.

- The 25th day of the next month after closing applies to those working on UTII. The entrepreneur must submit a declaration by the 20th of the same month.

Attention! It is recommended to retain tax documentation for 4 years after liquidation. Receipts for contributions are kept for 6 years.

How the calculator works

Since 2021, the calculator for calculations is based on Article 430 of the Tax Code of the Russian Federation and in fact the calculation formula can be written as follows:

Svzn = Rfix / 12 x Nmonth, where:

- Svzn – amount of insurance premium payable;

- Rfix – a fixed amount of a specific insurance contribution (to the Pension Fund of the Russian Federation or to the Federal Compulsory Compulsory Medical Insurance Fund);

- Nmonth – the number of months for which the contribution is paid (after all, the business may not have been started from the beginning of the year or only part of the payment needs to be calculated).

Until 2021, the calculator uses the formula established by Article 14 of Federal Law No. 212-FZ to calculate insurance premiums:

Свзн = minimum wage x Рtar x Nmonth, where:

- Svzn – amount of insurance premium payable;

- Minimum wage – the minimum wage value adopted by the state for the reporting year;

- Rtar – the rate of a specific insurance premium (in the Pension Fund of the Russian Federation - 26% or in the Federal Compulsory Medical Insurance Fund - 5.1%);

- Nmonth – the number of months for which the contribution is paid.

If you need to calculate an additional contribution amount for an individual entrepreneur with more than 300 thousand annual income, then the Pension Fund should receive an additional 1% on the amount exceeding the limit.

If the individual entrepreneur is an employer

Contribution rates

If an individual entrepreneur employs hired workers, then insurance premiums are calculated from the salary at the following rates:

- pensions - 22%;

- medical - 5.1%;

- social (sick leave and maternity) - 2.9%;

- social (from accidents) - the tariff depends on the type of activity. Typically 0.2%.

Contribution benefits

For individual entrepreneurs who are listed in the register of small and medium-sized enterprises (SMEs), there is a discount on contributions to compulsory pension insurance from employee salaries. Thus, payments in the amount of the minimum wage (12,130 in 2021, 12,792 in 2021) are subject to the standard 22%, but everything above the minimum wage is subject to a reduced rate of 10% (Article 427 of the Tax Code of the Russian Federation).

Do I need to register with the funds?

There is no need to register with the Pension Fund and the Compulsory Medical Insurance Fund. The FSS is registered within 30 days from the date of:

- concluding an employment contract with the first employee;

- or concluding a GPC agreement, which stipulates contributions “for injuries”.

Who can save

Some entrepreneurs can legally save on employee contributions through reduced rates if they are residents of special economic zones. The list of zones is extensive, if there are such zones in your region and you could become a member, please contact your accountant or our tax advisor for information about the benefits due to you.

If benefits were paid

Insurance premiums can be reduced by the amount of expenses spent on sick leave (payment for the first 3 days of sick leave is made at the expense of the individual entrepreneur himself) and benefits (paid entirely at the expense of the Social Insurance Fund). If the amount of benefits exceeds the contributions, contact Social Insurance for compensation for the resulting difference (clause 9 of Article 431 of the Tax Code of the Russian Federation, Part 2 of Article 4.6 of the Federal Law of December 29, 2006 N 255-FZ). Tax authorities can also offset the specified difference against upcoming payments (clause 9 of Article 431 of the Tax Code of the Russian Federation). The offset is made only after confirmation of expenses by Social Insurance (the fund conducts a desk audit).

Payment of contributions for employees

Contributions are transferred to the tax office by the 15th of the next month. If the date coincides with a weekend, the payment deadline is shifted to the first working day. Look for information on KBK on the website of the Federal Tax Service of Russia, where you can also make a payment. Social insurance contributions against accidents are transferred within the same time frame only to the Social Insurance Fund.

If you don't pay on time

Late payment of fees will result in penalties for each day of delay: 1/300 of the key rate of the Bank of Russia (from 10/30/2017 - 8.25%). If the delay in payment is due to incorrect calculation of contributions (the tax report understates the amount of salary), then you will be fined 20% of the unpaid amount. And if the non-payment is intentional, a fine of 40% of the due contributions. Usually, arrears are discovered during an on-site or desk inspection.

Reporting for employees

Individual entrepreneurs fill out the forms:

- SZV-TD - until the 15th of the next day. the month in which the hiring, dismissal, transfer or transition to electronic work books took place.

- SZV-M - submitted to the Pension Fund no later than the 15th of the following day. month following the reporting month;

- Calculation of insurance premiums (KND 1151111) - submitted to the tax office no later than 30 months;

- 4-FSS - provided to the FSS for up to 20 consecutive months. inclusive, in electronic form - up to 25 inclusive;

- SZV-STAZH - provided to the Pension Fund until March 1 of the next year.

Fines

The penalty for late submission of the calculation of insurance premiums or 4-FSS reporting is 5% (for each month of delay) of the contributions not paid on time, which must be transferred for the last quarter. Maximum - 30% of the amount of contributions, minimum - 1,000 rubles. For SZV-M and SZV-STAZH the fine is 500 rubles. for each employee not reflected on the form in a timely manner.

Profdelo clients do not face fines: we take on individual entrepreneurs for services and fully manage all the individual entrepreneurs’ accounting. Details at the link: