P.A. Bespalov works as a storekeeper at Alpha LLC. On January 13, he was fired due to the liquidation of the organization. When an employee is dismissed due to liquidation, the organization pays him a benefit in the amount of average monthly earnings.

Bespalov's average daily earnings is 484 rubles/day.

The benefit was calculated for the first month after dismissal - from January 14 to February 13. In this period, according to Bespalov’s work schedule (five-day work week), there are 23 working days. The severance pay amounted to 11,132 rubles. (484 RUR/day × 23 days). Bespalov received it on the day of his dismissal, January 13.

The Alpha accountant made the following entries in accounting:

Debit 25 Credit 70 – 11,132 rub. – severance pay accrued;

Debit 70 Credit 50 – 11,132 rub. - severance pay was issued.

Compensation under additional agreement upon dismissal

In addition, the employment contract or collective agreement may provide for other cases of payment of severance pay, as well as establish increased amounts of severance pay. According to Art. 57 of the Labor Code of the Russian Federation, if, when concluding an employment contract, no conditions were included in it, these conditions can be determined by a separate annex to the employment contract, or by a separate agreement of the parties, concluded in writing, which are an integral part of the employment contract. Thus, expenses in the form of payment of severance pay provided for in the additional agreement to the employment contract can be taken into account as part of expenses that reduce the tax base for corporate income tax. Labor legislation defines a list of situations in which the employer is obliged to pay severance pay upon termination of an employment contract. For example, severance pay in case of liquidation of a company, reduction in the number or staff of employees, etc. At the same time, the Labor Code allows for other cases of payment of severance pay to be provided for in an employment or collective agreement 1 . Sometimes a company agrees to pay an employee an additional one-time compensation upon dismissal and establishes such payment in the agreement on termination of the employment contract. However, this compensation is not provided for either in the list of mandatory payments under labor legislation, or in the labor or collective agreement. According to the courts, the agreement to terminate the employment contract is not part of it. It does not regulate relations related to the employee’s performance of a labor function. In this case, the income tax base cannot be reduced by the costs of paying compensation (compensation) to an employee upon dismissal 2 . However, the company may enter into an additional agreement with the employee to the employment contract, which will provide for the payment of severance pay upon its termination by agreement of the parties. The Russian Ministry of Finance and tax authorities in their recent letters explained that costs in the form of severance payments can be taken into account as part of expenses that reduce the income tax base. To do this, it is necessary 3 that such payment be provided for in an employment contract, an additional agreement (which is an integral part of it) or a collective agreement. Moreover, the text of the additional agreement must indicate that it is an integral part of the employment contract. Otherwise, the accounting of expenses for payment of compensation may be challenged by tax authorities. Below we provide a sample additional agreement to an employment contract. In earlier letters, the Russian Ministry of Finance opposed reflecting, when calculating the income tax base, the costs of compensation payments under an additional agreement to resigning employees 4 . Officials believed that these compensations are not directly provided for in Russian legislation, they do not meet the criteria of tax legislation and cannot be reflected as part of labor costs 5 .

Payment terms

Whether an employee will receive this type of compensation payment upon dismissal or not depends on many factors. Some organizations have a collective agreement that stipulates additional cases of assigning severance pay.

Useful video

The recorded earnings should include those payments to the employee that are assigned in the billing period and that are related to the employee’s work function. That is, salaries and bonuses should be taken into account; sick leave and maternity benefits, payment for business trips and vacations, and financial assistance should not be taken into account.

A reduction in production volumes, sales of products, goods and services inevitably leads to the need to reduce the number of personnel. Which categories of citizens are preferable and painless to dismiss? When a pensioner is laid off, is a benefit paid, and in what amounts is it tax deductible? – questions that arise for employers.

Severance pay is recognized as compensation in cases documented. Payment cannot be provided for dismissal at the initiative of the employer in accordance with the definition of the Supreme Court of the Russian Federation No. 5-KG 13-125 dated December 6, 2021. On this basis, a veiled severance pay to pensioners in case of staff reduction, formalized on paper as a payment by agreement of the parties, is considered illegal. This applies not only to preferential taxation, but can be interpreted as a violation of constitutional rights, since a pensioner has equal rights along with other categories of citizens.

Procedure for calculation and taxation

Termination of a fixed-term or open-ended contract under this article is mutually beneficial for both participants. Personnel changes include the veiled dismissal of retirees due to staff reductions, and compensation in the amount of several salaries significantly improves the financial situation compared to the payment of 2 salaries due directly upon reduction. Judicial practice in relation to the payment of compensation in the amount of the 3rd salary in the absence of employment is ambiguous, since receiving a pension, according to the courts, is nothing more than a benefit that protects against unemployment.

It is necessary to follow a certain algorithm of actions: first, you must put the agreement reached that the employee is leaving by mutual agreement in writing. When drawing up the document, the participation of the employee himself is allowed; he has the opportunity to offer more favorable conditions, including payment of compensation and its exact amount. It is advisable to indicate the following details in the agreement:

And yet: how to resign by agreement of the parties without problems for all participants in the process, if there are some specifics? The procedure for such termination of labor obligations is reminiscent of the procedure for terminating an employment contract at the citizen’s own request, but there are differences. Specifics of the process of terminating a contract on this basis:

Benefits and risks for the employer

In Russia, legislation provides the parties to an employment contract with the opportunity to separate by mutual consent. This method of terminating the relationship between an employee and an employer differs from dismissal at the employee’s own request. Article 78 of the Labor Code provides for such grounds for termination of a contract as dismissal by agreement of the parties. This option for ending cooperation is optimal if the relationship does not work out and is beneficial for each party.

We recommend reading: Certificate of Death According to Form No. 33 or No. 11

The amount of compensation upon dismissal, upon mutual agreement of the parties, must be fixed in the relevant written agreement. The law does not establish a strict amount of severance pay. Based on this, the employer has the right, when establishing it, to be guided by local documents or to specify the amount in the agreement on termination of the employment contract.

Compensation upon dismissal by agreement of the parties

Include the costs of paying employees severance pay, average earnings for the period of employment and compensation upon dismissal as part of labor costs. Moreover, expenses can include both benefits paid in accordance with labor legislation and additional compensation provided for in an employment or collective agreement. This follows from paragraph 1 and paragraph 9 of Article 255 of the Tax Code of the Russian Federation and is confirmed in the letter of the Ministry of Finance of Russia dated January 30, 2015 No. 03-03-06/1/3654. We are a municipal unitary enterprise, a common taxation system. Profit only at the end of the year. During the year, we fired people under the “Agreement of the Parties” (that’s what the order said and there is a signed agreement with each employee). We made the payment from account 91.2 “Other expenses”. The payment was made in a lump sum, in the amount of 2 or 3 times the average salary of the employee. Can we take these expenses into account in tax accounting and attribute them to profit in account 91.2 (NU)?

Please note => What should bank borrowers with a revoked license do?

Accounting for transactions with accountable persons

An accountable person is an employee who receives funds on account for travel and business expenses. For accounting purposes of transactions with these employees, account 71 “Settlements with accountable persons” is used. Amounts issued for reporting are reflected in debit, written off - in credit.

The head of the enterprise approves the lists of persons to whom money is given on account, and sets a deadline for the return of excess funds. Accountable persons undertake to draw up an advance report (no later than 3 days upon return from a business trip). The unspent balance is returned to the organization, overspending is paid to the employee. If the accountable person has not provided an advance report, or the excess funds have not been returned, then these amounts are withheld from his salary.

Basic wiring:

- The accountable amount was issued: Dt 71, Kt 50 (51).

- Write-off of accountable funds (for corresponding expenses or surplus): Dt 44 (10, 50, 51 ...), Kt 71.

Severance pay upon dismissal by agreement of the parties

A frequent condition for dismissal by agreement of the parties is the payment of compensation to the employee, while the amount of such payment is not regulated - neither minimum nor maximum, payment is made in the amount agreed upon by the parties. To formalize the payment, there is no need to indicate the amount in the dismissal order, but the amount of payment must be indicated either in the local act, or in the employment contract, or in the termination agreement. In addition to dismissal at the initiative of the employee or employer, the employment contract may be terminated by agreement of the parties in accordance with Art. 78 of the Labor Code of the Russian Federation at any time and on the terms agreed upon by the parties. Often the parties agree on the payment of severance pay upon dismissal by agreement of the parties.

Peculiarity

Dismissal by agreement of the parties with payment of compensation to the employee takes place on a voluntary basis, without recording facts of violations or other grounds that entail more negative consequences than positive ones. Speaking about termination of work as a result of an agreement, an important point is payments upon dismissal by agreement of the parties, since depending on the initiator and the circumstances of the dismissal, it will be determined whether compensation will be accrued or not, and if so, in what amount. The possibility of receiving compensation upon dismissal by agreement of the parties will be related to the grounds, procedure and timing.

Compensation upon dismissal

Since the agreement of the parties involves the dismissal of a person at his request, and not in connection with a violation, it is almost impossible to deprive him of payments. However, in practice, there are situations when an employer allows a person to leave his job at his own request so that he can preserve his reputation, but at the same time refuses to pay him compensation, since violations still occurred. The main thing here is to prove that the misconduct still occurred, regardless of what dismissal procedure was used. This will avoid paying compensation of any kind.

If the employer has not fixed the amount of severance pay either in the local regulations of the organization or in the employment contract, then the employee does not have the right to request it upon dismissal. Then he can only count on mandatory payments.

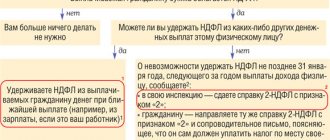

According to paragraph 3 of Art. 217 of the Tax Code in 2021, the amount of severance pay not exceeding 3 times the average monthly earnings is exempt from personal income tax. Thus, upon dismissal by agreement of the parties and the amount of 3 salaries is established as such a benefit, the accounting department should not calculate and withhold income tax from it.

On accounting for expenses of payments made upon dismissal of an employee by agreement of the parties

In connection with the business reorganization, agreements were concluded with employees of the CJSC on the termination of employment contracts (including those that are an integral part of the relevant employment contracts), which stipulated the date of dismissal and the amount of payment associated with dismissal. The workers were dismissed on the basis of paragraph 1 of Article 77 of the Labor Code of the Russian Federation (dismissal by agreement of the parties). This legal position was developed in the Resolutions of the Federal Arbitration Court of the Moscow District dated August 22, 2013 in case No. A40-147336/12-115-1029 and No. F05-14514/2013 dated November 20, 2013, which directly applied it to the payment of compensation upon dismissal of employees due to agreement of the parties.

Results

Dismissal by agreement of the parties today is perhaps the most popular basis for terminating an employment relationship. What should you remember when dismissing an employee on this basis?

- In case of disputes with employees, it is important to have evidence that both parties acted by mutual consent.

- When drawing up an agreement to terminate a contract, it makes sense to determine the amount of compensation and fix the procedure for transferring cases. When setting the amount of compensation, take care of the economic justification for the costs in order to avoid disputes with the tax authorities.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Payment of severance pay upon dismissal by agreement of the parties

The payment of severance pay to an employee upon dismissal by agreement of the parties is not directly mentioned in this article, however, taking into account Part 4 of this article, the employment contract may provide for other cases of payment of severance pay and other compensation payments, as well as establish increased amounts of severance pay. In a similar way, taxation is carried out on severance pay paid upon dismissal to employees of an organization on the basis of an agreement to terminate the employment contract, which is an integral part of the employment contract (letter of the Ministry of Finance of Russia dated June 19, 2014 No. 03-03-06 /2/29308).

Salary deductions

The task of accounting is to calculate salaries, accrual and deductions from it. The law does not limit the list of deductions from an employee’s salary, but the main ones include:

- personal income tax;

- according to executive documents;

- compensation for damage caused to the organization;

- union dues;

- on loans received;

- to repay advances;

- on transfers of insurance premiums to personal insurance, etc.

The total amount of deductions should be no more than 20% of the salary, and in the case of deductions based on executive documents, no more than 50%. However, when collecting alimony for minor children, when compensating for damage to health caused by a crime, as well as associated with the death of the breadwinner, the amount of deductions should be no more than 70%.

Deductions from wages are reflected by posting: Dt 70, Kt 68 (76, 73...)

Accounting for severance pay upon dismissal of an employee by agreement of the parties

In labor costs, the employer can include any accruals to employees in cash or in kind, incentive accruals and allowances, compensation payments related to work hours or working conditions, bonuses and one-time incentive accruals. A different situation arises with the imposition of insurance contributions on severance pay when an employee is dismissed by agreement of the parties. In accordance with subparagraph “e” of paragraph 2 of part 1 of Article 9 of the Federal Law of July 24, 2009 No. 212-FZ, all types of compensation payments established by law (within the limits of norms) associated with the dismissal of employees are not subject to insurance premiums, with the exception of compensation for unused vacation.

Please note => Public Land In St. 2019

Checking mutual settlements

Mutual settlements with an employee

You can check mutual settlements with an employee using the report Balance sheet for the account “Settlements with personnel for wages” in the Reports section - Standard reports - Account balance sheet.

It is logical to generate the report on the date of dismissal: in our example it is September 19. However, entries in accounting for calculating compensation and wages upon dismissal in the account “Settlements with personnel for wages” were generated only on September 30. Therefore, the report must be generated on this date.

The report shows that there is no debt to the dismissed employee at the end of the month.

Mutual settlements with the budget for personal income tax

To check the calculations with the budget for personal income tax, you can generate the report Analysis of account 68.01 “Personal income tax when performing the duties of a tax agent” in the section Reports - Standard reports - Account analysis.

In our example, payment of compensation and wages was carried out on September 19, the deadline for transferring personal income tax was September 20, i.e. the day following the day of payment. But in the accounting system, under the credit of account 68.01 “Personal income tax when performing the duties of a tax agent,” personal income tax, like wages, was accrued on September 30.

The absence of a final balance in account 68.01 “Personal income tax when performing the duties of a tax agent” means that there is no debt to pay personal income tax to the budget.

The accountant is used to this report, but it does not give an up-to-date picture of mutual settlements with the budget for personal income tax, since data on withheld and transferred personal income tax is accumulated in personal income tax registers, and not in accounting accounts. Therefore, we recommend that you use the report Control of personal income tax payment deadlines . In our opinion, it is more informative.

Control of personal income tax payment deadlines

To check the calculations with the budget for personal income tax, as well as the deadlines for payment, you can generate a report Control of deadlines for personal income tax payment in the section Salaries and personnel - Salary - Salary reports - Control of deadlines for personal income tax payment.

In our example, payment of compensation and wages was carried out on September 19, the deadline for transferring personal income tax was September 20, i.e. the day following the day of payment. We will generate a report for the period September 19-20 for Kolokoltsev I.F. To generate the necessary data, use the Settings to set:

- View - Advanced .

Selections tab by clicking the Add selection :

- Field - Individual ;

- Condition - Equal to ;

- Meaning - Kolokoltsev Ivan Fomich ;

- — In the header of the report.

Fields and sorting tab - do not change the existing settings.

Structure tab on the Add :

- Grouped fields - Recorder , check the box.

After completing the setup of the Personal Income Tax Payment Deadline Control , you must click the Close and generate . The program will generate a report.

- Write-off from the current account dated 09.19.2019 N 5 - a document of payment to the employee of amounts upon dismissal, established the deadline for paying the debt to the budget - 09.20.2019.

- Write-off from the current account dated September 19, 2019 N 6 - personal income tax payment document, repaid the debt to pay tax to the budget.

The absence of a final balance on the personal income tax payment due date indicates that personal income tax was paid to the budget on time.

Test yourself! Take a test on this topic using the link >>

See also:

- Salary settings in 1C

- Payroll

- Accrual of vacation pay

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

- Payroll Let's consider the features of calculating wages and insurance premiums in 1C....

- Test No. 60. Compensation for unused vacation upon dismissal...

- Amounts of the minimum wage, benefits, insurance premium rates in 2018-2020 Amounts of the minimum wage, benefits, insurance premium rates in 2018-2020...

- Accrual of vacation pay Let's consider the features of reflecting in 1C the accrual and payment of vacation pay to an employee....

Dismissal by agreement of the parties to personal income tax

It should be clarified that the severance pay (three salaries) will not be calculated from a specific amount (for example, received last month), but on the basis of average earnings calculated for the year (that is, the average annual salary multiplied by three). In general, upon dismissal, an employee may qualify for the following payments: It is legislated that in the event of dismissal, the employee will be paid 3 months' salary, plus compensation payments. However, this causes a lot of controversy and doubt, therefore, regarding the taxation of severance pay, it is limited to the fact that personal income tax is levied on that part of the funds that exceeds the amount of three times earnings. If a particular payment is higher than your average salary multiplied by three, then paying tax cannot be avoided.

Income tax on salary

The organization acts as a tax agent. It is obligated to pay personal income tax for its employees (13% and 30% for residents and non-residents, respectively). When determining the amount of tax, you need to remember that employees have the right to apply tax deductions:

- standard (for children, as well as various categories of persons defined in Article 218 of the Tax Code of the Russian Federation);

- social (for treatment, training, charity and voluntary pension provision);

- property (related to the sale and acquisition of property);

- professional.

Example. The employee received a salary of 35,000 rubles. He is a widower and has two school-aged children. The standard deduction for children is 1400 + 1400 = 2800, and since the employee is a widower, these deductions are doubled and will amount to 5600. The tax base will be calculated as 35,000 - 5600 = 29,400 rubles, the tax amount will be 29,400 * 13% = 3822 rubles.

Compensation for dismissal by agreement of the parties

However, in most cases, employers prefer to issue a document signed by the employee. The agreement then carries an additional informational and legal burden, and in addition to the main provisions, it fixes the procedure for transferring cases, determines the amount of compensation, etc. However, in practice there are many lawsuits, as a result of which employees were denied payment of severance pay, even when they were determined employment contract. For example, if a company goes bankrupt, judges recognize such terms of an employment contract as invalid. You should not provide an excessively high amount of compensation upon dismissal. This type of compensation does not create additional motivation for work; therefore, the court may refuse to pay an employee if there are negative financial consequences for the enterprise proven by the employer.

Dismissal by agreement of the parties: we part amicably

All that is required to carry out dismissal by agreement is the will of the employee and the employer, documented. Moreover, the entire procedure can take only one day - if the day the agreement is drawn up is the day of dismissal. Neither the employer nor the employee is required to notify each other in advance of their intention to terminate the employment contract. In addition, the employer does not need to notify the employment service and the trade union. Thus, it is obvious that it is much easier for an employer to “part” with an employee by agreement than, for example, by reducing numbers or staff. Such an agreement between the employee and the employer is the basis for dismissal, so it must be documented. However, the form of the dismissal agreement is not regulated, that is, the parties have the right to draw it up in any form. The main thing is that this document must contain:

Benefits and risks for the employer

First of all, we note that there is no conflict with the outgoing employee, who receives an absolutely neutral entry in the work book, as well as additional cash payments. Consequently, the chances of future complaints and litigation are reduced (especially if the “compensation” is paid on time and in full).

We invite you to familiarize yourself with Dismissal due to staff reduction 2021: payments and compensations

If they do appear, then the fact of the stability of the agreement, mentioned as a “minus” for the employee, as a basis for dismissal, turns into a “plus” for the employer. If this document is properly executed, the employee’s chances of being reinstated at work (and therefore receiving payment for forced absence and moral damages) are not great.

However, we cannot say there is a complete absence of risks in the event of termination of the employment relationship by agreement of the parties. Thus, if an employer delays payment of the amounts specified in the agreement, he faces a fine under Part 6 of Article 5.27 of the Code of Administrative Offenses of the Russian Federation (for legal entities - up to 50 thousand rubles, for individual entrepreneurs - up to 5 thousand rubles).

https://www.youtube.com/watch?v=ytcreatorsru

Also, the fact that dismissal occurs “by agreement” does not mean that the employer will not be responsible for violations committed when preparing the relevant personnel documents (dismissal order, work book, etc.). In this situation, a fine can be assessed under Part 1 of Article 5.27 of the Code of Administrative Offenses of the Russian Federation (for legal entities - up to 50 thousand rubles, for individual entrepreneurs - up to 5 thousand rubles).

Create a staffing schedule for free using a ready-made template

There are advantages to dismissal by agreement of the parties and for the employer:

- simplicity of the dismissal procedure;

- lack of obligation to indicate the reason for termination of cooperation;

- the ability to minimize the negative consequences of parting with an unwanted employee (especially when there is a risk of leaking valuable information);

- the opportunity to negotiate the most convenient conditions for both parties;

- the opportunity to reduce staff in this way and get rid of an unwanted employee;

- challenging such an agreement in court is quite problematic.

The only risk is that pregnant women have the right to withdraw their own application, according to judicial practice.

Pregnant women

Payments and compensation upon dismissal by agreement of the parties

The employer, in accordance with the agreement, regulates the amount of compensation payments when there is mutual agreement to terminate the employment contract. He has the right not to determine any benefits. By law, an employee receives only those payments that are stipulated in labor legislation. Such an agreement cannot be terminated unilaterally. But when a new contract is drawn up, the old one becomes invalid. When a specialist quits in this way, he is not required to work for two weeks in his old place. Termination takes place very quickly, within 24 hours, but only when this is stipulated in the concluded contract. In any case, the final decision on working time is made by the employer.

Procedure

The relations between employees and the organization where they are employed are regulated by the Labor Code. The possibility associated with the termination of relations on such a basis as an agreement of the parties is provided for in Article 78 of the said act.

Legislation

Through local acts, the issue regarding the transfer of affairs by the chief accountant can be resolved. This is due to the fact that the issue under consideration is not regulated by the legislator. According to general provisions, when implementing the process you will need to do:

It is almost impossible to challenge such a dismissal in court. It is impossible to revoke or terminate an already concluded agreement unilaterally. For example, if an employee changes his mind about resigning, the employer has the right to refuse him.

Dismissal by agreement of the parties: procedure, compensation

- Agreement with the signature of each party;

- Details of an open-ended or fixed-term employment contract that must be terminated;

- The date of the employee’s last working day and, accordingly, the end date of the employment relationship;

- The amount of compensation due to the employee in accordance with labor legislation and the organization’s charter;

- Date and place of signing the agreement. Without these details, the document is not recognized as valid;

- Employee details: full name and position;

- Full name of the employing company;

- Indication of the organizational and legal form of the employing organization;

- Details of the person authorized to sign securities (director, head of the human resources department, authorized representative, etc.): full name and position;

- employer's tax identification number;

- Signatures of the parties to the agreement and their transcripts.

An important feature of this process is voluntariness. That is, neither party has the right to force the other to make an appropriate decision. An attempt at such coercion is criminally punishable if the coerced party applies to the appropriate authorities.

21 Dec 2021 marketur 127

Share this post

- Related Posts

- For which offense can you get 4 years under Article 228?

- Statement of claim for payer code section

- Are deposits in B&N bank insured in SSV

- PFR number according to the tax identification number of the legal entity online

Delivery of documents

All work-related documents (work book, extracts from SZV-M, RSV and SZV-STAZH, salary certificate, etc.) are issued to the employee directly on the day of dismissal, that is, on the last working day. If the provision for the issuance of such documents is included in the text of the dismissal agreement, it is advisable to obtain a signature from the employee on the copy of the agreement that remains with the employer. This will confirm the timely transfer of the relevant papers to the dismissed employee.