A sales receipt without a cash receipt is valid in 2021

The sale of goods for cash is usually confirmed by issuing a cash receipt to the buyer. When using online cash registers, the required details of the cash register receipt contain all the necessary information about the seller and the goods sold (name, price, value). Therefore, drawing up a sales receipt at the same time as the cash register receipt is not required. What if the cash receipt is not issued or is lost? Is a sales receipt valid without a cash receipt?

However, there are no requirements for a sales receipt to confirm the fact of purchase in consumer protection cases. There may even be no sales or cash receipts at all. In this case, the fact of purchase can be confirmed by testimony (clause 5 of article 18, clause 1 of article 25 of the Law of the Russian Federation dated 02/07/1992 No. 2300-1).

Why can you recognize expenses if there are no additional details in the check?

However, costs can be justified using other documents, in particular, the director’s order to issue money for certain needs and the employee’s advance report. And if you attach a cash register check issued to an employee to this set, then the accounting department has the right to write off expenses, despite the absence of the buyer’s TIN and other new details in the check.

Keep records and prepare reports for the simplified tax system and UTII for free

Thus, in July 2021 and beyond, organizations and entrepreneurs may still not issue powers of attorney to accountables and accept cashier’s checks issued to individuals from them. The absence of additional details in the check provided by Law No. 54-FZ is not an obstacle to writing off expenses.

The main thing is that the economic feasibility of the purchase is reflected in other documents, including the expense report.

Please note: you can fulfill the requirements of the current version of Law 54-FZ for the details in the cash receipt using the “Kontur.Market” service. The service also ensures the transfer of data on punched checks to the INFS through the OFD. In addition, “Kontur.Market” is integrated with the service for maintaining records and submitting reports “Kontur.Accounting”, which allows you to quickly and accurately reflect sales data in tax and accounting.

How often does the accounting department of an enterprise require its employees, when purchasing certain goods for cash or by bank transfer, to provide a sales receipt along with other documents? What kind of form is this, is it really necessary for accounting operations?

VAT deduction on a cash receipt: is it possible without an invoice?

To avoid problems with the Federal Tax Service, whose inspectors refuse to deduct VAT in the absence of an invoice at the time of the on-site inspection, it is better to carry out the purchase and sale operation in special contract departments of retail stores

– specialists will issue an invoice, cash receipt order or invoice to the buyer who paid in cash. When the VAT amount is highlighted as a separate line in the listed documents, VAT can be deducted.

A common situation was considered. An employee is given money on account for the purchase of office supplies, for example. There is no invoice. The employee draws up an advance report and attaches a cash receipt with the VAT amount highlighted on a separate line. The company is wondering whether the accountant has the right to deduct VAT. If this is not possible, then can VAT be included as an expense when calculating the taxable base for income tax?

How to fill out the document correctly?

Typically, trading enterprises have in stock forms of sales receipts in order to provide them to the buyer at any time upon his request. Most often, representatives of enterprises (organizations) make such demands. Any seller should know how to fill out a sales receipt: this can be done in two ways:

- Using computer technology. This is done if the store (outlet) keeps records of the receipt and consumption of products in electronic form. The employee only has to enter the name and quantity of the goods selected by the buyer. The remaining data will be automatically entered into the printed form.

- Manually. In this case, all the necessary information is carefully entered into a standard form document.

All products are entered one by one into a special table. If there are products of the same type at different prices, each of them goes on a separate line. For example, “pencil at a price of 10 rubles per piece” and “pencil at a price of 15 rubles per piece.”

You cannot write “2 pencils worth 25 rubles.” Each product of the same article (or variety) and its price must be recorded separately.

After the table with the selected products, the total cost of the purchase is written down in numbers and in words. Finally, the seller’s details are indicated, his signature and the seal of the trading company are affixed.

If it is missing, then you should not replace it with various stamps. The law allows you to draw up a document without a seal, if it does not exist at all.

sales receipt

Expert opinion

Kuzmin Ivan Timofeevich

Legal consultant with 6 years of experience. Specializes in the field of civil law. Member of the Bar Association.

The sale of goods and the provision of services to individuals is documented by documents such as a cash receipt, sales receipt and BSO. Let's figure out what these documents are, in what cases each of them is needed, and when you can not issue anything to buyers.

You can receive goods using a cash receipt from 2021

For your information: We consider it necessary to note that a specific list of primary accounting documents to confirm expenses is not provided for by tax legislation (letter of the Federal Tax Service of Russia for Moscow dated March 22, 2021 N 16-15 / [email protected] ). In particular, tax legislation does not require the presence of a seller’s cash receipt to confirm the institution’s expenses. The letter of the Ministry of Finance of Russia dated July 18, 2021 N 03-01-15/50059 emphasizes the presence of three stages of the transition to online cash registers, which implies the mandatory availability of cash register receipts of a new type for all organizations and individual entrepreneurs only from July 1, 2021. Previously, during the period of validity of the old version of Law N 54-FZ, there was judicial practice that was positive for taxpayers. In the decisions of the Federal Antimonopoly Service of the Moscow District dated April 2, 2021 N KA-A40/2846-10 in case N A40-48569/08-14-170, the Eleventh AAS dated January 20, 2021 N 11AP-21855/13, the judges note that the Tax Code of the Russian Federation has not been established a list of documents that must be prepared when the taxpayer carries out certain expense transactions. Therefore, when deciding whether it is possible to take into account certain expenses for the purposes of calculating income tax, it is necessary to proceed from whether the documents submitted by the taxpayer confirm the expenses incurred by him or not. That is, the condition for including incurred costs as expenses is the ability, based on available documents, to make an unambiguous conclusion that the expenses were actually incurred. In turn, in the resolution of the Federal Antimonopoly Service of the North-Western District dated 02/18/2021 N A56-52410/2021, the judges directly stated that cash register receipts are not the only documents confirming travel expenses for hotel accommodation. In order to avoid tax risks, the taxpayer may, on the basis of clause 1 of Art. 34.2 of the Tax Code of the Russian Federation and clause 1, clause 2 of Art. 21 of the Tax Code of the Russian Federation, contact the Ministry of Finance of Russia or the tax authority at the place of registration of the organization to receive written clarification on this issue. Let us remind you that in accordance with Art. 111 of the Tax Code of the Russian Federation, the taxpayer’s compliance with written explanations given to him by a financial or tax authority on the procedure for calculating, paying a tax (fee) or on other issues of applying the legislation on taxes and fees is a circumstance that excludes the person’s guilt in committing a tax offense. In this case, the taxpayer is not liable for committing a tax offense.

We recommend reading: Supsidia Crimea Free for Young Family

Rationale for the conclusion: From July 3, 2021, Federal Law No. 54-FZ dated 22.05.2021 “On the use of cash register equipment when making payments in the Russian Federation” (hereinafter referred to as Law No. 54-FZ) is in force in the wording established by the Federal Law dated 07.03. .2021 N 192-FZ (hereinafter referred to as Law N 192-FZ), with the exception of certain provisions. Please note that previously significant amendments to Law No. 54-FZ were introduced by Federal Law dated July 3, 2021 No. 290-FZ (hereinafter referred to as Law No. 290-FZ) and Federal Law dated November 27, 2021 No. 337-FZ. In accordance with paragraph 1 of Art. 1.2 of Law No. 54-FZ, cash register equipment (hereinafter referred to as CCT), included in the register of cash register equipment, is used on the territory of the Russian Federation without fail by all organizations and individual entrepreneurs when making payments, except in cases established by Law No. 54-FZ. However, the right of some persons to make cash payments and payments using payment cards without using cash registers has been extended until July 1, 2021. For example, organizations (on PSN and UTII) and individual entrepreneurs (on PSN) engaged in the provision of veterinary and household services, repair services, maintenance and washing of vehicles, as well as those engaged in advertising will be able to continue to work without a cash register after July 1, 2021 using the external and internal surfaces of vehicles (part 7.1 of article 7 of Law N 290-FZ). Types of activities for which CCP may not be used are listed in paragraphs. 1-14 p. 2 tbsp. 346.26 Tax Code of the Russian Federation, paragraphs. 3, 6, 9-11, 18, 28, 32, 33, 37, 38, 40, 45-48, 53, 56, 63 p. 2 art. 346.43 Tax Code of the Russian Federation. The specified organizations and individual entrepreneurs are required to issue a document to the representative of the institution: a sales receipt, receipt or other document confirming the receipt of funds for the relevant product (work, service) in the manner established by clause 2.1 of Art. 2 of Law No. 54-FZ as amended in force until July 15, 2021 (Part 7.1 of Article 7 of Law No. 290-FZ). This document must contain its name, serial number, details established by paragraphs four to twelve of paragraph 1 of Art. 4.7 of Law No. 54-FZ. The title of the document is not regulated by law. In addition, until July 1, 2021, organizations and individual entrepreneurs using PSN and UTII, performing work that provides services to the population (with the exception of organizations and entrepreneurs that have employees with whom employment contracts have been concluded, providing public catering services), have the right not to use CCP when provided that they issue the appropriate strict reporting forms (SRF) in the manner established by Law No. 54-FZ (as amended). Please note that persons applying UTII and PSN are not required to provide clients with information about the applicable taxation system, but the institution can obtain such information from the tax authorities. To obtain information about the taxation system used by the counterparty, it is necessary to submit to the tax authority at the place of registration of the counterparty an application drawn up in any form indicating the required information. The deadline for providing a response by the tax authority is set within 30 calendar days (Article 12 of Federal Law No. 59-FZ dated 02.05.2021). In this case, no state duty is paid. The institution independently has the opportunity to check that when carrying out specific activities in a certain territory, it is generally possible to use UTII, that is, whether UTII has been introduced by the relevant regulatory legal acts of representative bodies of municipal districts, city districts, laws of federal cities of Moscow, St. Petersburg and Sevastopol (clause 1 Article 346.26 of the Tax Code of the Russian Federation). It is also necessary to check that the relevant type of activity is named in paragraph 2 of Art. 346.26 of the Tax Code of the Russian Federation and the conditions of Art. 7 or parts 7.1 of Art. 7 of Law No. 290-FZ.

Answers to frequently asked questions

Question No. 1: Is it necessary to maintain accounting using the simplified taxation system “DMR”?

No, an individual entrepreneur who has chosen the simplified taxation system “DMR” is not obliged to do this.

Question No. 2: How can I confirm air travel?

For this purpose, you should use all documents that are directly or indirectly related to air travel. At a minimum, this should be: an air ticket, a boarding pass. They must be accompanied by documents that will justify the trip (air travel) and justify its purpose. For example, a travel certificate, a business trip order.

You can receive goods using a cash receipt from 2021

The Ministry of Finance examined this situation and made conclusions: a cash receipt can be accepted for accounting as a primary document without supporting documents if it contains the following details: name of the document, content of the transaction, amount, date, full name of the employee, and most the main thing is the signature of the person in charge (seller).

Due to the entry into force of the new Accounting Law, a cash receipt may be the primary document for writing off expenses if it meets certain requirements, i.e. will contain all the necessary details on the basis of which this document can be recognized as primary.

Electronic boarding pass

Include payment for travel for business travelers in tax expenses based on a printed electronic ticket or boarding pass (letter of the Ministry of Finance No. 03-03-06/1/4908 dated January 28, 2020).

If an electronic ticket is lost, the flight costs will be confirmed by a certificate from the airline that the business traveler flew on the flight indicated on the ticket. If there is no certificate, the Ministry of Finance allows you to justify the expenses with a ticket and documents indirectly confirming the flight (letter of the Ministry of Finance No. 03-03-05/12957 dated February 28, 2019) - a mark in the passport, etc.

Is a sales receipt valid without a cash receipt for individual entrepreneurs and LLCs?

All this information is necessary in order to determine exactly where the product was purchased, as well as to establish the exact date and time of the purchase transaction. Also, the contents of the check help the government agency that monitors compliance with tax laws to monitor compliance with the rules of individual entrepreneurs. Advertising is allowed on the site, but only if the basic details are readable . If it is noticed that some props are not visible well enough, you need to stop the operation of the device.

We recommend reading: Sample application to a management company for window repairs

The fact of providing the FC when returning damaged goods will make your life much easier and relieve you of the burden of providing evidence that the goods were purchased directly from that place. Current legislation does not oblige you to return goods only if you have a control certificate, but its presence will make your life much easier.

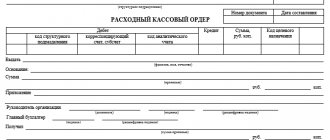

Cash receipt

What is a sales receipt? When purchasing goods, sellers issue buyers a cash receipt confirming the fact of payment for the goods, and in cases established by the rules of trade, a sales receipt confirming the fact of transfer of the goods. Apart from these two types of checks (commodity and cash), there are no others in commercial practice. Therefore, talking about a sales receipt is not entirely correct.

The answer to this question is debatable. There is a position of the Federal Tax Service of Russia, communicated in a letter dated June 25, 2021 N ED-4-3 / [email protected] , in which the tax authorities explained that the cash receipt does not contain all the required details of the primary document and only confirms payment for the goods. In particular, the name of the position and the signature of the person (seller) who performed the business transaction are missing. In this case, the cash receipt is issued to an accountable person, and not to an organization or individual entrepreneur, therefore, there must be other primary documents.

Businessman's responsibility

Entrepreneurs who do not provide the buyer with a sales receipt are considered offenders within the framework of administrative law (Article 14.5 of the Code of Administrative Offenses of the Russian Federation). Punishment may be applied to them. Sanctions – fine or warning.

This norm provides in the objective part - non-use of cash registers, use of an unregistered fiscal apparatus, violation of the procedure for conducting settlement transactions, etc. Liability – a fine of up to 40 thousand rubles (for organizations). For individual entrepreneurs, the amount of sanctions is much lower - up to 2 thousand rubles.

A sales receipt and a cash receipt are not the same accounting acts. A common feature is the transfer of a document to a buyer or client in retail trade to confirm the fact of the transaction and its payment. Each paper has its own meaning.

A sales receipt can be issued without a cash receipt, when the seller has the right not to use a cash register. Otherwise, it is illegal.

A sales receipt is an attachment to the main document that lists all purchased services and goods. We meet them every day, but not all buyers and sellers fully understand their purpose and importance.

Is a cash receipt suitable instead of a primary document for expenses?

Some categories of sellers have the right not to use cash register systems when making cash payments or payments using payment cards. These categories, in particular, include (clause 2.1 of Article 2 of the Federal Law of May 22, 2003 No. 54-FZ, hereinafter referred to as the Law on CCP): - organizations and individual entrepreneurs using UTII when selling goods, works, activities; - entrepreneurs who have switched to a patent taxation system when carrying out activities to which this system is applied.

In turn, this employee reports to the organization for the money spent by drawing up and submitting to the accounting department an advance report with attached cash and sales receipts, receipts for cash receipts, strict reporting forms and other documents confirming the fact of payment. It is on the basis of an advance report and sales receipts, not cash receipts, that the company takes into account inventory items purchased for it by an employee in cash. Cash receipts, receipts for cash receipt orders, strict reporting forms and other similar documents confirm only the fact of payment of goods and materials. Therefore, the Federal Tax Service of Russia came to the following conclusion (letter dated June 25, 2013 No. ED-4-3/ [email protected] ). The company has the right to confirm the expenses incurred with a cash receipt, however, to account for expenses for tax purposes, along with the cash receipt, other primary documents are required that indicate the connection of the expenses incurred with the organization’s activities aimed at generating income.

Carrying out payments without a cash register

Conducting cash transactions is not always convenient for the seller due to the following circumstances:

- purchasing a cash register is an additional expense;

- the need to report to the tax office and register the cash register;

- compliance with all formalities when creating accounting documents;

- salesperson training, etc.

That is why an individual entrepreneur may be interested in the possibility of making payments without a cash register. These actions are legal only in cases provided for by law. For example, when working for UTII, an entrepreneur issues clients not a cash receipt, but a BSO.

Calculations without cash registers are related to the procedure for taxation, work in specific market sectors, and a specific place of residence of the individual entrepreneur.

When a sales receipt is issued: specifics of application in the context of Law No. 54-FZ

Along with Law No. 54-FZ, the main one that regulates payments in retail trade, there is another noteworthy regulatory act - Decree of the Government of Russia dated January 19, 1998 No. 55 “On approval of the Rules for the sale of certain types of goods” (LINK).

Such sellers include, in particular, individual entrepreneurs and legal entities that pay UTII. Until July 1, 2021, they are given the opportunity not to use online cash registers, subject to the issuance of sales receipts - instead of cash receipts - to customers.

The legality of issuing PM without a cash register

The issuance of sales receipts instead of cash receipts is allowed for individual entrepreneurs on UTII if they meet the requirements for BSO. These actions will be legal if the individual entrepreneur is relieved of the obligation to use the fiscal apparatus when making payments.

In this case, the CN is equal to the PM and the importance of the specified information increases. PM is the only way to prove the fact of a purchase.

Rules for issuing a sales receipt in the absence of a cash register:

- The presence of mandatory details, since otherwise the legal force of the document is lost.

- Advertising on the reverse side should not overlap the official information on the PM.

- Each unit of goods is indicated on a separate line, without generalizations, with a decoding. If this condition is not met, the document may not be accepted by the accounting department.

- The amount under the act is indicated for each item separately and the total in a separate column (in numbers and in words).

- The paper is drawn up in two copies - for the buyer and the seller.

- Blank lines must be crossed out to protect against fraudulent transactions.

An example of the correct execution of a sales receipt:

The Ministry of Finance decided the fate of VAT on a cash receipt

Note that the courts are not so categorical. Thus, the Presidium of the Supreme Arbitration Court of the Russian Federation, in its resolution dated May 13, 2021 No. 17718/07, indicated that, according to clause 7 of Art. 168 of the Tax Code of the Russian Federation, when selling goods for cash in retail trade, the requirements for preparing payment documents and issuing invoices are considered fulfilled if the seller issues the buyer a cash receipt or other document of the established form. Consequently, if payment for goods was made taking into account VAT, the buyer has the right to deduct this tax.

According to the financial department, the company does not have the right to deduct VAT when purchasing goods at retail, even if the tax amount is highlighted on a separate line in the cash receipt. It will not be possible to include VAT as an expense when calculating income tax. This conclusion is contained in the letter of the Ministry of Finance of Russia dated January 24, 2021 No. 03-07-11/3094.

The first point of view: to write off expenses you need a check issued to an organization or individual entrepreneur

The lecturers believe that this letter refers to additional details that have been introduced since July for settlements between companies and individual entrepreneurs. It turns out that if the accountable person does not provide a power of attorney with the details of the organization (or individual entrepreneur), the seller will punch him a check without additional details.

And with the help of such a check it is impossible to justify expenses and reflect them in tax accounting. Consequently, from July 2021, a power of attorney becomes a mandatory attribute when an accountant goes to the store, because without it it is impossible to write off the cost of the purchase as expenses.

Submit income tax reports online for free

In what cases is a sales receipt issued without a cash register, nuances of issuance in 2021

A sales receipt without a cash receipt is valid and confirms payment or purchase of goods. It is used in controversial issues, as security for the rights of the buyer. Also, this document is used to confirm the use of funds for their intended purpose.

- Documentary substantiation of enterprise expenses in fiscal accounting. When generating reports on expenses and profits, documents confirming payment are taken into account.

- Confirmation of the use of funds for specific needs.

- When carrying out purchase and sale transactions among legal entities. The merchant can make demands for repayment of the debt on the basis of such receipts.

- Reimbursement of employee expenses for the needs of the enterprise or payment of travel allowances. Expenses are compensated based on the advance report of the accountable person. Quite often, supporting documents are needed to generate this report.

Specialized form

To begin with, it is worth noting that a sales receipt is a strict reporting form. It is provided to both individuals and legal entities as proof of purchase. This document is issued in two cases:

- If the seller does not have a cash register.

- At the buyer's request, as a transcript of the list of purchased goods.

In the first case, due to the lack of special equipment, the seller cannot issue the buyer a confirmation document in accordance with the requirements of the trade rules, so he is forced to fill out a specially designed form by hand, which contains all the necessary data and details.

In the second case, the situation is somewhat different. There are cash registers that issue a receipt without indicating the type of product. It indicates only the amount paid, which does not provide a comprehensive picture of the fact of purchase and sale.

For an ordinary buyer (individual) this point may be considered insignificant. But for an organization (enterprise), when making accounting entries, it is necessary to clearly indicate the name of the purchased product. In this case, you need a sales receipt, where all the information is present in full.

Do I need a sales receipt for an online cash register receipt?

On the one hand, the online cash register receipt should contain basic information about the item. Resolution of the Government of the Russian Federation No. 745 specified the requirements for the details of a cash register receipt. The check must include:

We recommend reading: Is it possible to turn off water to a gardener in St. Petersburg for failure to pay for water?

On the other hand, Federal Law No. 54, Article 4.7, details new requirements for the details of an online cash register receipt. The need to indicate the value added tax (VAT) rates on the receipt has been added to the basic details. If the receipt contains complete information, then a sales receipt can replace a cash receipt. Accounting outsourcing experts Glavbukh Assistant will help you understand the preparation of primary documentation and record keeping.

Is it necessary to use a cash register for individual entrepreneurs on a simplified basis?

- Retail sales of printed publications (newspapers, magazines, lotteries) and related products.

- Sale of small postal products in remote rural areas.

- Securities trading.

- Until July 1, 2021 – sale of passes directly in public transport (after this date, only drivers or conductors will be able to sell them without a ticket office).

- Catering in educational institutions for employees and students during classes.

- Trade at fairs, exhibitions or markets, but provided that the place of trade does not require the safety of these goods or equipment. Consequently, trading from a table is permissible without cash receipts, and from tents and kiosks, the presence of a cash register is mandatory.

- Sale of drinks from barrels and tanks (milk, beer, kvass).

- Trade without organizing a workplace: kerosene, various vegetable crops and melons, live fish.

- Retail trade of any goods by peddling.

- Sale of literature and other religious items for religious organizations.

- Subject to a special license, pharmacies in rural areas without cash registers are allowed to operate (if there are no other pharmacies there).

- Shoe repair.

- Repair or production of keys and other metal accessories.

- Care services for children, the elderly, and the disabled.

- Folk art craft.

- Sawing wood.

- Plowing land for the population.

- Porter services at any ports and stations.

- Renting your own home.

- Collection of various raw materials for recycling, except metal.

- Beauty salon services.

- Work of travel agencies.

- Services of some car repair shops.

The individual entrepreneur retains a copy of the paper or tear-off spines. Contains documents: serial number, date of sale of the goods, full name of the individual entrepreneur, the essence of the transaction (sale of goods, provision of services), amount, signature with a transcript of the seller. You can develop the forms yourself, but carefully ensure that they contain all the required items.

How to register the purchase of goods through an accountable person

To receive cash against the report, the employee must write an application in any form. Indicate in it the required amount, as well as for what purposes it will be spent. The head of the organization must make an inscription on the application stating what amount and for what period must be issued according to this application.*

The need to draw up such a document is explained by the fact that a cash receipt confirms only the amount that the employee spent. On its basis, it is impossible to take into account values acquired through an employee. The cash receipt does not contain such mandatory details of the primary document as the signatures of the responsible persons (Part 2 of Article 9 of the Law of December 6, 2021 No. 402-FZ, Clause 7 of the Instructions to the Unified Chart of Accounts No. 157n).

How to confirm expenses and avoid problems with the Federal Tax Service?

The position of the tax authorities is clear: a cash receipt only confirms the use of a cash register and the acceptance of funds from a person. It proves that an agreement for the purchase and sale of goods or services was concluded between the buyer and the outlet.

The document can be used to confirm costs without any other “primary” if it contains additional details:

- name of the form;

- the amount of the transaction performed;

- its content;

- date of;

- signature and surname of the responsible person.

A legal entity will not have problems confirming expenses if a bill of lading is attached to the check. It is important to ensure that the name of the company is indicated as the buyer, and not the full name of its employee representative. If you put the name of an individual, the tax authorities will not count such an expense as confirmed.

To give a check “strength” in the eyes of the Federal Tax Service, it is enough to accompany it with an advance report. The latter contains all the information that allows you to determine the direction and economic feasibility of spending money.

If you want to use a cash receipt without “accompaniment” to submit to the tax office, make sure that it contains all the necessary details. The amount, name of the purchased product, name and TIN of the outlet are contained in the document by definition. We need to add a few more significant details to it.

The first is the name. Often it is not in the standard form; care should be taken to ensure that it is written down. There is no need to “reinvent the wheel”: the wording “cash receipt” will be sufficient. The final “touch” is the name and “autograph” of the seller. Most store employees agree to sign a check, although they do not always understand why it is necessary.

If you want to avoid problems with the tax authorities, make sure that the accountable persons of your company accompany cash receipts with invoices or advance reports or take signatures from sellers. A receipt can be used to confirm expenses only if it contains all the details characteristic of a “primary receipt”.

Read more about the required details of a cash receipt in the article.

Similar articles

- Total amount for goods in a cash register receipt - rules for document execution

- Cash receipt details

- How to prepare an expense report without a cash receipt?

- How to check the authenticity of a cash receipt?

- Where is the cash receipt number?

The accountant presented a cash receipt with a list of goods; is it necessary to request a sales receipt?

According to Art. 1.1 of Law N 54-FZ (as amended by Law N 290-FZ), a cash receipt is a primary accounting document generated in electronic form and (or) printed using cash register equipment at the time of settlement between the user and the buyer (client), containing information about the calculation, confirming the fact of its implementation and complying with the requirements of the legislation of the Russian Federation on the use of cash register equipment. This concept is used for the purposes of Law No. 54-FZ (paragraph one of Article 1.1 of Law No. 4-FZ).

Based on the receipt order or act of acceptance of materials, a materials accounting card is filled out (the form can be developed on the basis of the unified form N M-17). All unified forms are approved by Decree of the State Statistics Committee of Russia dated October 30, 1997 N 71a.

ConsultantPlus: Forums

Question: Our organization is engaged in public catering (bar), transferred to the payment of UTII. There is a production need to purchase products frequently and in small quantities. Is it possible to capitalize them on the basis of cash receipts from supermarkets, which indicate the name of the product, quantity, price and purchase amount?

At the same time, we draw your attention to the fact that in accordance with the Guidelines for accounting of inventories, approved by Order of the Ministry of Finance of the Russian Federation dated December 28, 2021 N 119n, materials purchased by the accountable persons of the organization are subject to delivery to the warehouse. The receipt of materials is carried out in the generally established manner on the basis of supporting documents confirming the purchase (invoices and receipts from stores, a receipt for a cash receipt order - when purchasing from another organization for cash, an act or certificate of purchase on the market or from the public), which are attached to the advance payment report of the accountable person.

Individual entrepreneurs using UTII must indicate the name and quantity of goods on the receipt from February 1, 2021

Question: An individual entrepreneur, engaged in wholesale trade, applies a simplified taxation system and carries out non-cash payments under supply contracts, while at the same time, in retail trade, he applies UTII and makes cash payments. From what period should he use online cash registers and indicate the name of the product on the cash receipt?

Answer: In accordance with paragraph 1 of Art. 1.2 of the Federal Law of May 22, 2021 No. 54-FZ (as amended on July 3, 2021) “On the use of cash register equipment when making cash payments and (or) settlements using electronic means of payment” cash register equipment is used on the territory of the Russian Federation Federation is mandatory for all organizations and individual entrepreneurs when making payments, except in cases established by this law. Payment should be understood as the acceptance or payment of funds using cash or electronic means of payment for goods sold, work performed, services provided (Article 1.1 of the Federal Law of May 22, 2021 No. 54-FZ).

Introductory information

Let us remind you that when making payments between two organizations, two individual entrepreneurs, or between an organization and an individual entrepreneur, you need to use cash register equipment in two cases. The first is the acceptance and withdrawal of cash.

Expert opinion

Kuzmin Ivan Timofeevich

Legal consultant with 6 years of experience. Specializes in the field of civil law. Member of the Bar Association.

The second is the acceptance and issuance of non-cash funds using an electronic means of payment with its presentation (for example, using a plastic card).

From July 1, 2021, for such calculations in cash register receipts and strict reporting forms, it is necessary to indicate additional details provided for in the new paragraph 6.1 of Article 4.7 of the Federal Law of May 22, 2003 No. 54-FZ on the use of cash register systems (hereinafter referred to as Law No. 54-FZ). Such details include:

- name of the buyer or client (company name or full name of the entrepreneur);

- TIN of the buyer or client;

- information about the country of origin of the goods (when paying for the goods);

- excise tax amount (for excisable products);

- registration number of the customs declaration (when paying for imported goods).

Complete set for online cash register: cash register at a special price, OFD, cash register setup with registration with the Federal Tax Service and a discounted inventory system Send a request

The question arises: is it possible, starting from July, to accept from the accountable a check issued to him as an individual and include it in the package of documents that confirm the purchase expenses? Or do amendments to Law No. 54-FZ mean that now, in order to account for costs, along with other papers, a check issued to an organization or individual entrepreneur and containing additional details is required?

Experts hold two opposing points of view.