Cash documents are a special type of material assets of an organization, recorded in an active account 50.3. The forms on which monetary documents are printed are accounted for in off-balance sheet account 006. Analytical accounting is organized by type of monetary document. Monetary documents are purchased for non-cash and cash payments. Cash purchases can be made through accountable persons. The reflection of such operations in the organization’s document flow in practice has a number of significant nuances that should be taken into account.

How to take into account monetary documents ?

Organization of accounting of monetary documents

Monetary documents are documents certifying the fact of payment and the right to subsequent receipt of work or services. As a rule, such documents are drawn up on strict reporting forms (SSR).

| 1C:ITS For more information about strict reporting forms of the old and new sample (taking into account the current version of the Federal Law of May 22, 2003 No. 54-FZ), see the “Online cash desks” directory in the “Legal Support” section. |

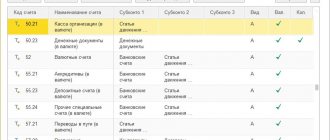

According to the Instructions for the application of the Chart of Accounts for accounting the financial and economic activities of organizations (approved by order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n, hereinafter referred to as the Chart of Accounts), monetary documents located at the organization’s cash desk (paid air and railway tickets, coupons for the disposal of solid household waste (MSW), postage stamps, etc.) are taken into account in subaccount 50-3 “Cash documents” in the amount of actual purchase costs. To account for monetary documents, the value of which is expressed in foreign currency, in “1C: Accounting 8” there is a separate subaccount 50.23 “Cash documents (in foreign currency)”.

On accounts 50.03 and 50.23, the program keeps records both in total and in quantitative terms. Analytical accounting is organized in the context of monetary documents (for this, the reference book Nomenclature of monetary documents is used). For each monetary document its type is indicated:

- Tickets;

- Vouchers;

- Stamps;

- Coupons for fuel and lubricants;

- Other.

When entering information in the card of a monetary document, you can indicate its value, then it will be automatically entered when registering the receipt or issue of the corresponding document.

In order for operations with monetary documents to be available to the user, it is necessary to enable the appropriate functionality of the program (section Main - Functionality). On the Bank and cash desk tab, set the Cash Documents flag (Fig. 1).

Rice. 1. Setting up functionality

After setting the flag in the Bank and Cash Department section of the program, the documents Receipt of monetary documents and Issue of monetary documents, as well as the Cash Documents journal, become available. From the journal you can generate a Report on the movement of monetary documents, which is intended to control received and issued monetary documents. To control the safety and analyze the movement of monetary documents, you can also use standard accounting reports.

The document Receipt of monetary documents is intended to reflect the fact of receipt of a monetary document at the organization's cash desk. In the header of the document you need to indicate the account for accounting of monetary documents (50.03 or 50.23). If you select account 50.23, then you must specify the currency for recording monetary documents. Depending on the method of receipt of the monetary document, the type of operation is selected:

- Receipt from the supplier;

- Receipt from an accountable person;

- Other receipts.

If a Receipt from a supplier is registered, then in the Settlement Account field you must specify the account for settlements with the counterparty.

At the same time, the document Receipt of monetary documents does not provide for simultaneous indication of both the account for accounting of settlements with the counterparty and the account for accounting for settlements for advances. Therefore, it is convenient to use account 76.05 “Settlements with other suppliers and contractors” as a settlement account. The same account should be indicated when reflecting payment to the supplier, then there will be no difficulties with offsetting advances.

For each nomenclature of received monetary documents, their quantity and amount (including taxes) are indicated. VAT is not allocated in the amount of the document, since the fact of receipt of a monetary document is not the fact of acceptance for accounting of goods or services, the right to which the document provides. Goods (work, services) can be taken into account later (for example, when registering an employee’s advance report on a business trip or on the purchase of fuel and lubricants using a coupon), then, as a general rule, VAT is taken into account.

The document Issuance of monetary documents reflects the following types of business transactions:

- Issuance to an accountable person;

- Return to supplier. When making a return, it is necessary to indicate the amount of the return, as well as the account of income or expenses, since the amount of the return may differ from the value of the monetary document;

- Other issue.

Main

Cash documents are a type of material assets that accompanies the movement of funds. Accounted for in account 50.3 at the cost of acquisition, stored in the cash register, according to the rules for storing cash. The movement of monetary documents is documented using standard cash documents, with the mark “stock” on them. The concepts of “monetary documents” and “strict reporting forms” are different in a broad sense. Strict reporting forms can serve as confirmation of already paid monetary documents, however, not all BSO can be monetary documents.

Accounting for fuel and lubricants using coupons

Fuels and lubricants include fuels (gasoline, diesel fuel, liquefied petroleum gas, compressed natural gas), lubricants (motor, transmission and special oils, greases), as well as special fluids (brake, coolant). An organization can purchase fuel and lubricants for cash and in non-cash form.

If the organization has chosen a non-cash form, then a supply agreement is concluded with the fuel supplier, according to which the organization transfers funds to the supplier’s bank account, and in return receives coupons or fuel cards, with which drivers refuel cars at gas stations (gas stations).

| 1C:ITS For more information on accounting for fuel and lubricants using fuel cards, see the “Directory of Business Operations. 1C: Accounting 8" section "Accounting and tax accounting". |

The use of coupons as a form of payment for fuel and lubricants has become widespread. To account for such transactions, it matters what type of coupons the organization uses and at what point ownership of the fuel and lubricants is transferred to the organization.

There are two types of coupons:

- liter (quantitative), which indicate the quantity and brand of fuel without specifying the amount (the price of fuel and lubricants is fixed on the date of payment of coupons; it is usually not indicated on coupons);

- sum or cost (monetary), which indicate only the amount for which you can refuel (the price of fuel and lubricants is determined on the date of refueling; coupons do not indicate either the price or quantity, but the brand of fuel may be indicated).

Depending on the terms of the agreement for the supply of petroleum products, ownership of fuel and lubricants may pass to the organization either at the time of receipt of coupons or at the time of refueling the car at a gas station. When refueling, the driver gives a coupon, and in return receives a tear-off coupon with a stamp of the redeemed coupon and a cash receipt. Coupons have a validity period established in the agreement with the seller of fuel and lubricants.

Fuel and lubricants are included in inventories (MPI) and are accepted for accounting at actual cost in accordance with the Accounting Regulations “Accounting for inventories” (approved by order of the Ministry of Finance of Russia dated 06/09/2001 No. 44n, hereinafter referred to as PBU 5 /01). According to the Chart of Accounts, the program uses subaccount 10.03 “Fuel” to account for fuel and lubricants.

If, under an agreement with the supplier, ownership of fuels and lubricants passes to the organization at the time of refueling the car at a gas station, then coupons for fuels and lubricants can be taken into account:

- as part of monetary documents on account 50.03 (as a rule, for sum coupons, but also acceptable for quantitative coupons);

- on off-balance sheet account 006 “Strict reporting forms” (usually for quantitative coupons).

A document that confirms fuel consumption, data on actual mileage and the production nature of the vehicle’s route is a waybill (approved by Resolution of the State Statistics Committee of Russia dated November 28, 1997 No. 78). This form of document is mandatory only for motor transport organizations. Other organizations can develop their own document form, which must contain the mandatory details provided for in Article 9 of the Federal Law dated December 6, 2011 No. 402-FZ “On Accounting” and Order of the Ministry of Transport of Russia dated September 18, 2008 No. 152 “On approval of the mandatory details and procedure for filling waybills."

If the organization's cars are equipped with an electronic mileage monitoring system (or mileage and fuel), then fuel consumption can be confirmed based on a printed system report signed by the responsible person.

There is no legal regulation of costs for fuels and lubricants, but the organization can itself establish fuel consumption standards by order of the manager.

In this case, you can be guided by the order of the Ministry of Transport of Russia dated March 14, 2008 No. AM-23-r or the standards specified in the vehicle operating instructions.

If standards are not established, then actual fuel consumption based on waybills is written off as expenses for ordinary activities. If the accounting policy of an organization provides for the use of fuel consumption standards, then the amount of fuel consumed within the standards is included in the organization’s expenses for ordinary activities, and in excess of the standards is included in other expenses.

In tax accounting, expenses for the purchase of fuel and lubricants can be taken into account in one of the following ways:

- as part of material expenses (based on clause 5, clause 1, article 254 of the Tax Code of the Russian Federation);

- as part of other expenses associated with production and (or) sales, such as the cost of maintaining official transport (clause 11, clause 1, article 264 of the Tax Code of the Russian Federation).

For profit tax purposes, expenses for fuel and lubricants are not standardized and are taken into account in full if they are economically justified, documented and incurred for the purpose of carrying out activities aimed at generating income (clause 1 of Article 252 of the Tax Code of the Russian Federation).

VAT on purchased fuels and lubricants is accepted for deduction in the general manner on the basis of an invoice presented by the supplier (clause 2 of Article 171 of the Tax Code of the Russian Federation, clause 1 of Article 172 of the Tax Code of the Russian Federation). As a rule, the supplier provides a set of documents (waybill, invoice) at the end of the month for the total amount of fuel sold during the month. The amount of fuel according to the supplier's invoice and according to the drivers' advance reports (according to tear-off coupons and cash receipts) must match.

Example 1

| Sewing Factory LLC (OSNO, VAT payer, applies PBU 18/02) purchases gasoline coupons in the amount of 30 pcs. from the organization Etalon-Kart LLC for a total amount of 58,500 rubles. (the numbers in the examples are conditional). The denomination of one coupon is 50 l. According to the terms of the agreement, ownership of the fuel and lubricants passes to the buyer at the time the vehicle is refueled at the gas station. Drivers receive gasoline using coupons received for reporting and draw up an advance report. The supplier provides documents for the fuel selected during the month (waybill, invoice) on the last day of each month. The cost of consumed gasoline is included in expenses at the end of the month according to travel sheets. Coupons for fuel and lubricants are recorded in account 50.03. |

Payment to the supplier for coupons is registered in the program by the document Write-off from current account with the transaction type Other settlements with counterparties, where account 76.05 should be specified as the settlement account.

As a result of posting the document, an accounting entry is generated:

Debit 76.05 Credit 51 - for the amount of the prepayment (RUB 58,500).

Please note that for those accounts where tax accounting is supported, the corresponding amounts are entered into special resources of the accounting register for tax accounting purposes. In the examples discussed in this article, there are no differences between accounting and tax accounting.

The receipt of monetary documents is reflected by a document of the same name with the transaction type Receipt from supplier (Fig. 2).

Rice. 2. Receipt of monetary documents

In the header of the document you should indicate the details of the primary document: date and number. The From tab is filled in by the user as follows:

| Field | Data |

| "Counterparty" and "Accepted from" | The supplier of fuels and lubricants from which the monetary documents were received is indicated (selected from the “Counterparties” directory) |

| "Treaty" | An agreement with a supplier is selected from the directory of the same name, and the type of agreement must have the value “Other” |

| "Settlement account" | The score is indicated as 76.05 |

On the Cash Documents tab, click the Add button to select incoming cash documents from the Nomenclature of Cash Documents directory. In Example 1, the monetary document has the form Coupons for fuel and lubricants (Fig. 3). The number and amount of received monetary documents is indicated.

Rice. 3. Nomenclature of monetary documents

When posting a document, the following entries are entered into the accounting register:

Debit 76.05 Credit 76.05 - for the amount of the offset advance (RUB 58,500). The offset is carried out between documents of settlements with counterparties Receipt of monetary documents and Write-off from the current account; Debit 50.03 Credit 76.05 - for the amount of gasoline coupons received (RUB 58,500) in the amount of 30 pcs.

The issuance of coupons to the driver is reflected in the document Issuance of monetary documents with the transaction type Issuance to an accountable person. On the To tab, the accountable person is indicated, which is selected from the Individuals directory.

On the Cash Documents tab, indicate the name of the coupon (selected from the Nomenclature of Cash Documents directory) and quantity, for example, 10 pcs. The cost of coupons is calculated automatically.

As a result of posting the document, the following posting is generated:

Debit 71.01 Credit 50.03 - for the amount of monetary documents issued to the accountable person (RUB 19,500) in the amount of 10 pieces.

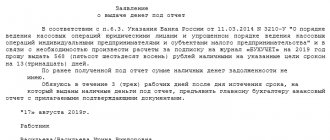

The posting of gasoline purchased by the driver using coupons and the accounting of input VAT on the gasoline received is reflected in the Advance report document (Bank and cash desk section). Let's say the driver has reported for all the tickets issued to him.

In the header of the document it is necessary to indicate the reporting accountable entity and the date of preparation of the advance report. If your organization keeps inventory records by warehouse, then you should fill in the Warehouse field.

On the Advances tab, use the Add button to select the document Issuance of monetary documents, according to which the accountable person received coupons.

Since the accountable person purchased inventory items, the Goods tab should be filled out in the Advance Report document. On this tab, click the Add button to fill in the table part (Fig. 4):

Rice. 4. Tabular part on the “Products” tab of the “Advance report” document

- in the Document (expense) field, the details of the primary documents received from the supplier are indicated;

- indicate the nomenclature, quantity and price of purchased gasoline in the appropriate fields, and the Amount field is calculated automatically;

- the supplier of fuels and lubricants is indicated;

- To register an invoice, you should set the checkbox in the Invoice field, and in the Invoice Details field, enter the date and number of the invoice received from the supplier. After executing the Write command, a link to the created document Invoice received for receipt is automatically added to the Invoice Details field of the Advance Report document;

- in the Accounting account and VAT account fields, fuel and lubricants accounting accounts and a VAT accounting account are indicated.

When posting the Advance Report document, the following transactions are generated:

Debit 10.03 Credit 71.01 - for the cost of gasoline received without VAT (RUB 16,525) in the amount of 500 liters; Debit 19.03 Credit 71.01 - for the amount of VAT (2,975 rubles).

The deduction of VAT on purchased gasoline will be reflected by the date of receipt of the invoice if the Reflect the deduction of VAT in the purchase book by the date of receipt in the form of the document Invoice received for receipt is checked.

By default, the date of receipt of the invoice corresponds to the date of the expense report, but if necessary, the date of receipt can be changed. If the flag is cleared, then the deduction can be reflected in the document Formation of purchase book entries (section Operations - Regular VAT operations) within 3 years after registration of fuel and lubricants.

To include the cost of gasoline in expenses, you need to create a Request-invoice document (Production section).

Let's say that the gasoline purchased with coupons was completely used up in accordance with the waybill. In the header of the document, the date of write-off of fuel and lubricants is indicated (the last day of the month) and the Warehouse field is filled in.

On the Materials tab, the name and quantity (500 l) of gasoline are indicated. If the item settings have been previously configured, the accounting account is filled in automatically. On the Cost Account tab, select the cost account to which materials are written off, for example, account 26 “General expenses”.

When posting a document, a posting is generated:

Debit 26 Credit 10.03 - for the cost of gasoline included in expenses (RUB 16,525).

| 1C:ITS How to account for monetary documents in the form of coupons, see the “Directory of Business Transactions. 1C:Accounting 8" section "Accounting and tax accounting": — accounting of fuels and lubricants; — accounting for services for removal and disposal of solid waste. |

Payment cards

They are usually purchased from operators. Each card has an individual number. The institution must develop and approve a local act regulating the use of communications. It defines the list of employees entitled to receive a payment card, as well as the conditions that they must fulfill when using it. For example, compensation is provided for the cost of calls made during business hours. In addition, the local act should regulate the procedure for personnel confirming expenses incurred.

Accounting for travel documents

Expenses for an employee’s travel to the place of business trip and back to the place of permanent work are included in business trip expenses (clause 12, clause 1, article 264 of the Tax Code of the Russian Federation). Travel documents (air and train tickets) can be purchased by an employee sent on a business trip independently. In this case, the employer is obliged to reimburse the employee for these expenses (Article 168 of the Labor Code of the Russian Federation). An organization can also purchase travel documents through specialized transport agencies.

Travel documents are issued on strict reporting forms (clause 2 of the Regulations on the implementation of cash payments and (or) payments using payment cards without the use of cash register equipment, approved by Decree of the Government of the Russian Federation of May 6, 2008 No. 359). The basis for deducting VAT on the costs of transporting employees to the place of business trip and back is a travel document in which the tax is highlighted as a separate line. Such a ticket or a copy thereof is registered in the purchase book after approval of the employee’s advance report (clause 18 of the Rules for maintaining the purchase book, approved by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137).

Often all travel documents are purchased in paperless form (electronic tickets). In this case, strict reporting documents are:

- route receipt of an electronic air ticket (clause 2 of the order of the Ministry of Transport of Russia dated November 8, 2006 No. 134);

- e-railway ticket coupon (clause 2 of Order No. 322 of the Ministry of Transport of Russia dated August 21, 2012).

According to the explanations of the Ministry of Finance of Russia, when purchasing air tickets electronically, the amount of VAT allocated as a separate line in the itinerary receipt of an electronic passenger ticket printed on paper is accepted for deduction (see letters dated January 30, 2015 No. 03-07-11/3522, dated 07/30/2014 No. 03-07-11/37594). In practice, this clarification also applies to the e-railway ticket coupon.

If an employee flies on a business trip by plane, then to confirm the costs of the flight, in addition to the itinerary receipt of the electronic air ticket, a boarding pass is also required. At the same time, the organization has the right to justify the consumption of air transportation services with any other documents that directly or indirectly confirm the fact of use of purchased air tickets (letter of the Ministry of Finance of Russia dated December 18, 2017 No. 03-03-RZ/84409).

If an employee goes on a business trip by rail, then the document confirming his travel expenses will be the control coupon of an electronic travel document (letter of the Ministry of Finance dated April 14, 2014 No. 03-03-07/16777).

No documents evidencing payment for an electronic ticket (for example, a bank card statement) are required to confirm these expenses (letter of the Ministry of Finance of Russia dated December 18, 2017 No. 03-03-RZ/84409).

The current legislation does not contain special rules regulating the procedure for recording electronic travel tickets. The purchase of an electronic travel ticket can be counted as receipt of a monetary document (since the electronic ticket fully meets its criteria) or as an advance payment for transport services (since the services are consumed later). Thus, the procedure for reflecting these transactions in the organization’s accounting records must be reflected in the accounting policy.

Example 2

| An employee of Confetprom LLC was sent on a business trip to Ufa from 04/09/2018 to 04/11/2018 (for 3 days). The daily allowance, according to the organization’s regulations on business trips, is 700 rubles. RUB 9,000 was transferred to the employee’s personal account for the report. A round-trip e-ticket was purchased by the organization through a transport agency. The cost of an air ticket on the route Moscow - Ufa - Moscow is 10,574 rubles. The amount of VAT (10%) is highlighted on the ticket as a separate line and amounts to 930 rubles. The cost of the service fee charged by the transport agency is 295 rubles. (including VAT 18%). In accordance with the accounting policy of the organization, electronic travel tickets are accounted for as monetary documents. Upon returning from a business trip, the reporting person submits an advance report, to which he attaches documents, including a boarding pass and documents from the hotel service provider (in the amount of RUB 7,000 excluding VAT). |

The transfer of funds to the employee's personal account, confirmed by a bank statement, is reflected in the document Write-off from current account with the transaction type Transfer to an accountable person. In the Recipient field, the accountable person is indicated, which is selected from the Individuals directory.

After posting the document Write-off from the current account, an accounting entry is generated:

Debit 71.01 Credit 51 - for the amount of funds issued for the report (9,000 rubles).

Settlements with the transagency can be made on account 76.05 using the following documents:

- Debiting from a current account with the transaction type Payment to supplier - to register payment;

- Receipt of monetary documents with the transaction type Receipt from the supplier - upon receipt of monetary documents;

- Receipt (act, invoice) with transaction type Services - to reflect expenses for transagency services.

In this case, the agreement with the transagency should look like:

- With the supplier - in the documents Write-off from the current account with the transaction type Payment to the supplier and Receipt (act, invoice);

- Other - in the documents Receipt of monetary documents and Write-off from the current account with the transaction type Other settlements with counterparties.

Thus, settlements with the transagency in Example 2 are carried out under two contracts with different types.

Payment to the transagency is registered by the document Debit from the current account with the transaction type Payment to the supplier (under an agreement with the type With supplier). After posting the document, an accounting entry will be generated:

Debit 76.05 Credit 51 - for the cost of air tickets, taking into account the service fee charged (RUB 10,869).

After posting the standard document Receipt (act, invoice) with the transaction type Services, the following entries are entered into the accounting register:

Debit 76.05 Credit 76.05 - for the amount of the offset advance (295 rubles). The offset is carried out between the settlement documents Receipt (act, invoice) and Write-off from the current account; Debit 26 Credit 76.05 - for the cost of transagency services excluding VAT (250 rubles); Debit 19.04 Credit 76.05 - for the cost of VAT (45 rubles).

The purchase of an electronic ticket is reflected in the document Receipt of monetary documents with the transaction type Receipt from the supplier. In Example 2, the monetary document has the form Tickets. When posting a document, the following entry is entered into the accounting register:

Debit 50.03 Credit 76.05 - for the amount of the ticket received (RUB 10,574) in the amount of 1 piece.

Under an agreement with the type Other, the advance payment does not offset. To offset an advance payment to a supplier (under an agreement with the type With supplier), you can use the document Adjustment of debt with the transaction type Debt write-off, after which the posting will be generated:

Debit 76.05 Credit 76.05 - for the amount of the offset advance (RUB 10,574). The offset is performed between the settlement documents Receipt of cash documents and Write-off from the current account. After completing this operation, the account 76.05 is closed.

The issuance of an electronic ticket to an accountable person is documented in the document Issuance of monetary documents with the transaction type Issue to an accountable person and is reflected by the posting:

Debit 71.01 Credit 50.03 - for the amount of the monetary document issued to the employee for reporting (RUB 10,574) in the amount of 1 piece.

Upon returning from a business trip, the reporting person submits an advance report. To include business trip expenses in expenses and account for input VAT, an Advance Report document is created. On the Advances tab, use the Add button to specify the following documents:

- Issuance of monetary documents, according to which the accountable person received a travel document;

- A debit from the current account, according to which funds were transferred to the employee’s bank card.

Information about business trip expenses (travel, accommodation and daily allowance) is reflected on the Other tab. This tab is filled out in accordance with the documents submitted by the accountable person. The following data is indicated in the fields (Fig. 5):

Rice. 5. Tabular part on the “Other” tab of the “Advance report” document

| Field | Data |

| "Document (expense)" | Enter information about primary documents |

| "Nomenclature" | The element corresponding to the flow rate is selected from the “Nomenclature” directory |

| "Amount", "VAT" | The amount and tax rate for the document are indicated, the “Total” field is calculated automatically |

| "Provider" | The counterparty is selected from the directory of the same name (for daily allowances this field is not filled in) |

| "SF" and "BSO" | Flags are set to register an electronic ticket as a strict reporting form. In this case, the “Invoice Details” field will be filled in automatically using the number and date of the BSO from the “Document (expense)” field. After executing the “Write” command, a link to the created “Invoice (strict reporting form)” document is automatically added to the “Invoice Details” field of the “Advance Report” document. |

| "Cost Account/Division" | Indicate the accounting expense account, the debit of which will include business trip expenses (for example, 26 “General business expenses”). If records are kept by division, the corresponding division is indicated |

| "Subconto" | The analytics for the cost account are indicated (for account 26 cost item “Travel expenses”) |

| “NU Cost Account” and “NU Subconto” | By default, they are filled in according to accounting data. They can be edited if necessary |

| "VAT invoice" | By default, account 19.04 “VAT on purchased services” is installed (if necessary, you can select a different VAT account) |

When posting the Advance Report document, the following transactions are generated:

Debit 26 Credit 71.01 - for the cost of an air ticket excluding VAT (9,644 rubles); Debit 19.04 Credit 71.01 - for the amount of VAT (930 rubles); Debit 26 Credit 71.01 - for the cost of living (RUB 7,000); Debit 26 Credit 71.01 - for the amount of daily allowance (RUB 2,100).

The deduction of VAT on an electronic air ticket will be reflected by the date of the advance report if the Reflect the deduction of VAT in the purchase book by the date of receipt in the form of an Invoice document (strict reporting form) is checked.

If the flag is cleared, the deduction can be reflected in the document Formation of purchase ledger entries.

To view the status of settlements with an accountable person, you can use the report Turnover balance sheet for account 71.01 “Settlements with accountable persons”.

In the balance sheet for account 71.01, the credit balance is 100 rubles. This means that the organization must pay the overspending of funds to the accountable person (in cash from the cash register or by transfer to the employee’s bank card).

Employee reports

But assets are given to an employee for a reason, but to fulfill a certain official assignment. Therefore, the moment comes when the employee must report to the accounting department in form AO-1.

This is a printed form that indicates:

- everything that we gave to the employee for reporting

- everything he spent this money on (or didn’t spend it, or maybe there was an overspending)

- Supporting documents (checks, invoices, acts, tickets...) are attached to this form.

Here is an example of the AO-1 form:

This report (AO-1) is compiled by the employee together with the accounting department and approved by the manager. At the very bottom, the number of documents and sheets on which they are attached to the report is indicated (checks are usually pasted in whole packs onto A4 sheets).

So, in order to print such a report (AO-1), write off debt on 71 accounts from an employee, and also accept expenses in the top three, there is the document “Advance report”:

Let's briefly go through his bookmarks:

Exchange and return of travel documents

In practice, there are situations when a ticket has to be returned or exchanged. In this case, for the return or exchange of a travel document (including an electronic one), the carrier withholds a commission (fine). The transport agency may also charge an additional fee for its services.

If the exchange or return of a ticket is due to operational necessity, then the organization can include as expenses for profit tax purposes both the cost of the originally purchased (minus the amount returned by the airline) and the new ticket (letter of the Ministry of Finance of Russia dated May 2, 2007 No. 03-03-06/ 1/252). Expenses in the form of a fine for reissuing and returning tickets reduce the tax base for corporate income tax (letter of the Ministry of Finance of Russia dated September 8, 2017 No. 03-03-06/1/57890).

Example 3

Let's change the conditions of Example 2. Due to production needs, an organization, through a transport agency, exchanges an electronic air ticket on the route Moscow - Ufa - Moscow (let's say the departure time from Ufa changes). The organization pays an additional RUB 3,880 to the trans agency, including:

|

After posting the document Write-off from current account with the transaction type Payment to supplier, an accounting entry will be generated:

Debit 76.05 Credit 51 - for the cost of air tickets, taking into account commission and additional services (3,880 rubles).

The exchange of an air ticket through a transagency is reflected in the following documents:

- Receipt of monetary documents with the transaction type Receipt from an accountable person (if the accounting reflected the issue of a ticket to an accountable person);

- Issuance of monetary documents with the transaction type: Return to supplier;

- Receipt of cash documents with the transaction type Receipt from supplier.

Additionally, you should create a document Receipt (act, invoice) with the transaction type Services to reflect additional expenses for the services of the transagency (590 rubles). When filling out the document Receipt of monetary documents with the transaction type Receipt from an accountable person on the From tab, fill in the details Accountable person and Received from (full name of the employee for the printed form).

On the Cash Documents tab, the name of the cash document, quantity (1 pc.) are indicated, and its value is filled in automatically. After posting the document, the following posting is generated:

Debit 50.03 Credit 71.01 - for the amount of the ticket received (RUB 10,574) in the amount of 1 piece.

In the document Issuance of monetary documents with the transaction type Return to supplier, on the Cash documents tab, not only the name of the monetary document, its quantity (1 piece) and cost (RUB 10,574), but also the return amount (RUB 9,374) is indicated, since the carrier withholds a commission of RUB 1,200. (10,574 rubles - 1,200 rubles = 9,374 rubles) (Fig. 6).

Rice. 6. Return of the monetary document to the supplier

Additionally, you need to fill in the details on the Income and Expense Accounts tab to reflect the differences between the accounting value of monetary documents and the refund amount:

- Item of income and expenses - selected from the directory Other income and expenses;

- Income account - an account for income that arises when the return amount exceeds the accounting value of monetary documents;

- Expense account - an account for expenses that arise when the book value of monetary documents exceeds the return amount.

After posting the document, the following transactions will be generated:

Debit 76.05 Credit 50.03 - for the cost of a refundable air ticket (RUB 10,574); Debit 91.02 Credit 76.05 - for the amount of the withheld commission for the return (RUB 1,200).

Then you should create a new document Receipt of monetary documents with the transaction type Receipt from supplier, where the receipt of a new air ticket should be reflected. After posting the document, the following transactions will be generated:

Debit 50.03 Credit 76.05 - for the amount of the ticket received (RUB 12,664) in the amount of 1 piece.

Further actions with the electronic ticket are similar to those described in Example 2.

Results

Accounting for monetary documents must be maintained using a special subaccount 50-3. They need to be issued with accountability. This will allow the company to minimize the risks of non-economic use of monetary documents, as well as incorrect calculation of the tax base for income tax or VAT.

Sources:

- Tax Code of the Russian Federation

- Law “On Accounting” dated December 6, 2011 N 402-FZ

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Normative base

Accounting for documents acting as means of payment is carried out on the account. 201 35 000. When preparing records on the movement of financial instruments, specialists must be guided by Instruction No. 157n. This document approved the Unified Plan of Accounts for state and territorial authorities, state academies of sciences, and management bodies of extra-budgetary state funds. In addition, recommendations are present in Instruction No. 174n. This document approved the Chart of Accounts for budgetary institutions and explanations to it.