2-NDFL

The 2-NDFL certificate reflects all amounts paid to the employee, withheld personal income tax and deductions provided. Such a certificate at the end of the year is issued for each employee who worked under an employment or civil contract.

2-NDFL includes only those payments that are subject to personal income tax. Article 2021 of the Tax Code of the Russian Federation lists payments from which personal income tax is not withheld. They do not need to be included in the certificate. These are, in particular, state benefits (but not sick leave), compensation, alimony, some types of financial assistance, etc.

Calculation of insurance premiums for the 3rd quarter: where to submit

Another salary reporting submitted to the Federal Tax Service is the unified calculation of insurance premiums (ERSV). Previously, it was accepted by the Pension Fund, but since 2021, control over social insurance contributions has passed to the tax authorities. Chapter 34 of the Tax Code of the Russian Federation began to regulate the calculation and payment of contributions for pension and health insurance, as well as insurance against temporary disability and in connection with maternity.

The report form was approved by order of the Federal Tax Service of Russia dated October 10, 2016 No. ММВ-7-11/551. It must be completed for the 3rd quarter and submitted to the tax authorities by October 30, 2021.

The full composition of the report is quite voluminous - this is the title page, the sheet “Information about an individual who is not an individual entrepreneur,” section 1, 10 appendices to section 1, section 2, appendix to section 2 and section 3. However, many appendices and sections are filled out only if there is the necessary data for this.

The calculation contains data on accrued contributions:

- on OPS;

- Compulsory medical insurance;

- VNiM.

This calculation does not include information on contributions for insurance against accidents at work and occupational diseases (NS and PE). Why? We'll talk about this in the next section.

Is it necessary to submit a zero RSV if the individual entrepreneur does not have employees? Let’s look into this forum topic.

If personal income tax could not be withheld

It happens that an individual received income from an individual entrepreneur or a company, but it was not possible to withhold tax from it. This most often happens if the income is in kind. For example, a company gave a partner a gift worth more than 4 thousand rubles, and by law must withhold personal income tax, but there is nothing to withhold it from, because the partner does not receive any cash payments from this company.

In such a situation, the company must still issue a 2-NDFL and indicate the value of the gift. Only in the certificate, instead of sign “1”, sign “2” is indicated. And the deadline for submitting a certificate with sign “2” is different - March 1, that is, a month earlier.

How to punish for failure to submit a report to Rosstat on time

IMPORTANT!

Failure to provide written notice of the requirement to provide a 57-T report does not remove the penalty. Statistical authorities insist that employers are obliged to independently monitor the approved lists.

The Code of Administrative Offenses of Russia provides for fines for violating the deadlines for submitting statistical reports. Thus, Article 13.19 provides for punishment in the form of a fine for a legal entity in the amount of 20,000 to 70,000 rubles.

6-NDFL

Not the easiest report, especially for beginners.

This is a general calculation, one for all employees, which contains information on accrued and paid income, calculated and withheld personal income tax, and provided tax deductions.

Just like in 2-NDFL, here you do not need to indicate income that is not subject to income tax at all, but partially taxable amounts are shown in full.

The calculation consists of two sections. In the first, cumulatively, generalized indicators from the beginning of the year are entered, in the second - actual indicators for the reporting period.

Filling out 6-NDFL still raises many questions, so we recommend that you read the article, where we tried to describe in detail and clearly how to fill out 6-NDFL, and what needs to be taken into account.

STATISTICAL REPORTING ON WAGES [p.109]

If we analyze statistical reporting data on labor costs (form 5-z Information on the costs of production and sales of products (works, services)), then in this reporting, as well as accounting statements (form No. 5, section 6 Costs incurred by the organization) we will find data on actual costs written off for sold products (i.e. included in distribution costs for trade organizations. As experience in recent years shows, debts accumulate for wage payments , therefore, the accrued wage fund, as a rule, exceeds labor costs, i.e., wages paid.But if the wage arrears did not increase, there would still be differences between accrued and attributed to the cost of production or distribution costs (commercial expenses, according to reporting) it is inevitable that part of the accrued production costs in industry, including accrued wages, is retained in work in progress, and in trade - part of the accrued wages, along with other accrued distribution costs, remains to be attributed to inventories if they increase, and is not written off for implementation. Of course, the opposite process is also possible, if work in progress decreases or inventories in trade decrease, wages will lag behind the write-off of costs of this type of sales. [p.352]

These timesheets are compiled in one copy and submitted to the accounting department. They allow not only to take into account the time worked by all categories of employees, but also to monitor compliance by workers and employees with the established work schedule. Based on the timesheets, wages are calculated and statistical reporting on labor is compiled. [p.248]

Timesheet accounting of working hours, accounting of basic and additional wages, calculation of taxes on wages, generation of output settlement and payment documents and statistical reporting forms, generation of accounting entries for wage accounting. [p.32]

To analyze wage calculations, the most popular statistical reporting is Information on the number and wages of employees by type of activity (form No. 1-T). Since January 1, 2001, all organizations have compiled and submitted to the relevant authorities a periodic reporting form Information on the number, wages and movement of workers (form No. P-4) and monthly reporting Information on overdue wages (form No. 3- F). [p.208]

The list of payments made in favor of individuals is determined by the Instruction on the composition of the wage fund and social payments, approved by Resolution of the State Statistics Committee of the Russian Federation dated November 24, 2000 No. 116. This list is used to conduct federal state statistical monitoring of labor and is used by organizations when filling out statistical reports on labor, which must be submitted to the statistical authorities in the prescribed manner. [p.191]

Sources of information for the analysis of the wage fund are cost estimates, statistical reporting on labor, data from timesheets and the personnel department, personal accounts (form No. T-54), settlement accounts (form No. T-51) or settlement and payment (form No. T-54). No. T-49) statements, calculations of average wages of certain categories of workers, etc. [p.274]

When compiling statistical reporting on labor, the amounts of money accrued for the reporting period are shown, regardless of the sources of their payment and budget items in accordance with the payment documents according to which settlements were made with employees for wages, bonuses, etc. regardless of the date of their actual payment. [p.276]

In development table No. 4, in addition to wage indicators, indicators are given in physical terms in man-days and man-hours. This table is opened for each month, and entries in it are made from payroll statements for the reporting month. Wages accrued to unpaid employees are shown in a separate line in the table. The indicators of development table No. 4 are used to compile statistical reporting for a construction organization on labor and wages. [p.73]

The sheet for recording the use of working time and calculation of wages (Form No. T-12, Appendix 10) and the sheet for recording the use of working time (Form No. T-13, Appendix 11) are used to record the use of working time of all categories of employees, to monitor workers’ compliance and employees of the established working hours, as well as for the preparation of statistical reporting on labor. [p.38]

In the second half of the 50s, major measures were taken to centralize the collection and processing of statistical reporting on industry, construction and some other sectors in the system of the Central Statistical Office of the USSR. Reporting of industrial enterprises and reporting on capital construction were centralized in the Central Statistical Office since 1957, reporting on new technology and agriculture - since 1958. Reporting on labor and wages, housing and communal services and some other industries was also centralized. With centralized data processing, enterprises and organizations submit reporting data to local statistical authorities. The data is checked and then processed at computer centers. Generalized statistical data and prepared analytical notes and reports are submitted to the government, relevant ministries and departments, local party and Soviet bodies. [p.12]

Necessary for analysis. information is contained in statistical reporting on labor (form No. 9 of the annual report, form No. 2-t and No. 4-periodic reporting), as well as in the corresponding accounting statements, calculations to the technical industrial financial plan, certificates of accrued and due wages received to the State Bank institutions from the enterprise in connection with the need to obtain funds to pay wages, and in other documents. [p.126]

The necessary information for this is contained in the statistical reporting on labor (form No. 2-t), as well as in the corresponding accounting reports, calculations for the technical industrial financial plan, certificates of accrued and due wages and other documents. [p.183]

The necessary information for this analysis is contained in statistical reporting on labor (form No. 9 of the annual report and No. 2 of periodic reporting), as well as in the corresponding accounting reports, calculations for the technical industrial financial plan, certificates of accrued and due wages compiled for State Bank institutions , and other documents. [p.132]

This construction of the personnel category code corresponds not only to the organization of analytical accounting of wages, but also to the forms of statistical reporting on labor and wages (forms No. 2-t and No. 4-t), as well as planning of labor and wage funds. [p.45]

Analysis of profit distribution is carried out on the basis of information obtained in the economic planning and financial departments, accounting, labor and wages departments. The accounting statements used are Balance sheet for the main activities of the production association (enterprise) f. No. 1, Appendix to the balance sheet f. No. 2, Product sales f. No. 12, Statement of profit (income) and loss (losses) f. No. 20, statistical reporting on labor, products, cost, introduction of new equipment, etc., as well as the Balance of Income and Expenses (financial plan), Appendix to accounting reports on calculations of payments from profit to the budget, information on the standards of contributions to the budget , a higher organization, to economic incentive funds, about the standards of payments for the funds. When analyzing the distribution of profit, it is important to check the correctness of excluding from the planned and actual amount of profit distributed according to standards the part that is used in a special manner. If violations are identified in the use of actually received profits, it is necessary to determine measures to correct the balance of income [p.15]

When compiling statistical reporting on labor, the amounts of money accrued for the reporting period (taking into account taxes and other deductions in accordance with the law) are shown, regardless of the sources of their payment and the items of estimates in accordance with the payment documents on which wages were settled with employees, bonuses, etc., regardless of the period of their actual payment. [p.466]

Timesheets are kept to record the use of working time for all categories of employees, to monitor compliance by workers and employees with the established working hours, to obtain data on time worked, calculate wages, and also to compile statistical reporting on labor. [p.113]

In addition, a number of tabular charts are specially compiled and then used to fill out established statistical reporting on personnel records, labor and wages. [p.231]

A summary tabular chart of accrued wages by type of payment on an accrual basis from the beginning of the year for the enterprise as a whole is compiled once a month based on the same array as the previous tabular chart. It serves as the basis for filling out some sections of statistical reporting on labor and wages compiled by type. f. No. 2-t, 4-t and 9. In addition, the tabulagram is intended for analyzing the use of the wage fund, also (together with other tabulagrams) for filling out a certificate to the State Bank to receive money for paying wages. [p.232]

They are used to record the use of working time by employees of an organization, to monitor employees’ compliance with the established working hours, to obtain data on hours worked, to calculate wages, and to compile statistical reporting on labor. In the case of separate accounting of the use of working time and settlements with personnel for wages, it is allowed to use section 1 Accounting for the use of working time of the timesheet in form No. T-12 as an independent document. [p.223]

A timesheet for the use of working time and calculation of wages (Form No. T-12), a timesheet for the use of working time (Form No. T-13) are used to record the use of working time of the organization’s employees, to monitor employees’ compliance with the established working time schedule, to receive data on hours worked, payroll calculations, as well as for compiling statistical reporting on labor. In the case of separate accounting of the use of working time and settlements with personnel for wages, it is allowed to use section 1 Accounting for the use of working time of the time sheet in form No. T-12 as an independent document (Appendix 29). [p.181]

Step 4. In accounting and when compiling statistical reporting on labor in June, the amount of 3243.94 rubles is shown as part of the wage fund. (at the same time, the payroll statement shows the full amount accrued in June (RUB 4,550.84), and the insurance contributions accrued on it to extra-budgetary funds are transferred in full). [p.192]

STATISTICAL REPORTING ON LABOR, WAGES AND NUMBER OF EMPLOYEES [p.479]

The use of working time is recorded in timesheets, in annual time cards, etc. Timesheets are opened either for the organization as a whole (small enterprises), or for its structural divisions and categories of employees. They are necessary not only to record the use of working time of all categories of workers, but also to monitor compliance by personnel with the established working hours, pay wages and obtain data on hours worked, as well as compile statistical reporting on labor. [p.164]

According to Form No. 3 of the statistical reporting of the Central Statistical Office of the USSR, all types of costs for drilling and casing wells are grouped into six consolidated elements: 1) materials (including casing pipes) 2) basic wages 3) operating costs of drilling equipment and drilling tools ( including depreciation of drilling equipment) 4) transportation costs 5) energy costs and 6) other services of auxiliary production from outside and other costs. [p.105]

In accounting, as is known, all wages are reflected in the credit of account 70 Settlements with personnel for wages, and in statistical reporting - in reporting form P-4 Information on the number, wages and movement of employees. In both cases, accrued wages are reflected. This point is methodologically very important. You should always distinguish between accruals and payments. In the term expenses this difference is eliminated. Both payments and accruals are expenses. [p.65]

Based on primary documentation, an analysis of the organization’s economic activities is carried out, the cost of work is determined, the consumption of materials, wages and labor costs is taken into account and controlled, and reports are compiled on various sections of production, economic and financial activities for higher organizations, statistical accounting bodies and financing banks. Therefore, special attention must be paid to the quality of primary reporting documentation and the timeliness of its submission. [p.393]

The reserves for labor productivity growth should be calculated using Table. 2.14. The example given in the table shows, first of all, the magnitude of the reserves for growth in labor productivity, which can be identified using calculations based on statistical reporting. Table data 2.14 indicate that the largest reserve is the elimination of manufacturing defects, the implementation of which will provide a relative saving of 15 people and an increase in productivity by 2.2%. The implementation of all identified reserves would allow the enterprise to reduce its workforce by 21 people and increase labor productivity by 3.1%. An increase in labor productivity by this amount will save 41.8 thousand rubles. wage fund. Another reserve for saving the wage fund is the elimination of unproductive payments, i.e. additional payments for overtime work in the amount of 6.8 thousand rubles. and additional payments to piece workers for deviations from normal working conditions in the amount of 1.1 thousand rubles. [p.73]

ANALYSIS OF THE IMPLEMENTATION OF THE PLAN FOR THE WAGE FUND is one of the areas of analysis of the labor plan, carried out to check the validity of wage planning, control and operational management of the wage organization. In the process of A.v.p. according to federal wages the correspondence of the volume of wages to its planned fund is established for the divisions of the organization, categories of industrial and production personnel and for the non-industrial group, the reasons for deviations are identified, and reserves for its savings are revealed. Analysis of the use of wage funds is carried out taking into account quantitative and qualitative economic indicators. activities of the organization, the situation with wages in the labor market in the region, with the ratio of growth rates of labor productivity and wages at competing enterprises. Sources of data for analyzing the expenditure of wages can be financial statements for the enterprise, statistical reporting for the industry, region, and competing enterprises. [p.10]

Statistical accounting is widely used to evaluate plan implementation. It allows you to summarize data on the volume and growth rate of industrial production, the implementation of product sales, taking into account contractual obligations for the supply of products, dynamics of labor productivity and wages, etc. Based on statistical accounting data, statistical reporting is compiled in certain forms and submitted to the authorities Central Statistical Office of the USSR (CSO USSR), where it serves as the basis for obtaining summary data in sectoral, territorial and national economic contexts. [p.172]

DEPARTMENT OF LABOR AND WAGES ORGANIZATION - a functional unit of the organization that carries out standardization and organization of labor, tariffication of labor processes, development of remuneration systems, organization and planning of labor and wages, taking into account the conditions and regimes of work and rest, management of all types of work motivation - high level wages, favorable conditions for a career, providing the necessary independence at work, creating conditions for the implementation of the ideas of one or another employee, interest in their work, ensuring the necessary independence for management and specialists, creating, if necessary, a more flexible work schedule, ensuring an environment which recognizes the employee’s merits, creating a healthy psychological climate at work, ensuring the employee’s confidence that he will not lose his job, good material support for old age, a favorable management style, ensuring satisfaction with his work, creating opportunities for self-realization of the employee as an individual, ensuring the presence of an element of competition in labor development and improvement of a system for assessing the work of personnel formation of a collective agreement and organizing control over the progress of its implementation control over compliance with the Labor Code of the Russian Federation in the field of standardization and remuneration of labor, internal regulations organization of work on certification of workplaces development of work schedules for the organization (one-, two- and three-shift mode) and coordination of work schedules of structural divisions, technical and economic analysis. indicators of structural divisions for labor; compilation of statistical reporting on labor indicators. [p.443]

The reporting of an industrial enterprise is divided into monthly, monthly, quarterly and annual. Intra-monthly - limited, as a rule, to information on issues that are particularly important for the national economy, for example, on the production of the main products in quantitative terms. Monthly—contains statistical information about product output in value and physical terms, the movement of personnel, the use of the wage fund, the cost of production and financial statements (balance sheet, transcript of its individual articles, data on the implementation of the product sales plan, etc.). In addition to the listed information, the quarter contains data on the actual amount of profit, incentive funds, etc. The most complete for assessing the economic activity of an enterprise is the annual report of the enterprise. [p.32]

The planning department prepares long-term and annual work plans for management, develops operational monthly plans and carries out all the work on grassroots planning at sites, draws up a construction and financial plan for management with the involvement of other departments, monitors its implementation, manages (together with H&S and accounting) the implementation of economic accounting at sites and in teams, controls the expenditure of the wage fund, develops estimates of administrative and business expenses, maintains operational records and analysis of the implementation of plans for areas and management as a whole, compiles statistical reporting and, together with accounting and other departments, reports on management activities. In addition, the planning department, in the absence of a health and safety department in the management, makes calculations based on existing bonus systems and develops staffing schedules. [p.50]

Deadline

6-NDFL is submitted 4 times a year.

Based on the results of the first quarter, half a year and nine months - within a month after the end of the reporting period.

At the end of the year - until April 1.

6-NDFL, just like 2-NDFL, can be submitted in paper form only if information is submitted for 24 or fewer people. If more, the form will only be accepted electronically.

Is it necessary to generate salary reports if there were no payments during the reporting period? No no need. Zero salary reports are not provided. But if you have employees, and you have previously submitted salary reports, for peace of mind it would not hurt to contact the tax office and send them an explanation of why you are not submitting anything this time (for example, because all employees are on administrative leave).

Filling out 6-NDFL quickly and without errors in the “My Business” online service

The service will remind you of deadlines, take into account all the nuances of filling out, generate, check and send reports.

Get free access

Reporting to funds

Despite the 2021 reform in insurance coverage, salary reporting in 2021 to extra-budgetary funds has only been partially cancelled. You will have to submit information about calculated contributions for injuries to Social Insurance. And the Pension Fund will have to report on the length of service of the insured persons.

Calculation 4-FSS

The form is fixed by order of the Social Insurance Fund dated September 26, 2016 No. 381.

Please note that the deadline for submitting a calculation to Social Security directly depends on the method of submitting data.

Report electronically:

- for 2021 - 01/27/2020;

- 1st quarter 2021 - 04/27/2020;

- half year 2021 - 07/27/2020;

- 9 months 2021 - 10/26/2020;

- 2020 - 01/25/2021.

You submit 4-FSS on paper:

- for 2021 - 01/20/2020;

- 1st quarter 2021 - 04/20/2020;

- half year 2021 - 07/20/2020;

- 9 months 2021 - 10/20/2020;

- 2020 - 01/20/2021.

The method of provision is determined by the average number of employees:

- up to 25 people - allowed on paper or electronically;

- 25 or more employees - only in electronic format.

Instructions for filling out: >Sample of filling out form 4-FSS in 2020.

Fines: 5% of the amount of insurance coverage payable for each full or partial month of delay. No more than 30%, but not less than 1000 rubles. Officials - a fine under Art. 15.33 Code of Administrative Offenses of the Russian Federation - from 300 to 500 rubles.

SZV-M

The form of the monthly form is fixed by the resolution of the Pension Fund of Russia board dated 02/01/2016 No. 83p.

Report by the 15th day of the month following the reporting month:

- for December 2021 - 01/15/2020;

- January 2021 - 02/17/2020;

- February 2021 - 03/16/2020;

- March 2021 - 04/15/2020;

- April 2021 - 05/15/2020;

- May 2021 - 06/15/2020;

- June 2021 - 07/15/2020;

- July 2021 - 08/17/2020;

- August 2021 - 09/15/2020;

- September 2021 - 10/15/2020;

- October 2021 - 11/16/2020;

- November 2021 - 12/15/2020;

- December 2021 - 01/15/2021.

It is allowed to submit reports earlier than the deadline, but only if verified information is available.

If the reporting form includes information about 25 employees or more, then report only electronically. Other policyholders have the right to report on paper.

Instructions for filling out: >Reporting SZV-M: step-by-step instructions for filling out.

New SZV-TD

The report in the SZV-TD form is a new electronic book, the transition to which begins in 2021. Not all policyholders report, but only those whose staff has undergone personnel changes. The grounds for filling out and submitting the SZV-TD include:

- conclusion of a new employment contract;

- termination of an employment contract or agreement with an employee;

- assignment of qualifications, transfer to another job, other personnel changes that require reflection in the work book;

- submission by an employee of an application to choose the method of maintaining a work record in 2021 and subsequent years.

Rules for drawing up a new pension report are in the article > “How to fill out a new monthly SZV-TD report.” Submit reports to the Pension Fund on a monthly basis. The timing coincides with SZV-M. Submit information for generating electronic work books by the 15th day of the month following the reporting month.

SZV-STAZH

Enshrined in Resolution of the Board of the Pension Fund of January 11, 2017 No. 3p.

The report is submitted annually, before March 1 of the year following the reporting year:

- for 2021 - 03/02/2020;

- 2020 - 03/01/2021.

Instructions for filling out: >Fill out and submit the SZV-STAZH form to the Pension Fund of Russia.

Responsibility for failure to submit SZV-M. SZV-TD and SZV-STAZH - 500 rubles for each employee. The fine for officials is similar - from 300 to 500 rubles (Article 15.33 of the Code of Administrative Offenses of the Russian Federation).

If the due date falls on a holiday or weekend, then the accountant's 2021 payroll reports are submitted on the first working day.

What has changed in Form 3-F

The new form 3-F, a sample of which is presented below, has undergone minor technical changes. It has updated the periods for which information must be provided. In particular, the reporting year was changed in lines No. 9, 10 and 11:

- in line No. 9, the year 2018 was replaced by 2019;

- in line No. 10, the year 2017 was replaced by 2018;

- in line No. 11, the year 2018 was replaced with 2019.

The updated form will come into effect in 2021. Legal entities must report on it, starting with the report as of February 1, 2020. You will find a list of reporting forms sent to Rosstat in our article.

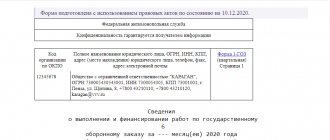

Who submits report 57-T in 2021

Not everyone will be required to report wages using the new form, but only those employers who were included in a special sample of statistical bodies. The official list of reporting organizations is posted on the Rosstat website.

Representatives of Rosstat determine who submits Form 57-T for 2021. A list of organizations that are exempt from submitting a new report has already been published. The following are completely excluded from federal statistical observation:

- public sector management;

- defense sector of the state (army, police, state security);

- insurance companies and financial and credit organizations;

- public entities and small businesses.

Some institutions received written notification of the need to submit a reporting document. There is no need to wait for an official request; check whether your organization is included in the list on the website of the statistical authorities. The letter may get lost or arrive late, and for failure to provide information, the institution faces a significant fine (up to 70,000 rubles). Reporting should be done once every two years, no later than November 29, 2019.

IMPORTANT!

Representatives of Rosstat report that the published list of employers is not final and is being updated. Officials recommend periodically monitoring changes to sample lists.

Related documents

- Sample. Information on the number and remuneration of employees. Form No. 1 (utilities)

- Sample. Comparison statement of the results of inventory of fixed assets. Form No. inv-18 (order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49)

- Sample. Comparison statement of the results of inventory of inventory items. Form No. inv-19 (order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49)

- Sample. Agreement on repayment of mutual debt

- Sample. Agreement on repayment of mutual debt

- Sample. Cover letter for the accounting report

- Sample. Accompanying register of documents. Form No. 16

- Sample. Certificate No. 1. Components of the actual cost of received material assets

- Sample. Certificate for the act of inventory of settlements with buyers, suppliers and other debtors and creditors (Order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49)

- Sample. Certificate of movement of the actually created reserve for possible loan losses

- Sample. Certificate of verification of compliance with the procedure for conducting cash transactions and working conditions with cash and compliance with clause 9 of Decree of the President of Russia of May 23, 1994 No. 1006

- Sample. Certificate of average monthly earnings for pension calculation

- Sample. Certificate of the amount of earnings taken into account when calculating the pension

- Sample. Certificate of balances of required reserves (Order of the Central Bank of the Russian Federation dated March 30, 1996 No. 02-77)

- Sample. Management balance sheet of the enterprise

- Sample. A conditional example of calculating the amount of funds subject to additional transfer by a credit institution to required reserves when using the right to intramonthly reduce required reserve ratios (Order of the Central Bank of the Russian Federation dated March 30, 1996 No. 02-77)

- Sample. A conditional example of calculating the amount of a fine for underpayment to required reserves (Order of the Central Bank of the Russian Federation dated March 30, 1996 No. 02-77)

- Sample. Accounting for telegraph expenses that will be deducted from the payment amount

- Cash flow statement of a medical insurance organization for compulsory medical insurance. Form No. 4a-insurer (Rosstrakhnadzor order dated April 16, 1996 No. 02-02-12)

- Cash flow statement of an insurance organization. Form No. 4-insurer (Order of Rosstrakhnadzor dated April 16, 1996 No. 02-02-12)

When to take it

State statistical bodies have supplemented the list of mandatory reporting with the new No. 57-T “Information on wages of employees by profession and position.” The unified form was approved by a separate Order of Rosstat dated July 15, 2019 No. 404, OKUD code - 0606007.

IMPORTANT!

Submit the new form 57-T to statistics for 2021 by November 30. Report once every two years. If the organization has already done this in 2021, there is no need to submit reports in 2021!

Report form: