The need to submit a corrective report, as a rule, arises if errors were discovered after the submission of the RSV-1 calculation, and this led to an underestimation of the amount of contributions payable. The provisions for making changes to the calculation are contained in Article 17 of Law No. 212-FZ dated July 24, 2009 and the Procedure for filling out the RSV-1 calculation (approved by Resolution of the Pension Fund Board of January 16, 2014 No. 2p). We will tell you in our article how to make an adjustment to the RSV-1, whether it is always necessary to submit a “clarification” and what nuances to take into account when submitting corrective and canceling persucheta information.

In what cases may an updated report be needed?

The grounds for filing an adjustment are contained in the provisions of the Tax Code of the Russian Federation. So, according to Art. 81 of the Tax Code of the Russian Federation , an adjustment is required if the calculation itself understates the amount that must be paid for a certain period.

It should be noted that the corrective document in this case is not new, but is directly related to the previous one.

However, it is important to take into account that in some situations, some errors lead to the fact that the report is not considered submitted at all. This means that the organization can face very impressive sanctions for violating the reporting procedure.

Such errors include:

- inaccuracies when filling out sections containing personalized accounting information;

- inaccuracies in determining the base, amount of payments and amount of contributions;

- discrepancies in calculating the amount of contributions for specific employees in relation to the total amount of contributions for the organization as a whole.

In all these cases, the organization is required to submit a new DAM form.

Reference! Submitting corrective reporting documentation in cases where a new report is required does not make any sense, since the previous DAM is considered not submitted at all.

Correction of errors in the calculation of insurance premiums for 2014

Errors in calculating insurance premiums can be caused by various reasons. These include accounting errors, non-application of changed legal norms, calculation of insurance premiums if the employee has already quit, and erroneously paid benefits. In order to correct the error, it is necessary to conduct an internal audit of the reports already submitted. In this case, the issue of correcting reporting will depend on whether there was an overpayment or arrears on insurance premiums.

How errors are corrected depends on who discovered the error and whether the error resulted in an understatement of insurance premiums paid. Errors that lead to underestimation of insurance premiums include the following:

- unlawful application of a reduced tariff;

- payment of benefits without supporting documents;

- arithmetic errors in accounting that lead to increased payments of contributions.

Errors that lead to overestimation of insurance premiums include excessive charging of insurance premiums:

- for payments to citizens of Belarus temporarily staying in the territory of the Russian Federation;

- for the amount of royalties excluding documented expenses associated with the fulfillment of obligations under the copyright or license agreement;

- for payments to a Group I disabled employee who submitted a disability certificate late.

Also, errors may be associated with the calculation of insurance premiums for non-taxable payments listed in Art. 9 of the Law of July 24, 2009 No. 212-FZ.

To find the mistake, it is recommended:

- recalculate the taxable base;

- recalculate the amount of insurance premiums;

- reflect corrections on the card;

- make corrective accounting entries for additional accrual of insurance premiums;

- make adjustments to previously submitted reports.

The rules for correcting errors made when calculating insurance premiums to the Pension Fund of Russia, the Federal Social Insurance Fund of Russia, and the Federal Compulsory Medical Insurance Fund are set out in Art. 17 of Law No. 212-FZ. According to the provisions of this article, errors are corrected only by the period during which they were committed. Following this rule in many cases obliges payers to submit an updated calculation of insurance premiums. The occurrence of the obligation to submit an updated calculation depends, as in taxation, on the consequences of the errors.

IMPORTANT IN WORK

Non-payment or incomplete payment of insurance premiums as a result of understating the base for their calculation, other incorrect calculation of insurance premiums or other unlawful actions (inaction) of employer-insurers is classified as a violation of the legislation of the Russian Federation on insurance premiums.

The error was discovered by the inspectors

The inspection body will request an explanation of the error. If the error led to an underestimation of the base subject to insurance premiums, then the payer of the contributions will be assessed penalties.

The error was discovered by the company itself (IP), and the error led to an underestimation of the contributions paid

The payer of insurance premiums is obliged to make the necessary changes to the calculation of accrued and paid insurance premiums and submit to the body monitoring the payment of insurance premiums an updated calculation of accrued and paid insurance premiums in the prescribed manner (clause 1 of Article 17 of Law No. 212-FZ).

GOOD TO KNOW

The procedure for submitting an updated calculation of insurance premiums is generally similar to the rules for filing updated tax returns when correcting errors that lead (or do not lead) to an understatement of the amount of tax payable.

The error was discovered by the company itself (IP), and the error did not lead to an underestimation of the contributions paid

If the payer of insurance premiums discovers in the calculation submitted to the body for control over the payment of insurance premiums errors that do not lead to an underestimation of the amount of insurance premiums payable, the payer of insurance premiums has the right to make the necessary changes in the calculation of accrued and paid insurance premiums and submit them to the body for control over the payment of insurance premiums. contributions, an updated calculation of accrued and paid insurance premiums in the manner established by this article. In this case, an updated calculation of accrued and paid insurance premiums, submitted after the expiration of the established deadline for submitting a calculation of accrued and paid insurance premiums, is not considered submitted in violation of the deadline (clause 2 of Article 17 of Law No. 212-FZ).

IMPORTANT IN WORK

If the payer of insurance premiums discovered in the calculation of accrued and paid insurance premiums submitted by him to the territorial branch of the fund (forms RSV-1, 4 FSS) the fact of non-reflection or incomplete reflection of information, as well as errors leading to an underestimation of the amount of insurance premiums payable, then he must make the necessary changes to the specified calculation and submit a revised version of it.

Correction of the underestimated amount of contributions according to the law

If the amount of insurance premiums is underestimated, then it is necessary to recalculate the amount of insurance premiums paid and make an additional payment.

When submitting an updated calculation (corrective calculation for the corresponding period) to the territorial control body, a number is entered in this detail indicating which account updated calculation for the same period is being submitted (for example, 001, 002, etc.) (clause 5.1 of section II “Filling out the title part of the calculation” The procedure for filling out the calculation form for accrued and paid insurance contributions for compulsory pension insurance to the Pension Fund of the Russian Federation and for compulsory medical insurance to the Federal Compulsory Medical Insurance Fund by payers of insurance premiums making payments and other benefits to individuals (form RSV-1 Pension Fund), clause 5.3 of Section II “Filling out the title part of the calculation” of the Procedure for filling out the calculation for accrued and paid insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity and for compulsory social insurance against accidents at work and occupational diseases, as well as expenses for payment of insurance coverage (Form-4 FSS)).

In this case, in the “Adjustment Type” field of the RSV-1 Pension Fund calculation, you should also indicate one of the proposed code options for the reason for submitting the updated calculation:

- code 1 is entered when clarifying the calculation regarding indicators related to the payment of insurance contributions for compulsory pension insurance (including additional tariffs);

- code 2 – clarification of the calculation regarding changes in the amounts of accrued insurance contributions for compulsory pension insurance (including at additional tariffs);

- code 3 – clarification of calculations regarding insurance premiums for compulsory medical insurance or other indicators that do not affect individual accounting information for insured persons.

The updated calculation of both RSV-1 and 4 FSS is presented in the form that was in force in the period for which errors (distortions) were identified (clause 5 of Article 17 of Law No. 212-FZ). To the updated RSV-1 form of the Pension Fund of the Russian Federation, personalized accounting documents must also be attached, prepared according to the form in force in the period for which errors were identified in relation to the insured persons, the data for which is being adjusted.

Not so often, but it is still possible that the updated calculation is submitted to the territorial branch of the fund before the deadline for its submission. In this case, it is considered submitted on the day of filing the updated form RSV-1 or 4 FSS (clause 3 of article 17 of Law No. 212-FZ).

If the inspection body found an error and added additional contributions, then these contributions must be reflected in the calculation form:

- on line 120 “Additional insurance premiums accrued from the beginning of the billing period” section. 1;

- line 121 “Including from amounts exceeding the maximum base for calculating insurance premiums” section. 1;

- in Sect. 4 “Amounts of additionally accrued insurance premiums from the beginning of the billing period.”

Example 1.

On January 22, 2015, the organization submitted the PFR RSV-1 calculation for 2014 to the territorial office of the Pension Fund. On February 7, the organization’s accountant discovered an error in the size of the base for calculating insurance premiums: when calculating it for December, 9,877 rubles were underaccounted. In connection with this, the policyholder submitted an updated calculation in accordance with the PFR form RSV-1 for 2014 to the territorial branch of the Pension Fund on February 11.

When calculating insurance premiums, the employer uses general insurance premium rates; employee income for January–December, included in the base for calculating insurance premiums, did not reach 624,000 rubles; the additional accrued amounts of insurance premiums and penalties were transferred on February 10.

In the adjusted calculation, the adjustment number 001 is indicated on the title page of the form, and 2 is indicated in the “Adjustment type” field.

Compared to the data entered in the originally submitted calculation form, the changes will affect:

- Section 1 “Calculation of accrued and paid insurance premiums”;

- subsection 2.1 “Calculation of insurance premiums by tariff” of section 2 “Calculation of insurance premiums by tariff and additional tariff”;

- Section 6 “Information on the amount of payments and other remunerations and the insurance experience of the insured person,” to be filled out for an individual whose income was not taken into account in the database when preparing the submitted RSV-1 Pension Fund calculation.

Unaccounted 9877 rub. will increase the values of the originally submitted calculation entered by:

- in columns 3 (total from the beginning of the billing period) and 6 (including for the third month of the last three months of the reporting period) lines 200 and 210 (amount of payments and other remunerations accrued in favor of individuals), 204 and 214 (bases for calculation of insurance contributions for compulsory pension insurance and compulsory health insurance) of the table in subsection 2.1;

- in columns 4 (the amount of payments and other remunerations accrued in favor of an individual) and 5 (the base for calculating insurance contributions for compulsory pension insurance from the amounts of payments and remunerations that do not exceed the maximum value of the base for calculating insurance contributions, in total) lines 400 (total from the beginning of the billing period) and 403 (including for the third month of the last three months of the reporting period) of the table in subsection 6.4 “Information on the amount of payments and other remuneration accrued in favor of an individual.”

From this amount, the organization accrued an additional 2172.94 rubles. = (9877 rub. x 22%) in the Pension Fund and 503.73 rub. = (8562 rub. x 5.1%) in the Federal Compulsory Medical Insurance Fund.

By the first of the indicated amounts (RUB 2,172.94), the indicators of the initially submitted calculation increase, entered:

- in columns 3 and 6 of line 205 (accumulated insurance contributions for compulsory pension insurance from amounts not exceeding the maximum base for calculating insurance contributions) of the table given in subsection 2.1;

- in column 3 (insurance contributions for compulsory pension insurance for periods starting from 2014) lines: 110 (insurance contributions accrued since the beginning of the billing period, in total);

- 113 (including for the third month of the last three months of the reporting period);

- 114 (total payable for the last three months);

- 130 (total payable) and 150 (balance of insurance premiums payable at the end of the reporting period) of the table in section 1;

The values of the initially submitted calculation of the RSV-1 Pension Fund of the Russian Federation are increased by the second amount (503.73 rubles), indicated:

- in columns 3 and 6 of line 215 (insurance premiums for compulsory health insurance) of the table of subsection 2.1;

- in column 8 (insurance premiums for compulsory health insurance) lines 110, 113, 114, 130 and 150 of the table in section 1.

In the “corrective” field of subsection 6.3 “Type of information correction” of section 6 of the calculation, an X is entered.

In section 6, with the type of information correction “corrective”, information is indicated in full, both correctable (correctable) and not requiring correction. The data in the corrective form completely replaces the data recorded on the basis of the “original” form on the individual personal account.

Subsection 6.6 “Information on corrective information” of Section 6 of the calculation is not filled out, since it is prescribed to be filled out in forms with the “initial” type of information if, in the last three months of the reporting period, the payer of insurance premiums adjusts the data submitted in previous reporting periods.

Since the updated calculation of insurance premiums for 2014 was submitted before the deadline for its submission - February 15, 2015 (clause 1, paragraph 9, article 15 of Law No. 212-FZ), the day for submitting the calculation is considered to be February 11.

ORIGINAL SOURCE

A calculation of accrued and paid insurance premiums is submitted to the territorial body of the Pension Fund on paper no later than the 15th day of the second calendar month following the reporting period, and in the form of an electronic document - no later than the 20th day of the second calendar month following the reporting period. contributions for compulsory pension insurance to the Pension Fund and for compulsory health insurance to the Federal Compulsory Medical Insurance Fund.

Article 15 of Law No. 212-FZ.

The organization had to pay the monthly obligatory payment for December no later than January 15 (clause 5 of Article 15 of Law No. 212-FZ), while the organization transferred additional amounts of insurance premiums on February 10. Due to the delay in payment, the policyholder must also pay a penalty.

Penalties are accrued for each calendar day of delay in fulfilling the obligation to pay insurance premiums, starting from the day following the deadline for payment of insurance premiums established by Law No. 212-FZ (clause 3 of Article 25 of Law No. 212-FZ). The day of payment of contributions is not included in the period of accrual of penalties for late payment of these insurance premiums, since the day of fulfillment of the obligation to pay insurance premiums cannot simultaneously be the day of delay in fulfilling this obligation in respect of which penalties are accrued (letter of the Ministry of Labor of Russia dated May 16, 2014 No. 17-4/B-211). Taking this into account, the delay in payment of insurance premiums amounted to 25 days ((16 + 9), where 16 and 9 are the number of days of delay in payment in January and February).

Penalties for each day of delay are determined as a percentage of the unpaid amount of insurance premiums. The interest rate of penalties is taken to be equal to one three hundredth of the refinancing rate of the Bank of Russia in force on these days (clauses 5, 6 of Article 25 of Law No. 212-FZ).

Penalties to the Pension Fund of Russia will amount to 14.94 rubles. (2172.94 rubles x 8.25%: 300 days x 25 days), in the Federal Compulsory Medical Insurance Fund - 3.46 rubles. (RUB 503.73 x 8.25%: 300 days x 25 days).

Non-accounting in the database for calculating insurance premiums for December is 9877 rubles. is an incorrect reflection of the fact of the organization’s economic activity, which is recognized as an error in accounting (clause 2 of PBU 22/2010). This error was identified before the end of the reporting year. An error in the reporting year, identified before the end of this year, is corrected by entries in the relevant accounting accounts in the month of the reporting year in which it was identified (clause 5 of PBU 22/2010).

Based on this, in February the following entries are made in accounting:

| Debit | Credit | Amount (rub.) | Operation |

| 07 February | |||

| 20 | 69 subaccount “Settlements with the Pension Fund of the Russian Federation” | 2172,94 | The amount of insurance contributions to the Pension Fund for December has been additionally accrued |

| 20 | 69 subaccount “Settlements with FFOMS” | 503,73 | The amount of insurance contributions to the Federal Compulsory Medical Insurance Fund for December has been additionally accrued |

| 10th of November | |||

| 99 | 69 subaccount “Settlements with the Pension Fund of the Russian Federation” | 14,94 | Penalties accrued to the Pension Fund for late payment of insurance premiums for December |

| 99 | 69 subaccount “Settlements with FFOMS” | 3,46 | Penalties have been accrued to the Federal Compulsory Compulsory Medical Insurance Fund for late payment of insurance premiums for December |

| 69 subaccount “Settlements with the Pension Fund of the Russian Federation” | 51 | 2172,94 | The additional accrued amount of insurance premiums was transferred to the Pension Fund of the Russian Federation |

| 69 subaccount “Settlements with the Pension Fund of the Russian Federation” | 51 | 14,94 | Penalties have been transferred to the Pension Fund of Russia |

| 69 subaccount “Settlements with FFOMS” | 51 | 503,73 | The additional accrued amount of insurance premiums was transferred to the FFOMS |

| 69 subaccount “Settlements with FFOMS” | 51 | 3,46 | Penalties have been transferred to the Federal Compulsory Compulsory Medical Insurance Fund |

If the policyholder does not have time to submit an updated calculation before the deadline for submitting the calculation and does so after its end, then in two cases he has the opportunity to be released from liability.

Let us remind you that for incomplete payment of insurance premiums as a result of underestimating the base for their calculation or other incorrect calculation of insurance premiums, a fine in the amount of 20% of the unpaid amount of insurance premiums may be collected from the payer. Exemption from this liability is possible upon submission of a “clarification” (clause 4 of article 17 of Law No. 212-FZ):

- already after an on-site inspection for the corresponding billing period, as a result of which the inspectors did not find the facts and errors that appeared in the updated calculation;

- until the moment when the payer learned about the discovery by the territorial department of the fund of facts of non-reflection or incomplete reflection of information, as well as errors leading to an underestimation of the amount of insurance premiums payable, or about the appointment of an on-site inspection for a given period.

But in the second case, before submitting the updated calculation, the payer must pay the missing amount of insurance premiums and the corresponding penalties.

End of example 1.

Let us assume that the calculation of 4 FSS for 2014 by the organization was submitted to the territorial branch of the FSS of Russia on January 12, the updated calculation - on February 11, arrears on insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity and for compulsory social insurance against accidents cases at work and occupational diseases resulting from non-accounting in the base for calculating insurance premiums for September 9877 rubles, as well as penalties accrued for the delay in payment of insurance premiums for September, were paid on February 10, when calculating insurance premiums for injuries, the organization uses tariff 0.3%.

From those not included in the database for calculating insurance premiums for September, 9,877 rubles. The policyholder in the FSS of Russia additionally accrued 286.43 rubles. = (9877 rub. x 2.9%) for disability insurance and 29.63 rub. = (9877 rubles x 0.3%) for injury insurance, which is reflected in accounting entries on February 7:

| Debit | Credit | Amount (rub.) | Operation |

| 20 | 69 subaccount “Settlements with the Federal Social Insurance Fund of Russia for disability insurance” | 286,43 | The amount of insurance contributions to the Federal Social Insurance Fund of Russia for disability insurance for December has been additionally accrued |

| 20 | 69 subaccount “Settlements with the Federal Social Insurance Fund of Russia for injury insurance” | 29,63 | The amount of insurance contributions to the Federal Social Insurance Fund of Russia for injury insurance for December has been additionally accrued |

| From these amounts, on November 10, penalties were accrued for the delay in payment of insurance premiums for September: RUB 1.97. = (286.43 rubles x 8.25%: 300 days x 25 days) - for disability insurance and 0.20 rubles. = (RUB 29.63 x 8.25%: 300 days x 25 days) – for injury insurance: | |||

| 99 | 69 subaccount “Settlements with the Federal Social Insurance Fund of Russia for disability insurance” | 1,97 | Penalties have been accrued to the Federal Social Insurance Fund of Russia for the delay in payment of insurance premiums for disability insurance for December |

| 99 | 69 subaccount “Settlements with the Federal Social Insurance Fund of Russia for injury insurance” | 0,20 | Penalties have been accrued to the Federal Social Insurance Fund of Russia for the delay in payment of insurance premiums for injury insurance for December |

| On the same day, the accrued amounts of insurance premiums for disability and injury insurance, as well as penalties, were transferred to the Federal Treasury to the account of the Social Insurance Fund: | |||

| 69 subaccount “Settlements with the Social Insurance Fund (by type of insurance)” | 51 | RUB 286.43 (29.63, 1.97, 0.20 rub.) | The amount of insurance premiums (penalties) for disability insurance (for injuries) has been transferred. |

In the updated calculation of 4 FSS, adjustment number 001 is indicated on the title page of the form.

When preparing an updated calculation, the general filling procedure is applied. The calculation is filled in completely, and not just the tables of the sections in which the indicators change.

Compared to the data entered into the originally submitted calculation form 4 of the FSS, the changes will affect individual rows of the tables:

- 1 “Calculations for compulsory social insurance in case of temporary disability” of Section I “Calculation of accrued and paid insurance contributions for compulsory social insurance in case of temporary disability and expenses incurred”;

- 3 “Calculation of the base for calculating insurance premiums” of Section I;

- 6 “Base for calculating insurance premiums” of Section II “Calculation of accrued and paid insurance premiums for compulsory social insurance against industrial accidents and occupational diseases and expenses for payment of insurance coverage”;

- 7 “Calculations for compulsory social insurance against accidents at work and occupational diseases” of section II of the calculation.

The amount not taken into account in the base for calculating insurance premiums for September is 9877 rubles. will increase the indicators of the initially submitted calculation of 4 FSS, introduced by:

- in columns 3 (total from the beginning of the billing period) and 6 (including for the third month of the last three months of the reporting period) lines 1 (amounts of payments and other remunerations accrued in favor of individuals) and 4 (total, the base for calculating insurance contributions) table 3 of section I;

- in column 3 (payments and other remuneration in favor of employees for whom insurance premiums are calculated, total) lines: 1 (total from the beginning of the billing period);

- 2 (including for the last three months of the reporting period);

- 5 (including for the third month) of table 6 of section II.

By the additional accrued amount of insurance premiums for disability insurance, 286.43 rubles, the indicators of the previously submitted calculation, indicated by the lines, increase:

- 2 (accrued for payment of insurance premiums) and the sublines of this line “for the last three months of the reporting period” and “3rd month”;

- 8 (total);

- 19 (debt due to the policyholder at the end of the reporting period) of Table 1 of Section I.

The additional accrued amount of insurance premiums for injury insurance, 29.63 rubles, increases the values of the initially submitted calculation, indicated by the lines:

- 2 (accrued for payment of insurance premiums) and the sublines of this line “for the last three months of the reporting period” and “3rd month”;

- 8 (total);

- 15 (debt due to the policyholder at the end of the reporting period) of table 7 of section II of the calculation.

ORIGINAL SOURCE

Payment of the calculated amounts of insurance premiums to the FSS of Russia and penalties and the submission of an updated calculation of 4 FSS to the territorial branch of the fund together allow the payer of insurance premiums to avoid liability for non-payment of insurance premiums.

— Subclause 1, clause 4, art. 17 of Law No. 212-FZ.

How to make a new report correctly

So, it has been established that the adjustment is submitted on a document of the same form as the erroneous calculation itself with the incorrect amount. This is important to consider because the 2021 DAM form has undergone significant changes compared to the 2021 form.

In the document itself, on its title page, the serial number of the adjustment itself is indicated. After this, current and updated information is entered into it. In addition, the information that was filled out correctly should also be transferred to the document.

However, this rule does not apply to Section 3 of the DAM, which specifies personal accounting data for employees. It includes only those related to employees for whom there were inaccuracies in the calculation of contributions.

In the RSV form used in 2021, in section 4 there is a field “Sign of cancellation of information about the insured person.” It must be filled out when submitting the adjustment. The code “1” is entered in the corresponding field.

How to submit updated data

The corrective form must be submitted in the same form as the main calculation. In this case, existing legislative requirements on this issue must be taken into account.

So, in 2021, in most cases, an electronic document is submitted. This applies to all those organizations in which the number of full-time employees exceeds 10 people. If the organization or enterprise has fewer employees, then the organization’s management has a choice between electronic document management and sending documents in traditional paper form.

Important! Failure to comply with the required form for submitting documentation leads to the fact that the DAM is recognized as not submitted, which is fraught with the imposition of additional penalties on the organization.

The reporting itself is submitted directly to the tax office, with which the organization is registered as a taxpayer.

It should be noted that according to similar rules, not only calculations are submitted in the DAM form, that is, related to the deduction of insurance premiums, but also tax returns. Adjustments to tax returns are permitted if an erroneous calculation of the amount of tax being calculated has led to the fact that it is actually less than it should be.

“Cancelling” adjustment of RSV-1 section 6

A “cancelling” adjustment is indicated in subsection 6.3 if the previously submitted accounting information must be completely removed, that is, cancelled. For example, an employee who had already been dismissed was mistakenly accrued wages and contributions.

For such employees, only subsections 6.1 – 6.3 are completed, and in subsection 6.4 you only need to indicate the category code of the insured person. The remaining subsections of section 6 will remain blank.

Please note that you need to submit the corrective RSV-1 in the same way as the initial calculation: if the number of insured persons is 25 people or more - only electronically, if the number is smaller, then you can submit the calculation electronically, or on paper.

Deadlines for submitting clarifications

The deadlines for submitting corrective documents under the DAM are also established by law.

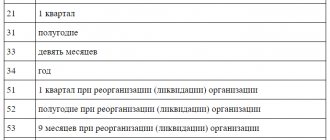

Thus, it has been determined that without consequences in the form of fines and penalties, the adjustment must be submitted before the deadline for submitting the calculation itself. Let us remind you that the DAM must be submitted by the 30th day of the month following the reporting quarter.

Accordingly, if an error is discovered before this deadline, the organization must pay the missing amount of insurance premiums, and then submit a corrective document to the tax office.

Attention! If the document is submitted after the 30th day, then, among other things, the organization has an obligation to pay penalties, which are accrued on the unpaid amounts of insurance premiums.