Kontur.Accounting - the optimal service for the simplified tax system

Automated calculation of taxes and transactions with employees.

The simplest accounting possible. The service itself will generate KUDiR, declaration and reports. Try for free

The founders of the organization distribute profits and pay dividends every year. LLCs using the simplified tax system distribute profits in the general manner, but the calculation and payment of dividends using the simplified system have their own peculiarities. In this article we will tell you how to calculate and pay dividends using the simplified tax system.

Differences in calculating dividends under different tax regimes

Comparative table combining all tax regimes for LLCs:

| simplified tax system | UTII | Unified agricultural tax | BASIC | |

| Dividend calculation | Dividends are paid from profits after paying a “simplified” tax - depending on the regime - 6% or 5–15%; Payment of dividends for the second type of regime is not a reason to include it in the “expenses” column and thereby reduce the tax base | Dividends are distributed among the founders based on the accounting report data | Taxation of dividends occurs according to Articles 346.5–346.15 of the Tax Code of the Russian Federation | Dividends are accrued based on the results of the first three months, half a year and year. Source: net income. Distributed among the founders according to the charter, otherwise - according to the share in the authorized capital of the LLC |

| Calculation of personal income tax and income tax | For a resident (individual, organization) – 13% of the amount; For other persons (foreign citizens and enterprises) – 15% | |||

Important! If a Russian company owns half a share or more of it in the authorized capital of a company for 365 days before the order to pay dividends, then no tax is paid on the amount of profit.

Conditions of use

^Back to top of page

Employees<100 people

Income < 150 million rubles.

Residual value <150 million rubles.

Separate conditions for organizations:

- The share of participation of other organizations in it cannot exceed 25%

- Prohibition of the use of the simplified tax system for organizations that have branches

- An organization has the right to switch to the simplified tax system if, based on the results of nine months of the year in which the organization submits a notice of transition, its income did not exceed 112.5 million rubles (Article 346.12 of the Tax Code of the Russian Federation)

Calculation of dividends under the simplified tax system

The procedure for paying dividends is determined by the following documents:

- Tax code.

- Federal Law No. 14 “On LLC”.

- Charter of the enterprise.

- Minutes of the meeting of the founders of the company.

When preparing the charter, participants must take care to draw up the following points:

- restrictions on the distribution of dividends (additional conditions not specified in the law under which payment cannot be made);

- the procedure for dividing profits - taking into account the proportionality of investments or according to another scheme.

On the balance sheet, dividends are distributed in the column “Retained income” (1370). According to simplified accounting reports, the company’s net income on the simplified tax system can be found out by the balance of account 84 “Uncovered loss, Retained income.” Data for this year – “Net income/loss” (line 2400). When paying dividends to participants, the company, which is on the simplified tax system, is considered a tax agent in relation to profits and personal income tax. Consequently, the enterprise must withhold and transfer these taxes to the state budget.

Basic moments

First, let’s figure out what is meant by the word “dividends”, what regulations regulate the accrual and procedure for their payment. This will avoid unnecessary problems when keeping records.

Definition

Every year, enterprises are faced with the issue of income distribution and dividend payment. What is included in this concept for tax purposes?

In accordance with Article 43, paragraph 1 of the Tax Code, dividends are considered to be all income of shareholders (participants) on the shares that they own.

Such amounts are received from the company when distributing net income according to the proportions of the participants’ shares in the authorized capital of such an enterprise.

Net income is the profit that remains after taxation (Article 42, paragraph 2 of Law No. 208-FZ of December 26, 1995).

Net income indicators are determined based on accounting data. That is why enterprises using the simplified tax system must keep accounting records.

Normative base

If you pay dividends, you are a tax agent in accordance with the rules of Art. 214 paragraph 2 and art. 275 clause 2 of the Tax Code.

Tax agents are persons who undertake to determine and withhold a specific type of fee from the taxpayer for the purpose of subsequently transferring it to the state treasury (Article 24, paragraph 1 of the Tax Code).

So, if an organization pays dividends to its participants, then these rules will apply.

Enterprises under a special tax regime (simplified) must also perform the functions of tax agents (Article 346.11, paragraph 5 of the Tax Code).

Taxes on dividends withheld by tax agents must be transferred to the budget no later than the day following the day of payment (Article 287, paragraph 4 of the Tax Code).

Tax on the income of an individual must be paid to the treasury on the day of payment of profits (Article 226, paragraph 6 of the Tax Code). In the event that the founder is one person, then the decision on payment will be made by him alone, having drawn up the appropriate documentation.

Dividends issued to a participant are a taxable item (personal income tax) at a rate of 9 percent. If the shareholder is not a resident of the Russian Federation, then you will have to pay 15%.

When distributing dividends in favor of Russian enterprises, rates of 0 and 9% are applicable. The organization has the right to use 0% in relation to participants who owned 50% of the contribution to the authorized capital throughout the year. 9% will be paid by all other companies (Article 284, paragraph 3 of the Tax Code).

A foreign company will have to calculate tax at a rate of 15%.

Payments that are not dividends

By law, dividend payments cannot be:

- Shares that are the property of the founder.

- Investments in a non-profit company necessary for statutory activities not related to entrepreneurship.

- Amounts paid upon liquidation of a company, if they do not exceed the amount of the founder’s contribution to the authorized capital of the LLC.

Important! Dividend payments are exclusively amounts from the net profit of the LLC, proportional to the participant’s share.

Expenses paid with borrowed funds

— “Simplified” include in expenses the cost of a fixed asset if two conditions are met: full payment and commissioning. Moreover, it does not matter from what means the payment was made. This is confirmed by the letter of the Ministry of Finance of Russia dated January 13, 2005 No. 03-03-02-04/1/2. You can rest assured and write off the cost of the fixed asset, paid for with a loan, as expenses from the moment of commissioning. — Is it necessary to reflect the loan repayment in the Income and Expense Accounting Book?

If you have any questions, you can consult for free via chat with a lawyer at the bottom of the screen or call by phone (consultation is free), we work around the clock.

- It is necessary, but only in column 6 of section 1 “Expenses - total”, since the return of borrowed funds is not an expense that reduces the tax base, just like the amount of the loan upon receipt is income.

Payment of dividends for various groups of individuals and organizations

The differences relate only to the amount of taxation:

| Category | Withholding tax amount | |

| Private person (Russian citizen) | Personal income tax – 13% | |

| Private person (non-resident) | ||

| IP | ||

| Russian company with: half or more of the share in the authorized capital; 50% of depositary receipts from the deposit amount | Income tax | 0% |

| Other Russian companies | 13% | |

| Foreign corporations | 15% | |

Important! A resident is an individual who resides on the territory of the Russian Federation for more than 183 days during the year.

Enter the site

If you have any questions, you can consult for free via chat with a lawyer at the bottom of the screen or call by phone (consultation is free), we work around the clock.

Students who successfully complete the program are issued certificates of the established form. Students who successfully complete the program are issued certificates of the established form. Having considered the issue, we came to the following conclusion: Amounts of personal income tax withheld by an organization from the income of an individual in the form of dividends are not included in expenses that reduce the tax base for taxes paid in connection with the application of the simplified taxation system. And before submitting updated returns, it is necessary to pay the amount of tax arrears and the corresponding penalties. The founders of a Russian organization, who are individuals, when receiving income in the form of dividends from a Russian organization, are recognized as payers of personal income tax. The amount of personal income tax in relation to income from equity participation in an organization received in the form of dividends is determined taking into account the provisions of Art. Based on clause Before

Liability for non-payment of dividends

Dividends may not be paid in two cases:

- No charges, no payments. If there was no order to accrue dividends, then failure to pay dividends in this tax period does not have any consequences for the LLC.

- There is accrual, no payment. Such dividends cannot be considered received. Therefore, taxes cannot be charged on them. The founders have the right to appeal this state of affairs in court.

Despite the fact that, according to Article 28 of Federal Law No. 14-FZ, the procedure for paying dividends is established directly by the founders, the waiting time for payments should not exceed 60 days after the order for the accrual of funds is issued. If the company does not pay the money within this period, then by law the participants have the right to demand 1/360 of the refinancing rate for each overdue day. Read also the article: → “Tax on dividends for individuals and legal entities. 2 calculation examples”

If the LLC fails to pay the funds due to its own fault, then the head of the enterprise can be held administratively liable. The fine for the enterprise will be 500–700 thousand rubles.

Rates and payment procedure

^Back to top of page

1Transition to the simplified tax system simultaneously with the registration of individual entrepreneurs and organizations. The notification can be submitted along with a package of documents for registration. If you have not done this, then you have another 30 days to think about it (

clause 2 art. 346.13 Tax Code of the Russian Federation

)

2Transition to the simplified tax system from other taxation regimes. The transition to the simplified tax system is possible only from the next calendar year. Notification must be submitted no later than December 31 (

clause 1 art. 346.13 Tax Code of the Russian Federation

)

Transition to the simplified tax system with UTII from the beginning of the month in which their obligation to pay the single tax on imputed income was terminated (clause 2 of article 346.13 of the Tax Code)

In this case, the taxpayer must notify the tax authority about the transition to the simplified tax system no later than 30 calendar days from the date of termination of the obligation to pay UTII.

The notification can be submitted in any form or in the form recommended by the Federal Tax Service of Russia.

^Back to top of page

Tax amount=Tax rate*Tax base

For a simplified taxation system, tax rates depend on the object of taxation chosen by the entrepreneur or organization.

For the object of taxation “income” the rate is 6%.

According to the laws of the constituent entities of the Russian Federation, the rate can be reduced to 1%. Tax is paid on the amount of income.

When calculating the payment for the 1st quarter, income for the quarter is taken, for the half-year - income for the half-year, etc.

If the object of taxation is “income minus expenses”, the rate is 15%.

At the same time, regional laws may establish differentiated tax rates according to the simplified tax system in the range from 5 to 15 percent. The reduced rate may apply to all taxpayers or be established for certain categories. In this case, to calculate the tax, income is taken, reduced by the amount of expense.

We suggest you read: How to challenge a donation agreement for an apartment (real estate){q}

For entrepreneurs who have chosen the “income minus expenses” object, the minimum tax rule applies: if at the end of the year the amount of calculated tax is less than 1% of the income received for the year, a minimum tax is paid in the amount of 1% of the income received.

When applying a simplified taxation system, the tax base depends on the selected object of taxation: income or income reduced by the amount of expenses:

- The tax base under the simplified tax system with the object “income” is the monetary value of all income of the entrepreneur.

- On the simplified tax system with the object “income minus expenses,” the base is the difference between income and expenses. The more expenses, the smaller the size of the base and, accordingly, the tax amount will be. However, reducing the tax base under the simplified tax system with the object “income minus expenses” is possible not for all expenses, but only for those listed in Art. 346.16 Tax Code of the Russian Federation.

Income and expenses are determined on an accrual basis from the beginning of the year. For taxpayers who have chosen the “income minus expenses” object, the minimum tax rule applies: if for the tax period the amount of tax calculated in the general procedure is less than the amount of the calculated minimum tax, then a minimum tax is paid in the amount of 1% of the actual income received.

An example of calculating the amount of an advance payment for an object “income minus expenses”

During the tax period, the entrepreneur received income in the amount of 25,000,000 rubles, and his expenses amounted to 24,000,000 rubles.

- We determine the tax base of

25,000,000 rubles. — 24,000,000 rub. = 1,000,000 rub. - We determine the amount of tax

1,000,000 rubles. * 15% = 150,000 rub. - We calculate the minimum tax of

25,000,000 rubles. * 1% = 250,000 rub.

You need to pay exactly this amount, and not the amount of tax calculated in the general manner.

The laws of the constituent entities of the Russian Federation may establish a tax rate of 0% for two years for individual entrepreneurs registered for the first time and carrying out activities in the production, social and (or) scientific spheres, as well as in the field of consumer services to the population. From September 29, 2021, services for providing places for temporary residence have been added to this list (clause 4 of Article 346.20 of the Tax Code of the Russian Federation).

The validity period of these tax holidays is until 2021.

Features of dividend payments under the simplified tax system

When paying dividends to simplified companies, you should pay attention to the following nuances:

- Such payments are made no more often than once a quarter. The recommended period is once a year (this makes it easier to calculate the company’s profit).

- Payment is made only by decision of all participants. A general meeting cannot be held earlier than two months after the close of the previous reporting period.

- The basis for payment is accounting data.

- Payments are made only when the authorized capital is fully paid.

- If the amount of the authorized capital does not “reach” the net income, the payment of dividends is impossible.

- If the company is declared insolvent, then the accrual of dividends is prohibited.

- For an enterprise using the simplified tax system, net profit is the difference in income under accounting and the single tax.

When and how to pay dividends to the founder of an LLC using the simplified tax system

This type of payment is the prerogative of the LLC. Consequently, they have nothing to do with individual entrepreneurs, regardless of the tax system (OSN, Unified Agricultural Tax, simplified tax system, UTII). At the same time, an individual entrepreneur can receive and distribute dividends if he is also the founder of the company. The profit of an individual entrepreneur is taxed within its own regime and, unlike an LLC, the entrepreneur can freely dispose of it without waiting for an order to pay dividends.

| ★ Best-selling book “Accounting from scratch” for dummies (understand how to do accounting in 72 hours) > 8,000 books purchased |

https://www.youtube.com/watch{q}v=ytcreatorsru

LLC income is distributed among the founders according to the charter. If there is no clause regarding the payment of dividends, then the proceeds are distributed in proportion to the invested share of each participant. If he has a percentage in the authorized capital, say, 45%, then the share in the distribution of profits will be the same.

If the company’s net profit at the end of the year turns out to be negative, then the founders cannot claim dividends, and the LLC does not have the right to pay dividend income to the founders. Also in this situation, it is important to understand that the net profit indicator has nothing to do with the balance of funds in the current account or in the cash register at the end of the year.

When paying dividends annually, you must comply with the deadlines provided for by the above-mentioned law on LLCs. The decision on the distribution of profits between the founders is made at the annual meeting of the founders of the LLC. Such a meeting should be held strictly in March-April of the year following the reporting year. The payment of dividends itself must be made within 60 days after the corresponding decision is made on the distribution of profits between the participants of the LLC.

When paying profits to the founders, 13% of personal income tax is withheld from it. Contributions to funds, as is the case when paying wages to employees, are not accrued in this case. Based on the results of the year in which the company paid profit to the founders, this fact is reflected in income certificates in form 2-NDFL. That is, if we are talking about, say, profit for 2021, then it will be paid in 2019, and accordingly, information about this income of an individual will appear in the 2-NDFL certificates for 2021, which the company will submit in 2021.

However, at the moment, the legislation provides for the submission by companies - tax agents of another report on payments to individuals - a quarterly certificate 6-NDFL. Data on dividend payments in this certificate will also be reflected upon the fact of their implementation, that is, when paying income based on the results of 2021, for example, in May 2021, the amount paid to the founder must be taken into account in the 6-NDFL certificate submitted based on the results of the 2nd quarter of 2016 of the year.

Participant's refusal to pay dividends

The period within which a participant can demand accrued dividends from the LLC is from 60 days to three years, counted from the date of expiration of the two-month period. If the founder does not apply for money, then the unclaimed funds go to the item of undistributed income of the enterprise.

However, the fact of refusal from them is not provided for by law. But the recipient of dividends has the right to relieve himself of all obligations if this does not violate the rights of the other founders. Such a step should be recorded in writing, where the founder renouncing his rights must specify the purposes to which funds from his share should be directed. The company can spend this amount on these needs without waiting for the expiration of three years.

Despite the fact that there is no fact of receipt of income, personal income tax or income tax on this amount is withheld on the day when the founder signed the document on refusal. If a participant ignores the payment of profits, no tax is charged on them.

The concept of dividends and conditions for their accrual

Any commercial structure is created to make a profit.

But the procedure for receiving it by owners may be different. For an individual entrepreneur (IP), all business assets, including cash, are personal property. He can dispose of them arbitrarily: withdraw cash, transfer to his bank account, etc. Of course, one should not get carried away with this, because responsibilities to staff, counterparties and the payment of taxes do not disappear anywhere. But for our topic, it is important that individual entrepreneurs do not have a special mechanism for generating profit, that is, the concept of dividends does not apply to it.

But for the founders of legal entities, everything is not so simple. To receive their share of the company's income, owners must:

- Determine the financial result (it, of course, must be positive).

- Pay due mandatory payments from profits.

- Check if they have the right to distribute income. The restriction may be due, for example, to incomplete payment of the authorized capital or to the difficult financial situation of the company.

- Hold a general meeting at which a decision is made on the procedure for distributing profits and specific amounts of payments.

These payments in favor of the founders are called dividends.

A sample decision on the payment of dividends can be found here

Issuance of accountable money after purchase

for their purchases. Can I include the cost of inventory items in expenses? - You can, although there is one thing. Tax authorities insist that accountable disbursement of funds must occur before spending, not after. Therefore, follow-up reporting may raise doubts. If such a turn is undesirable for you, draw up a loan agreement with the employees who purchased the goods and materials. The employee allegedly provided a loan to the organization, and the organization, as soon as he made a purchase, returned the loan to him. We guarantee that there will be no friction with the tax authorities then.

Should payments from the net profit of previous years be recognized as dividends?

Payments from the profits of previous years, in all likelihood, can also be classified as dividends. The fact is that the legislation (tax and civil) does not contain a ban on the issuance of dividends from past profits (Article 43 of the Tax Code of the Russian Federation, Article 28 of Law No. 14-FZ, Article 42 of Law No. 208-FZ).

The regulatory authorities in their explanations also adhere to this point of view. Confirmation is contained in letters from the Ministry of Finance of Russia dated 03/20/2012 No. 03-03-06/1/133, dated 04/06/2010 No. 03-03-06/1/235 and the Federal Tax Service of Russia for Moscow dated 06/08/2010 No. 16-15 / [email protected] , dated June 23, 2009 No. 16-15/063489.

The Ministry of Finance clarifies that such payments are considered dividends if one condition is met: the net profit was not sent to the reserve fund or the employees' corporatization fund. And the tax service believes that such a procedure for distributing profits should be reflected in the company’s charter.

However, if you look at the previous explanations of the financial department, you will find some inconsistency there. Thus, the Ministry of Finance in letters dated 06/17/2010 No. 03-03-06/1/415, dated 03/17/2008 No. 03-04-06-01/60 and dated 02/06/2008 No. 03-03-06/1/83 approves that such issues are not his competence. And the letter dated 08/23/2002 No. 04-02-06/3/60 states that if an organization needs to pay dividends, then this can only be done at the expense of profits generated in the just past tax period.

Judicial practice shows: arbitrators are in favor of paying dividends from past profits (resolutions of the FAS North Caucasus District dated January 23, 2007 No. F08-7128/2006, FAS East Siberian District dated August 11, 2005 No. A33-26614/04-S3- Ф02-3800/05-С1). That is, the decisions contain indirect confirmation: such dividends should be taxed.

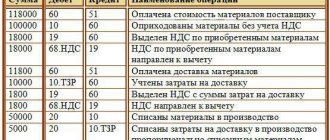

Read in this material how accounting policies are structured under the simplified tax system.

Insurance and labor costs

- Include. These contributions are included in the costs of compulsory insurance of employees and property specified in subparagraph 7 of paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation. — What about personal income tax and paid sick leave? — Personal income tax transferred to the budget from wages and temporary disability benefits issued are classified as labor costs. They will reduce your tax base based on subparagraph 6 of paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation. — And one more thing: we voluntarily insure inventory balances. Is it possible to include our insurance costs in calculating the tax base? - Unfortunately no. The costs of voluntary insurance are not included in the list of expenses that reduce the tax base for the single tax and are listed in paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation.

If the travel company is an agent

— If an agency agreement is concluded, then the income that affects the amount of tax should really only include remuneration. And this does not contradict the cash method: income will include the amount that was actually received from the principal or withheld from his income in accordance with the concluded agreement. — What will happen to the expenses in this case?

I mean, is it possible to reduce income for any expenses? If you have any questions, you can consult for free via chat with a lawyer at the bottom of the screen or call by phone (consultation is free), we work around the clock.

- Of course you can. The agent's single tax base under the simplified tax system is reduced by expenses that fell entirely on the agent, that is, were not reimbursed by the principal. Of course, if these expenses are named in the list of paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation, paid, documented and economically justified.

Learn how to prepare management reports in our new online course. Owners are willing to pay more for management reports than for tax reports. We'll give you an algorithm for setting up reports and show you how to integrate them into your daily accounting. Distance learning. We issue a certificate. Sign up for the course “Everything about management accounting: for accountants, directors and individual entrepreneurs.” For now for 3500 instead of 6000 rubles.

Waybills

- Yes, they are needed. “Simplified” firms are exempt from accounting in full, but, like all other companies, they are required to prepare primary documents. Gasoline expenses must be documented, including travel documents. However, keep in mind: if you do not have a motor transport company, you can independently develop a waybill form (it is not necessary to use the one approved by Resolution of the State Statistics Committee of Russia dated November 28, 1997 No. 78). But at the same time, it must indicate all the details of the primary document listed in paragraph 2 of Article 9 of the Federal Law of November 21, 1996 No. 129-FZ “On Accounting”. Similar explanations are given in the letter of the Ministry of Finance of Russia dated February 20, 2006 No. 03-03-04/1/129.

Accounting for intangible assets

If you have any questions, you can consult for free via chat with a lawyer at the bottom of the screen or call by phone (consultation is free), we work around the clock.

— Since your object of taxation is income, you do not have tax accounting for expenses, including intangible assets.

But for acquired intangible assets it is required to keep accounting records in accordance with paragraph 3 of Article 4 of the Federal Law of November 21, 1996 No. 129-FZ. Thus, if you do not keep accounting records in full, then you must fill out special registers for intangible assets, recording acquisition, depreciation and disposal. — What if we sell trademarks? — In tax accounting, you need to reflect cash received from sales as income, and in accounting, the disposal of intangible assets.