Accounting account 97 is used to reflect summarized information about the amounts of expenses actually incurred in the current reporting period, but relating to future periods. How to account for future expenses and what transactions reflect transactions on account 97 - you will find answers to these questions in our article.

Characteristic

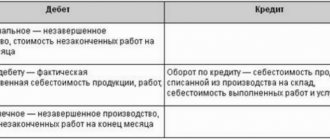

This item may reflect expenses related to mining and preparatory work, development of production facilities, units, installations, and other production equipment. Account 97 in the balance sheet shows the costs associated with the reclamation of land plots and carrying out other environmental work, as well as with measures to prepare production for operation during the season. The article covers amounts for the repair of objects belonging to the category of fixed assets, carried out unevenly throughout the year (when the enterprise does not form an appropriate fund or reserve), and so on. The data contained in accounting account 97 for expenses is written off from the debits:

- Account 20 for main production.

- Account 26 for general business expenses.

- Account 23 for auxiliary production.

- Account 44 in selling costs.

- Account 25 for general production expenses and so on.

Analytical accounting for cost items for upcoming periods is carried out in accordance with the types of costs.

Entries to record revenue recognition

In accounting, to reflect transactions describing the formation of the financial result for the period, account 90 is used with subaccounts for separate reflection:

- revenue;

- cost of products or services sold;

- VAT;

- excise taxes;

- profit or loss.

This account reflects the revenue received from the main activities of the company (types of activities classified as ordinary are specified in the organization’s charter), revenue from other activities is reflected in account 91 “Other income and expenses.” Thus, the proceeds from the sale of a fixed asset will not be reflected in account 90, but will go to account 91.

D 62 K 90.1 - this entry reflects the recognition of revenue from the sale of goods and the accrual of accounts receivable.

Accounting uses the accrual method – i.e. Revenue is recognized when the goods pass to the buyer, not when cash is received for the transaction.

Specifics

In the capitalization provision given in the paragraph above, however, a significant addition should be made. In particular, the expenses of the upcoming reporting years include those costs incurred that cannot be recovered in future periods. It follows from this that accounting account 97 is included in the category of financial distribution items. Its specificity lies in the fact that the amount of costs actually incurred - usually cash paid - turns out to be higher than the costs that relate to the current period. It can be represented like this:

A – B = C, where:

- the amount of expenses that are accrued or paid is A;

- expenses that relate to the reporting year when expenses A - this is B;

- costs of future periods are B.

What applies to deferred expenses?

Deferred expenses mean the preparatory costs that an organization incurs to generate income in the future. According to legislative norms, the debit of account 97 can reflect expenses for:

- the right to use intellectual property;

- preparatory work (seasonal, mining, start-up and other expenses);

- loan servicing;

- interest accrued on the bill amount.

The basis for reflecting amounts as deferred expenses are primary documents confirming the receipt of income in the future (contract agreement, license agreement, etc.).

Explanation

In many educational publications, as well as in practice, examples are often given of cases relating to the issue of magazines and newspapers, pre-paid rent, an advance payment for telephone services paid for several months, payment of interest on loans in advance and other similar situations. All these expenses are not related to the costs of future periods. This is due to the fact that if the editorial office that publishes magazines and newspapers fails to fulfill its obligations, for example, it will have to return the amounts paid. If the landlord violates the contractual terms, he is also obliged to reimburse part of the unused funds. Thus, if expenses were incurred, and money or other assets were contributed to a counterparty or correspondent, we are not talking about deferred expenses, but about ordinary receivables.

Procedure for closing accounting accounts

At the end of the calendar year, all economic entities sum up the results of their activities. The main result of a company’s work is its financial result: profit or loss. To determine how effectively an organization operated, it is necessary to draw up accounting records and determine the financial result. And this procedure is impossible without closing some accounting accounts.

Every month, the accountant checks the balances of the cost and financial results accounts:

- sch. 25, 26, 28 should be closed at the end of the month;

How to write off selling expenses - read the article “Accounting entries for business expenses.”

- sch. 20, 23, 29 may have work in progress, or may be completely closed - this depends on the specifics of the organization’s economic activities; on account 44 there may also be a balance - the company's transportation costs;

- sch. 90 and 91 do not have balances at the end of the month as a whole, however, amounts accumulate in each subaccount that are closed with final transactions at the end of the year.

By the end of the calendar year, the accountant needs to identify the financial result. It is determined by the amounts accumulated in the account. 99.

For information on the procedure for closing these accounts at the end of the year and calculating the amount of profit/loss, read the article “How and when to reform the balance sheet?”

Explanations on the Plan

The above approach formed the basis of the new Instructions. In particular, from the explanations that accompany accounting account 97, the previously present provision that this article may reflect costs related to the payment of rent for the upcoming period is excluded. Many experts believe that the list of expenses given in the new Plan is quite rational. In addition, PBU 10/99 (clause 3) contains an indication that advance payments, deposits, advances, etc. cannot be recognized as expenses for future periods. In practice, however, disputes often arise between accountants and tax agents, which often end in court.

We close accounting account 90 “Sales”

At the end of the reporting month, the company is obliged to determine the financial result of its activities. This operation is a comparison of subaccounts. 90. That is, the accountant compares the indicators of subaccount 90-1 “Revenue” and the value of cost of sales, which is defined as the sum of subaccounts 90-2 “Cost”, 90-3 “VAT”, 90-4 “Excise taxes”, 90-5 “Trade and export duties."

If the company made a profit (revenue exceeded total costs), then the accountant generates the following entry:

Dt 90-9 Kt 99 - profit from sales is reflected.

If the company operates at a loss (revenue is lower than total costs), then the following entry is recorded:

Dt 99 Kt 90-9 - reflects the monthly loss for the company’s activities.

Consequently, subaccounts. 90 may have a balance at the end of the reporting month, but the total value of the synthetic BSC must be equal to zero.

Which accounts are closed at the close of the year? The following accounting entries are generated for this account at the end of the year:

| Operation | Debit | Credit |

| The “Revenue” sub-account was closed at the end of the year | 90-1 | 90-9 |

| The cost of production is included in the financial result | 90-9 | 90-2 |

| VAT is written off in favor of profits and losses | 90-9 | 90-3 |

| Excise taxes are included in the financial results of operations | 90-9 | 90-4 |

| Export trade duties written off at the end of the year | 90-9 | 90-5 |

Static reporting

In theory, liabilities and property act as accounting objects. International standards for financial reporting are based on this concept. In fact, there is no room here for the category of future expenses. This is due to the fact that account 97 in the balance sheet does not imply either liabilities or assets. This is considered a “black hole” in the asset world. In fact, it contributes to a clearer determination of the financial results of the enterprise. This “hole” acts as evidence of the superiority of scientific theory over common sense. This article is present in the accounting of actually arising obligations and property not for the expenses of upcoming periods, but in the course of managing financial indicators. But if the state of the enterprise is assessed, the company’s cash flows are analyzed, then the costs of future years should be excluded from the reporting.

Account 84 “Retained earnings (uncovered loss)”

The result of a company's commercial activities can be either profit (if income exceeds expenses) or loss (in the opposite situation).

To reflect and accumulate data on financial results in accounting, it is customary to use account 84 “Retained earnings (uncovered loss).” This account contains information about the net total amount accumulated by the company at the end of the relevant reporting period. In other words, account 84 reflects not only the net profit (NP) generated in the current period, but along with it also the retained earnings of previous years (NP) or uncovered loss (UN).

ATTENTION! The state of emergency for the past year is shown on line 2400 of the financial results report (hereinafter referred to as the report). The balance of NP or NU minus dividends can be seen in line 1370 of the balance sheet.

In the tax guide from ConsultantPlus you will find step-by-step instructions for filling out line 1370 of the balance sheet. If you do not have access to the K+ system, get a trial online access for free.

How the company’s PE is calculated, see the article “How to calculate net profit (calculation formula)?” .

The amount of NI for previous years is indicated by the credit turnover of account 84. In circumstances where the company received NI in the current year, the company compensates for it from retained earnings remaining from previous years. If the company did not have NP or NU in previous years, the financial result indicated in line 1370 of the balance sheet (taking into account the payment of dividends) will be equal to the PE from the report.

Read about the nuances of reflecting retained earnings in the balance sheet in the material “Retained earnings in the balance sheet (nuances).”

Debit

Based on the information given above, the question arises about what a specialist should attribute to the DB account. 97. Anything that is normally included is subject to property tax. As stated above, certain expenses should be reported as net accounts receivable. Using this approach, the specialist removes the relevant objects from taxation. In account 97 it is necessary to include only those costs that the company incurred, and there is no one to return them to. First of all, these are the costs of geological exploration, mining, preparatory and survey work associated with the seasonality of the supply of goods, the provision of vacations, production, repair of operating systems, reclamation, acquisition of licenses, recruitment, assignment of specialists, economic activities in the absence of sales, and so on. The specificity of all these expenses is that the company has already incurred them and, as a rule, after that they cannot be reimbursed by anyone.

Deferred expenses when obtaining a software license

One of the most common transactions on account 97 is the reflection of deferred expenses associated with the conclusion of license agreements for the use of software.

Let's consider an example: in August 2015, Molniya LLC entered into a license agreement with Computer Service JSC. Under the agreement, Molniya LLC receives the rights to use the software for a period of 3 years. The cost of the contract is a one-time payment in the amount of RUB 342,500.

The following entries were made in the accounting of Molniya LLC:

| Dt | CT | Description | Sum | Document |

| Funds were transferred in favor of Computer Service LLC as payment under the license agreement | RUB 342,500 | Payment order | ||

| 97 | The cost of the contract is included in deferred expenses | RUB 342,500 | License agreement | |

| 012 | The software is accounted for on an off-balance sheet account | RUB 342,500 | License agreement | |

| 20 (, 44…) | 97 | Monthly write-off of expenses for using the software (RUB 342,500 / 36 months) | RUB 9,514 | License agreement |

Write-off

“Temporary capital” will be included in costs for the reporting periods to which they should be attributed. This can be done either in relation to the time periods themselves, if these are indirect costs that occur at a specific time, or they act as direct costs related to a specific volume of production. During the write-off process, account 97 is credited. In this case, expense items that relate to the current reporting time are debited. The previous Instructions for the plan of accounts indicated that the periods during which it is necessary to write off expenses of future periods for production costs and other sources are regulated by law and other regulations. There is no such provision in the new recommendations. According to the Regulations on Accounting and Reporting, the enterprise has the right to determine the write-off period for expenses of future periods independently.

Questions and answers on using account 97

Question: What are the reasons for the changes in accounting for deferred expenses?

Answer: Associated with the following changes:

- a new edition of clause 65 “Regulations on accounting and financial reporting” (as amended by Order of the Ministry of Finance of Russia No. 186n dated December 24, 2010), from which the concept of “deferred expenses” is excluded;

- exclusion from the new form of the balance sheet (approved by Order of the Ministry of Finance of Russia No. 66n dated July 2, 2010) of a direct mention of the line “Deferred expenses”.

Conclusion : Changes in the procedure for applying account 97 are associated with amendments to a number of regulatory documents on accounting.

Question: For what reason were changes made to the accounting of deferred expenses and their reflection in the financial statements?

Answer : Introduced with the aim of streamlining accounting, systematizing reflected data and bringing it closer to international financial reporting standards (IFRS).

The balance of account 97 “Deferred expenses” is reflected in the balance sheet asset (clause 20 of PBU 4/99). However, until 2011, not all amounts recorded in this account met the conditions for recognition of assets. In a number of cases, organizations kept expenses in this account that were in no way related to the receipt of income over several reporting periods or had such an indirect connection with them that the accounting principle of prudence, that is, readiness to recognize expenses, was violated.

Such free use of the active account was allowed by the provisions of the previously valid version of clause 65 “Regulations on accounting and financial reporting”, which has now undergone changes: “65. Costs incurred by the organization in the reporting period, but related to the following reporting periods, are reflected in the balance sheet as a separate item as deferred expenses and are subject to write-off in the manner established by the organization (uniformly, in proportion to the volume of production, etc.) during the period to which they relate."

This order led to the fact that in account 97 the amounts were accumulated unsystematically; it was quite difficult to group and classify them even for the accountants themselves. This caused, for example, such negative consequences for users of reporting and the organization itself, such as:

- artificially inflating the amount of the balance sheet asset, as well as the net assets (the difference between the value of assets and the amount of liabilities) of the organization;

- the possibility of concealing actual losses or overstating the organization’s profit by attributing current expenses to expenses of future periods (delay in recognizing expenses);

- violation of the principle of rational accounting, when, formally following previously existing norms, the organization attributed to account 97 and distributed over several reporting periods amounts that did not have a significant impact on the results of financial and economic activities.

As a consequence of all this, there followed a distortion of information about the actual state of affairs. This is a gross violation of one of the main tasks of accounting and preparation of financial statements - the formation of complete and reliable information about the activities and property status of the organization (Article 1 of Federal Law No. 129-FZ of November 21, 1996).

In addition, we should not forget about the planned transition to IFRS standards. The presence of account 97 complicated this transition, since international standards do not contain such a thing as deferred expenses. Since each amount from account 97 required identification and reclassification for IFRS purposes, the transition process became labor-intensive.

Conclusion : Changes in Russian legislation in accounting for deferred expenses are aimed at eliminating possible distortions in financial statements and improving accounting.

Question: Does the organization have the right to continue to use account 97 “Deferred expenses” after the changes made to clause 65 “Regulations on accounting and financial reporting”?

Answer : It has the right to apply. The use of account 97 is not prohibited or abolished by law.

A literal interpretation of clause 65 “Regulations on accounting and financial reporting” in the new edition of Order of the Ministry of Finance of Russia No. 186n dated December 24, 2010 allows us to conclude that the use of this account in accounting is not suspended. This rule establishes a general “reference” rule for accounting for expenses related to the following reporting periods - such expenses must be taken into account in accordance with the documents governing the conditions for recognition, accounting and write-off of certain assets of the organization.

"65. Costs incurred by the organization in the reporting period, but relating to the following reporting periods, are reflected in the balance sheet in accordance with the conditions for recognition of assets established by regulatory legal acts on accounting, and are subject to write-off in the manner established for writing off the value of assets of this type.”

The formation of deferred expenses is currently still provided for, in particular, by the following accounting regulations:

- Chart of Accounts and Instructions for its Application (approved by Order of the Ministry of Finance of Russia No. 94n dated October 31, 2000);

- PBU 14/2007 “Accounting for intangible assets” (when reflecting license payments for the right to use intellectual property);

- PBU 2/2008 “Accounting for construction contracts” (when reflecting upcoming expenses under a construction contract);

- PBU 4/99 “Accounting statements of an organization” (when creating a balance sheet);

- Methodological instructions (approved by Order of the Ministry of Finance of Russia No. 119n dated December 28, 2001 (when reflecting expenses in the form of the cost of materials related to preparatory work)).

In the current situation, the Russian Ministry of Finance does not deny that, for example, one-time fixed payments under license agreements are deferred expenses (letter No. 07-02-06/64 dated April 26, 2011).

In addition, clause 19 of PBU 10/99 continues to be in effect, which, also through a reference norm, allows accountants to reasonably distribute expenses between several reporting periods.

"19. Expenses are recognized in the income statement: ... by reasonably allocating them between reporting periods when expenses result in the receipt of income over several reporting periods and when the relationship between income and expenses cannot be clearly determined or is determined indirectly; ..."

Conclusion : It is advisable to use account 97 “Deferred expenses” if there are reasons for this.

Question: What conditions must be met to recognize costs as deferred expenses?

Answer: Deferred expenses are recognized as expenses of an organization that:

- relate to several reporting periods;

- meet the conditions for recognizing any type of asset.

Confirmation: clause 65 “Regulations on accounting and financial reporting”.

One of the main conditions for recognizing any kind of asset in accounting is the ability to generate economic benefits (income) in the future. Therefore, only expenses that cause the receipt of income over several reporting periods should be recognized as deferred expenses (clause 7.2 of the “Accounting Concept in the Market Economy of Russia” (approved by the Methodological Council on Accounting under the Ministry of Finance of Russia on December 29, 1997), clause 19 of PBU 10 /99 “Organization expenses”).

For example, when obtaining the rights to use a computer program under a written license agreement, which are reflected in deferred expenses in accordance with clause 39 of PBU 14/2007 “Accounting for intangible assets,” an intangible asset arises, received for use for a period specified by the agreement or civil law .

Controversial point: the list of deferred expenses is closed or open (see below the question “Does an organization, at its discretion, have the right to recognize expenses as deferred expenses?”).

Question: How to take into account expenses that relate to several reporting periods, but do not meet the conditions for recognizing them as expenses of future periods?

Answer : You need to take into account the following:

- current expenses of the organization (for example, expenses for payment of vacation pay for upcoming and transferable vacations) - if all the conditions for recognizing them as such are met;

- accounts receivable (for example, one-time payments under insurance contracts) - in case of transfer of advances;

- assets of the organization (for example, expenses for the acquisition of fixed assets) - in the event of expenses that form the value of the organization’s property.

Confirmation: clause 65 “Regulations on accounting and financial reporting”.

Question: Does an organization have the right to recognize costs as deferred expenses at its discretion?

Answer : A single point of view on this issue has not been developed.

Opinion one: starting from 2011, the list of deferred expenses is closed. Costs can be attributed to account 97 only in cases directly named in accounting regulations:

- when reflecting license payments for the right to use intellectual property (clause 39 of PBU 14/2007 “Accounting for intangible assets”);

- when reflecting upcoming expenses under a construction contract (clause 16 of PBU 2/2008 “Accounting for construction contracts”);

- when reflecting expenses in the form of the cost of materials related to preparatory work (clause 94 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia No. 119n dated December 28, 2001).

Second opinion: the list of deferred expenses is open. However, in order to recognize expenses as such, it is necessary that all the necessary conditions for this are met (belonging to several reporting periods, compliance with the conditions for recognizing any type of asset).

For example, expenses associated with the maintenance of fixed assets can be recognized as deferred expenses if:

- their amounts exceed the limit on the value of fixed assets established by the organization for accounting purposes;

- The frequency of maintenance is more than a year, that is, its results are used for more than 12 months).

In this situation, all conditions for recognizing such expenses as a fixed asset are met (clause 4 of PBU 6/01). However, they cannot be recognized as such, since they do not have a physical form, that is, they are not an inventory item (clause 6 of PBU 6/01). At the same time, all criteria for their inclusion in deferred expenses have been met. A similar approach can be applied to the costs of modernizing intangible assets. This opinion is also expressed by employees of the Russian Ministry of Finance in unofficial comments.

Optimal option: the principle of prudence in accounting policies suggests that the organization should be more willing to recognize expenses in accounting (clause PBU 1/2008 “Accounting Policies of the Organization”). Meanwhile, we must not forget that the condition on the correspondence of ongoing expenses and income - as the economic essence of any business transaction, is also contained in tax accounting (clause 1 of Article 272 of the Tax Code of the Russian Federation). Therefore, until appropriate changes are made, for example, to PBU 10/99 and PBU 18/02, organizations have the right to continue to use account 97 to reflect assets that reasonably qualify for recognition as deferred expenses. Otherwise (with a complete refusal to distribute the relevant expenses between several reporting periods), this can lead to the emergence of a huge number of differences according to PBU 18/02, the labor costs for their reflection in accounting will definitely violate the principle of rationality of its maintenance.

Question: On which line of the balance sheet should deferred expenses be reflected?

Answer : You can reflect:

- as part of line 1170 “Other non-current assets”, if the formation of deferred expenses is associated with assets reflected in section I of the balance sheet (for example, this is how you need to reflect the amounts of fixed one-time payments under written license agreements if the period of use of these rights exceeds 12 months);

- as part of line 1210 “Inventories” or line 1260 “Other current assets” - if the formation of deferred expenses is associated with assets reflected in section II of the balance sheet (for example, expenses for the purchase of materials used for preparatory work in seasonal production).

Confirmation: clauses 19, 20 PBU 4/99.

In this case, the organization has the right to enter additional lines into the balance sheet and otherwise detail the reflection of this information in the reporting (clauses 6, 11 PBU 4/99, clause 3 of Order of the Ministry of Finance of Russia No. 66n dated July 2, 2010).

Question: Should a one-time payment be recognized as deferred expenses (accounted for in account 97) under insurance contracts concluded for more than one reporting period?

Answer : There is no need to recognize and account for account 97.

Insurance of various risks is for the insured organization the acquisition of a service, which consists in the insurer’s willingness to compensate for losses in connection with the occurrence of an insured event (Chapter 48 of the Civil Code of the Russian Federation).

Such readiness is ongoing and limited to the insurance period. In the event of early termination of the contract (under certain conditions), the insurance company must return part of the insurance payments proportional to the remaining term of the contract (clause 1 of Article 958 of the Civil Code of the Russian Federation). Therefore, by paying for the entire insurance period in advance, the organization makes an advance payment (gives an advance to the insurer).

Prepayment (advance payment) is not recognized as an expense of the organization (clause 3 of PBU 10/99). Therefore, accounts receivable must be recorded in accounting. Costs appear gradually as the insurance contract expires.

In international accounting practice, including when preparing reports in accordance with IFRS, insurance payment is also reflected as an advance payment.

A similar point of view is expressed by many accounting specialists, including such a union of professional accountants as the Committee on Interpretations.

Conclusion : The amounts paid by the organization under the insurance contract are not deferred expenses of the organization.

Question: Recognize as deferred expenses (account on account 97) the payment of vacation pay for vacations starting in one month and ending in another month (reporting period)?

Answer : There is no need to recognize and account for account 97.

Since 2011, all organizations (with the exception of small enterprises that are not issuers of publicly offered securities) are required to create a reserve for upcoming vacation payments without fail, since such obligations of the organization are estimated (clauses 4, 5 of PBU 8/2010 “Estimated obligations, contingent liabilities and contingent assets").

Contributions to the reserve are made evenly and are recognized as current expenses of the organization (clause 8 of PBU 8/2010).

Vacation pay amounts are paid from the created reserve. Consequently, the organization does not need to re-evenly distribute paid vacation pay (including by assigning it to account 97 “Future expenses”).

In addition, the cost of paying vacation pay does not meet the conditions for recognizing any type of asset of the organization.

Therefore, even small, including micro-enterprises that do not create a reserve for upcoming vacation pay, the cost of paying vacation pay should be attributed immediately to the organization’s current expenses (clause 65 “Regulations on accounting and financial reporting”, clause 8 PBU 10/99 "Organization expenses").

Conclusion : Vacation pay amounts are not deferred expenses of the organization.

Question: Recognize as deferred expenses (account on account 97) such types of expenses as interest (discount) accrued on a bill by the issuing organization (on a bond by the issuing organization), additional borrowing costs (for example, costs for information consulting services, costs for examination of contracts)? The accounting policy of the organization provides for their equal write-off as expenses during the period for repayment of borrowed funds provided for in the bill (bond, loan agreement). The borrowed funds received are not related to the acquisition (creation) of an investment asset.

Answer : There is no need to recognize them as deferred expenses and record them on account 97.

Deferred expenses are recognized as expenses of the organization that:

- relate to several reporting periods;

- meet the conditions for recognizing any type of asset (for example, fixed assets, intangible assets).

Confirmation: clause 65 “Regulations on accounting and financial reporting”.

At the choice of the bill issuer (bond issuer, borrower), interest (discount) accrued on the bill (issued bond) issued by it, or additional loan costs are reflected in the accounts:

- as part of other expenses in those reporting periods to which these accruals relate;

- evenly during the period for payment of the received funds stipulated by the bill (bond, loan agreement).

Confirmation: para. 2 clause 8, para. 2 clause 15, para. 2 clause 16 PBU 15/2008 “Accounting for expenses on loans and credits”.

Thus, when choosing the second accounting method, these expenses comply with the first condition for recognizing expenses as deferred expenses - they relate to several reporting periods.

However, they are the organization's accounts payable. They do not correspond to any type of assets, since they do not contain characteristics and do not meet the conditions for their recognition. They, as opposed to assets, are liabilities of the organization.

Confirmation: para. 1 clause 15, para. 1 clause 16 PBU 15/2008.

Conclusion : Since the second condition for recognizing costs as deferred expenses is not met, interest (discount) accrued on the bill by the organization-issuer of the bill (bonds by the issuer organization) does not need to be taken into account on account 97.

Question: What are the reasons for the changes in accounting for deferred expenses?

Answer: Associated with the following changes:

- a new edition of clause 65 “Regulations on accounting and financial reporting” (as amended by Order of the Ministry of Finance of Russia No. 186n dated December 24, 2010), from which the concept of “deferred expenses” is excluded;

- exclusion from the new form of the balance sheet (approved by Order of the Ministry of Finance of Russia No. 66n dated July 2, 2010) of a direct mention of the line “Deferred expenses”.

Conclusion: Changes in the procedure for applying account 97 are associated with amendments to a number of regulatory documents on accounting.

Question: For what reason were changes made to the accounting of deferred expenses and their reflection in the financial statements?

Answer: Introduced with the aim of streamlining accounting, systematizing reflected data and bringing it closer to international financial reporting standards (IFRS).

The balance of account 97 “Deferred expenses” is reflected in the balance sheet asset (clause 20 of PBU 4/99). However, until 2011, not all amounts recorded in this account met the conditions for recognition of assets. In a number of cases, organizations kept expenses in this account that were in no way related to the receipt of income over several reporting periods or had such an indirect connection with them that the accounting principle of prudence, that is, readiness to recognize expenses, was violated.

Such free use of the active account was allowed by the provisions of the previously valid version of clause 65 “Regulations on accounting and financial reporting”, which has now undergone changes: “65. Costs incurred by the organization in the reporting period, but related to the following reporting periods, are reflected in the balance sheet as a separate item as deferred expenses and are subject to write-off in the manner established by the organization (uniformly, in proportion to the volume of production, etc.) during the period to which they relate."

This order led to the fact that in account 97 the amounts were accumulated unsystematically; it was quite difficult to group and classify them even for the accountants themselves. This caused, for example, such negative consequences for users of reporting and the organization itself, such as:

- artificially inflating the amount of the balance sheet asset, as well as the net assets (the difference between the value of assets and the amount of liabilities) of the organization;

- the possibility of concealing actual losses or overstating the organization’s profit by attributing current expenses to expenses of future periods (delay in recognizing expenses);

- violation of the principle of rational accounting, when, formally following previously existing norms, the organization attributed to account 97 and distributed over several reporting periods amounts that did not have a significant impact on the results of financial and economic activities.

As a consequence of all this, there followed a distortion of information about the actual state of affairs. This is a gross violation of one of the main tasks of accounting and preparation of financial statements - the formation of complete and reliable information about the activities and property status of the organization (Article 1 of Federal Law No. 129-FZ of November 21, 1996).

In addition, we should not forget about the planned transition to IFRS standards. The presence of account 97 complicated this transition, since international standards do not contain such a thing as deferred expenses. Since each amount from account 97 required identification and reclassification for IFRS purposes, the transition process became labor-intensive.

Conclusion: Changes in Russian legislation in accounting for deferred expenses are aimed at eliminating possible distortions in financial statements and improving accounting.

Question: Does the organization have the right to continue to use account 97 “Deferred expenses” after the changes made to clause 65 “Regulations on accounting and financial reporting”?

Answer: It has the right to apply. The use of account 97 is not prohibited or abolished by law.

A literal interpretation of clause 65 “Regulations on accounting and financial reporting” in the new edition of Order of the Ministry of Finance of Russia No. 186n dated December 24, 2010 allows us to conclude that the use of this account in accounting is not suspended. This rule establishes a general “reference” rule for accounting for expenses related to the following reporting periods - such expenses must be taken into account in accordance with the documents governing the conditions for recognition, accounting and write-off of certain assets of the organization.

"65. Costs incurred by the organization in the reporting period, but relating to the following reporting periods, are reflected in the balance sheet in accordance with the conditions for recognition of assets established by regulatory legal acts on accounting, and are subject to write-off in the manner established for writing off the value of assets of this type.”

The formation of deferred expenses is currently still provided for, in particular, by the following accounting regulations:

- Chart of Accounts and Instructions for its Application (approved by Order of the Ministry of Finance of Russia No. 94n dated October 31, 2000);

- PBU 14/2007 “Accounting for intangible assets” (when reflecting license payments for the right to use intellectual property);

- PBU 2/2008 “Accounting for construction contracts” (when reflecting upcoming expenses under a construction contract);

- PBU 4/99 “Accounting statements of an organization” (when creating a balance sheet);

- Methodological instructions (approved by Order of the Ministry of Finance of Russia No. 119n dated December 28, 2001 (when reflecting expenses in the form of the cost of materials related to preparatory work)).

In the current situation, the Russian Ministry of Finance does not deny that, for example, one-time fixed payments under license agreements are deferred expenses (letter No. 07-02-06/64 dated April 26, 2011).

In addition, clause 19 of PBU 10/99 continues to be in effect, which, also through a reference norm, allows accountants to reasonably distribute expenses between several reporting periods.

"19. Expenses are recognized in the income statement: ... by reasonably allocating them between reporting periods when expenses result in the receipt of income over several reporting periods and when the relationship between income and expenses cannot be clearly determined or is determined indirectly; ..."

Conclusion: It is advisable to use account 97 “Deferred expenses” if there are grounds for this.

Question: What conditions must be met to recognize costs as deferred expenses?

Deferred expenses are recognized as expenses of the organization that:

- relate to several reporting periods;

- meet the conditions for recognizing any type of asset.

Confirmation: clause 65 “Regulations on accounting and financial reporting”.

One of the main conditions for recognizing any kind of asset in accounting is the ability to generate economic benefits (income) in the future. Therefore, only expenses that cause the receipt of income over several reporting periods should be recognized as deferred expenses (clause 7.2 of the “Accounting Concept in the Market Economy of Russia” (approved by the Methodological Council on Accounting under the Ministry of Finance of Russia on December 29, 1997), clause 19 of PBU 10 /99 “Organization expenses”).

For example, when obtaining the rights to use a computer program under a written license agreement, which are reflected in deferred expenses in accordance with clause 39 of PBU 14/2007 “Accounting for intangible assets,” an intangible asset arises, received for use for a period specified by the agreement or civil law .

Controversial point: the list of deferred expenses is closed or open (see below the question “Does an organization, at its discretion, have the right to recognize expenses as deferred expenses?”).

Question: How to take into account expenses that relate to several reporting periods, but do not meet the conditions for recognizing them as expenses of future periods?

Answer: You need to take into account the following:

- current expenses of the organization (for example, expenses for payment of vacation pay for upcoming and transferable vacations) - if all the conditions for recognizing them as such are met;

- accounts receivable (for example, one-time payments under insurance contracts) - in case of transfer of advances;

- assets of the organization (for example, expenses for the acquisition of fixed assets) - in the event of expenses that form the value of the organization’s property.

Confirmation: clause 65 “Regulations on accounting and financial reporting”.

Question: Does an organization have the right to recognize costs as deferred expenses at its discretion?

Answer: A single point of view on this issue has not been developed.

Opinion one: starting from 2011, the list of deferred expenses is closed. Costs can be attributed to account 97 only in cases directly named in accounting regulations:

- when reflecting license payments for the right to use intellectual property (clause 39 of PBU 14/2007 “Accounting for intangible assets”);

- when reflecting upcoming expenses under a construction contract (clause 16 of PBU 2/2008 “Accounting for construction contracts”);

- when reflecting expenses in the form of the cost of materials related to preparatory work (clause 94 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia No. 119n dated December 28, 2001).

Second opinion: the list of deferred expenses is open. However, in order to recognize expenses as such, it is necessary that all the necessary conditions for this are met (belonging to several reporting periods, compliance with the conditions for recognizing any type of asset).

For example, expenses associated with the maintenance of fixed assets can be recognized as deferred expenses if:

- their amounts exceed the limit on the value of fixed assets established by the organization for accounting purposes;

- The frequency of maintenance is more than a year, that is, its results are used for more than 12 months).

In this situation, all conditions for recognizing such expenses as a fixed asset are met (clause 4 of PBU 6/01). However, they cannot be recognized as such, since they do not have a physical form, that is, they are not an inventory item (clause 6 of PBU 6/01). At the same time, all criteria for their inclusion in deferred expenses have been met. A similar approach can be applied to the costs of modernizing intangible assets. This opinion is also expressed by employees of the Russian Ministry of Finance in unofficial comments.

Optimal option: the principle of prudence in accounting policies suggests that the organization should be more willing to recognize expenses in accounting (clause PBU 1/2008 “Accounting Policies of the Organization”). Meanwhile, we must not forget that the condition on the correspondence of ongoing expenses and income - as the economic essence of any business transaction, is also contained in tax accounting (clause 1 of Article 272 of the Tax Code of the Russian Federation). Therefore, until appropriate changes are made, for example, to PBU 10/99 and PBU 18/02, organizations have the right to continue to use account 97 to reflect assets that reasonably qualify for recognition as deferred expenses. Otherwise (with a complete refusal to distribute the relevant expenses between several reporting periods), this can lead to the emergence of a huge number of differences according to PBU 18/02, the labor costs for their reflection in accounting will definitely violate the principle of rationality of its maintenance.

Question: On which line of the balance sheet should deferred expenses be reflected?

Answer: You can reflect:

- as part of line 1170 “Other non-current assets”, if the formation of deferred expenses is associated with assets reflected in section I of the balance sheet (for example, this is how you need to reflect the amounts of fixed one-time payments under written license agreements if the period of use of these rights exceeds 12 months);

- as part of line 1210 “Inventories” or line 1260 “Other current assets” - if the formation of deferred expenses is associated with assets reflected in section II of the balance sheet (for example, expenses for the purchase of materials used for preparatory work in seasonal production).

Confirmation: clauses 19, 20 PBU 4/99.

In this case, the organization has the right to enter additional lines into the balance sheet and otherwise detail the reflection of this information in the reporting (clauses 6, 11 PBU 4/99, clause 3 of Order of the Ministry of Finance of Russia No. 66n dated July 2, 2010).

Question: Should a one-time payment be recognized as deferred expenses (accounted for in account 97) under insurance contracts concluded for more than one reporting period?

Answer: There is no need to recognize and account for account 97.

Insurance of various risks is for the insured organization the acquisition of a service, which consists in the insurer’s willingness to compensate for losses in connection with the occurrence of an insured event (Chapter 48 of the Civil Code of the Russian Federation).

Such readiness is ongoing and limited to the insurance period. In the event of early termination of the contract (under certain conditions), the insurance company must return part of the insurance payments proportional to the remaining term of the contract (clause 1 of Article 958 of the Civil Code of the Russian Federation). Therefore, by paying for the entire insurance period in advance, the organization makes an advance payment (gives an advance to the insurer).

Prepayment (advance payment) is not recognized as an expense of the organization (clause 3 of PBU 10/99). Therefore, accounts receivable must be recorded in accounting. Costs appear gradually as the insurance contract expires.

In international accounting practice, including when preparing reports in accordance with IFRS, insurance payment is also reflected as an advance payment.

A similar point of view is expressed by many accounting specialists, including such a union of professional accountants as the Committee on Interpretations.

Conclusion: The amounts paid by the organization under the insurance contract are not deferred expenses of the organization.

Question: Recognize as deferred expenses (account in account 97) the payment of vacation pay for the vacation that begins

ready to advise you on any issue (registration of an LLC, legal services). Contact us by phone: 8 (831) 437-16-78.

Concession of specialists

In some cases, in the current market conditions, such operations are becoming very popular. One enterprise, breaking the employment contract with a specialist, allows him to get a job in another company. The latter, in turn, compensates for this loss. Operations of this type are widespread in the field of sports. However, nowadays, such transactions are increasingly being concluded in other areas of economic life. The enterprise that cedes the specialist makes the following entry: Db 51 Kd 91.1.

The buyer's wiring is as follows: Db 97 Kd 51.

Then, during the contract period, the following entry will be made monthly: Db 91.2 Kd 97.

But in this case, the company will have to pay property tax.

Postings to display profits and losses on account 99

In general, the accounting entry for making a profit or incurring losses in account 99 is as follows:

- Dt99 – Kt84 – retained earnings are taken into account;

- Dt84 – Kt99 – transfer of the amount of net loss;

- Dt99 – Dt90 – write-off of losses for the leading type of activity;

- Dt90 – Kt99 – reflection of profit for the leading type of activity;

- Dt99 – Kt91 – display of losses from other types of activities;

- Dt91 – Kt99 – receipt of income from other types of activities;

- Dt96 – Kt99 – increase in profit due to the balance of unused reserves;

- Dt99 – Kt10 – write-off of the cost of materials damaged as a result of emergency situations;

- Dt73 – Kt99 – recovery of expenses incurred from those responsible in emergency circumstances;

- Dt99 – Kt68 – calculation of income tax.

Profits and losses from emergency circumstances and situations include cash flows due to fire, flood, nationalization of an enterprise, natural disasters, receipt of insurance compensation, etc.

Economic activities of the company in the absence of sales

Often, at the beginning of its activities, a company suffers losses. At the same time, the company’s work is unfolding and is in full swing, but during the reporting period the company did not manage to do anything or managed to do it, but was unable to implement it. In such a situation, everything that was recorded throughout the year in items for main and auxiliary production, general and general production expenses, and maintenance costs must be credited. All costs that are collected should be charged to account 97 (debit). As the sale of manufactured products progresses, costs will be written off from this item in DB account. 90.2.

Postings for the distribution of net profit at the end of the year (account 84)

| Debit | Credit | Operation |

| D84 | K82 | formation of reserve capital from net profit. |

| D84 | K84 | repayment of losses from previous years is reflected. |

| D84 | K75 (70) | dividends payable have been accrued. |

Uncovered loss for the year can be covered as follows: (click to expand)

- Due to the additional capital formed on account 83;

- Due to the reserve capital formed on account 82;

- Due to additional contributions from company participants.

Score 97: closing

The above option can be considered theoretically correct. But in practice, the question arises about whether there will actually be production and sales subsequently. Currently, there are a huge number of companies operating that make expenses every day, and expect income “someday”. This situation creates a difficult situation. Where to write off the debit turnover that records account 97?

There is little choice here, and expenses that are unlikely to pay off in the future will have to be written off in DB account. 99. But in this situation, it is logical to assume that these costs can be immediately transferred to article 99. The accountant, therefore, will resolve that controversial situation solely on the basis of his professional judgment. He will decide whether to immediately write off the account. 99 and reflect expenses for that period or show expenses according to Db account. 97 and then transfer them as shown above, if sales and production still take place. The specialist can write them off as losses for those upcoming periods to which, due to the lack of activity, they are not related. It is advisable to reflect the chosen option in the accounting policy of the enterprise.

Postings to cover losses for the year

| Debit | Credit | Operation |

| D83 | K84 | coverage of losses using additional capital funds is reflected. |

| D82 | K84 | coverage of losses from reserve capital is reflected. |

| D75 | K84 | coverage of losses through additional contributions of the founders is reflected. |

In order to reflect profit/loss at the end of the year in accounting, together with account 84, use Account 99 - profits and losses, Account 91 - other income and expenses, Account 90 - sales.

Profit can be directed to reserve capital - Account 82, loss is covered from additional capital - Account 83.

Taxes

The issues of taxation of costs considered to be deferred expenses are quite complex and uncertain. In accordance with paragraph 1 of Art. 272 of the Tax Code, costs are accepted in the period to which they actually relate. In this case, the time of actual payment of funds or other payment does not matter. The date of recognition of expenses for accepted services and work of a production nature is the day the payer signs the corresponding acceptance certificate.

However, one should take into account the legal requirement for the need to compare expenses and income that will lead or led to this profit. Costs are recognized in the tax (reporting) period in which they arise in accordance with the terms of the transaction (under agreements with specific deadlines for fulfilling obligations) and the principle of proportional and uniform formation of income and expense items (under agreements that last more than one tax period), in accordance with the provisions of the current Tax Code (in paragraph 1 of Article 272).

It follows from this that many costs, which, according to accounting rules, are transferred to the costs of future years, must be included in the tax base. This must be done during the reporting period in which they actually occurred. However, experts say that in each specific situation it is necessary to analyze and evaluate the possibility of comparability of expenses incurred and income received.

Disposal of retained earnings from previous years

The profit received by the company can be distributed exclusively by order of the owners of the company. This norm is provided for by the laws “On Limited Liability Companies” dated 02/08/1998 No. 14-FZ and “On Joint-Stock Companies” dated 12/26/1995 No. 208-FZ.

But there are also certain distribution frameworks that establish that when an NP is formed at the end of the year, the company is allowed to use it for the following purposes:

- issuance of dividends;

- repayment of previously incurred losses;

- to account 84 to accumulate profits for the purpose of its further use;

- formation of reserve capital;

- increase the authorized capital;

- other purposes established by laws No. 14-FZ and No. 208-FZ.

For example, the company's management has the right to reward employees from distributed profits. Find out how to correctly account for such payments in the material from ConsultantPlus. If you do not have access to the K+ system, get a trial online access for free.

The direction of NP for the above purposes is accompanied by the corresponding entries in accounting:

| This year's NP is aimed at: | Dt | CT |

| For accrual of dividends | 84 | 75 |

| Formation of reserve capital | 84 | 82 |

| Increase the authorized capital | 84 | 80 |

In circumstances where the company decides to use retained earnings in account 84 to compensate for losses from previous years, it is necessary to make a posting between internal subaccounts. In other words, do internal wiring.

When a company receives a loss at the end of the year, it is allowed to repay it from the following resources:

- reserve capital;

- NP of previous years;

- authorized capital (after changes in the charter);

- target funds belonging to the founders.

In this case, the following wiring is required:

| If the loss is covered by: | Dt | CT |

| Reserve capital | 82 | 84 |

| Founders' target funds | 75 | 84 |

| Authorized capital | 80 | 84 |

In addition, the company has the opportunity to significantly reduce the loss incurred in the current period due to retained earnings from previous years. In a company that decides to do this, the accountant will make an internal entry to account 84.