Individual entrepreneurs are required to pay insurance premiums “for themselves.” Even if there is no income, contributions must still be paid, but there are exceptions. And if you hire employees, you need to pay contributions both for yourself and for the employees.

Insurance premiums “for yourself” Basic concepts about contributions Amount of contributions in 2021, 2022 and 2023 Income for calculating 1% of excess Grace periods Payment of insurance premiums If an individual entrepreneur works for less than a full year Voluntary insurance Self-reporting If an individual entrepreneur is an Employer

Contribution rates Benefits on contributions Do I need to register with the funds Who can save If benefits were paid Payment of contributions for employees If they did not pay on time Reporting for employees Fines

Bonus in the form of tax reduction

What details are used for paying insurance premiums for individual entrepreneurs in 2021?

For entrepreneurs, insurance premiums for themselves are mandatory payments. They are paid both in the presence and absence of employees. If an individual entrepreneur fails to make a payment on time for various reasons, he will have to pay additional sanctions and fines, and he will also have problems with the Federal Tax Service.

Attention! The requirement to pay contributions for yourself is given in the provisions of Art. 430 NK.

Previously, the process of transferring money was carried out only through the Pension Fund, but now the money is deposited into the Federal Tax Service. From 2021, significant changes have been made for businessmen. Previously, to calculate contributions, the minimum wage established by each region was taken into account. Now there is a fixed payment for yourself, and it is also possible to submit a receipt in electronic form.

The fixed contribution is paid only for the entrepreneur himself, and for hired workers it is calculated individually.

In 2021, 3 types of contributions have been established for businessmen:

- Fixed payment for yourself. With the help of these contributions, the citizen’s future pension is formed. In 2021, this payment is 40,874 rubles. Of this amount, 32,448 rubles. is transferred to compulsory pension insurance, and 8,426 rubles. is sent to health insurance. If the annual income is more than 300 thousand rubles, then you will have to pay an additional 1% on the excess, so the exact amount is calculated individually by each entrepreneur. But the total payment cannot exceed 8 * 32448 rubles.

- Contributions for employees. The amount of the fee depends on the citizen’s income, and not only the salary is taken into account, but also additional amounts received from the employer. They can be in the form of bonuses, incentive payments or allowances. 22% of total income is deducted. If a citizen receives more than 1.292 million rubles in a year, then the businessman pays 10% on the excess amount.

- Contributions to compulsory medical insurance. The payment is 8426 rubles. in a year.

All payments are transferred not to the Pension Fund, but to the Federal Tax Service, and during this process the correct details are indicated based on the pre-established BCC.

BCCs change regularly, so before making a payment it is recommended to check this information with Federal Tax Service employees, and you can also use the tax service website.

The current data is on the Federal Tax Service website , for which you select the “IP” section. Income classification codes are selected from the list of sections. Next, insurance premiums are selected, which allows you to open a section with details.

If the entrepreneur enters the details incorrectly, this will lead to late payment and the accrual of penalties.

Income tax for employees

The state collects personal income tax from the salary of each employee. As a result, the person receives the money minus this payment. The tax rate is 13%. Personal income tax is withheld from the last part of the monthly salary.

Example of personal income tax calculation

The individual entrepreneur has a manager with a salary of 30,000 rubles. According to the agreement, the advance is paid on the 5th, and the second part of the salary is paid on the 25th. At the end of the month, the employee was awarded a bonus in the amount of 6,000 rubles.

The employer must transfer to the manager on the 5th the first part of the salary - 15,000 rubles, and on the 25th the rest minus income tax: (15,000 + 6,000) - 13% × (30,000 + 6,000) = 16,320 rubles.

The employer will need to transfer 4,680 rubles to the personal income tax account to the tax account on the day the employee is paid or the next day.

Rules for creating a calculation form for insurance premiums

Until December 31, entrepreneurs can pay the fee at any time. If you need to generate a receipt, this can be done remotely on the Federal Tax Service website.

Important! Businessmen can make the entire payment at once or distribute it over months, transferring funds in parts.

If the entrepreneur’s income for the year exceeds 300 thousand rubles, then contributions from the excess are made after December 31 of the current year.

Businessmen prefer to use the Federal Tax Service website to generate receipts for the following reasons:

- even when using online banking or mobile banking, it is not possible to use a ready-made payment system;

- at bank cash desks or at the post office you can pay contributions using a receipt, but you won’t be able to do it, so you will have to make a payment order yourself;

- On the tax office website you can not only make a payment form, but also get up-to-date information.

To generate a receipt, the following rules are taken into account:

- Initially, you need to register on the Federal Tax Service website;

- personal information about the taxpayer is filled out in the personal account;

- on the main page, select the “Payment of taxes and insurance premiums” section;

- a form opens in which some information is entered automatically;

- click the “fill out payment document” button, which is located at the bottom of the page;

- select the type of contribution and type of payment;

- the period for which the receipt is generated is indicated;

- the details of the recipient of the money are entered;

- the details of the entrepreneur are entered, and in the “Address” line the place of registration is indicated, and not the address of the place of work;

- when selecting the Federal Tax Service branch where the citizen is registered, the line “Federal Tax Service Code” is automatically filled in.

After completing these steps, a receipt appears, which can be paid on the website or printed, after which it is handed over to bank or post office employees. It is advisable to carry out a check to ensure that the entered data is correct.

It is also useful to read: Application for refund of overpaid insurance premiums

Employer Responsibilities

To register as an employee, an entrepreneur needs:

- Conclude an employment contract, according to which you pay wages at least twice a month. The amount of remuneration must correspond to the established minimum wage.

- Register with the Social Insurance Fund as an employer - come with documents no later than 30 days after signing the first employment contract. The pension fund will receive information about the employer automatically.

- Transfer tax from an employee’s salary and make contributions to the following types of insurance: pension, medical, temporary disability, industrial accidents.

After payments are made on time, the entrepreneur must submit the relevant reports.

Nuances of filling out a receipt

The site has a special menu with tips, so if you follow them exactly, there will be no difficulties in creating the form. To fill it out, the data available in your personal account is used, and you also have to enter information from the taxpayer’s personal documentation.

During the process, the following nuances are taken into account:

- in the taxpayer status of individual entrepreneurs, enter code 09;

- the payment basis is the TP code if there are no fines or penalties;

- When choosing a tax period, indicate “annual payment”.

If erroneous information is entered, this may cause late payment, which leads to the accrual of fines.

Reports for your employees

In addition to timely payment of all contributions, the entrepreneur is obliged to submit reports on this:

| Report | Due dates |

| 6-NDFL to the Federal Tax Service | annually until April 30, July 31, October 31 and general annual report until March 1 |

| 2-NDFL to the Federal Tax Service | annually until March 2 |

| 4-FSS to FSS | until the 20th of April, July, October and January |

| on insurance premiums to the Federal Tax Service | until the 30th in April, July, October and January |

| data on the average number of employees in the Federal Tax Service | annually until January 20 |

An entrepreneur is required to submit all of the listed reports, even if he has 1 employee.

How is the receipt paid?

As soon as the payment slip is generated, it can be immediately printed or saved electronically. Using paper documentation, you can deposit funds at bank or post office branches.

It is possible to use a remote payment method, but it is available only to entrepreneurs who have previously opened a “Bank-Client” system in an accessible system. Bank cards or electronic services are used for payment .

For non-cash payment, you need to indicate the businessman’s TIN in your personal account on the Federal Tax Service website. After depositing funds, the taxpayer receives a special confirmation of payment, which can be easily saved on a computer or other device, and can also be printed.

Employees on other terms

In some cases, it is more convenient and cheaper for individual entrepreneurs to use the work of specialists without hiring staff. More information about such situations:

An individual under a civil contract. The employer will have to calculate and pay almost the same amount to the budget as for a regular employee. It is necessary to list personal income tax, medical and pension insurance.

Individual entrepreneur or self-employed. This specialist is obliged to pay taxes for himself; he will only need to pay remuneration for the work according to the contract.

The second option is clearly more profitable for the individual entrepreneur. But he threatens with large fines and additional assessments of unpaid taxes from regulatory authorities.

Rules for document execution

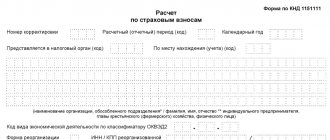

It is required to use a new form with a separate designation - KND 1151111. The form is filled out for all employees. The document contains the following types of information:

- Personal data for all persons who were insured. We need the addresses where they live and are registered, TIN.

- Information regarding who acts as the payer of insurance premiums. This type of payment is considered separately.

- Description of the same obligations, only for peasant farms.

- Description of an individual who does not have the status of an individual entrepreneur. It must be contributed by everyone who operates in the current market.

Attention! The paper version of registration and submission is chosen in most cases.

How is the pension calculated?

Payment of annual insurance premiums is the basis for calculating pensions for entrepreneurs (individual entrepreneurs without employees) on a general basis, i.e. upon reaching retirement age and having insurance coverage. Currently, age and length of service increase annually until they reach the maximum values provided for by law.

Since individual entrepreneurs annually pay a minimum fixed contribution, they are usually accrued a pension at the subsistence level.

Can an individual entrepreneur work without employees?

The economic activities of an individual entrepreneur are carried out by him practically on the same regulatory conditions as the activities of legal entities. There are certain differences:

- Only legal entities are allowed to engage in certain types of activities;

- Several simplified taxation options are allowed for entrepreneurs.

Unlike legal entities, an individual entrepreneur can carry out its activities independently and carry out accounting without the involvement of hired employees. Typically, this form of existence is preferred by persons who receive profit from the services provided, for example, accounting operations, IT services, legal advice, training, and so on.

On the other hand, if an individual entrepreneur still attracts workers, but does not formalize them, then he bears responsibility similar to legal entities. The amount of the fine can range from 1 to 5 thousand rubles for each employee with whom an employment contract has not been concluded within 3 days. In addition, regulatory authorities may suspend activities for up to 3 months.

Decree for individual entrepreneurs without employees

Sick leave is accrued under similar conditions in connection with pregnancy and childbirth. But since the minimum amount of such sick leave is 51,918.9 rubles, it is more profitable to pay about 4 thousand rubles than to completely lose benefits.

The peculiarity is that when going on maternity leave in 2021, contributions for 2021 must be paid.

Also, to receive child care benefits, you need to pay a voluntary contribution to the Social Insurance Fund for the previous year. Considering that the monthly benefit amount is 4,512 rubles or 6,284.65 rubles, respectively, for the first and second child, the payment of contributions is fully justified.

Payment procedure

Insurance payments can be made as a one-time payment or divided into several parts. The choice of an entrepreneur is determined by the specifics of the activity and its scale. A one-time payment is relevant in a situation where a business representative is confident that he will be able to pay the full insurance amount within the deadline established by law without harm to his activities. In practice, it is more convenient and safer to make contributions to the budget current account throughout the year in equal parts, defining advance payments.

Who should submit the report?

The obligation to submit reports from an entrepreneur without employees is removed. But there is a high probability that regulatory authorities will require additional clarification.

In any case, it must be reported separately that the subject simply does not have hired force. A zero report is always submitted, even when there are workers, but they are not continuing to work and are temporarily absent from the site. Document samples help you understand the filling rules.

Penalty for late reporting

Fines apply even to companies that do not have employees or work at the moment. The penalties are described as follows:

- If there is no report - a fine of 1000 rubles.

- 300-500 rubles is a punishment for administrative persons on whose part violations are detected.

- Transactions on bank cards and accounts are suspended. If the shortcomings are eliminated, then the situation is corrected.

- 200 rubles when only some registration rules are not followed.

Let's sum it up

After the decision of the Constitutional Court of the Russian Federation dated January 30, 2020 No. 10-O, tax authorities changed their opinion on accounting for expenses for calculating 1% contributions from excess income under the simplified tax system to the exact opposite of what they previously adhered to.

Now, income for determining the calculation base of 1% of the excess can be reduced by confirmed expenses. And the overpayment can be returned, but you must first make a calculation whether it will be profitable.

Read also

23.04.2020

Background

For a long time, tax officials were unanimous that under the income-expenditure simplified tax system, the calculation of contributions of 1% of the excess is based on a base equal to the received . It was not allowed to take into account expenses (letter of the Federal Tax Service of Russia dated September 23, 2019 No. BS-4-11/19262, letter of the Ministry of Finance of Russia dated July 31, 2020 No. 03-15-05/67206).

The reasoning was based on the wording of the Tax Code. In Art. 430 states that for the simplified system, income for the purpose of calculating 1% of the excess is calculated on the basis of Art. 346.15. This article does not say a word about expenses.

But such rules put general-regime individual entrepreneurs in an unequal position (they could, when calculating 1%, reduce income for expenses) and simplified individual entrepreneurs, which contradicts the basic principles of tax law.

There were individual court decisions where the courts sided with taxpayers. However, the official position of the tax authorities remained the same.

Maximum amounts of accruals for individual entrepreneurs

Rates for social and pension contributions may change for employers who pay their subordinates well. There are maximum amounts of employee income at which tariffs change:

- pension contributions until the end of the year will be only 10% if the employee receives from 1,150,000 rubles per year;

- Social insurance contributions are not charged if the employee’s annual income is more than 865,000 rubles.

These rates are revised every year.

Reporting

Fixed insurance payments

An entrepreneur does not need to report if he does not have employees. To avoid claims from regulatory authorities, it is enough to pay all payments on time. However, if there are personnel who are in an employment relationship with a business representative, he needs to submit reports to each authorized authority, which are compiled based on the results of the past month.

How can an individual entrepreneur save on fees?

Due to the amount of insurance premiums, reduce taxes under certain taxation systems:

- The general taxation system or “simplified” income minus expenses. Here, all expenses for insurance premiums are considered as expenses. Therefore, the amount of income tax is reduced.

- Single tax on imputed income or “simplified” income. The amount of contributions is subtracted from the amount of taxes, but there is a limit on the amount of reduction - up to 50% of the tax.

An alternative is to outsource some of the company's tasks.

Outsourcing of accounting is a colossal saving on the staff of accountants. If you want to optimize your expenses, our company will take care of all your accounting and reporting to the Federal Tax Service. Read more about our services by following the link

Online cash register for individual entrepreneurs without employees

In recent years, there has been a gradual introduction of online cash registers for various types of businesses (cash register equipment (CCT)). Deferments were granted several times to certain categories. According to changes to the legislation dated 06.06.19 (No. 129-FZ), the next deferment until 07.01.21 was received by individual entrepreneurs who do not have employees who:

- personally provide services;

- sell products they produce directly.

Remember: Bill No. 682709-7, which was adopted by the Federation Council and signed by the President - Federal Law 129-FZ dated 06/06/2019 states that for individual entrepreneurs without employees, cash registers are not needed until 07/01/2021.

Entrepreneurs who sell low-cost goods (ice cream, newspapers, soft drinks by the glass) or provide inexpensive services to the population (shoe repair, key making), as well as a number of other business transactions, are completely exempt from the obligation to use online cash registers.

What happens for non-payment

It would seem that everything here is extremely clear: penalties and fines. However, readers who often ask this question to the experts of the Papa Pomog magazine want to know the exact current amounts of these sanctions. Let's find them out!

As I already wrote above, reports are submitted on contributions for employees. As practice shows, this is where an individual entrepreneur most often receives a fine. Its size is 1 thousand rubles. provided that the fees have been paid on time.

If the payments are late, the fine will be from 5 to 30% of the amount payable indicated in the calculation for each, even less than a month of delay, but not less than 1 thousand rubles. (Article 119 of the Tax Code of the Russian Federation).

And again an example.

IP Makarov I.S. I was late with the payment for the 1st quarter of 2021 by 1 month 3 days. The deadline for submission is April 30, in fact, the entrepreneur-employer reported on June 02, 2021. The estimated amount of contributions payable is 64,000 rubles.

Despite the fact that the delay in submitting the report was a little more than one month, we calculate the fine for 2 months: (64,000*5%)*2=6,400 rubles. We compare the obtained value with the minimum set value. The calculated amount is more than 1 thousand rubles. This means that IP Makarov I.S. will pay 6,400 rubles.