Innovations in the P-3 form from 2020

Starting with reporting for January 2021 , it is necessary to fill out and submit Form P-3 “Information on the financial condition of the organization” on a new form.

The new P-3 form was approved by Rosstat order No. 421 dated July 24, 2019 in Appendix No. 6. Instructions for filling out the new P-3 form were introduced by Rosstat order No. 711 dated November 27, 2019. It looks like this:

The new form P-3 2021 can be downloaded for free using the following link (excel):

FORM P-3 IN 2021

The form has not undergone significant changes. But the list of entities who must submit this form has been changed.

Completing the fourth section

Just like the two previous sections, this section is filled out only once every quarter. It reflects information on shipped products and services provided by different countries:

- Line 51 is intended to describe settlements with Russian companies.

- Information on settlements with organizations of the CIS countries is reflected in lines 52 to 62.

- Settlements with non-CIS companies are reflected in line 63.

Indicators that can be used to characterize the state of settlements are:

- the volume of products, services and works sold (together with taxes and excise taxes) - the first column;

- debts of customers and buyers, including overdue ones - column two;

- debt to suppliers, including overdue – third column;

- debt on received loans, including overdue ones - column four.

Also in the fourth section the following information should be reflected:

- the head of the organization - his last name and initials;

- responsible employee – surname, initials and position of the person involved in reporting.

Who submits form P-3 in 2020

Statistical reporting forms are quite simple and understandable to use. Respondents and deadlines for submitting forms are usually indicated on their cover pages. Form P-3 is no exception.

For convenience, we will list those who should and who should not submit this report to the diagram:

There is no exemption from submitting the zero form P-3. If a legal entity is included in the list of applicants and there are no indicators, they submit a zero - a completed title page and empty other sections.

Intermediate statistics

To quickly assess the financial activities of business entities, interim reporting is prepared. Compiled for a month, quarter with an accrual result from the start of the reporting annual period. The information allows Rosstat to keep abreast of the monthly and quarterly development of companies, analyze, and use the effectiveness of investment projects to plan economic development for the near and distant future.

Reporting is completed on the basis of a comprehensive accounting analysis, consisting of an analytical, synthetic invoice.

Separate legal entities that do not produce goods or provide services do not provide reporting under P-Z. These include housing construction cooperatives, GSK, housing cooperatives and others. The norm was formed by the corresponding Order No. 625.

Deadlines for submitting form P-3 in 2020

There is a correlation between submitting form P-3 by deadline, depending on who submits this form:

KEEP IN MIND

The form that is submitted at the end of the quarter is essentially the same monthly form on which the “quarterly” sections are completed. 2 more days are allotted for its delivery.

Even if monthly submission of the report is established, some sections of the P-3 form are filled out only based on quarterly results. We will consider the features of filling out form P-3 below.

When to take it

There are three deadlines for submitting the form depending on various factors:

- Every month, up to and including the 28th, P-3 is handed over to organizations with more than 15 employees and a turnover of over 800 million rubles per year. If within two years the number and annual turnover are below the specified parameters, there is no need to report.

- Every quarter: April 30, July 30, October 30, January 30. Two categories of persons submit information quarterly. Newly created or reorganized organizations in the current or past year, as well as holders of a mining license. For these persons, the number and turnover do not matter.

- Once a year, before January 30, federal state unitary enterprises and joint-stock companies with shares in federal ownership submit the form. An important condition: during the previous two years, the number of employees was up to 15 people, and the turnover was up to 800 million rubles per year.

Composition of form P-3

Form P-3 is a generalized form about the financial condition of an enterprise and allows Rosstat to analyze the company’s ability to maintain economic efficiency and manage capital.

It is filled out throughout the organization as a whole. There is no need to submit separate reports for each department.

The form contains the following sections:

And here is the approach to filling out form P-3 in different cases:

- only the title page is filled out by those organizations that are required to submit a report, but do not operate or do not have indicators for filling out form P-3 (in this case, Sections 1-4 are presented blank);

- those who must submit Form P-3 monthly fill out the Cover Sheet and Section 1 monthly, and Sections 2-4 quarterly.

Responsibility for violations

Late submission of a report in Form No. P-3 or submission of false information is punishable by fines:

- for an official – 10-20 thousand rubles;

- for an organization – 20-70 thousand rubles.

In case of repeated violation, fines increase: 30-50 thousand rubles for an official, 100-150 thousand for a company.

If errors or inaccurate data are discovered after filing the report, a corrected form must be submitted within three days of their discovery.

If errors are detected by Rosstat, the company will be notified. Three days are also allowed from the date of receipt of the notification to submit the correct form.

When sending the updated form No. P-3, you must attach a cover letter with explanations.

Documentation:

Procedure for filling out form P-3

Form P-3 is filled out on the basis of synthetic and analytical accounting accounts. If an organization prepares interim reporting, then data from such reporting must be entered into Form P-3. If the company does not have such an obligation, primary accounting information should be used.

Cost indicators in form P-3 are rounded to the nearest thousand rubles.

No sections of the form are a generalization of its other sections, so you can fill out the sheets in order.

Title page

The title page must be submitted in any case, no matter who submits the P-3 form and at what time. It is necessary to fill in the following information:

- the period for which the reporting is prepared;

- name of the reporting enterprise;

- postal address of the company;

- OKPO.

Section 1

Lines 01-02 show the financial result from the general activities of the enterprise. This includes income from core activities and other income reduced by all expenses. Reflects pre-tax financial results.

Line 01 contains data for the reporting period of the current year, and line 02 contains data for the same period of the previous year.

Lines 03-12 show accounts receivable:

- line 03 – total receivables;

- line 05 identifies the debts of buyers and customers for goods, works and services from the total debt;

- lines 06 and 07 separate from the debt of buyers that which is secured by bills received, as well as debt on government orders;

- line 12 selects short-term receivables from the total amount.

Lines 13-25 show accounts payable:

- line 13 – general creditor;

- Lines 15-25 highlight from the total accounts payable debts to the budget, to state extra-budgetary funds, suppliers and contractors, as well as short-term creditors;

- Line 20 highlights from the debt to suppliers and contractors that which is secured by issued bills of exchange.

Line 26 is responsible for debt on loans and borrowings, line 27 is for short-term loans and borrowings.

In column 2, for each line, it is necessary to highlight the amount of overdue debt, if any.

Debt must be calculated for each counterparty and for each agreement separately. That is, if the counterparty is both a buyer and a supplier or has several contracts at the same time, then it is impossible to summarize the balance for each contract; they must be shown separately.

Section 2

The section is filled out only based on the results of the quarter. There are 2 columns in the section. The first column reflects the data of the reporting period of the current year, the second – the data of the same period for the previous year.

Line 30 shows revenue from main activities. VAT, excise taxes and other similar payments are not included here.

Line 31 is intended to reflect the cost.

Line 32 reflects general production expenses and expenses for maintaining the enterprise.

Line 33 is calculated. The difference is entered into it: line 30 – line 31 – line 32.

Line 34 reflects proceeds from the sale of fixed assets, if such transactions took place during the reporting period.

Line 35 is intended to indicate interest on loans that the organization took into account as expenses in the reporting period.

Section 3

The section is filled out quarterly.

Consists of lines 36-41, intended for information about non-current assets, and lines 42-50, intended for information about current assets.

Line 50a - “Net assets” - is filled out only in the report for the full year as of the end of the year.

In non-current assets the following are highlighted line by line:

- NMA, R&D results; separately - contracts, lease agreements, business reputation, marketing assets;

- OS, profitable investments; separately – land plots and environmental management facilities;

- unfinished capital additions.

In current assets the following are highlighted line by line:

- stocks; separately - production inventories, costs in work in progress, finished products, goods for resale;

- VAT on purchased assets;

- short-term financial investments;

- cash.

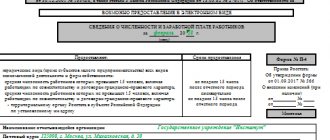

Section 4

Another quarterly section P-3.

Section 4 of form P-3 contains information about the organization’s interaction with Russian counterparties (totally on page 51) and with counterparties from other countries. CIS countries are highlighted in separate lines (pp. 53-62). Non-CIS countries are combined in one line 63.

The following information must be filled in:

- volume of goods shipped, including VAT and other similar payments;

- customer debt (separately - overdue);

- debt to suppliers and contractors (separately - overdue);

- debt on received loans and borrowings (separately - overdue).

General information about the organization

The title part of the report contains general information about the enterprise. The name of the enterprise is indicated in full and, in brackets, in abbreviated form. The name must correspond to the constituent documents. The OKPO statistics code must be indicated on the title. When submitting reports, information about the address and actual location of the enterprise is provided. The data provided on the activities of a separate branch is accompanied by the name and address of the actual location.

The form presents comparative figures for the reporting and previous periods. When reorganizing the structure or changing the organizational form of an enterprise in one of the relevant periods, data must be presented according to the conditions of the reporting period. Additionally, explanations are provided for filling out the form in case of changes that occurred during the reporting period.

Correspondence of lines of form P-3 to accounting lines

Let's put into the table the correspondence of the lines of form P-3 with the lines of the balance sheet and the financial results statement.

| FORM LINE P-3 | BALANCE SHEET LINES | FINANCIAL STATEMENT LINES |

| Line 01 Section 1 | – | Profit (loss) before tax for the reporting period |

| Line 02 Section 1 | – | Profit (loss) before tax for the same period of the previous year |

| Line 30 Section 2 | – | Revenue |

| Line 31 of Section 2 | – | Cost price |

| Line 32 of Section 2 | – | Selling expenses + Administrative expenses |

| Line 36 Section 3 | Result for section 1 “Non-current assets” | – |

| Line 42 Section 3 | Result for section 2 “Current assets” | – |

Completing the second section

The second section describes profit and cost information. It is filled out only once per quarter. All data must fully correspond to the data from the financial statements. results.

This section is completed in the following order:

- Line 30 records the total amount of profit from the sale of products, works and services. The amount is indicated excluding VAT.

- Lines 31 and 32 are intended to indicate the cost of production, administrative and commercial costs.

- In line 33, the organization must calculate the financial result from its activities.

- Line 34 reflects information about revenue for sold fixed assets.

- Line 35 takes into account interest on the use of borrowed money.

Example of filling out form P-3

Let Principle LLC be one of those legal entities that need to submit Form P-3. The accountant of Princip LLC fills out form P-3 based on the results of the first quarter of 2021. Interim financial statements are not prepared, so Form P-3 is filled out based on primary accounting data.

Based on the results of the first quarter, it is necessary to fill out all sections of the P-3 form. LLC "Princip" has no counterparties abroad.

This is what a sample of a completed P-3 form looks like in 2021:

Form representation methods

The enterprise has the right to independently choose the method of reporting. Several reporting methods are allowed:

- Representation by an authorized representative of the company in person. The document is submitted on paper. Used if you have time to visit the territorial office of Rosstat.

- By post. The shipment is accompanied by an inventory to confirm that Form P-3 was sent. Used when the territorial authority is remote or has access to the Internet.

- In electronic form, using an electronic signature to transfer data. The forms must contain a code assigned to identify the territorial authority. The transfer is made using an electronic digital signature certificate or specialized telecom operators. Used when there is no time to visit a territorial office or post office.

Each reporting method has advantages and disadvantages.

| Conditions | Personal submission | Mailing | Electronic form |

| Advantages | No additional expenses | There is no need to personally visit the territorial authority, obtain an electronic digital signature or contact an operator | Data transfer rate |

| Flaws | Significant waste of time | Additional shipping costs | The need to create an electronic signature or enter into an agreement with the operator. |