Account 11 is used to reflect information about animals, beasts, fish, poultry, and bees that are being fattened and are not included in the main herd.

Account 11 “Animals for growing and fattening”, as a rule, is used by agricultural producers to summarize information about animals that do not belong to adult productive livestock. The chart of accounts accounts for the account. 11 to production inventories, that is, to the current assets of the company. Unlike the account. 01, which takes into account the main adult livestock, count. 11 is, in fact, an account reflecting information about the agricultural producer’s work in progress.

Attention! Account 11 is not intended for accounting for adult large livestock, but can be used for all small animals (rabbits, bees, poultry), since the transfer from fattening to the main herd seems to be too labor-intensive, therefore, to simplify accounting, they are taken into account on the account. eleven.

Account 11 is active, as it reflects information about the assets (property) of the company.

Accounting is carried out by the number of heads, their weight and cost.

The costs of growing and fattening are written off from Kt. 11 on account 20 or count. 29 depending on the accounting policy.

Purpose of 11 accounts

The eleventh account in accounting practice is not so common in practice. He is a “worker” for agricultural enterprises involved in raising livestock.

What happens in life is that, due to the specific nature of production activities, certain enterprises use highly specialized balance sheet accounts, which include item 11 “Animals for fattening and rearing.” They are usually used by zoos, circuses, livestock farms, etc.

The indicated position summarizes data on existing animals representing the property of an economic entity and their movement. Such animals include fattening herds, young animals, birds, service dogs, etc.

If we consider the structure of the balance sheet, then the balances on the 11th position of the Chart of Accounts are part of inventories and are reflected in the second asset section of the balance sheet. To make it more convenient to keep track of such transactions, account 11 has sub-accounts, including:

- 11/1, in which young animals are taken into account until the animals reach a certain age and indicators;

- 11/2, which takes into account the main animals in fattening herds;

- There are a number of other sub-accounts that are opened depending on the type of animal.

The costs of keeping animals are reflected in such items as main production (20), auxiliary production (23) and service farms (29).

Accounting by debit

Debit turnover by account. 11 reflect the acquisition of animals, as well as offspring and weight gain.

If the animal was purchased from a third party, the procedure for recording this transaction depends on the specifics of the accounting policy.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

If an enterprise uses accounting and actual prices for purchases, then the purchase of animals is carried out through an account. 15:

- Dt 11 Kt 15 - at discount prices;

- Dt 15 Kt 60 - at actual prices;

- Dt 15 Kt 16 (or vice versa) - deviations between prices.

If the use of account 15 is not provided for by the accounting policy, then the posting is made immediately to the account. 60 or 76 (in case of purchasing animals from an individual):

Dt 11 Kt 60 (76).

Young animals can be contributed by the founder as a contribution to the authorized capital. In this case, the account is activated. 75 “Settlements with founders”:

Dt 11 Kt 75.

Also on the account. 11 may include animals that were previously part of the main herd when they are culled. In this case, the Fixed Assets account is credited:

Dt 11 Kt 01.

The offspring is accounted for in correspondence with the cost account. If we are talking about productive or breeding livestock, then you need to use count. 20 “Main production”. The offspring of working livestock is taken into account in correspondence with the account. 23 “Auxiliary production”:

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

Dt 11 Kt 20 (23).

The weight gain and growth of animals are taken into account in correspondence with the account. 20 or 23 is similar to offspring. The difference is that throughout the year, planned indicators are used. This is due to the fact that it is technically difficult to measure actual growth on a monthly basis. At the end of the year, the amount is adjusted to the actual amount by an additional entry or reversal.

Basic cost structure

Account 20 accumulates the following types of costs:

- material, which are aimed at purchasing materials, raw materials, supplies, equipment, etc., necessary in the production process;

- wages and social needs - costs that go towards wages and insurance premiums for workers and other persons involved in production;

- depreciation - deduction for wear and tear of fixed assets that are directly involved in the manufacturing process;

- other costs, which include travel expenses, shortages identified within the limits of natural loss, deferred costs, etc.

In order for an accountant to be able to include indirect costs in the cost of each unit of goods manufactured, work performed or service rendered, these costs must be distributed. An enterprise has the right to independently choose one indicator of cost distribution, for example, the value of inventory assets used in the process of manufacturing goods.

Costs recorded in accounting account 20 should be written off to the standard (planned) or actual cost of manufactured products.

Regulatory acts

The procedure in which this balance should be used correctly is clearly and in detail specified in the Instructions of the Ministry of Finance attached to the chart of accounts subject to accounting.

The key nuance is that within the framework of this paper, instructions for calculating the costs of agricultural products were developed, which were called Methodological Recommendations for the Accounting of Animals in Growing and Fattening. The document describes all recommendations in detail.

Accounting: animals are recognized as OS

When purchasing adult animals (breeding, working, productive livestock) to form the main herd, capitalize them as fixed assets. Assign an inventory number to each animal, and give large animals (cows, stud bulls, etc.) a nickname. For each animal of the main herd, open an inventory card, for example, in form No. OC-6, in which you enter all the data characterizing the animal.

This is stated in paragraph 150 of the Methodological Recommendations, approved by Order of the Ministry of Agriculture of Russia dated June 19, 2002 No. 559.

In accounting, the costs associated with the acquisition of adult animals, which are fixed assets, are reflected in account 08 “Investments in non-current assets” subaccount “Acquisition of adult animals”. The acceptance of fixed assets for accounting is reflected in account 01 “Fixed assets”.

Make the following entries in accounting:

Debit 08 subaccount “Purchase of adult animals” Credit 60

– reflects the cost of animals purchased for a fee, which will be taken into account as part of fixed assets;

Debit 08 subaccount “Purchase of adult animals” Credit 23 (26, 70, 76...)

– reflects the costs of purchasing animals, which will be included in fixed assets.

Upon completion of operations to form the main herd:

Debit 01 sub-account “Working and productive livestock” Credit 08 sub-account “Purchase of adult animals”

– breeding, productive, and working livestock are accepted for registration.

This procedure follows from the Methodological Recommendations (accounts 01, 08), approved by Order of the Ministry of Agriculture of the Russian Federation dated June 13, 2001 No. 654, paragraphs 147–149 of the Methodological Recommendations approved by Order of the Ministry of Agriculture of the Russian Federation dated June 19, 2002 No. 559.

For more information about accounting for fixed assets received under paid contracts, see How to reflect the purchase of fixed assets in tax accounting.

Dt Account name Kt

123456Next ⇒

LECTURE 3. ACCOUNTS AND DOUBLE ENTRY

The concept of accounting accounts, their purpose and structure

Double entry of transactions on accounts, its rationale

Synthetic and analytical accounts, their purpose and relationship

Chart of accounts, its structure and purpose

Summarizing current accounting data. Turnover balance sheets

Classification of accounting accounts

The concept of accounting accounts, their purpose and structure

The balance sheet of an organization as a form of financial reporting contains data characterizing accounting objects in monetary terms as of a certain (usually reporting) date. However, in the process of economic activity, making management decisions and carrying out control measures, operational information is needed on the state and movement of assets, liabilities, and the formation of financial results for individual business transactions. For this purpose, accounting uses a system of accounting accounts in which facts of economic activity (business transactions) are recorded using the double entry method.

System of accounts - a method of economic grouping, current accounting and control of property

, obligations and business processes

. For each economically homogeneous accounting object, a separate account is opened: fixed assets, materials, intangible assets, authorized capital, settlements with suppliers and contractors, finished products, etc. Accounting

records are made in such an account, previously prepared with primary accounting documents .

Graphically, an account represents a table of a certain form, adapted for accounting records.

Externally, accounts look different depending on the software products used to automate accounting and the accounting forms used by organizations.

The most typical and simplified form of an accounting account is a two-sided table.

Dt Account name Kt

Depending on the nature of the accounting objects being taken into account, active and passive accounts with certain numbers are distinguished.

Active accounts are intended for property accounting. Active accounts are 01 “Fixed assets”, 04 “Intangible assets”, 10 “Materials”, 41 “Goods”, 50 “Cash”, 51 “Cash accounts”, etc.

Passive accounts are designed to record liabilities.

Main production: determining the composition of costs

The production process is a technological cycle for the creation, development, and assembly of finished products at an enterprise.

The totality of all costs associated with the production and sale of finished products forms its cost. The main production can be described as follows. Organizations carrying out production activities determine the cost of manufactured products. To account for the total amounts of such expenses, account 20 is used, the transactions for which we have collected in one table. It is applied in accordance with the chart of accounts approved by Order of the Ministry of Finance of the Russian Federation No. 94n dated October 31, 2000.

Primary production costs are costs that relate to the production of certain types of goods, works or services directly related to the main activity of the enterprise. Such costs can be direct or indirect.

Direct costs include the costs of purchasing raw materials and supplies involved in the manufacture of goods in a broad sense, remuneration for workers, damage from defects, depreciation, etc.

Indirect costs include costs associated with maintenance, administration and control of the production process.

It turns out that accounting account 20 for dummies is “Main production”, which reflects all production and general business costs of the organization.

At the “Main production” the following costs are taken into account:

- production of industrial and agricultural products;

- carrying out construction, installation, dismantling, geological exploration and design and survey work;

- provision of communication and transportation services;

- carrying out R&D work - research and development work;

- maintenance, operation and repair of highways, etc.

BASIC

Agricultural producers who meet the criteria of paragraph 2 of Article 346.2 of the Tax Code of the Russian Federation calculate income tax at a rate of 0 percent. At the same time, a prerequisite for such compliance is that the organization must produce the products sold itself (letter of the Ministry of Finance of Russia dated December 4, 2012 No. 03-03-06/1/620). This rate applies to activities related to the sale of produced, as well as manufactured and processed agricultural products. This is stated in paragraph 1.3 of Article 284 of the Tax Code of the Russian Federation.

The costs of purchasing animals that are not recognized as fixed assets should be included as part of material expenses (subclause 1, clause 1, article 254 of the Tax Code of the Russian Federation).

Animals related to fixed assets should be taken into account at their original cost (clause 9 of Article 258 of the Tax Code of the Russian Federation). Starting from the next month after the facility is put into operation, begin calculating depreciation (clause 4 of Article 259 of the Tax Code of the Russian Federation).

After the animals are registered, deduct input VAT (Article 171 of the Tax Code of the Russian Federation). At the same time, other conditions must be met.

The cost of animals included in fixed assets before January 1, 2013 is subject to property tax (clause 1 of Article 374 of the Tax Code of the Russian Federation). Animals included in fixed assets after January 1, 2013 are not subject to property tax (subclause 8, clause 4, article 374 of the Tax Code of the Russian Federation).

Typical entries for the Main Production account

Let's present the key transactions for account 20 with comments in the table:

| accounting entry | the name of the operation |

| Dt 20 Kt 02, 10, 21, 60, 69, 70 | Write-off of costs directly related to the manufacture of GWS |

| Dt 20 Kt 23 | Write-off of auxiliary production costs |

| Dt 20 Kt 25, 26 | Write-off of indirect expenses |

| Closing 20 am | |

| Dt 28 Kt 20 | Defects in production taken into account |

| Dt 40 Kt 20 | The cost of finished products is taken into account in accordance with its standard cost |

| Dt 43 Kt 20 | The actual cost of GWS is reflected |

| Dt 90.2 Kt 20 | Manufactured GWS are sent for sale |

| Dt 91.2 Kt 20 | Canceled orders taken into account |

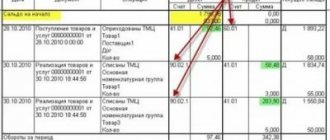

Accounting of animals for growing and fattening

The specificity of various production processes implies the use of highly specialized balances. These also include account 11 “Animals for growing and fattening”. It is used by many livestock farms, as well as entertainment establishments such as circuses and zoos.

The purpose of the balance sheet is to accumulate data on the presence of animals as property of the company, as well as on the movement of this asset.

In the main accounting document, called the balance sheet, it relates to the inventory category, and its reflection is carried out within the second section. For the convenience of conducting accounting operations, it is customary to open subsections on the balance sheet:

- 11/1. These are young animals. Young animals are counted on the account, and this happens until they reach the established age period and condition. And this parameter is considered to be different for different species.

- 11/2. Fattening animals. Within this balance, accounting transactions are carried out based on species in the main livestock herds.

- 11/3. All operations on poultry used for laying eggs or slaughter are reflected here.

- 11/4. The balance is dedicated to animals, or more precisely, to a detailed display of information on each of them.

- Other subsidiary accounts, which display transactions for each individual type of animal.

Within the balance sheet under consideration, a large number of transactions are carried out daily. To avoid collecting them in large quantities, you can make entries based on the results of the monthly period.