An individual entrepreneur has the right to reduce the amount of tax if he works under the patent system. You can reduce the amount of tax when purchasing cash register equipment by no more than 18,000 rubles per unit. However, there is one more condition under which it is possible to carry out the plan: the online cash register must be registered during the period from February 1, 2021 to July 1, 2021. Your tax amount depends on the correctly completed notification. If you have any doubts, it is best to seek help from a specialist.

Recommended form of notification for tax reduction

The Federal Tax Service has established a recommended form of notification to reduce the amount of tax on the purchase of cash register equipment when working in the patent system. So how do you fill out a reduction notice? It can be completed in either written or electronic form. If you chose to fill it out electronically, then you must have an electronic signature of the individual entrepreneur.

The notice consists of 3 sheets. It must be written in Russian letters, black, purple or blue. On the first sheet at the very top you indicate your TIN. Next, in the notification, fill in the code of the tax authority to which the individual entrepreneur applies to reduce the amount of tax. On the same sheet, fill out the last name, first name and patronymic, if the person has one. The contact details, number of completion and signature of the taxpayer are also indicated there. If the filing is carried out by a representative of the taxpayer, then copies of documents that confirm the authority of the person must be attached to the notification.

On the second page, on sheet A, you must indicate information about the cash register equipment itself. Complete data about all online cash registers should be provided here: the name of the cash register, serial number, registration number that was received from the tax authority, the date the cash register was registered and the amount of expenses. The amount of expenses includes not only the purchase of equipment, but also the costs incurred for its installation, setting up work - that is, all those that needed to be made for the cash register to work in accordance with the requirements of the federal law on cash register systems.

On the third page of the tax reduction notice, on sheet B, information about the patent is filled out. This notification sheet is used if an individual entrepreneur wants to reduce the amount of tax on several patents. In this case, it is necessary to indicate the amount of expenses for the acquisition of cash registers, the patent number and the date on which it was issued, the amount of tax on it, as well as the period within which the tax was paid. The TIN is also indicated at the top.

If the patent is received for less than six months, then the lines with the payment of parts of the tax - namely, 170-200 - are not filled in. If the patent was received for a period of six months to a year, then the lines for the full amount of tax payment - namely, 15-160 - do not need to be filled out. If the expenses exceed the amount for which the patent was purchased, then a tax reduction can be made for another patent, but this requires filling out line 210 and a new notification.

Sample of filling out an application to confirm the right to offset advance payments for personal income tax

The structure of the form is quite simple and understandable, but still some points may cause slight difficulties.

- At the beginning of the document, the TIN and KPP of the enterprise that is the foreigner’s employer are written, and the number of pages in the application is indicated next to it.

- Below, you should enter the serial number of the application for the current year (remember, it can be written at least every month - there are no explanations or restrictions on this issue in the legislation).

- Then the code of the tax service to which the completed form will be sent is entered in numbers.

- After this, the application indicates the full name of the employing organization or the personal data of the individual entrepreneur.

- Next, in the appropriate cells, you should note the year for which you want to reduce the amount of personal income tax and the number of pages on which the application is written.

- Next to it you need to indicate how many documents confirming the payment of advance payments are attached.

Filling out information about the taxpayer

Filling out information about the taxpayer is in the lower left corner of the first sheet of the document. Here you enter data about the person who, with his signature, confirms the authenticity of the information included in the application: the head of the company, his representative, or an individual entrepreneur.

You must provide information about the individual:

- surname-first name-patronymic,

- TIN,

- contact phone number (in case the tax authorities have any questions),

- date of filling out the application.

There is a space on the right for a tax specialist to fill out; here the taxpayer does not need to write anything.

Sample of filling out the second page of the application

The next part concerns directly the foreign citizen who claims to reduce personal income tax through advance payments under a patent. Here you need to enter his personal information:

- FULL NAME,

- date of birth,

- TIN,

- information from the identity document: series, number, date of preparation and place of issue.

Then all information entered in the application is confirmed by the signature of the applicant.

Tax deduction for online cash registers: how to minimize tax on UTII or patent

- Submit the declaration in the manner usual for you. An explanatory note can be sent via telecommunication channels as an attachment to a letter (informal document flow).

- In your UTII tax return, indicate how much money was spent on the purchase and implementation of an online cash register.

- Fill out the explanatory note and attach it to the declaration.

In the current declaration form for UTII there are no lines in which you can enter the costs of purchasing cash register equipment. The portal of regulatory legal acts has published, in which a section will appear devoted to the calculation of the amount of expenses for the acquisition of cash registers, which reduces the amount of the single tax.

Until the new UTII declaration form is approved, the amount of expenses for cash registers can be taken into account on line 040 of Section 3 of the current form.

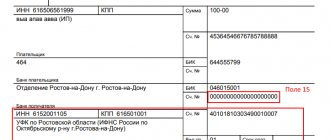

On the recommended form of notification of a reduction in the amount of tax paid in connection with the use of the patent taxation system by the amount of expenses for the purchase of cash register equipment

Letter of the Federal Tax Service No. SD-4-3/ dated 04/04/2019 The Federal Tax Service sends for use in its work the recommended form of notification of a reduction in the amount of tax paid in connection with the use of the patent taxation system by the amount of expenses for the purchase of cash register equipment ( hereinafter referred to as the Notification) and instructs the Departments of the Federal Tax Service for the constituent entities of the Russian Federation to bring this letter to the subordinate tax authorities and taxpayers.

“On the use of cash register equipment when making cash payments and (or) payments using electronic means of payment”

If several sheets B of the Notification are filled out, the value of the indicator according to line code 210 is indicated on the last page of Sheet B to be filled out; in the previous pages, a dash is placed on this line. At the same time, please note that an individual entrepreneur has the right to notify the tax authority of a reduction in the amount of tax paid in connection with the use of the patent taxation system in any form with the obligatory indication of the information provided for in Article 2 of Federal Law No. 349-FZ of November 27, 2019

“On amendments to part two of the Tax Code of the Russian Federation”

Acting State Advisor of the Russian Federation, 3rd class D.S.

Application to reduce personal income tax for children

The personal income tax deduction for a child is an amount not subject to taxation that is due to an employee with children. The employer does not have the right to independently reduce tax payments if the employee does not apply to him with a corresponding application.

Attention! There is no legally established form for such an application - the employee writes it in any form, indicating the type of tax deduction, the reason, the number of children to whom the deduction rule applies, listing the attached documents. Before writing an application, you should consult with the employer - some companies have developed forms for such documents, and the employee only has to fill out the necessary fields.

New employees with children write a corresponding application for a tax deduction when applying for a job; those employed a long time ago - from the moment they received such a right, that is, from the moment the child was born or adopted.

Instructions for individual entrepreneurs: how to apply deductions to online cash registers

It is impossible to sum up the costs of different copies of CCP.

- 18,000 rubles for the first cash register;

- 15,000 rubles for the second.

Moreover, this amount, unlike insurance premiums, can be transferred.

PSN: a notification form has been prepared for applying a deduction for expenses on online cash registers

Website design Login Stay logged in Login via social network account: Registration A request to confirm registration will be sent to the e-mail specified in the form.

Login (min. 3 characters): * * Password: * * Password confirmation: * * E-mail address: * * First name: Last name: Gender: Gender Male Female Protection from automatic registration

Individual entrepreneur notification form on a patent to receive a deduction for an online cash register

That is, a separate copy of Sheet B is drawn up for each. Moreover, if there is a balance in the amount of expenses - if it is greater than the cost of all patents, the amount of this balance is recorded only on the last copy of Sheet B.

The previous ones are marked with dashes. You can download the form of notification of deduction for online cash register for individual entrepreneurs on a patent (PDF file). Please note that the expenses on the basis of which the deduction in question is applied, in addition to the cost of the online cash register, also include:

- cost of fiscal storage;

- cost of cash register software;

- the cost of the services of specialists who carried out paid setup of the online cash register.

How to cancel a fine

The organization also has the right to claim a complete abolition of punishment. To do this, you need to send a request to cancel the fine to the tax office.

The circumstances under which a fine can be canceled are established in Art. 111 of the Tax Code of the Russian Federation, namely:

- natural disaster, emergency or force majeure;

- the person who committed the unlawful act was in a sick condition;

- implementation of official written explanations from authorized bodies regarding the identified offense;

- other circumstances that may be recognized by the Federal Tax Service or the court as mitigating.

Online cash register: tax deduction

Unlike insurance premiums, which reduce the tax only for the period in which they are paid, the cost of CCP can be taken into account for several quarters. Therefore, you first need to reduce the tax on contributions, and then reduce the remaining tax by the amount spent on purchasing cash register equipment.

The amount of expenses for cash register systems that did not fit into the tax reduction for one quarter can be taken into account in the next period.

To exercise the right of individual entrepreneurs to deduct, the tax authorities planned to change the declaration.

However, the new form will definitely not appear by the beginning of the reporting period for the 1st quarter. And therefore, the Federal Tax Service issued a letter dated February 20, 2019 No. SD-4-3/, in which it proposed to take into account the costs of purchasing cash registers in the current declaration form, and not to show the amount of these costs anywhere in it, but to attach an explanatory note to the report. In this case, line 040 of section 3 is calculated taking into account the expenses incurred for the purchase of cash register equipment.

The individual entrepreneur purchased two copies of the CCP.

P-6 statistics

In order for organizations to report on their activities, quite a few reporting forms are provided. One of them is form P-6 statistics. It must be filled out by those legal entities that made any financial investments during the reporting period.

This form is intended to provide information to Rosstat about financial investments made by the organization. All those legal entities that made such investments during the reporting period and have an average number of employees of more than fifteen people are required to submit it. The following legal entities are exempt from submitting Form P-6:

- credit organizations;

- insurance organizations;

- municipal and state organizations;

- SMP;

- non-state pension funds.

All information in this report is entered for the company as a whole, without highlighting information on branches, if any.

Form P-6 “Information on financial investments” is submitted once a quarter. The information in it is reflected on an accrual basis for each reporting period. The report must be submitted to the territorial office of Rosstat before the twentieth day of the month following the reporting quarter.

Components of reporting

The attachment report includes three sections containing information about:

- money and financial investments;

- borrowed funds;

- reserves and capital.

The first two sections are completed for each reporting quarter. They contain a detailed breakdown of analytics regarding sources of income and investments, reflecting changes in cost indicators.

The third section of the P-6 statistics form is filled out only for the reporting period of six months. It reflects information about investments in the authorized capital with details by person.

Procedure for filling out the first section

The first section of the statistical form P-6 is filled out in the following order:

- In the 1st column, lines from 010 to 435 reflect financial investments at the beginning of the year.

- Columns 2 to 5 are intended to indicate changes in investments during the reporting period.

- In the 2nd column, lines 010 to 435 take into account the investments that the legal entity made during the reporting period, not taking into account the repayment of loans and securities.

- Column 3 specifies the return of granted loans and the sale of securities.

- Column 4 reflects changes in investments due to quoted or exchange rate revaluation.

- The 5th column is intended to account for changes in investments due to changes in assets that were not reflected in the previous columns.

- Column 6 indicates the amount of investment that was accumulated at the end of the year.

- Column 7 records the income that the legal entity received for its share in the authorized capital and for the use of securities.

Procedure for filling out the second section

The instructions for filling out the P-6 statistics form provide the following rules for filling out the second section:

- Line 500 should be equal to the sum of lines 510, 530, 540 and 600.

- The 1st column contains information about the amount of borrowed money at the beginning of the year.

- In the 2nd column, information about receiving borrowed money is written down.

- Column 3 is intended for information about the repayment of loan obligations.

- In the 4th column enter information about changes in obligations due to quotation and exchange rate differences.

- The 5th column contains data on other changes in obligations not reflected in the previous columns.

Procedure for filling out the third section

Filling out the third section of form P-6 is carried out in the following order:

- Line 700 reflects information about the company’s reserves and capital.

- Lines 710 to 800 are filled in only for the period from January to June of the reporting year.

- Line 710 indicates the amount of the authorized capital, which is reflected in the constituent documents. From this line, the share of participation of non-residents and residents is separated, lines 720 and 730, respectively.

- From line 730, information is highlighted: on the participation of non-financial companies (line 740);

- banks (line 750);

- insurance companies and non-state pension funds (line 760);

- other financial institutions (line 770);

- state bodies controls (line 780);

- the population and non-profit companies that provide services to the population (line 790).

Shares can be purchased either for cancellation or for subsequent resale.

Sample form

filling out form P-6.

Tax deduction for online cash register

Thus, if you are an individual entrepreneur in the catering industry - for example, you have a small cafe - then it would be most profitable to purchase a cash register as soon as possible and immediately register it: you are guaranteed to receive a tax deduction when purchasing an online cash register in 2021.

But in 2021, you will be able to claim reimbursement only if you do not have hired employees. If, according to an employment contract, at least one person is employed in your cafe, you will no longer be able to return expenses to the cash register.

If you combine UTII and PSN, you will be able to receive a tax deduction for an online cash register using only one mode. When purchasing an online cash register for UTII, a tax deduction cannot be obtained for the period that preceded the registration of the cash register.

Deduction for online cash register: the recommended form of notification of tax reduction for PSN has been approved

Starting from 2021, entrepreneurs on PSN can reduce tax on the amount of expenses for purchasing an online cash register.

To take advantage of the deduction, individual entrepreneurs must submit to the inspectorate a special notification of a reduction in the amount of tax by the amount of expenses for purchasing the cash register. The recommended notification for this is given in the letter from the Federal Tax Service of Russia. The notification form consists of three parts:

- title page;

- sheet A, where information about the purchased cash register equipment is indicated;

- Sheet B, which reflects the reduction in the amount of tax on cash register expenses.

Line 050 of sheet A “Amount of expenses for the acquisition of cash register systems” indicates the amount of expenses for:

- purchasing the cash register itself;

- purchase of a fiscal drive;

- purchasing software;

- performance of related work and provision of services (services for setting up cash register equipment, etc.), including the costs of bringing cash register equipment into compliance with the requirements of the Federal Law (for example, costs of paying for OFD services; also see.

How to receive a notification

In order to receive a notification from the tax office about the right to reduce personal income tax through advance payments, the employer of a foreign citizen needs to contact the local tax service with a corresponding request, which is also drawn up in the form of an application in the approved form.

Within 10 days after this application is received by tax specialists, they are required to send the required notification.

Moreover, before sending it, tax officials must make sure that the FMS has proof of the conclusion of an employment contract between a foreigner and a Russian enterprise, and also that a notification has not yet been sent to anyone in relation to this person.

KND 1112020

In 2021, businessmen with a patent have the right to deduct from tax the amount they spent on installing and purchasing a cash register. This rule applies to the following situations:

- They have no employees;

- The business is not related to catering or retail;

- The cash register was registered in the period from 02/01/2017 to 07/01/2019;

- The device is in the register of CCP of the Federal Tax Service.

Individual entrepreneurs who sell retail and have hired staff, unfortunately, are already late. They had the right to reduce the tax until the end of 2021.

This amount includes:

- Cash register price;

- The cost of the fiscal drive and software;

- The amount of money spent on the installation and maintenance of the CCP.

What is the essence of the innovation: letter from the Federal Tax Service dated 04/04/2019 No. SD-4-3/ [email protected]

In accordance with Art. 346.51 of the Tax Code of the Russian Federation, individual entrepreneurs on PSN have the right to reduce the calculated tax (patent fee) by the amount of expenses associated with the purchase of online cash registers - if such expenses were incurred during the periods indicated in the specified article of the Tax Code. Namely - from 02/01/2017 to 07/01/2019 (if the individual entrepreneur has no employees) or from 02/01/2017 to 07/01/2019 (if the individual entrepreneur has employees).

Subscribe to our channel in Yandex Zen - Online Cashier! Be the first to receive the hottest news and life hacks!

The deduction can be applied to any number of patents. That is, one patent is “closed” first, and if there is an “unused balance” for online checkout expenses, it is transferred to other patents.

1. Ask our specialist a question at the end of the article. 2. Get detailed advice and a full description of the nuances! 3. Or find a ready-made answer in the comments of our readers.

To use the right to deduct, individual entrepreneurs on PSN must send a notification to the Federal Tax Service. Until recently, it had to be compiled in free form. But the Federal Tax Service decided to standardize this procedure - by approving a unified form of the corresponding notification in a letter dated 04/04/2019 No. SD-4-3/ [email protected] (LINK).

Let's take a closer look at its structure.

Wording options for petitions

The following are usually indicated as mitigating facts:

- committing an offense for the first time;

- unintentionality of actions;

- impossibility of paying wages to employees due to the collection of a fine;

- the activity is unprofitable or seasonal;

- the organization is a bona fide taxpayer, etc.

If you are preparing a petition to the tax office to reduce the fine for late submission of reports, the following will be recognized as mitigating facts:

- disproportionate punishment to the nature and gravity of the offense committed;

- insignificance of delay;

- lack of intent to commit an offense;

- absence of negative consequences for the budget;

- a technical failure that prevented the report from being submitted on time;

- the fact of committing a violation for the first time.

IMPORTANT!

Regardless of what circumstances are cited, it is necessary to supplement the petition with copies of documents confirming the existence of the facts mentioned.