Recommendations for users of 1C:Enterprise programs

If changes are made to the appendix to the purchase book, for example, to section 8.1, then the information from the purchase book as part of the adjustment comes with the sign “1” - the information is relevant, and the appendix - section 8.1 with the sign of relevance “0” - the information is not relevant.

Procedure for adjusting the calculation of insurance premiums In what case is it necessary to adjust the calculation of contributions in 2021? If an organization or individual entrepreneur has discovered that in the Calculation of insurance premiums they submitted, for any reason, the amount of contributions payable was underestimated, it is necessary to submit an updated Calculation to the tax office (clause 1, 7, Article 81 of the Tax Code of the Russian Federation).

Once all the data on incoming and consumed products has been filled in, you should proceed to the control and dispatch stage.

A report with error code 50 will not be received by the Pension Fund; it will have to be urgently redone. If the protocol contains inaccuracy codes 30, the reporting also needs to be redone. To decipher error codes, use tables 34-41 (Resolution of the Board of the Pension Fund of the Russian Federation dated December 6, 2018 No. 507p).

Results

Adjustment of 4-FSS in 2020-2021 is carried out according to the rules provided for in Art. 24 of Law No. 125-FZ. If in the original calculation, due to errors, the base for contributions “for injuries” was underestimated, submission of an adjustment is mandatory. In such circumstances, before submitting the clarification, the missing amount of contributions and penalties must be paid. Then the company will be able to avoid a fine. In other cases, the employer can adjust 4-FSS voluntarily.

Sources:

- Federal Law of July 24, 1998 No. 125-FZ (as amended on December 2, 2019) “On compulsory social insurance against industrial accidents and occupational diseases”

- Order of the Federal Insurance Service of the Russian Federation dated September 26, 2016 No. 381 (as amended on June 7, 2017) “On approval of the form of calculation for accrued and paid insurance contributions for compulsory social insurance against industrial accidents and occupational diseases, as well as for expenses for the payment of insurance coverage and The order of filling it out"

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

When adjusting the VAT return is not necessary

If a request has been received from the tax office to provide an explanation of the submitted declaration (clause 3 of Article 88 of the Tax Code of the Russian Federation). The explanations must include the rationale for the changes made to the revised VAT return.

Reception of such files occurs only in “manual mode”, that is, the inspector himself registers this report in the IFTS software. And even if the shipment is agreed upon, but a refusal is received, the subscriber must contact the inspector again and find out further actions (re-send, submit on paper, by letter or other options).

Important: If the document contains adjustment blocks for employees for any period of 2013, then they need to be corrected for the reporting period for 2021.

If information on one of the employees is missing, the report will be sent to the Pension Fund, but the error will need to be corrected. For example, they forgot to include an employee who is on maternity leave or on maternity leave for up to one and a half years. To correct, fill out a report of the “Additional” type. Section three contains information. An EFA with the “Original” type is attached to the revised report.

What are the most common mistakes?

Rules for filling out forms change regularly, programs are updated, and this leads to errors.

The employee generates a document, sends it, shortcomings are identified, and the question immediately arises of how to make a corrective SZV-TD report to eliminate the violations. In practice, the following types of errors are often encountered:

- incorrect date of application for maintaining a work record book;

- the signature of the authorized person is invalid;

- incorrect file format;

- The reporting period in the SZV-TD is incorrectly indicated;

- incorrect employer details;

- errors in writing dates, numbers, information about work activities.

Use free instructions from ConsultantPlus experts to fill out the SZV-TD - even more examples of filling out and deadlines.

to read.

When do you need to submit a VAT clarification?

Sending accounting forms through Kontur.Extern is carried out in two stages:

- Compilation of a report. The user has several options to choose from:

- formation directly in the service;

- uploading a document prepared in advance and editing it;

- downloading a report file completely ready for sending.

- Checking the document and sending it to the Federal Tax Service.

The seller issues an adjustment invoice to the buyer “if there is a change in the cost of goods shipped (work performed, services rendered), transferred property rights, including in the event of a change in price (tariff) and (or) clarification of the quantity (volume) of goods shipped (work performed, services provided), transferred property rights” (clause 3 of Article 168 of the Tax Code of the Russian Federation). Section 6 (initial) - in section 6.2 the current period. You only need to fill out subsection 6.6 with additional accrued contributions.

The only difference when filling out the updated calculation from the primary one is that in certain fields it is necessary to note that the calculation is corrective.

Provide reliable and correct information. Depending on the type of error made, sections are filled out differently. If you indicated the wrong full name, SNILS, fill out sections 1, 2, 3.

If inaccuracies caused, on the contrary, an overpayment, tax legislation does not oblige you to submit an amendment.

There are 2 ways to make adjustments within the package:

- According to the new rules , the reporting period is always the one in which the data for adjustments is sent, that is, the current period.

- According to the old rules, 2021 is always taken as the current period.

But it is better to bring the taxpayer’s data in line with the data of the Federal Tax Service so that, if necessary, you can easily make offsets or refunds of overpaid amounts.

Pension Fund departments often resolve such issues at their own discretion, so before making an adjustment, you need to clarify the information with the relevant territorial office.

The downloaded report must be checked by the user independently and saved on a computer disk or flash drive.

Where to submit the adjustment and in what form

You need to submit the corrective 4-FSS to the same territorial office of the FSS where the original calculation was submitted and where you are registered as an insured.

To complete the adjustment calculation, you must use the form that was in effect in the billing period for which changes are made (clause 1.5 of Article 24 of Law No. 125-FZ of July 24, 1998).

It is not difficult to figure out which form to submit the adjustment calculation in - the calculation form does not change often.

Find out about the evolution of the 4-FSS form and its current form here .

You can see samples of filling out Form 4-FSS for different reporting periods, as well as a line-by-line algorithm for filling out a report in ConsultantPlus. If you do not have access to this legal system, a full access trial is available for free online.

Calculation of insurance premiums: adjustment

A., then he will need to prepare a clarifying version of Section 3 with changed data for this employee.

The report is filled out in the usual way - the same as on paper or in other programs / services. However, there are fields common to most reports:

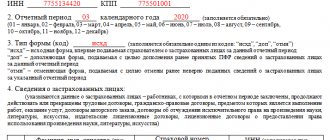

- "KND forms" . Approved code - it is entered automatically.

- “Adjustment number” or “Document type” . Here you need to indicate “0” if the document is submitted for the first time, or the serial number of the corrective report if an adjustment is submitted. The maximum value is 999.

Reporting adjustments must be submitted to all regulatory authorities where the primary information was submitted.

If you have uploaded ready-made files, we first recommend deleting the existing declaration and application files in the draft, and then uploading new files that will be sent when submitting the adjustment.

The field “Relevance indicator” is filled in only in VAT annexes. It appears if the “Adjustment number” field contains a value other than 0.

If for some reason an organization did not report for the last tax period before the reorganization, then all rights and obligations to submit tax reports are assigned to the successor organization.

In Art. 81 of the Tax Code of the Russian Federation describes cases when no sanctions are imposed on the taxpayer when submitting an updated calculation. This applies to situations:

- submission of an amendment in which contributions payable will become less than in the primary report;

- submitting an update before the deadline for submitting the main calculation expires;

- submitting a clarification in case of an independently identified error before scheduling an on-site tax audit (in this case, the penalty for contributions must be paid before submitting the clarification if the payment deadline has already arrived);

- submitting a clarification in case of an independently identified error, if the tax authorities did not notice this error during an on-site audit.

When filling out the adjustment, you should remember that:

- all necessary sheets of the form are filled out, even if the information on them does not differ from the initial calculation;

- section 3 on personalized accounting is filled out only for those individuals affected by the changes;

- all columns indicate new indicators (not the values by which the primary calculation indicators need to be reduced or increased, but new ones).

Three rules for completing and sending corrections

If you have never had to amend 4-FSS before, difficulties may arise. How to make adjustments to 4-FSS while complying with regulatory requirements?

When preparing and sending the 4-FSS adjustment report to the fund in 2020-2021, we recommend adhering to the following rules:

- Enter the adjustment number on the title page of 4-FSS - there is a separate field for this:

- All other data must be reflected in the same way as in the original 4-FSS, taking into account the corrected errors and inaccuracies. If changes are made to the calculation due to changes in the taxable base or individual indicators, then reflect fully updated data in the calculation, and not the difference between the primary and adjusted data.

- Along with the corrective 4-FSS, it is advisable to send a covering letter to the fund, in which you need to reflect the reasons for submitting the updated calculation and indicate what information was corrected or supplemented.

There is no required form for such a letter. You can use the following example as a guide:

Attention! It is not necessary to issue a cover letter - such a requirement is not contained either in Law No. 125-FZ, or in the procedure for issuing 4-FSS, approved. order No. 381. Therefore, you can do without it.

What type of adjustment to indicate in RSV-1 (decoding) in 2019

There is no penalty for adjustments. The main thing is to submit the corrective report within the deadlines established for submitting the ERSV.

Additional sheets are not attached if an error occurred when transferring data from the primary purchase book or sales book to information from the purchase / sales book - section 8 or 9 of the declaration.

Experience with the Contour.Elba tool. The task was completed quickly and professionally. Let's keep working! Thank you

When uploading the updated tax return, all information from the additional sheet of the purchase book will be transferred to Appendix 1 to Section 8 (Fig. 23).

In addition, in some situations it is necessary to re-submit the calculation even if the amounts of contributions to be accrued are correctly indicated. So, according to paragraph 7 of Art. 431 reports are considered not submitted in the following cases:

- Entering erroneous personal data on an employee - in section. 3 incorrectly entered or completely missing SNILS codes, INN, and the employee’s residential address.

- Identification of inaccuracies in numerical indicators - for example, in the amount of the taxable base or in payments to an individual, as well as in the amount of calculated contributions to section. 3.

- The discrepancy between the general values of the numerical indicators in Sect. 3 for the enterprise as a whole with those specified in subsection. 1.1, 1.3 App. 1 to section 1 information.

- Discrepancy between the total amount of accrued contributions for compulsory pension insurance from the base within the limit (for all employees in section 3) with the amount of compulsory pension insurance contributions for the enterprise as a whole, specified in subsection. 1.1 App. 1 to section 1.

The field “Relevance indicator” is filled in only in VAT annexes. It appears if the “Adjustment number” field contains a value other than 0.

Of course, the information accumulated in it must be truthful. Unfortunately, no one is immune from errors, and therefore they happen in reporting. Let's find out whether it is possible to submit adjustments to the financial statements, and how to do this.

Then messages should come from the tax authority. Depending on the result, this could be:

- "Notice of receipt of an electronic document" . This means that the report has been successfully delivered to the Federal Tax Service.

- "Error message" . Indicates that the tax authority received the document, but something went wrong when receiving it. This could be a problem with the shipping container, with decryption, and so on. When an error message is sent, the document flow for this report ends. To send it again, you need to read the text of the error. If necessary, it is recommended to contact the technical support of the EDF operator. When the error is resolved, the report is retransmitted.

How to cancel

If there are errors that cannot be corrected with one document (data was submitted to a namesake - the wrong employee), here’s how to correct the error in the SZV-TD report and cancel previously sent information:

- Duplicate the form with incorrect information.

- In the “Cancellation Sign” field, put an “X” (without quotes).

- Send the document to the FSS.

This will cancel the previously submitted document. After you have made a cancellation in the SZV-TD report for the employee, instead of whom the information was sent to another person (namesake), create and send a new (correct) form.

There are no differences between how to cancel a SZV-TD report in Kontur if you need to submit a new form or cancel without submitting new data, and how to cancel a SZV-TD report in VLSI: there are no special requirements for the software, you must fill it out correctly the form itself and send it to the Pension Fund.

If you encounter technical difficulties, we recommend contacting the support line of your software developer.

How to correct errors in RSV-1 now

The main sections of the updated declaration (1-7) are presented in the same form as the corresponding sections of the primary declaration, taking into account the changes made in the amount of tax subject to tax deduction (lines 120, 190 and 200 of section 3) (Fig. 14) and , therefore, the amount of tax payable to the budget (line 040 of section 1) (Fig. 13).

Put “0” if the clarification contains a new version of the purchase book, sales book and other applications.

If you do not need to send a new version of the application, then the Relevance Sign should be equal to 1 - the information is current.

Updated calculation of insurance premiums

An important criterion influencing the need to adjust the annual financial statements is the degree of materiality of the error, which is established by the company. In this case, the magnitude and nature of the error, as well as the size of the distortion of balance sheet items that followed it, are taken into account.

This is a report from the electronic document management operator that the form has been accepted by him. It indicates the date and time of dispatch (for all regions of Russia - Moscow, for the Kaliningrad region - local).

The corrective information is provided in the corrective form and incorrect information is excluded. When entering data, pay special attention to the preparation of section. 3. This sheet is not submitted to all employees, but only to those for whom corrections are made. All other pages that have already been submitted earlier are obligatory.

How to submit a corrective report SZV-TD

The employer submits the completed corrective form, as well as the primary one, to the Pension Fund of the Russian Federation in the established format. Companies and individual entrepreneurs with fewer than 25 employees can submit a paper version of the report. Other employers are required to submit the report electronically. For violation of the electronic form, a fine of 1000 rubles is provided (Part 4 of Article 17 of Law No. 27-FZ of 04/01/1996).

You can view a complete guide to personnel issues and the electronic work book for free in the ConsultantPlus system.