We recently wrote about how to correctly fill out KUDIR for those who use the simplified Income form. What do individual entrepreneurs fill out in other special modes? Individual entrepreneurs on UTII do not fill out any KUDIR, they must take into account only their physical indicators, by which the tax is calculated, but individual entrepreneurs on a patent are required to keep track of their income, not in the KUDIR, but in the income book. How to fill it out correctly? Read in this article.

The most convenient way to fill out KUDIR automatically, keep records and submit reports is in a special service.

Let's start, as always, with the general rules:

- The book is filled out in chronological order;

- Records are made positionally, the basis of the record is a specific primary document;

- Records are kept in Russian; if the attached documents include papers in a foreign language, they must have a translation;

- The book can be filled out in paper form, or you can first keep it in electronic format and then print it out;

- The document must be laced, numbered, sealed with the individual entrepreneur’s signature and seal, if any;

- If a correction is made, it must be justified (plus it must be confirmed by the signature of the individual entrepreneur.

Let us highlight one of the rules separately:

The book is opened for each patent; accordingly, it reflects the income related to the validity period of a particular patent. If you purchased a patent for a year, then there will be one book, if there are two patents, each for six months, then there will be two books, each for its own patent.

Now about how to fill out an income accounting book (or KUD).

It has a unified form approved by the Ministry of Finance of the Russian Federation, the same order of the financial department approves the KUDIR form for the simplified tax system and the procedures for filling out these forms. Here you can see and.

The form contains only a title page and one section where income is reflected. Expenses are not reflected in it at all, including contributions to funds - on a patent they cannot be deducted from the tax amount, so there is no point in showing them.

Purpose of the income ledger under the patent system

In accordance with Law No. 402-FZ, entrepreneurs are exempt from the need to maintain accounting records. Of course, this simplifies the company’s administrative paperwork, but does not eliminate the obligation to record revenue. According to paragraph 1 of Art. 346.53 of the Tax Code, accounting for sales income in terms of activities on the PSN is carried out in a special manner, namely in a special book, the form and procedure for filling which is regulated by the Ministry of Finance of the Russian Federation.

Certification of the book at the territorial office of the Federal Tax Service is not required, as is the preparation of tax returns (Article 346.52). However, despite the fact that when working on PSN, it is not the actual amount of income of an individual entrepreneur that is taken into account, but the conditionally possible one, maintaining KUDiR is necessary to comply with the revenue limits established by law. In 2021, those entrepreneurs whose total income does not exceed 60 million rubles have the right to work on a patent. from the beginning of the year (clause 6 of article 346.45). Business transactions when receiving income in terms of PSN are reflected in chronological order in the accounting book, which allows you to quickly check the amount of revenue for the current period.

How to keep a register

There are two acceptable ways to maintain a book of income on a patent:

- on paper sheets in the form of a bound book;

- electronic.

If you choose the first option, then after the patent ceases to be valid or the tax period ends, the merchant is obliged to submit this register to the Federal Tax Service, where it will be checked.

If we are talking about the electronic version, then they work with special files on the computer, where the individual entrepreneur types information about income. Under the same conditions as in the first case, it is necessary to print the document and submit it to the tax authority.

Regardless of whether the activities carried out by a merchant involve cooperation with foreign counterparties and clients, all records must be kept in Russian or must be translated into it.

If the entries were made in another language, then the translation is written in the next column. It is important that the entrepreneur certifies the adequacy of the translation using the date, stamp and signature. If it works without a seal, then an autograph and the corresponding date are enough.

The most important feature, which is also the main requirement that must be taken into account when maintaining a book, is strict adherence to chronological order. It is also important that the book is filled out without corrections and clearly. If the adjustment could not be avoided, then the reason must be indicated each time. But this is not enough: the fact that the accounting in the new way was correct must be confirmed by a financial receipt document signed by the individual entrepreneur.

Composition of the income book under the patent taxation system

According to Order No. 135n in 2021, the form of the income accounting book for individual entrepreneurs on a patent consists of section I, which includes 4 lines where the following are written:

- On pages 1-3 - mandatory details of primary financial documentation confirming the fact of a business transaction. This is, first of all, the date and number of cash orders, checks, payment requests and orders, account statements, invoices, BSO, contracts, etc. Page 1 indicates the number in order, page 2 – date/number of the document, page 3 – contents of the operation.

- Page 4 reflects the amount of income from the transaction in relation to the activity for which the patent is applied.

Important! If an entrepreneur applies two tax regimes - for example, the simplified tax system and the PSN, it is necessary to keep two different books to separate the accounting of business transactions. In this case, compiling one register is not allowed.

Income documents

The execution and receipt of a number of documents automatically gives a signal about the need to enter the next income position into the register. So, the following financial documents can confirm your arrival:

- agreements that stipulate the receipt of financial resources such as prepayment or advance payment;

- cash receipts orders;

- checks and payment orders;

- invoices for the transportation of goods (TTN, if this is income);

- financial documents of strict reporting.

Let's say a few words about the nuances that may arise with an advance payment. If the transaction is successful, the advance received is shown in the financial statements as profit. However, it may happen that later for some reason it had to be returned. Then the merchant proportionately reduces the profit received. The main thing is not to forget to make adjustments to the income book. Such cases are within the bounds of the law.

Income book for individual entrepreneurs on a patent - rules for filling out:

- For each tax period, a new book form is created - the period must correspond to the period of issue of the patent. If an entrepreneur receives a new patent instead of an old one, a new KUDiR is formed.

- It is allowed to compile a book in paper or electronic form. In the first case, you need to pre-stitch and number all the pages, certify the document with the signature of the individual entrepreneur and a seal, if available. If the reporting is prepared by computer, the certification of the bound and numbered book is carried out after printing.

- There is no need to register KUDiR with the Federal Tax Service.

- All transactions are reflected in the book by cash method - the procedure for recording income is defined in clause 2 of Art. 346.53, that is, as they are, so to speak, produced. We received the money and reflected it in the book.

- There is no need to enter expenses into the book, only income in rubles in chronological order.

- Correction of indicators is possible if supporting documents are available - errors and corrections are certified by the signature/seal of the individual entrepreneur.

Note! The absence of a book is interpreted as a gross violation of legislative requirements for the rules for accounting for income/expenses and threatens the entrepreneur with penalties of 10,000-30,000 rubles.

KUDiR for individual entrepreneurs on OSNO

The procedure for filling out the Book for individual entrepreneurs under the general taxation regime was approved by joint Order of the Ministry of Finance No. 86n and the Ministry of Taxes of Russia No. BG-3-04/430 dated 08/13/02.

We have prepared a sample document for the OSNO “Book of Expenses and Income of Individual Entrepreneurs”; you can download it for free at the end of the article.

The book of income and expenses for individual entrepreneurs on OSNO consists of a sheet with information about the individual entrepreneur, a sheet with contents and 6 sections:

- Accounting for income and expenses.

- Calculation of depreciation of fixed assets.

- Calculation of depreciation for small business enterprises not written off as of 01/01/2002.

- Calculation of depreciation of intangible assets.

- Calculation of accrued and paid wages.

- Determination of the tax base.

Several tables have been developed for each of them; they must be filled out for each type of activity separately.

The sheet “Information about the individual entrepreneur” indicates the registration data of the individual entrepreneur, his bank accounts, license numbers, cash register numbers, types of business activities, place of business, telephone numbers.

The “Contents” sheet lists all completed tables with page numbers.

6.1 reflects the summary data on the basis of which the declaration is filled out.

Book of accounting of income and expenses, sample of filling out section 6.1

KUDiR for individual entrepreneurs on the simplified tax system

The document for the simplified tax system is much simpler, and it is filled out not only by individual entrepreneurs, but also by organizations that use the simplified taxation system.

The book of income and expenses for the simplified tax system 2021 consists of a title page and 4 sections:

- Income and expenses.

- Accounting for the costs of acquiring fixed assets and intangible assets taken into account when determining the tax base.

- Calculation of the amount of loss that reduces the tax base under the simplified tax system.

- Expenses that reduce the amount of the calculated simplified tax system.

The title page indicates: name of the individual entrepreneur, INN, object of taxation, bank account details, tax period, OKPO code.

In section 1, the amounts of income are recorded in chronological order as payments are received from clients.

Sample of filling out KUDiR 2021 “income minus expenses” (hereinafter referred to as “D minus R”):

This is what section 1 of KUDiR 2021 of the simplified tax system looks like, you can find excel at the end of the article.

The last, 5th, column is filled out only for the simplified tax system with the taxable object “D minus R”.

The figures reflected in the first section of KUDiR are summed up quarterly on an accrual basis, and based on the data obtained, the taxable base for the simplified tax system is determined.

Sections 2 and 3 are filled out only with the simplified tax system “D minus R”.

Section 4 is filled out only for the object of taxation “Income”, it shows paid insurance premiums and other things determined by clause 3.1 of Article 346.21 of the Tax Code of the Russian Federation.

The amounts specified in section 4 reduce the amount of the accrued simplified tax system in full for individual entrepreneurs without employees and by no more than 50% if the individual entrepreneur makes payments of remuneration to individuals.

Responsibility for incorrect conduct of CUD

Russian legislation provides for liability for incorrect reporting or failure to provide reporting by business entities.

If supervisory authorities identify any violations in the activities of an entrepreneur related to incorrect or incomplete accounting of his commercial activities, then you can receive a fine of 10 thousand rubles per violation, and if repeated violations are detected, the fine may already amount to 30 thousand rubles This also applies to those who do not keep records of their business activities at all.

It follows from this that all commercial activities of business entities, including those under patents, are strictly controlled by law, and if you violate the current norms and rules, you can run into fines. Therefore, you need to be careful and responsible when filling out the CUD. To correctly fill out reports, you need to familiarize yourself with the rules and samples for filling out the CUD.

What is considered income when maintaining tax records on a patent?

When maintaining tax reporting for a business based on a patent, you should correctly record income. Let's look into the details of accounts in KUDiR, which is accepted as income for individual entrepreneurs:

- All profits of individual entrepreneurs on a patent are formed using the cash method; the procedure for fixing profits is defined in paragraph 2 of Art. 346.53. The cash accounting method means that only amounts received into the individual entrepreneur's current account or received at the cash desk can be included in the Book. It follows from this that if the services are provided within a certain period specified in the contract, and the money from the client has not yet arrived, the income is not reflected in the register. The planned income cannot be considered the profit of the individual entrepreneur.

- It should be clarified that the income of an individual entrepreneur is recognized not only as money received, but also as profit received in kind. In this option, income must be reflected in KUDiR on the day of transfer; such income is taken into account at the market price of inventory items. This is governed by Section 346.53(5) of the Code. Moreover, the market value of profits received in kind must be determined based on the provisions of Article 105.3 of the Tax Code of the Russian Federation.

- When a merchant using PSN receives income in foreign currency, he must recalculate the denomination at the official exchange rate of the Central Bank of the Russian Federation established at the time of receipt. This rule is also enshrined in paragraph 5 of Article 346.53 of the Tax Code of the Russian Federation.

- A separate issue is prepayment under contracts. Here you need to know that even money received into the account is not considered profit until the full amount specified in the agreement is received. This is regulated, which clearly states that all advances, as well as collateral and deposits cannot be classified as business income for accounting purposes.

- Often, individual entrepreneurs have questions regarding returned advances for services or goods. The answer here is clear: when the deal is terminated and the advance payment is returned to the customer (buyer), the amount that had to be returned is indicated in the revenue part of KUDiR. Only it is recorded with a negative indicator. Accordingly, the profit received decreases. Such steps are enshrined in regulations.

- Let's consider another important question: how can an entrepreneur in the patent regime enter data into KUDiR if he does not have cash register equipment (CCT). After all, there can be many such operations per day if an individual entrepreneur provides, for example, one-time services to the population. In accounting, it is the specific details of the primary account that are important, and not the fact that a certain operation was carried out. This means that an individual entrepreneur can take the form of a cash receipt order (CRO) as a basis or independently develop another document convenient for him. In this case, in column No. 3 KUDiR “Content of operation” you can put the wording “receipt of cash proceeds” and add a fifth column to the Book (“note / comments”), where you indicate specifics. By drawing up 2 PKOs, the first for the amount of profit received on strict reporting forms, the second - for the amount of cash received, the businessman will be able to correctly reflect his daily income in two documents. In the notes it will be necessary to list the numbers of all BSOs; when their number is significant, it is enough to indicate the numbering: “from No.... to No...”.

The commercial activity of an entrepreneur is a chain of compliance with clear algorithms prescribed in the Tax Code of the Russian Federation. To avoid questions and sanctions from tax authorities, it is recommended to strictly follow them. Fortunately, keeping business records using the patent taxation system is the minimum set of reporting requirements among all tax regimes, where the key link is the Income Accounting Book. Proper maintenance of this mandatory reporting document will protect the individual entrepreneur from fines.

Video: everything about the patent system

The conclusion is obvious: if the business of an individual entrepreneur applying the patent regime, without staff, bears a fairly light tax and insurance burden, then the reporting of the patent owner with his employees is heavy and labor-intensive. Any report that is not submitted on time may result in sanctions and financial penalties. In this regard, it is recommended to competently and constantly maintain an Income Book and be meticulous in all payment and reporting formalities of the individual entrepreneur. And remember: everything related to relationships with regulators is quite serious.

Shoals with a book

In case of violations and incorrect reporting on a patent, one can expect a negative reaction from the state represented by the tax authority. Therefore, the income ledger will be the main focus.

If a tax audit reveals gross violations and inaccuracies in filling out and maintaining a book, this may result in a fine. If we are talking about a single violation, then the size of the sanction is set at 10,000 rubles. When the rules for working with a book were violated or ignored repeatedly over a long period, the treasury will have to pay 30,000 rubles (clauses 1 and 2 of Article 120 of the Tax Code of the Russian Federation). The complete absence of an income accounting book or its ignorance formally also falls under this norm.

Therefore, individual entrepreneurs with a patent can be advised to pay special attention to maintaining and correctly filling out the income book.

Despite the fact that the use of the patent system falls as easily as possible on the shoulders of the entrepreneur, it also has its pitfalls. Therefore, it is better to know about all the pitfalls in advance in order to avoid unpleasant situations with tax inspectors and penalties. Be careful with the patent system, rely on legal norms. In this case, many mistakes can be avoided.

An example of filling out the PSN income book

What is an IP patent

An individual entrepreneur’s patent is permission from the tax office to engage in certain types of activities for a certain number of months. For example, a private hairdresser can buy a patent for 2-3 months in order to understand the demand for their services.

To buy an individual entrepreneur patent, you need to submit an application to the tax office at your place of business. The application indicates the type of activity and the period for which the patent is issued - from 1 to 12 months within one calendar year.

The application is submitted 10 working days before the patent begins to be valid. If you want to continue working for PSN, do not forget to submit a new application on time. An already issued patent cannot be renewed.

The validity of a patent is limited not only by its term, but also by the territory of the municipality indicated in the document. Moreover, the cost of a patent for the same type of activity in different localities will vary.

Fines

For violation of the deadlines for submitting completed reports, fines are imposed ranging from 10,000 rubles (for minor and one-time sins) and up to 30,000 (malicious violators). In addition to collecting penalties, a common method of persuading taxpayers on the part of the inspectorate is to block the bank account of an individual entrepreneur.

In addition to violating deadlines, sanctions may also apply for incorrect execution of forms and strict reporting forms. Minimum size 200 rubles.

In relation to an individual entrepreneur, sanctions for late submission of reports are varied:

- For personal income tax not transferred and not withheld from employee salaries, a 20% fine of the tax amount is inevitable.

- For each document (certificate, report, information document) not submitted on time, you will have to part with 200 rubles.

- For false data, another minus 500 rubles for each document.

- For falsification of reports there is a fine of 10,000.

For financial well-being, it is better to prevent all these cases and control the timing.

A patent for an individual entrepreneur will relieve him of the headache called “accounting and tax reporting.” If you don’t hire staff, then it’s enough to pay for the patent once and live in peace for the whole year. For employers, the requirements for taxes and contributions are more serious.

Filling out the income section, the tabular part of the CUD

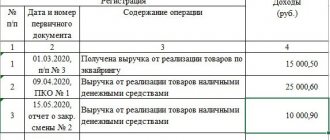

Individual entrepreneurs who are on the simplified patent taxation system fill out the following columns of the income accounting table, thus:

- the first column of the accounting table indicates the serial number of the business operation that is subject to accounting in the CUD;

- the second column of the accounting table indicates the number and date of the primary document, which will serve as the basis and confirmation of the completed business transaction;

- in the third column of the accounting table, the content of the business operation, which is subject to accounting in the CUD, is briefly described;

- the fourth column of the accounting table indicates income in rubles from the entrepreneurial economic activity of the individual entrepreneur, which clearly corresponds to the issued patent giving the right to such commercial activity.

Amounts of income in KUD are displayed only in whole rubles, without kopecks.

How to reflect income transactions based on how the income was received:

- When income is received in the current account of an individual entrepreneur, in the corresponding column of the accounting table we write the document basis payment order No. and the date of the document, if there were several payments for that day, then you can indicate as a document - the basis a bank statement for that day, also indicating its number and date;

- If the income was received through the cash register in cash, then you must indicate the date and number of the cash Z-report;

- If the income was received in cash but not through a cash register, then you need to draw up a receipt order - a standard PKO, indicating its date and number in the accounting book. If customers are issued sales receipts or other standard BSO, a receipt must also be issued for them.

The CUD can have as many lines as desired; the number of lines is equal to the number of business operations during the reporting period, which is limited by the validity period of the patent and the calendar year. At the end of the reporting period, the results need to be summed up in the reporting book. The book is then printed and stapled.

Filling procedure

The tabular form of maintaining the corresponding section of the book (and there is only one here) leaves practically no room for errors; it is only important to carefully fill out all its columns:

- record number in order;

- details of the accounting document (its number and date of issue);

- description of the income transaction (related to the receipt of any income by the entrepreneur);

- the amount of income received from the transaction specified in the previous section. The amount is indicated in Russian rubles. This section includes only those incomes that were received as a result of performing the activities for which the patent was issued.

Filling out the title page of the KUD

The title page must be filled out on a standard form in full accordance with the footnotes. The following information is required:

- For what reporting period are entries kept in the accounting book (for example, for 2021);

- Start date of maintaining the CUD;

- Full name of the entrepreneur;

- TIN of the entrepreneur;

- Full name of the subject of the Russian Federation that issued the patent to the entrepreneur;

- Specify the specific validity period of the patent, in the format “day.month.year”;

- The entrepreneur's place of residence;

- Bank details of the individual entrepreneur - current account number and name of the credit institution.

How to keep an accounting book: methods, procedures and rules for filling out, documents and accounting nuances

First, let's figure out what methods of conducting KUDiR exist. Actually, there are only two of them:

- The accounting book can be purchased in paper form or simply take the template and print it. You can download the form, as well as clarify the procedure for its execution, by going from the portal of the Federal Tax Service of the Russian Federation to the basic official website of the Consultant via hyperlink. Different download formats may be offered:

- PDF - for optimal filling by hand;

- Excel - for saving on a computer and maintaining KUDiR in electronic form.

- Maintaining the Account Book in electronic form is much more convenient. After all, here you can always correct inaccurate information, add or remove extra lines, etc. The only difference in this format is that at the end of the reporting period, for submission to the Federal Tax Service (at the request of the tax authorities), the document is printed, all pages are numbered. Then the Accounting Book is stitched according to standard rules and endorsed by the entrepreneur. If the individual entrepreneur has a seal, its imprint is placed next to the signature of the responsible person.

Entrepreneurs who fill out their Book by hand have the opportunity to make corrections to the document. But such adjustments must be properly executed:

- It is forbidden to use correctors or erase data with an eraser;

- incorrect data is simply crossed out, and the date of correction and the entrepreneur’s visa are placed next to it;

- clarification of data must be supported by original fiscal documents;

- Please note that the presence of a large number of corrections may raise legitimate questions among inspectors, so it is recommended to avoid them.

As we have already said, this document was approved by the Ministry of Finance, the exact name of the form is Appendix No. 3 to Order of the Ministry of Finance of the Russian Federation No. 135n dated October 22, 2012. Do not confuse this template with Appendix No. 1, which is intended to be maintained by simplifiers on the simplified tax system. The template for a business applying a patent is simpler; it does not contain data and sections unnecessary for the report.

In the KUDiR, which is filled out by individual entrepreneurs on PSN, only income is taken into account

Step-by-step instructions for filling out the KUDiR form

As for the form of the Register of Individual Entrepreneurs on a patent and the algorithm for filling it out, everything is elementary. The form contains only 2 sheets - the title page of KUDiR and Section I - Income. Let's figure out what data is entered into the document and how:

- The title page of the Book of Income Accounting for individual entrepreneurs applying the patent taxation system is drawn up at the moment when the received patent comes into force.

- in our case - from the beginning of 2021. If a work permit under PSN was received, for example, from April 1, you need to put the corresponding day of the year (18_04_01) in the “date” block. Please note that the date format is defined as reverse: the last two digits of the year are put first, then the month and only then the day;

- in the block identifying the individual payer, the full name of the entrepreneur is written (as indicated in the passport or extract from the Unified State Register of Entrepreneurs), the numbers of the individual entrepreneur’s business identifier are entered in the TIN line;

- Next come: the region in which permission to carry out commercial activities under the patent was received, as well as the period for which it was issued;

- Filling out the residence address of an individual entrepreneur is not difficult; here you need to write the address according to the requirements of the Ministry of Communications of the Russian Federation: with a zip code and other postal details;

- in the lower left block all current accounts issued to the businessman are indicated. First comes the code number, then the name and location of the credit institution;

- The code of the municipality (OKATO) can be clarified in a separate tax service using the link. Everything is quite simple there: just find in the drop-down list the code of the municipality where the business activity will be carried out;

- OKEI code - data from the all-Russian classifier of units of measurement. When filling out the Accounting Book in our version, it will always be the ruble code - 383.

The title page of KUDiR contains information about the individual entrepreneur on the PSN and the patent he received. - Filling out Section I, which reflects the entrepreneur’s income, should not raise any questions:

- the first column contains the serial number of the registered primary;

- then put the date and number of the primary document;

- the name of the transaction and the amount received from a specific payment by the client or counterparty;

- many do not take into account (and the format of this column is not configured in the tax template) that the amount of income should be indicated in rubles;

- if the form is maintained electronically, the final line of the template - “total” - sets the autosum;

- In this case, do not forget to immediately set up the footer, which should indicate the page numbering. In our case - No. 1, but if there are many receipts per month, KUDiR can stretch over several sheets. It is important that the numbering of the pages is reflected when printing; an unnumbered Book will not be accepted by the tax authorities;

- It is necessary to note one more important point that is worth knowing: the page numbering, according to the document flow standard, does not include the title page of the Book, so section No. 1 begins from the first page.

In section I KUDiR, when receiving income, all four columns are filled in; if there is no income, the fields are left empty - The final page of the Book (regardless of the format in which it was kept) indicates the total number of completed sheets. The electronic KUDiR is printed and endorsed by the entrepreneur. Moreover, the signature must be personal. A book that is not signed by the owner of the business may not be taken into account during the audit.

So, if everything is obvious according to the algorithm for designing the title page of KUDiR (see step-by-step instructions above), then when drawing up the first section of the accounting document you need to know certain formal requirements. They are as follows:

- The KUDiR must reflect all the actual business income of the individual entrepreneur on the patent, these include both receipts of money to the current account or cash register of the individual entrepreneur, and funds received in kind, as well as profits in foreign currency. What needs to be taken into account here is that profits earned from business activities not covered by a patent are not included in this Book.

- Business expenses are not reflected in this document, which is logical, because they are taken into account in the tax accounting of this regime (there is not even a column for this in KUDiR).

- All entries in the register are made strictly in chronological order. This rule is regulated in subparagraph 1.1 of Appendix No. 4 to Order of the Ministry of Finance of the Russian Federation No. 135n.

- When opening a new patent, a new accounting book is opened for each new reporting period (see paragraph 1.4 of the specified Appendix). If an individual entrepreneur receives a new patent to replace the expired old one, it is logical that a new Book begins to be maintained, since, according to paragraph 2 of Article 346.49 of the Tax Code of the Russian Federation, the reporting tax period is the period for which the patent permit was issued.

- All data is entered into KUDiR based on the primary data. The list of primary documentation is closed; only the following documents can be included here:

- originals of individual entrepreneur contracts with contractors or individuals;

- cash receipt orders;

- fiscal checks, payment orders;

- invoices reflecting profit (so-called TTN);

- strict reporting forms (SRF).

- The income accounting book is compiled in a single copy.

- The storage period for KUDiR is determined by tax legislation and, as for all tax reporting, is 4 years. If papers are destroyed or lost, fines may be imposed on the private enterprise.

- When the business of an individual entrepreneur extends, including to foreign counterparties (clients), the register must be kept strictly in Russian, all fiscal documents must be translated into Russian.

- All amounts are entered in the registrar in rubles and kopecks;

- Since the reporting period of PSN payers is 1 calendar year or (if the patent validity period is shorter) the period for which the PSN permit was issued, the Book is maintained on an accrual basis without defining intermediate reporting periods (month, quarter, half-year). This is the difference between the Book of PSN-payers and the registers of other taxation systems.

The regulator will not notice if minor errors are made during the registration of KUDiR. The key requirement here is that the register is maintained regularly and contains complete data on all completed individual entrepreneur operations.

Video: how to create separate individual income books for different patents in 1C

Reporting and payments of individual entrepreneurs with PSN with employees

If you involve employees in your business, the tax burden and the number of reports will increase significantly.

Particular difficulties for entrepreneurs are caused by the need to annually confirm the type of activity with the Federal Insurance Service (FSS). Every entrepreneur is required to do this by April 15 after the end of the current year.

| Frequency of presentation | Document submission deadlines | Place of delivery | |

| Income Journal | Once per period | At the end of the period | Tax |

| Information on the number of employees on staff | Once a year | Until January 20 | At the place of residence of the entrepreneur Tax |

| Help 2-NDFL | Once a year | Until April 1 | At the place of registration of the businessman Tax |

| Help 6-NDFL | Every quarter | Until 30.04 (Q1) Until 31.07 (1st half of the year) Until 31.10. (9 months) Until 31.01 (reporting year) | At the place of registration of the businessman Tax |

| Quarterly | Until the 20th day of the month following the reporting quarter | Social Insurance Fund | |

| Form SZV-M | Monthly | Until the 15th day of the month following the reporting month | Pension Fund |

| Calculation of insurance premiums | Quarterly | Until 30.04 (Q1) Until 31.07. (1st half of the year) Until 31.10. (9 months) Until 30.01 (reporting year) | At the place of registration of the businessman Tax |

| SZV-STAZH | Annually | Until March 1 of the year following the reporting year | Pension Fund |

In addition, immediately after the first employee appears in your company, you need to register with the Social Insurance Fund (you are given 10 days to do this) and the pension fund (you can visit the Pension Fund within 30 days).

As for payments, the entrepreneur and his employees must pay personal income tax and contributions to the Pension Fund and Social Insurance Fund. Personal income tax is paid monthly. In addition, immediately after the first employee appears in your company, you need to register with the Social Insurance Fund (you are given 10 days to do this) and the pension fund (you can visit the Pension Fund within 30 days). Also, reporting required to be submitted to the Pension Fund of Russia includes forms RSV-1, ADV-6-5 and SZV 6-4. They are rented quarterly.

In this case, information about employee income and withheld personal income tax must be provided to the Federal Tax Service at the place of registration of the individual entrepreneur. This information must be provided once a year by April 1st.